|

市場調查報告書

商品編碼

1939742

歐洲中中型卡車租賃:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Europe Medium And Heavy Duty Truck Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

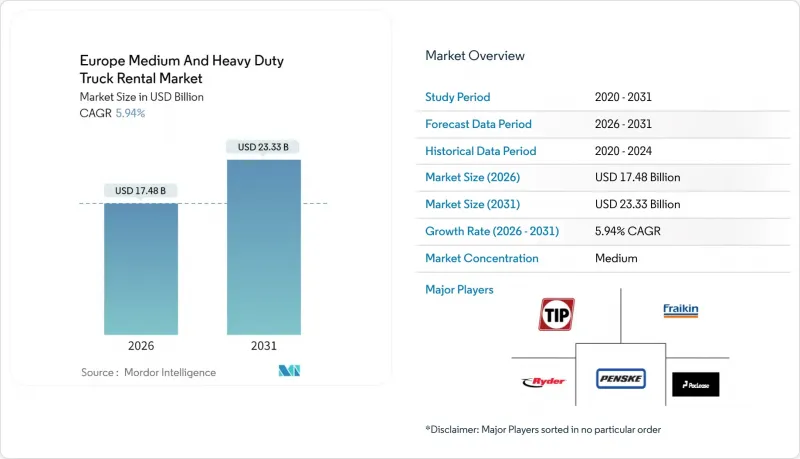

預計到 2026 年,歐洲中型和重型卡車租賃市場規模將達到 174.8 億美元。

這意味著從 2025 年的 165 億美元成長到 2031 年的 233.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.94%。

這項加速成長得益於電子商務貨運量的成長、更嚴格的排放氣體法規(有利於外包車隊)以及在高利率環境下對營運成本的關注。此外,數位化預訂平台的普及(縮短了交易時間並擴大了客戶覆蓋範圍)以及電氣化試點專案(降低了終端用戶的技術風險門檻)也進一步推動了成長。儘管重型車輛在歐洲主要走廊沿線仍佔據主導地位,以最大限度地提高運輸效率,但隨著都市區零排放區的擴大,人們對中型車輛和電動車的興趣也日益濃厚。

歐洲中中型卡車租賃市場趨勢及分析

電子商務主導彈性貨運能力激增

受線上零售蓬勃發展的推動,TIMOCOM現貨市場的貨物需求年增92%,預計2024年大部分時間裡,貨物需求與運力比將超過70%。貨運代理和第三方物流業者正依靠短期租賃來應對高峰需求,而無需增加永久性資產。僅在郵政和小包裹領域就以顯著的複合年成長率成長,給歐洲中中型卡車租賃市場的營運商帶來了運轉率壓力。零售商也利用租賃來試行新的區域樞紐,然後再投入資金,為車隊的柔軟性奠定了堅實的基礎。隨著2025年復活節移至4月,預計新一輪的緊急需求將進一步增強短期租賃的需求動能。

高利率週期中的成本規避重點

歐洲央行收緊貨幣政策,導致商用卡車融資成本在2025年初超過4%,年中回落至3.61%,但仍高於2022年之前的水準。因此,小規模車隊將租賃作為一種防禦性營運支出,以應對資產折舊。 2024年第四季,現貨運價格年增,燃油和碳排放稅額外費用的上漲進一步凸顯了浮動收費模式的合理性。中型卡車用戶將感受到最顯著的變化,因為殘值不確定性加劇了資金籌措風險。可變期限合約和市場定價模式目前支援眾多自有品牌分銷網路,從而擴大了歐洲中型和重型卡車租賃市場供應商的潛在客戶群。

柴油資產殘值波動

到2025年中期,2023款和2021款二手重型卡車的價格有所下降,凸顯了即將到來的排放氣體法規帶來的貶值風險。如果柴油車的貶值速度超過車隊預定的更新週期,依賴二手市場進行車隊更新的租賃公司將面臨利潤率壓縮。儘管營運商透過縮短持有期和實現動力系統配置多樣化來規避風險,但整車更換仍然是資本密集的。加速折舊免稅額進一步抑制了傳統的車輛所有權模式,間接推高了租賃需求。然而,這也縮小了擁有大量柴油車庫存的租賃公司的利潤來源。

細分市場分析

即使到了2025年,線下通路仍將佔據歐洲中中型卡車租賃市場72.48%的佔有率,因為基於關係的長期租賃合約仍然佔據主導地位。然而,受客戶對全天候自助服務平台、透明收費系統和即時車輛查詢的偏好驅動,線上平台正以7.77%的複合年成長率快速擴張。租賃業者正在採用整合API將庫存資訊與托運人的運輸管理系統同步,從而將人工報價週期從數小時縮短至數分鐘。訂閱收費系統、電子文檔簽名和內建保險選項進一步提升了平台的易用性。

線上預訂的成長加劇了競爭格局的複雜性。數位化原生平台利用低交易成本,觸及了以往由本地代理商服務的規模小規模的運輸公司。同時,現有企業正透過全通路策略應對,將標準車輛的自助預訂與複雜計劃的人工客戶管理結合。因此,歐洲中中型卡車租賃市場呈現雙軌模式:大量短期需求轉向線上,而客製化合約仍在線下進行。在預測期內,數位化帶來的更高透明度將推動車隊運轉率的提升,從而在無需相應增加資產的情況下創造過剩運力。

長期租賃預計將在2025年佔據歐洲中中型卡車租賃市場61.72%的佔有率,對於路線可預測的托運人來說,長期租賃具有規模經濟效益,且每日成本更低。同時,短期合約以8.49%的複合年成長率成長,在那些存在季節性需求高峰、企劃為基礎工作或電子商務需求突然成長的行業中蓬勃發展。雖然短期合約的柔軟性溢價可能高達15-20%,但托運人願意接受這一價格差異,以避免車輛閒置的風險。

由於預計遵守歐7排放標準的成本將會增加,越來越多的業者選擇試用新一代車輛,導致短期租賃交易量激增。租賃公司正在採用動態定價演算法,以在假日和收穫季節等需求高峰期最大限度地利用有限的運力來提高收入,從而提高單車收益。同時,長期合約提供了穩定的現金流,以支持車隊擴張的資本投資。平衡這些收入來源需要可靠的需求預測和資產重新配置策略,而建立分析能力是歐洲中型重型卡車租賃市場競爭優勢的關鍵。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 電子商務主導彈性貨運能力快速成長

- 在高利率週期中,應著重於成本規避。

- 更嚴格的歐盟7排放標準使得租車比買車更有優勢。

- 補貼型電動卡車試點計畫可降低租賃普及風險

- 原始設備製造商推出“卡車即服務”

- 跨境碳課稅加劇了季節性需求波動

- 市場限制

- 柴油資產殘值波動

- 由於駕駛人,服務運轉率。

- 充電樁併網延遲

- 數位貨運平台的輕資產競爭

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(金額)

- 按預訂類型

- 線下預訂

- 線上預訂

- 按租賃類型

- 短期租賃

- 長期租賃

- 按卡車級別

- 中型(7.5-16噸)

- 重型(超過16噸)

- 按最終用戶行業分類

- 普通貨物和第三方物流

- 建築和基礎設施

- 零售和快速消費品(FMCG)

- 郵政、小包裹與電子商務

- 廢棄物和市政服務

- 依推進類型

- 柴油引擎

- 電池式電動車

- LNG/CNG

- 混合

- 按國家/地區

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 波蘭

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- TIP Group

- Fraikin SAS

- Ryder System Inc.

- Penske Truck Leasing

- PACCAR Leasing Company

- Heisterkamp Transportation Solutions

- Easy Rent Truck & Trailer GmbH

- Mercedes-Benz CharterWay

- Scania Group

- Scania Group

- SIXT SE

- Enterprise Flex-E-Rent

- Dawsongroup Truck & Trailer

- Dawsongroup Truck & Trailer

- DKV Mobility

第7章 市場機會與未來展望

Europe Medium & Heavy-Duty Truck Rental market size in 2026 is estimated at USD 17.48 billion, growing from 2025 value of USD 16.50 billion with 2031 projections showing USD 23.33 billion, growing at 5.94% CAGR over 2026-2031.

This acceleration rests on rising e-commerce freight volumes, stringent emissions policy that favors outsourced fleets, and a preference for operating-expense models during an elevated interest-rate climate. Growth is further amplified by digital booking platforms that compress transaction times and broaden customer reach, while electrification pilots reduce technology-risk barriers for end users. Heavy-duty vehicles dominate demand because they maximize payload economics on core European corridors, yet medium-duty and electric options are gaining attention as cities expand zero-emission zones.

Europe Medium And Heavy Duty Truck Rental Market Trends and Insights

E-Commerce-Led Surge in Flexible Freight Capacity

Intensified online retail has lifted freight offers on the TIMOCOM spot marketplace by 92% year-over-year, pushing the freight-to-capacity ratio past 70% for most of 2024 . Carriers and 3PLs lean on short-term rentals to absorb peak season spikes without adding permanent assets. The postal and parcel segment alone is expanding at a notable CAGR, a pace that tightens utilization for every Europe Medium & Heavy-Duty Truck Rental market operator. Retailers also use rentals to pilot new regional hubs before committing capital, supporting a structurally higher baseline for fleet flexibility. As Easter shifts to April in 2025, a fresh swell of ad-hoc demand is expected to reinforce short-term leasing's momentum.

Cost-Avoidance Focus Amid High Interest-Rate Cycle

European Central Bank tightening pushed corporate truck loan costs above 4% in early 2025 before easing to 3.61% mid-year, levels that still exceed pre-2022 norms . Smaller fleets, therefore, treat rentals as a defensive operating expense hedge against asset depreciation. Spot transport prices climbed year-over-year in Q4 2024, an uptick driven by fuel and carbon surcharges that further validate variable-cost models. Medium-duty users exhibit the sharpest shift as residual-value uncertainty compounds financing risk. Variable-term contracts and marketplace pricing now underpin many private-label distribution networks, broadening the addressable pool for Europe's Medium & Heavy-Duty Truck Rental market providers.

Residual-Value Volatility of Diesel Assets

Used heavy-duty truck prices slid in 2023 model-year units and 2021 models by mid-2025, underscoring the depreciation risk tied to looming emissions regulations. Rental companies that rely on resale markets to refresh fleets face compressed margins when diesel values sag faster than scheduled de-fleet cycles allow. Operators adopt shorter holding periods and hedge with diversified propulsion mixes, yet outright replacement remains capital-intensive. Accelerated depreciation further deters traditional ownership, indirectly expanding rental demand; however, it simultaneously tightens profit pools for rental providers that maintain large diesel inventories.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Euro 7 Norms Favoring Rental Over Ownership

- Subsidized E-Truck Pilots De-Risking Rental Adoption

- Driver Shortages Limiting Utilization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Offline channels still controlled 72.48% of the European Medium & Heavy-Duty Truck Rental market share in 2025, as relationship-based contracts remain the norm for long-term leasing. Nevertheless, online portals are scaling quickly at a 7.77% CAGR as customers prefer 24/7 self-service dashboards, transparent rates, and instantaneous vehicle availability. Rental operators deploy integrated APIs that sync inventory with shipper transportation-management systems, reducing manual quote cycles from hours to minutes. Subscription-style pricing, digital document signatures, and embedded insurance options further reinforce platform convenience.

The growth of online booking also sharpens competitive boundaries: digital-native platforms leverage lower transaction costs to reach small haulers historically served by local agencies. Legacy firms counter with omnichannel strategies that blend self-service ordering for standardized units and human account management for complex projects. As a result, the European Medium & Heavy-Duty Truck Rental market witnesses a twin-track model in which high-volume short-term demand migrates online while bespoke contracts persist offline. Over the forecast window, digital engagement is expected to raise fleet utilization through better visibility, thereby unlocking capacity without proportional asset growth.

Long-term leasing controlled 61.72% of the European Medium & Heavy-Duty Truck Rental market share in 2025 and enjoys economies of scale that keep daily costs low for shippers with predictable routes. Yet short-term contracts, expanding at 8.49% CAGR, flourish in industries characterized by seasonal peaks, project-based work, or rapid e-commerce surges. The flexibility premium can reach 15-20% over equivalent long-term day rates, but shippers willingly absorb that markup to sidestep idle-fleet risk.

As Euro 7 compliance costs loom, more operators opt for trial periods with next-generation vehicles, a dynamic that feeds short-term leasing pipelines. Rental companies employ dynamic pricing algorithms to maximize yield on scarce capacity during holiday or harvest surges, widening revenue per unit. Conversely, long-term deals contribute stable cash flows, underpinning fleet-expansion capex. Balancing these streams requires robust demand forecasting and asset re-allocation strategies, cementing analytics as a competitive differentiator across the European Medium & Heavy-Duty Truck Rental market.

The Europe Medium & Heavy-Duty Truck Rental Market Report is Segmented by Booking Type (Offline Booking and Online Booking), Rental Type (Short-Term Leasing and Long-Term Leasing), Truck Class (Medium-Duty (7. 5-16t) and Heavy-Duty (Above 16t)), End-User Industry (General Freight and 3PL, Construction and Infrastructure, and More), Propulsion Type, and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- TIP Group

- Fraikin SAS

- Ryder System Inc.

- Penske Truck Leasing

- PACCAR Leasing Company

- Heisterkamp Transportation Solutions

- Easy Rent Truck & Trailer GmbH

- Mercedes-Benz CharterWay

- Scania Group

- Scania Group

- SIXT SE

- Enterprise Flex-E-Rent

- Dawsongroup Truck & Trailer

- Dawsongroup Truck & Trailer

- DKV Mobility

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce-Led Surge in Flexible Freight Capacity

- 4.2.2 Cost-Avoidance Focus Amid High Interest-Rate Cycle

- 4.2.3 Stricter Euro 7 Norms Favoring Rental Over Ownership

- 4.2.4 Subsidized E-Truck Pilots De-Risking Rental Adoption

- 4.2.5 OEM "Truck-as-a-Service" Roll-Outs

- 4.2.6 Cross-Border Carbon Tolls Amplifying Seasonal Demand Swings

- 4.3 Market Restraints

- 4.3.1 Residual-Value Volatility of Diesel Assets

- 4.3.2 Driver Shortages Limiting Utilization

- 4.3.3 Grid-Connection Delays for Depot Chargers

- 4.3.4 Digital Freight Platforms' Asset-Light Competition

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Booking Type

- 5.1.1 Offline Booking

- 5.1.2 Online Booking

- 5.2 By Rental Type

- 5.2.1 Short-term Leasing

- 5.2.2 Long-term Leasing

- 5.3 By Truck Class

- 5.3.1 Medium-Duty (7.5-16 t)

- 5.3.2 Heavy-Duty (Above 16 t)

- 5.4 By End-user Industry

- 5.4.1 General Freight and 3PL

- 5.4.2 Construction and Infrastructure

- 5.4.3 Retail and FMCG

- 5.4.4 Postal, Parcel and E-commerce

- 5.4.5 Waste and Municipal Services

- 5.5 By Propulsion Type

- 5.5.1 Diesel

- 5.5.2 Battery-Electric

- 5.5.3 LNG / CNG

- 5.5.4 Hybrid

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Spain

- 5.6.5 Italy

- 5.6.6 Netherlands

- 5.6.7 Poland

- 5.6.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 TIP Group

- 6.4.2 Fraikin SAS

- 6.4.3 Ryder System Inc.

- 6.4.4 Penske Truck Leasing

- 6.4.5 PACCAR Leasing Company

- 6.4.6 Heisterkamp Transportation Solutions

- 6.4.7 Easy Rent Truck & Trailer GmbH

- 6.4.8 Mercedes-Benz CharterWay

- 6.4.9 Scania Group

- 6.4.10 Scania Group

- 6.4.11 SIXT SE

- 6.4.12 Enterprise Flex-E-Rent

- 6.4.13 Dawsongroup Truck & Trailer

- 6.4.14 Dawsongroup Truck & Trailer

- 6.4.15 DKV Mobility

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告

2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告 租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類)

租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類) 2026-2030年全球汽車租賃市場

2026-2030年全球汽車租賃市場 汽車租賃市場分析及預測(至2035年):依類型、產品類型、服務、技術、最終用戶、部署類型、用途、模式及功能分類

汽車租賃市場分析及預測(至2035年):依類型、產品類型、服務、技術、最終用戶、部署類型、用途、模式及功能分類 汽車租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南汽車租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南汽車租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 車輛租賃市場成長機會分析:全球,2024-2029年全球汽車租賃市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

車輛租賃市場成長機會分析:全球,2024-2029年全球汽車租賃市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本汽車租賃市場報告:按預訂類型、租賃期限、車輛類型、用途、最終用戶和地區分類(2026-2034 年)

日本汽車租賃市場報告:按預訂類型、租賃期限、車輛類型、用途、最終用戶和地區分類(2026-2034 年)