|

市場調查報告書

商品編碼

1940800

越南汽車租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Car Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

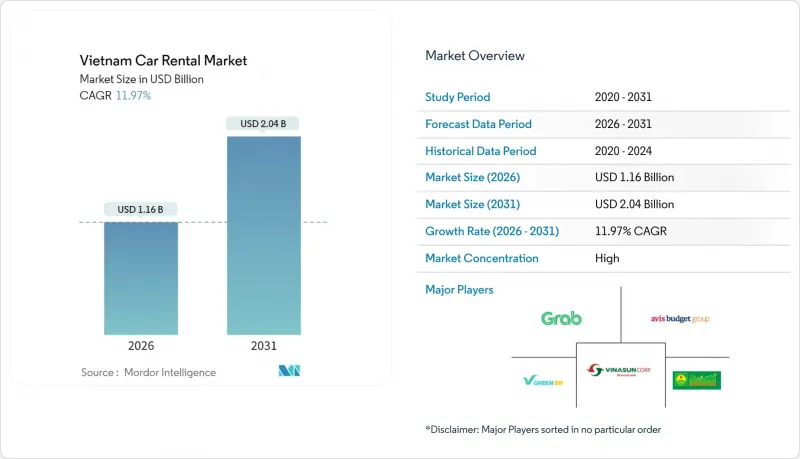

預計到 2026 年,越南汽車租賃市場規模將達到 11.6 億美元,高於 2025 年的 10.4 億美元。

預計到 2031 年將達到 20.4 億美元,2026 年至 2031 年的複合年成長率為 11.97%。

休閒和商務旅行的成長、快速的都市化以及政府的清潔旅行政策正在推動這一成長。 2024年最後四個月,國際入境旅客人數激增68.3%,國內旅遊支出也超過了疫情前水平,從而提振了短期租賃的需求。佔越南人口13%的中產階級可支配所得的增加,刺激了對高階自駕遊的需求。數位化透過線上平台簡化了預訂、支付和車輛運作流程,並提高了市場認知度,進一步推動了成長。最後,基於2027年之前免收車輛註冊費以及快速擴展的公共充電網路的電氣化舉措,正在創造一個獨特的競爭格局,使電動車服務和傳統租賃服務能夠並存發展。

越南汽車租賃市場趨勢及分析

旅遊業復甦帶動休閒租車需求成長

2024年1月至4月,國際觀光數量年增68.3%。休閒需求的激增直接體現在週末和假日預訂率上,這主要得益於自駕遊覽下龍灣、中部高原和湄公河三角洲的遊客數量增加。越南政府2025-2026年永續旅遊發展宣傳活動,以及租車公司車輛電氣化計劃,將消費者對環保出行方式的偏好與政策獎勵相結合。長期度假的增加和都市區家庭自駕遊文化的興起,支撐了全年需求。租車公司在旅遊旺季期間增加主要旅遊路線的車輛供應,並利用動態定價來應對季節性需求高峰。隨著旅遊需求的復甦,短期租賃車輛的運轉率率已恢復到疫情前的峰值水平,從而提高了每輛車的盈利。

中階可支配所得的增加

越南中產階級持續壯大,預計到2023年將佔總人口的13%,推動零售額在2024年初達到8.5%的年成長率。可支配收入的成長催生了對高階租賃車型(從SUV到豪華轎車)的新需求。消費者更重視車輛狀況、品牌聲望和禮賓級服務。日益成長的財富也讓週末短途用戶層成為主流休閒方式,自駕遊從偶爾的奢侈享受逐漸轉變為主流休閒休閒。為了實現差異化競爭,租車公司紛紛推出分級忠誠度計畫、智慧型手機解鎖服務以及兒童安全座椅等免費附加服務。儘管關稅高昂,但對豪華車的需求不斷成長,促使進口商提前推出高階車型,打造更多元化的車型陣容。最終,收入的成長將降低價格彈性,使營運商能夠在不降低需求的情況下,將關稅和車輛升級帶來的成本增加轉嫁給消費者。

主要城市交通擁擠及停車位短缺

胡志明市的通勤者每年因交通壅塞浪費大量時間,導致租車運轉率下降,燃油成本上升。停車位短缺,尤其是在第一郡和河內老城區,導致過夜停車費高昂,租車公司必須自行承擔或轉嫁這些費用。政策趨勢,例如河內提案於2030年禁止汽油動力車輛,也為車隊規劃帶來了不確定性。雖然未來的智慧交通系統(ITS)專案有望緩解這些壓力,但短期的交通堵塞應對措施迫使租車公司實施基於遠端資訊處理的路線規劃和延遲還車罰款條款。車輛調度延遲和額外的停車費降低了客戶滿意度,並促使價格敏感型用戶轉向其他出行方式。

細分市場分析

到2025年,線上通路將佔越南汽車租賃市場59.88%的佔有率,凸顯了該國向電子商務的快速轉型。超過160%的行動普及率使得旅客即使在取車前幾分鐘也能預訂車輛,而整合的電子錢包則加快了支付速度。該細分市場預計13.12%的複合年成長率反映了其便利性和成本效益。數位化平台降低了分店成本,並支援動態定價演算法,從而提高了運轉率。線下門市仍佔40.12%的佔有率,主要服務老年人和有特殊需求的企業客戶。然而,隨著客流量的下降,分店模式正面臨利潤壓力,迫使現有企業轉型為線上和線下融合的混合模式。

傳統租車公司透過門房服務和個人化行程規劃來維持客戶忠誠度,而線上新興企業則以限時折扣和用戶評價吸引價格敏感型客戶。隨著資料隱私和支付安全監管的日益嚴格,平台營運商致力於透過投資加密技術和合規認證來維護客戶信任。這種競爭促進了越南租車市場的發展,提升了服務品質、車輛透明度和行程後回饋機制。

預計到2025年,短期租賃將佔越南汽車租賃市場61.10%的佔有率,這主要得益於旅遊業的復甦和商務旅行的成長。週末旅客和商務旅客更傾向於按日計費,這樣可以避免擁有車輛、支付堵塞費和停車位短缺等諸多麻煩。在春節和統一日等公共假期期間,車輛使用量會達到高峰,迫使企業提前在機場和旅遊景點部署車輛。該細分市場預計年複合成長率將達到13.05%,這主要得益於越南旅遊業的成長,預計到2026年,越南的遊客數量將達到600萬人次,以及越南國內蓬勃發展的旅遊文化。

長期租賃業務佔比達38.90%,為營運商提供了穩定的收入來源。企業客戶、外籍人士和外交使團更傾向於簽訂包含全方位維護服務的月度契約,從而提高了預算的可預測性。 IFRS 16的實施加速了這項轉型,車隊正逐步轉向營業性租賃。為了保障車輛殘值,租賃服務商正在實施遠端資訊處理技術、監控里程限制並進行預防性維護。隨著外商直接投資的增加和工業園區的擴張,長期租賃需求正呈現出地理分散化趨勢,從傳統中心城市擴展到廣寧省和同奈省等其他省份。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 旅遊業復甦帶動休閒租賃需求

- 中階可支配所得的增加

- 向基於應用程式和線上預訂的轉變

- 透過綠色智慧運輸(GSM)促進電氣化

- IFRS 16實施後企業的車隊外包

- 政府主導的智慧運輸示範計劃

- 市場限制

- 低成本的叫車服務和摩托車的主導地位

- 高額汽車進口關稅和登記費

- 主要城市交通擁擠及停車位短缺

- 主要城市以外地區缺乏電動車充電網路

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方和消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 按預訂類型

- 線上

- 離線

- 按租賃期限

- 短期(少於30天)

- 長期(超過30天)

- 透過使用

- 旅遊休閒

- 日常通勤

- 企業和外派人員流動性

- 透過車輛推進系統

- 內燃機(ICE)

- 電池電動車(BEV)

- 混合動力電動車(HEV/PHEV)

- 最終用戶

- 個人

- 公司

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Vietnam Sun Corporation(Vinasun)

- Mai Linh Group

- Green & Smart Mobility JSC(GSM)

- Grab Holdings Inc.

- Gojek Vietnam

- Avis Budget Group

- Enterprise Holdings

- Hertz Corporation

- Sixt SE

- Saigon Car Rental Co. Ltd.

- Thuexe.vn

第7章 市場機會與未來展望

Vietnam car rental market size in 2026 is estimated at USD 1.16 billion, growing from 2025 value of USD 1.04 billion with 2031 projections showing USD 2.04 billion, growing at 11.97% CAGR over 2026-2031.

Growing leisure and business travel, rapid urbanization, and the government's clean-mobility agenda underpin this expansion. International arrivals jumped 68.3% during the last four months of 2024, and domestic tourism spending now exceeds pre-pandemic levels, lifting short-term rental volumes. Rising disposable incomes among Vietnam's 13%-strong middle class have spurred demand for premium, self-drive options. Digitization further fuels growth as online platforms streamline booking, payment, and fleet utilization while widening market visibility. Finally, the push for electrification-anchored by registration-fee waivers through 2027 and a rapidly scaling public charging network-creates a distinct competitive space where electric mobility services coexist with traditional rental offerings.

Vietnam Car Rental Market Trends and Insights

Tourism Rebound Drives Leisure Rentals

International visitor arrivals rose 68.3% during the first four months of 2024. The leisure surge translates directly into higher weekend and holiday bookings as travelers opt for self-drive journeys across Ha Long Bay, the Central Highlands, and the Mekong Delta. Vietnam's 2025-2026 national campaign for sustainable tourism dovetails with rental firms' plans to electrify fleets, aligning customer preference for eco-friendly choices with policy incentives. Extended public holidays and a growing culture of road trips among urban families sustain year-round demand. Rental operators increase fleet availability in peak vacation corridors, using dynamic pricing to capture seasonal spikes. As travel rebounds, occupancy ratios of short-term fleets have already returned to pre-pandemic peaks, lifting per-vehicle profitability.

Rising Disposable Incomes Among the Middle Class

Vietnam's middle class reached 13% of the population in 2023 and continues to expand, driving a retail sales increase of 8.5% year-on-year through early 2024. Higher disposable income unlocks new demand for premium rental categories-from SUVs to luxury sedans-where clients prioritize vehicle condition, brand cachet, and concierge-level service. Rising affluence also broadens the user base for weekend getaways, turning self-drive trips into mainstream recreation rather than occasional indulgence. To differentiate offerings, rental firms respond with tiered loyalty programs, smartphone-based vehicle unlock, and complimentary add-ons like child seats. Premium demand encourages importers to expedite the arrival of luxury models despite high tariffs, creating a more diverse fleet mix. Ultimately, income gains cushion price elasticity, allowing operators to pass on cost inflation from tariffs or fleet upgrades without eroding volumes.

Urban Congestion and Limited Parking in Major Cities

Ho Chi Minh City commuters lose more hours annually to congestion, eroding rental vehicle productivity and inflating fuel costs. Parking shortages, especially in District 1 and Hanoi's Old Quarter, lead to high overnight storage fees that operators must absorb or pass on. Policy moves such as Hanoi's proposed gasoline-vehicle restrictions from 2030 inject uncertainty about fleet composition planning. While the ITS program promises future relief, near-term congestion forces rental companies to adopt telematics-enabled routing and penalty clauses for late returns. Customer satisfaction suffers when pickups are delayed or parking surcharges appear, nudging price-sensitive users toward alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward App-Based and Online Bookings

- Government Smart-Mobility Sandbox Projects

- Sparse EV-Charging Network Outside Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online channels underpinned 59.88% of the Vietnam car rental market share in 2025, spotlighting the country's rapid pivot to e-commerce. Mobile penetration above 160% enables travelers to secure vehicles minutes before pickup, while integrated e-wallets accelerate checkout. The segment's anticipated 13.12% CAGR reflects convenience and cost efficiency, as digital platforms slash branch overheads and support dynamic pricing algorithms that lift utilization. Offline counters, holding 40.12%, still serve older demographics and corporate bookings requiring bespoke terms. Yet branch-based models face margin compression as foot traffic declines, prompting legacy firms to hybridize with click-and-collect services.

Traditional agencies leverage concierge experiences and personalized itinerary planning to retain loyalty, whereas online newcomers court price-sensitive segments with flash discounts and user-generated reviews. Platform operators invest in encryption and compliance certifications to preserve trust as regulatory frameworks around data privacy and payment security harden. The Vietnam car rental market benefits from this competition as service quality, fleet transparency, and post-trip feedback loops improve.

Short-term rentals controlled 61.10% of the Vietnam car rental market size in 2025, buoyed by tourism rebound and growing corporate travel. Weekend trippers and business visitors embrace day-based contracts that avoid the hassles of ownership, congestion charges, and parking scarcity. Utilization peaks during public holidays such as Tet and Reunification Day, compelling firms to pre-position vehicles at airports and tourist hotspots. The segment's 13.05% CAGR outlook remains tied to Vietnam's projected 6-million-visitor milestone in 2026 and robust domestic vacation culture.

Long-term rentals, with 38.90% share, anchor revenue stability for operators. Corporate clients, expats, and diplomatic missions favor monthly contracts bundled with full-service maintenance, enabling predictable budgeting. IFRS 16 accelerates the shift, pushing fleets toward operational leases. Providers deploy telematics to monitor mileage caps and preventative servicing, safeguarding residual value. As foreign direct investment climbs and manufacturing parks proliferate, long-term rental demand spreads from traditional centers into provinces such as Quang Ninh and Dong Nai, diversifying geographic exposure.

The Report Covers the Car Rental Industry in Vietnam. The Market is Segmented by Booking Type (Online and Offline), Rental Duration (Short-Term and Long-Term), Application Type (Tourism and Leisure, Daily Commuting and Corporate and Expat Mobility), Vehicle Propulsion (Internal Combustion Engine, and More), and by End-User (Individual and Corporate). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vietnam Sun Corporation (Vinasun)

- Mai Linh Group

- Green & Smart Mobility JSC (GSM)

- Grab Holdings Inc.

- Gojek Vietnam

- Avis Budget Group

- Enterprise Holdings

- Hertz Corporation

- Sixt SE

- Saigon Car Rental Co. Ltd.

- Thuexe.vn

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tourism Rebound Drives Leisure Rentals

- 4.2.2 Rising Disposable Incomes Among Middle Class

- 4.2.3 Shift Toward App-Based and Online Bookings

- 4.2.4 Electrification Push Via Green-and-Smart Mobility (GSM)

- 4.2.5 Corporate Fleet Outsourcing Post-IFRS 16

- 4.2.6 Government Smart-Mobility Sandbox Projects

- 4.3 Market Restraints

- 4.3.1 Dominance of Low-Cost Ride-Hailing and Motorbikes

- 4.3.2 High Vehicle Import Tariffs and Registration Fees

- 4.3.3 Urban Congestion and Limited Parking in Major Cities

- 4.3.4 Sparse EV-Charging Network Outside Tier-1 Cities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Booking Type

- 5.1.1 Online

- 5.1.2 Offline

- 5.2 By Rental Duration

- 5.2.1 Short-term (Less than 30 days)

- 5.2.2 Long-term (Above 30 days)

- 5.3 By Application Type

- 5.3.1 Tourism and Leisure

- 5.3.2 Daily Commuting

- 5.3.3 Corporate and Expat Mobility

- 5.4 By Vehicle Propulsion

- 5.4.1 Internal-Combustion Engine (ICE)

- 5.4.2 Battery-Electric Vehicle (BEV)

- 5.4.3 Hybrid Electric Vehicle (HEV/PHEV)

- 5.5 By End-user

- 5.5.1 Individual

- 5.5.2 Corporate

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Vietnam Sun Corporation (Vinasun)

- 6.4.2 Mai Linh Group

- 6.4.3 Green & Smart Mobility JSC (GSM)

- 6.4.4 Grab Holdings Inc.

- 6.4.5 Gojek Vietnam

- 6.4.6 Avis Budget Group

- 6.4.7 Enterprise Holdings

- 6.4.8 Hertz Corporation

- 6.4.9 Sixt SE

- 6.4.10 Saigon Car Rental Co. Ltd.

- 6.4.11 Thuexe.vn

7 Market Opportunities & Future Outlook

2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告

2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告 租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類)

租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類) 2026-2030年全球汽車租賃市場

2026-2030年全球汽車租賃市場 汽車租賃市場分析及預測(至2035年):依類型、產品類型、服務、技術、最終用戶、部署類型、用途、模式及功能分類

汽車租賃市場分析及預測(至2035年):依類型、產品類型、服務、技術、最終用戶、部署類型、用途、模式及功能分類 歐洲中中型卡車租賃:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)汽車租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲中中型卡車租賃:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)汽車租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 車輛租賃市場成長機會分析:全球,2024-2029年全球汽車租賃市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

車輛租賃市場成長機會分析:全球,2024-2029年全球汽車租賃市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本汽車租賃市場報告:按預訂類型、租賃期限、車輛類型、用途、最終用戶和地區分類(2026-2034 年)

日本汽車租賃市場報告:按預訂類型、租賃期限、車輛類型、用途、最終用戶和地區分類(2026-2034 年)