|

市場調查報告書

商品編碼

1937273

汽車租賃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Car Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

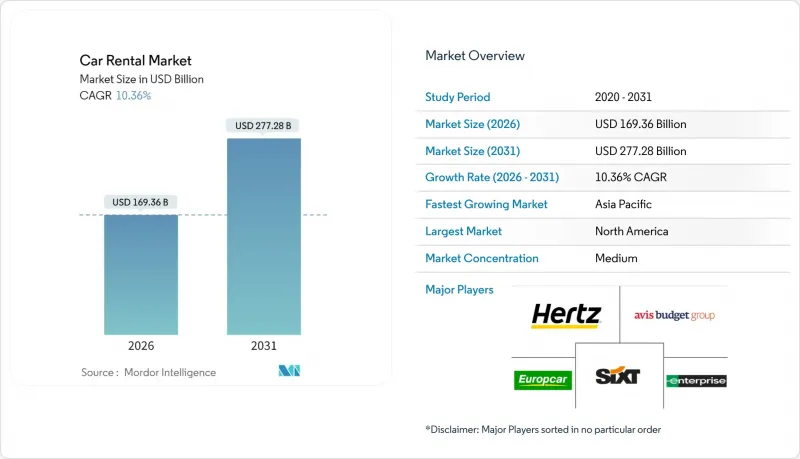

2025年汽車租賃市場價值1534.7億美元,預計到2031年將達到2772.8億美元,高於2026年的1693.6億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 10.36%。

這一成長軌跡表明,市場已從疫情引發的低迷中穩步復甦。新興經濟體可支配收入的成長、機場基礎設施的持續擴張以及數位化預訂管道的普及,都在推動持續的需求。營運商正利用動態定價引擎,結合航班到達、高速公路擁塞和當地活動等數據,來促進收入成長。曾經被視為次要參與者的點對點平台,如今正加強安全保障和忠誠度獎勵,以吸引更多房東加入其生態系統。儘管車輛電氣化仍不均衡,但企業永續性措施正穩步推動低排放車型的採購,即便一些老牌企業出現了高額減記。

全球汽車租賃市場趨勢與洞察

疫情後休閒旅遊業迅速復甦

休閒旅客數量已超過新冠疫情前的峰值,美國運輸安全局的安檢數量同比增幅不到十分之一,歐洲機場也出現了類似的成長。更高的客座率直接轉化為更高的租車櫃檯吞吐量,尤其是在週末,混合辦公模式允許旅客停留更長時間。旅客傾向於提前預訂並延長租車期限,這為以每日利用率目標為導向的營運商帶來了更高的單筆交易收入。 「Breezea」旅行模式將商務和休閒結合,由於高階主管增加了私人旅遊日,平均租車期限也隨之延長。公司會議的常態化推高了工作日的需求密度,使車隊負責人能夠更平衡地分配一週的車輛資源。儘管車隊運力增加,但美國運通全球商務旅遊預測,到2025年,美國每日租車價格仍將小幅上漲,價格韌性仍顯著。

線上和行動預訂平台的滲透率不斷提高

隨著數位化管道重塑客戶獲取方式,Avis Budget Group 的雲端原生定價系統能夠快速為忠誠會員量身打造專屬優惠。行動應用簡化了辦理入住流程,促進了保險提升銷售,並支援一鍵延時,從而縮短了櫃檯等待時間。流暢的支付流程鼓勵交叉銷售道路救援系統和通行費套餐,提高了輔助服務的使用率。在部分城市,Uber 用戶現在可以直接透過 Uber 應用程式預訂 Turo 車輛,實現了兩個平台的無縫整合。此舉以極低的成本將數百萬月有效用戶引入 Turo 租車管道。預測分析收集點選流和航班數據,最佳化城市間的需求曲線,使營運商能夠在需求高峰到來之前重新調整庫存。

共乘和汽車共享替代方案的興起

隨著基於應用程式的叫車服務在地面交通支出中主導,Uber 和 Lyft 等平台主導城市交通,傳統租車業務正在衰落。叫車服務因其價格透明、無現金支付以及「禮賓司機」服務對飽受交通堵塞和停車難題困擾的城市遊客的吸引力而日益流行。P2P平台正在形成新的競爭格局。這些模式規避了機場特許經營費,因此可以收取更低的標價。傳統業者正透過設立優先登機通道和白牌合作關係來應對,以期重奪在城市中心的市場佔有率。然而,都市區日租車業務仍面臨著來自按需出行方式的結構性壓力。

細分市場分析

截至2025年,線下平台佔據了汽車租賃市場54.12%的佔有率。同時,預計線上平台在預測期(2026-2031年)內將以10.42%的強勁複合年成長率成長。這種格局的變化正在削弱傳統實體門市的影響力,但矛盾的是,它也促使一些中型品牌拓展其全球業務。對於會員而言,便利性顯而易見:預先填寫的個人資料和安全的行動鑰匙讓客戶可以完全繞過櫃檯,簡化流程。此外,推播通知功能可告知客戶航班延誤狀況,方便客戶輕鬆調整取車時間,進而提升整體滿意度。在智慧型手機普及率較低的地區,線下實體店體驗仍然發揮作用,但由於人員配備和設施成本較高,預訂成本也較高。

Digital Traffic 正在加強與航空公司應用程式、飯店平台和第三方線上旅行社的合作,以推動旅遊方案的交叉銷售。這種整合降低了獲客成本,並透過配套服務開闢了新的收入來源。此外,這些交易產生的數據資源為車隊負責人提供了預測城際需求的洞察,從而實現車輛的及時調度並減少閒置天數。因此,在租車行業中,那些採用 API 優先策略的營運商在利用率指標方面顯著優於競爭對手。

根據體驗式旅遊趨勢,預計到2025年,休閒旅客將佔汽車租賃市場55.68%的佔有率,並在預測期(2026-2031年)內維持10.45%的複合年成長率。規劃多城市自駕遊的家庭重視車輛的自由度和行李的柔軟性,而這些正是團體旅行所缺乏的。疫情期間推出的非接觸式取車方式因其便利性而備受歡迎,乘客可以避免擁擠的接駁巴士,直接從行李提取處前往停車場。高燃油效率和寬敞的貨物空間也是休閒旅客關注的重點,推動了跨界車型的銷售。

商務旅行量正在恢復到2019年的水平,混合辦公模式讓員工有更多帶薪休假時間,從而延長了平均租期。這種商務與休閒結合的模式支撐了工作日和週末的需求,使收入曲線趨於平緩。具備整合排放報告功能的可程式設計企業帳戶有助於吸引注重永續性發展的公司,即使商務旅行量趨於平穩,也能增強需求的韌性。

區域分析

到2025年,北美將佔據全球租車市場35.02%的佔有率,反映出該地區成熟的旅行基礎設施和強大的汽車擁有文化。 Avis Budget Group在2023年實現了120億美元的營收,主要得益於機場客流量的復甦和忠誠度計畫續訂率的提高。其動態定價引擎利用航班延誤資料來捕捉最後一刻的預訂需求。雖然在缺乏充電基礎設施的鄉村州際公路沿線地區,電動車的普及率仍然有限,但紐約和洛杉磯等城市中心已開始強制要求低排放車輛。儘管在以共乘平台為主導的都市區走廊地帶競爭日益激烈,但租車仍然是單程州際旅行的主要交通方式。

預計亞太地區在預測期(2026-2031年)將以10.62%的複合年成長率成長。中產階級日益成長的旅行需求、落地簽政策以及強勁的航空座位成長正在推動市場發展。 Enterprise Mobility正積極拓展其網路,計劃於2024年在泰國開設10分店,目前在日本擁有97個服務點。印尼、越南和印度的入境旅遊人數均實現了兩位數成長,由於公共運輸能力緊張,遊客紛紛轉向自駕遊。中國電動車製造商正透過與租賃公司合作,以折扣價提供電動跨界車,進軍旅遊市場,以低成本的方式提升國際品牌知名度。

歐洲是一個成熟但競爭異常激烈的市場。 SIXT與Stellantis簽訂的多年期25萬輛汽車供應契約,在半導體短缺的情況下確保了供應,並推進了該公司的電氣化藍圖。阿姆斯特丹計劃於2025年設立零排放區,促使營運商為電動車預留高價值停車位。歐洲大陸內部邊境的開放擴大了跨境汽車租賃業務,但道路收費系統的差異使車輛追蹤變得複雜。 Europcar重返美國市場,並在亞特蘭大和達拉斯設立基地,顯示其對跨大西洋業務的興趣重燃。同時,拉丁美洲和中東地區受益於高速公路網路的改善以及沙烏地阿拉伯「2030願景」等旅遊推廣活動的推動,但貨幣波動和進口限制要求企業靈活配置資金。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 疫情後休閒旅遊業迅速復甦

- 線上和行動預訂平台的滲透率不斷提高

- 廉價航空的擴張創造了多模態需求。

- 企業ESG政策加速電動租車車隊的普及

- 利用數據驅動的動態定價工具提高運轉率

- 新興市場機場基礎設施升級

- 市場限制

- 叫車和共享汽車等出行方式越來越普遍。

- 快速的電動車技術迭代週期增加了殘值風險

- 機場收費給營運商利潤率帶來壓力。

- 都市區內燃機車輛的上限

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模及成長預測(金額)

- 透過預約方式

- 離線

- 線上

- 透過使用

- 休閒

- 商業

- 最終用戶

- 自駕遊個人

- 專車接送服務

- 企業車隊訂閱

- P2P租賃

- 按車輛類型

- 緊湊型/經濟型轎車

- 小型車和中型車

- 標準尺寸和全尺寸汽車

- SUV 和 MPV

- 豪華/高級汽車

- 按租賃期限

- 短期

- 中期

- 長期

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 其他歐洲

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Avis Budget Group Inc.

- Hertz Global Holdings Inc.

- Enterprise Holdings Inc.

- Europcar Mobility Group

- Sixt SE

- Localiza Rent a Car SA

- ALD Automotive

- Beijing CAR Inc.(CAR Inc.)

- GIG Car Share

- Lyft Rental

- Uber Rentals

- Silvercar by Audi

- Getaround

- Zoomcar

- Ola Drive

- Fast Rent A Car

- Bettercar Rental

- TT Car Transit

- Renault Eurodrive

- Shenzhen Supreme Car Rental Co., Ltd.

第7章 市場機會與未來展望

The Car Rental Market was valued at USD 153.47 billion in 2025 and estimated to grow from USD 169.36 billion in 2026 to reach USD 277.28 billion by 2031, at a CAGR of 10.36% during the forecast period (2026-2031).

This trajectory confirms the sector's decisive rebound from its pandemic trough. Rising disposable income in emerging economies, continued airport infrastructure upgrades, and wider access to digital booking channels are steering sustained demand. Operators are capturing incremental revenue by matching dynamic pricing engines with data on flight arrivals, highway congestion, and local events. Peer-to-peer platforms, once considered fringe, have doubled down on safety guarantees and loyalty perks, drawing new hosts into the ecosystem. Fleet electrification remains uneven, yet corporate sustainability mandates have ensured steady procurement of low-emission models despite headline-grabbing write-downs at some incumbents.

Global Car Rental Market Trends and Insights

Rapid Rebound Of Post-Pandemic Leisure Travel

Leisure passenger volumes have eclipsed pre-covid peaks, with U.S. Transportation Security Administration screenings up less than one-tenth year over year and mirrored surges seen at European airports. Higher seat factors translate directly into stronger rental counter throughput, particularly on weekends when hybrid work allows extended stays. Travelers are booking earlier and keeping cars longer, a pattern that lifts revenue per transaction for operators employing day-based utilization targets. Bleisure trips lengthen average rental duration as executives tack on personal days. Normalizing corporate meetings add weekday demand density, allowing fleet planners to deploy assets more evenly through the week. Price resilience remains evident, with American Express Global Business Travel forecasting U.S. daily rates to inch up slightly across 2025 despite rising fleet capacity.

Growing Penetration Of Online And Mobile Booking Platforms

As digital channels redefine customer acquisition, Avis Budget Group's cloud-native pricing system swiftly tailors offers for its loyalty members. Mobile apps streamline check-in, upsell insurance, and permit mid-trip extensions with one tap, shrinking counter dwell time. Seamless payment flows encourage cross-selling roadside assistance, toll packages, and lifting attachment rates. Uber riders in select cities can now reserve Turo vehicles directly through the Uber app, seamlessly integrating the two platforms. This move channels millions of monthly active users into Turo's rental funnel, all at a marginal cost. Predictive analytics harvests clickstream and flight data to refine city-pair demand curves, allowing operators to rebalance inventory before peak surges hit.

Popularity Of Ride-Hailing And Car-Sharing Substitutes

App-based rides are taking the lead in ground transport spending, with platforms like Uber and Lyft dominating urban travel, marking a decline for traditional rentals. Fare transparency, cashless payment, and driver-as-concierge appeal to city visitors reluctant to navigate traffic and parking. Peer-to-peer platforms layer another competitive vector: These models dodge airport concession fees, allowing lower headline prices. Traditional operators have responded with fast-pass pick-up lanes and entering white-label partnerships to regain relevance in downtown corridors. Nonetheless, urban day rentals continue to face structural pressure from on-demand alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Low-Cost Airlines Creating Multi-Modal Travel Demand

- Corporate ESG Mandates Accelerating Adoption Of EV Rental Fleets

- Rising Residual-Value Risk Amid Rapid EV Technology Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, offline platforms commanded a 54.12% share of the car rental market. Meanwhile, online platforms are projected to experience a robust growth rate of 10.42% CAGR during the forecast period (2026-2031). This evolving landscape has diminished the prominence of traditional brick-and-mortar counters, yet paradoxically broadened the global reach of even mid-tier brands. The convenience is palpable for loyalty members: pre-populated profiles and secure mobile keys allow them to bypass counters entirely, streamlining their experience. Moreover, with push notifications alerting them to flight delays, customers can effortlessly adjust pick-up times, enhancing overall satisfaction. While offline walk-ups still play a role in areas with limited smartphone access, they grapple with higher booking costs due to staffing and facility expenses.

Digital traffic is increasingly converging with airline applications, hotel platforms, and third-party online travel agencies, now cross-selling mobility options. This integration reduces customer acquisition costs and paves the way for additional revenue through bundled services like insurance and GPS add-ons. Furthermore, the data reservoirs generated from these transactions provide fleet planners with foresight into city-pair demands, enabling timely fleet transfers and reducing idle days. As a result, operators adopting API-first strategies have significantly outpaced their competitors in utilization metrics within the car rental sector.

Based on experiential tourism trends, leisure travelers generated a 55.68% share of the car rental market in 2025 and will sustain a 10.45% CAGR during the forecast period (2026-2031). Families designing multi-stop road vacations prize vehicle control and luggage flexibility unavailable on group tours. Contactless delivery options introduced during the pandemic remain popular as they let renters proceed directly from baggage claim to parking bay, avoiding crowded shuttle buses. Higher fuel efficiency and spacious cargo areas rank at the top of leisure renters' preference lists, directing procurement toward crossover models.

Business travel is regaining 2019 trip counts, as the average length of rental has increased due to hybrid work policies that allow employees to add personal days. This blend of business and leisure supports weekday and weekend utilization, smoothing the revenue curve. Programmable corporate accounts that bundle emissions reporting help operators attract sustainability-minded firms, reinforcing demand resilience even if corporate trip volumes plateau.

The Car Rental Market Report is Segmented by Booking Mode (Offline and Online), Application (Leisure and Business), End User (Self-Drive Individual and More), Vehicle Type (Mini & Economy Cars, Compact & Intermediate Cars, and More), Rental Length (Short-Term, Medium-Term, and Long-Term), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America comprises a 35.02% share in the car rental market in 2025, reflecting mature travel infrastructure and a high vehicle ownership culture. Avis Budget Group posted USD 12 billion in 2023 sales as airport passenger flows regained momentum and loyalty program re-enrollments climbed. Dynamic pricing engines exploited flight disruption data to capitalize on last-minute bookings. Electric vehicle uptake remains tempered by charging deserts along rural interstates, yet corporate clients have begun mandating low-emission classes for city centers such as New York and Los Angeles. Competitive intensity is elevated in urban corridors where ride-hailing platforms maintain a stronghold, though rentals still dominate one-way interstate journeys.

Asia-Pacific is forecast to grow with a 10.62% CAGR during the forecast period (2026-2031). Rising middle-class travel, visa-on-arrival schemes, and vigorous airline seat growth underpin market momentum. Enterprise Mobility opened ten Thai branches in 2024 and now operates ninety-seven Japanese sites, illustrating aggressive network build-out. Indonesia, Vietnam, and India report double-digit inbound tourism growth, straining public transit capacity and directing visitors toward self-drive solutions. Chinese EV makers enter the tourist segment by offering discounted electric crossovers via rental partnerships, creating a low-cost path to overseas brand exposure.

Europe remains a sophisticated yet fiercely competitive arena. SIXT's multi-year deal for 250000 Stellantis vehicles secures supply amid chip shortages and advances its electrification roadmap. Amsterdam introduces zero-emission zones in 2025, prompting operators to reserve high-value parking slots for electric fleets. Cross-border rentals flourish on the continent's open internal borders, though differing road toll regimes complicate fleet tracking. Europcar's re-entry into the United States with Atlanta and Dallas outlets signals renewed transatlantic ambitions. Elsewhere, Latin America and the Middle East benefit from improving highway networks and inbound events such as Saudi Arabia's Vision 2030 tourism push, yet currency volatility and import restrictions require agile capital allocation.

- Avis Budget Group Inc.

- Hertz Global Holdings Inc.

- Enterprise Holdings Inc.

- Europcar Mobility Group

- Sixt SE

- Localiza Rent a Car S.A.

- ALD Automotive

- Beijing CAR Inc. (CAR Inc.)

- GIG Car Share

- Lyft Rental

- Uber Rentals

- Silvercar by Audi

- Getaround

- Zoomcar

- Ola Drive

- Fast Rent A Car

- Bettercar Rental

- TT Car Transit

- Renault Eurodrive

- Shenzhen Supreme Car Rental Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Rebound Of Post-Pandemic Leisure Travel

- 4.2.2 Growing Penetration Of Online And Mobile Booking Platforms

- 4.2.3 Expansion Of Low-Cost Airlines Creating Multi-Modal Travel Demand

- 4.2.4 Corporate Esg Mandates Accelerating Adoption Of Ev Rental Fleets

- 4.2.5 Data-Driven Dynamic Pricing Tools Boosting Utilisation Rates

- 4.2.6 Airport Infrastructure Upgrades In Emerging Markets

- 4.3 Market Restraints

- 4.3.1 Popularity Of Ride-Hailing And Car-Sharing Substitutes

- 4.3.2 Rising Residual-Value Risk Amid Rapid Ev Technology Cycles

- 4.3.3 Airport Concession Fees Squeezing Operator Margins

- 4.3.4 Regulatory Caps On Ice Vehicles In Urban Cores

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Booking Mode

- 5.1.1 Offline

- 5.1.2 Online

- 5.2 By Application

- 5.2.1 Leisure

- 5.2.2 Business

- 5.3 By End User

- 5.3.1 Self-Drive Individual

- 5.3.2 Chauffeur-Drive

- 5.3.3 Corporate Fleet Subscription

- 5.3.4 Peer-to-Peer Rental

- 5.4 By Vehicle Type

- 5.4.1 Mini & Economy Cars

- 5.4.2 Compact & Intermediate Cars

- 5.4.3 Standard & Full-Size Cars

- 5.4.4 SUVs & MPVs

- 5.4.5 Luxury / Premium Cars

- 5.5 By Rental Length

- 5.5.1 Short-Term

- 5.5.2 Medium-Term

- 5.5.3 Long-Term

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Avis Budget Group Inc.

- 6.4.2 Hertz Global Holdings Inc.

- 6.4.3 Enterprise Holdings Inc.

- 6.4.4 Europcar Mobility Group

- 6.4.5 Sixt SE

- 6.4.6 Localiza Rent a Car S.A.

- 6.4.7 ALD Automotive

- 6.4.8 Beijing CAR Inc. (CAR Inc.)

- 6.4.9 GIG Car Share

- 6.4.10 Lyft Rental

- 6.4.11 Uber Rentals

- 6.4.12 Silvercar by Audi

- 6.4.13 Getaround

- 6.4.14 Zoomcar

- 6.4.15 Ola Drive

- 6.4.16 Fast Rent A Car

- 6.4.17 Bettercar Rental

- 6.4.18 TT Car Transit

- 6.4.19 Renault Eurodrive

- 6.4.20 Shenzhen Supreme Car Rental Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space Analysis & Unmet Needs

汽車麥克風市場規模、佔有率和成長分析:按麥克風類型、應用、連接方式、車輛類型和地區分類-2026-2033年產業預測

汽車麥克風市場規模、佔有率和成長分析:按麥克風類型、應用、連接方式、車輛類型和地區分類-2026-2033年產業預測 租車市場機會、成長要素、產業趨勢分析及2026-2035年預測。

租車市場機會、成長要素、產業趨勢分析及2026-2035年預測。 租車市場:2026年至2032年全球市場預測(依租賃期限、燃料類型、服務功能、用戶層、車輛類型及預訂方式分類)汽車租賃市場:2026-2032年全球市場預測(依租賃期限、驅動方式、車輛等級、車輛類型、銷售管道及客戶類型分類)

租車市場:2026年至2032年全球市場預測(依租賃期限、燃料類型、服務功能、用戶層、車輛類型及預訂方式分類)汽車租賃市場:2026-2032年全球市場預測(依租賃期限、驅動方式、車輛等級、車輛類型、銷售管道及客戶類型分類) 2026年全球自駕汽車租賃市場報告2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告

2026年全球自駕汽車租賃市場報告2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告 2026-2034年全球汽車麥克風市場規模、佔有率、趨勢和成長分析報告租車及租賃市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類)

2026-2034年全球汽車麥克風市場規模、佔有率、趨勢和成長分析報告租車及租賃市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類)