|

市場調查報告書

商品編碼

1910655

中東汽車租賃市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Middle East Car Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

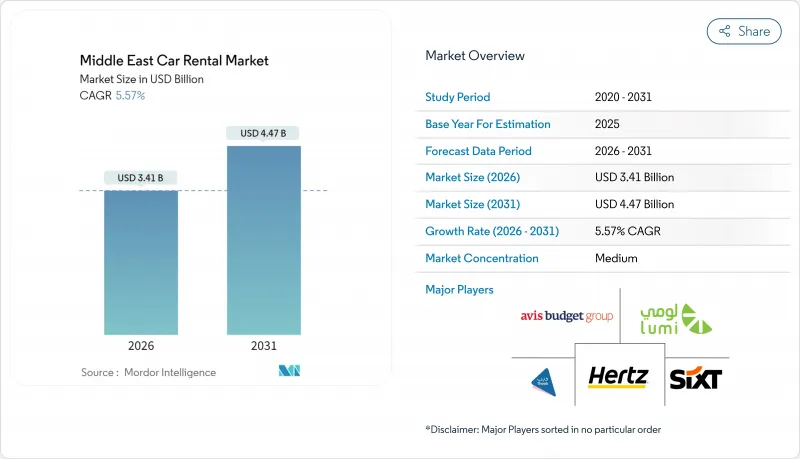

預計到 2026 年,中東汽車租賃市場價值將達到 34.1 億美元。

這代表著從 2025 年的 32.3 億美元成長到 2031 年的 44.7 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.57%。

入境旅遊的成長、對高階出行方式的需求以及數位技術的廣泛應用正在推動市場擴張。預計2024年國際旅客造訪量將比疫情前水準增加32%,達到9,500萬人次,將持續帶動租車需求。目前,基於應用程式的預訂量已佔總交易量的約三分之二,其中豪華車和電動車細分市場成長最為迅速。沙烏地阿拉伯的「2030願景」和2030年世博會等政府主導的大型企劃正在推動出行走廊的擴張,促進車輛升級,並在機場之外開發新的收入來源。相對分散的市場格局,加上大規模創業融資,預計將進一步推動產業整合。

中東汽車租賃市場趨勢與洞察

海灣合作理事會走廊旅遊業復甦

2024年,海灣合作理事會(GCC)國家的旅遊業顯著復甦。沙烏地阿拉伯的遊客人數激增69%,旅遊收入達606億美元。旅遊業為阿拉伯聯合大公國的國內生產毛額(GDP)貢獻了599億美元,相當於該國經濟規模的11.7%。卡達在2025年上半年迎來了100萬名遊客的顯著成長。同時,科威特正大力投資以旅遊為中心的基礎建設,從而推動了對更多車輛的需求。這種跨境交通流動將要求營運商在不同轄區之間進行策略性車隊調配,建立穩健的走廊式服務策略,並適應不同的法規結構——所有這些都必須充分利用不斷成長的客流量。

快速轉向應用程式預訂

智慧型手機的高普及率和數位支付的成熟度使得行動預訂量超過了線下交易量,降低了分銷成本,並使企業能夠直接獲取客戶資料。在阿拉伯聯合大公國,近乎普及的5G網路覆蓋範圍和消費者對非接觸式服務的偏好正在加速這一趨勢,而沙烏地阿拉伯的年輕人口也在推動行動裝置使用量的成長。嵌入式身份驗證和無鑰匙進入提升了便利性,而預測分析則最佳化了車輛輪換。擁有自主應用程式的企業可以避免第三方費用,提高利潤率,並透過忠誠度工具確保客戶的終身價值。

共乘壓力

在大都會圈,叫車服務的擴張正逐步取代傳統的短程城市出行,而這些出行方式以往主要由私人租車主導。然而,對於多日觀光旅行、家庭旅行和城際旅行而言,租車仍然具有強大的吸引力,並維持著穩固的需求基礎。為了因應這種變化,營運商正在拓展服務範圍,並專注於推出能夠提升租車體驗的加值服務。他們也將必要的導航工具與叫車平台整合,打造無縫接軌的多式聯運出行方案。透過策略性地將租車服務定位在長途旅行和高價值用途,他們有效地減少了客戶流失到叫車平台的趨勢,並在日益便捷的出行方式中確保了私家車的持續吸引力。

細分市場分析

預計到2025年,線上預訂將佔中東汽車租賃市場62.12%的佔有率,預測期內複合年成長率(CAGR)為6.74%。線下櫃檯仍主要服務於機場和飯店的散客,但面臨高昂的營運成本。行動優先的介面支援即時升級、添加選項和積分獎勵,從而縮短預訂前置作業時間並提高車輛利用率。從長遠來看,全通路策略將成為主流,實體門市將專注於客戶支援和車輛交付,而數位管道將承擔銷售、支付和提升銷售功能。

競爭主要集中在專有應用程式與市場聚合平台之間。整合了即時車輛庫存管理、數位身份驗證和無鑰匙取車等功能的營運商正在縮短交易時間。阿拉伯聯合大公國智慧型手機的普及加速了行動支付的普及,而擁有廣泛4G網路的沙烏地阿拉伯也緊隨其後。科威特和阿曼目前仍依賴線下預訂,但隨著消費者期望的改變,它們也穩步採用行動解決方案。

預計到2025年,休閒和旅遊租賃將佔中東汽車租賃市場收入的95.10%,並在2031年之前以7.22%的複合年成長率成長。杜拜、杜哈、利雅德和Muscat憑藉著大型活動和寬鬆的簽證政策,保持著對遊客的吸引力。然而,企業需求正在推動收入來源多元化,跨國公司紛紛在沙烏地阿拉伯和阿拉伯聯合大公國設立區域總部。

全年持續的會議和計劃主導差旅正在緩解假日高峰期帶來的季節性風險。同時服務遊客和企業高管的公司正在最佳化車隊配置,在旅遊旺季使用經濟型轎車,在淡季則將豪華轎車分配給企業客戶。這種雙市場策略有助於穩定現金流並提高整體運轉率。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 海灣合作理事會走廊旅遊業復甦

- 向基於應用程式的預訂方式的快速轉變

- 大型活動和基礎設施計劃(2030願景、2030年世博會)

- 企業行動訂閱採用情況

- 政府對電動車租賃的激勵措施

- 整合出行超級應用的興起

- 市場限制

- 取代叫車的壓力

- 與勞動力本土化相關的合規成本

- 電動車租賃保險供給能力短缺

- 進口依賴型車輛供應瓶頸

- 價值/供應鏈分析

- 監管環境

- 技術展望(車載資訊系統、OTA、電動車)

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過預約方式

- 線上

- 離線

- 透過使用

- 休閒/旅遊

- 日常使用/商務

- 按車輛類型

- 經濟

- 奢華與高階

- 按最終用戶類型

- 自駕

- 專車接送

- 按服務類型

- 機場內部

- 機場外/區域內

- 透過推進力

- 內燃機(ICE)

- 電動和混合動力汽車

- 按國家/地區

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 科威特

- 卡達

- 其他中東國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、 首次股票公開發行、車隊電氣化)

- 市佔率分析

- 公司簡介

- Avis Budget Group

- Hertz Corporation

- Enterprise Holdings Inc.

- Sixt SE

- Europcar Mobility Group

- Lumi Rental Company

- Theeb Rent A Car

- Yelo

- Fast Rent A Car

- Al Talaa International Transportation Co(Hanco)

- Telgani Company

第7章 市場機會與未來展望

The Middle East car rental market size in 2026 is estimated at USD 3.41 billion, growing from 2025 value of USD 3.23 billion with 2031 projections showing USD 4.47 billion, growing at 5.57% CAGR over 2026-2031.

Rising inbound tourism, premium-oriented mobility demand, and broad digital adoption underpin the expansion. International arrivals surpassed pre-pandemic levels by 32% in 2024, translating into 95 million visitors and sustained rental demand . App-based reservations already account for close to two-thirds of total transactions, while luxury and electric fleet niches record the fastest volume gains. Government-backed megaprojects such as Saudi Arabia's Vision 2030 and Expo 2030 are widening mobility corridors, encouraging fleet upgrades, and opening new off-airport revenue pools. Moderate market fragmentation, coupled with sizable venture funding, signals further consolidation.

Middle East Car Rental Market Trends and Insights

Tourism Rebound Across GCC Corridors

GCC destinations recorded a pronounced tourism recovery in 2024, led by Saudi Arabia's 69% surge in arrivals and tourism receipts of USD 60.6 billion. The United Arab Emirates contributed USD 59.9 billion to GDP from travel and tourism, equivalent to 11.7% of the economy . In the first half of 2025, Qatar welcomed a significant influx of one million visitors. Meanwhile, Kuwait is making substantial investments in visitor-centric infrastructure, indicating a rising demand for additional fleets. These cross-border movements require operators to strategically reposition vehicles across jurisdictions, establish robust corridor-based service strategies, and adapt to varying regulatory frameworks, all while leveraging the growing utilization rates.

Rapid Shift to App-Based Bookings

High smartphone penetration and digital payments maturity enable mobile reservations to eclipse counter transactions, trimming distribution overheads and granting operators direct access to customer data. In the UAE, near-ubiquitous 5G coverage and consumer preference for contactless services accelerate the trend, while Saudi Arabia's youthful demographic amplifies mobile adoption. Embedded identity verification and keyless entry elevate user convenience, and predictive analytics refine fleet rotation. Firms that own proprietary apps bypass third-party commissions, enhance margins, and lock in lifetime customer value through loyalty tools.

Ride-Hailing Substitution Pressure

The expansion of ride-hailing services in bustling metropolitan areas increasingly captures short city trips that once favored self-drive rentals. However, for multi-day tourism, family vacations, and intercity commutes, the allure of rental cars remains strong, sustaining a solid base of demand. In response to this shifting landscape, operators are ramping up their offerings, highlighting premium service tiers that elevate the rental experience. They're also bundling essential navigation tools and forging partnerships with e-hail platforms to create seamless blended mobility passes. By strategically positioning rentals for longer journeys and higher-value usage, they effectively minimize the loss of customers to on-demand rides, ensuring that the charm of a personal vehicle endures amidst the rising tide of convenience.

Other drivers and restraints analyzed in the detailed report include:

- Mega-Events and Infrastructure Projects (Vision 2030, Expo 2030)

- Corporate Mobility-Subscription Adoption

- Labor-Nationalization Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online reservations represented 62.12% of the Middle East car rental market size in 2025 and are projected to climb at a 6.74% CAGR during the forecast period. Offline counters still capture walk-in tourists at airports and hotels, but suffer higher overheads. Mobile-first interfaces support instant upgrades, add-ons, and loyalty redemption, shrinking booking lead times and lifting utilization. In the longer run, omnichannel strategies will persist, with physical outlets pivoting toward customer support and vehicle handover while digital funnels handle sales, payments, and upselling.

Competition centers on proprietary apps versus marketplace aggregators. Operators that integrate real-time vehicle availability, digital KYC, and keyless pick-ups are lowering transaction times. The UAE's smartphone penetration accelerates uptake, and Saudi Arabia follows closely, aided by widespread 4G coverage. Kuwait and Oman remain more reliant on desk bookings but are steadily onboarding mobile solutions as consumer expectations shift.

Leisure and tourism rentals supplied 95.10% of the Middle East car rental market revenue in 2025, advancing at a forecast 7.22% CAGR through 2031. Mega-events and relaxed visa regimes sustain destination appeal across Dubai, Doha, Riyadh, and Muscat. Nevertheless, corporate demand is diversifying revenue streams as multinationals locate regional headquarters in Saudi Arabia and the United Arab Emirates.

Seasonality risk tied to holiday peaks is being diluted by year-round conferences and project-driven travel. Firms adept at serving both tourists and executives optimize fleet mix, rotating economy cars during peak visitor influx and allocating premium sedans for business accounts in shoulder months. This dual-market posture stabilizes cash flow and raises overall utilization.

The Middle East Car Rental Market is Segmented by Booking Type (Online and Offline), Application (Leisure/Tourism, Daily Utility/Business), Vehicle Type (Economy, Luxury and Premium), End-User Type (Self-Driven and Chauffeur), Service Model (On-Airport, and Off-airport/Local), Propulsion (Internal-Combustion ICE, Electric and Hybrid), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Avis Budget Group

- Hertz Corporation

- Enterprise Holdings Inc.

- Sixt SE

- Europcar Mobility Group

- Lumi Rental Company

- Theeb Rent A Car

- Yelo

- Fast Rent A Car

- Al Talaa International Transportation Co (Hanco)

- Telgani Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tourism Rebound Across GCC Corridors

- 4.2.2 Rapid Shift to App-Based Bookings

- 4.2.3 Mega-Events and Infrastructure Projects (Vision 2030, Expo 2030)

- 4.2.4 Corporate Mobility-Subscription Adoption

- 4.2.5 Government EV-Rental Incentives

- 4.2.6 Emergence of Integrated Mobility Super-Apps

- 4.3 Market Restraints

- 4.3.1 Ride-Hailing Substitution Pressure

- 4.3.2 Labor-Nationalization Compliance Costs

- 4.3.3 Thin EV-Rental Insurance Capacity

- 4.3.4 Import-Driven Vehicle Supply Bottlenecks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (Telematics, OTA, EV)

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Booking Type

- 5.1.1 Online

- 5.1.2 Offline

- 5.2 By Application

- 5.2.1 Leisure / Tourism

- 5.2.2 Daily Utility / Business

- 5.3 By Vehicle Type

- 5.3.1 Economy

- 5.3.2 Luxury and Premium

- 5.4 By End-User Type

- 5.4.1 Self-driven

- 5.4.2 Chauffeur

- 5.5 By Service Model

- 5.5.1 On-airport

- 5.5.2 Off-airport / Local

- 5.6 By Propulsion

- 5.6.1 Internal-Combustion (ICE)

- 5.6.2 Electric and Hybrid

- 5.7 By Country

- 5.7.1 Saudi Arabia

- 5.7.2 United Arab Emirates

- 5.7.3 Kuwait

- 5.7.4 Qatar

- 5.7.5 Rest of Middle East Countries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, IPOs, Fleet Electrification)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Avis Budget Group

- 6.4.2 Hertz Corporation

- 6.4.3 Enterprise Holdings Inc.

- 6.4.4 Sixt SE

- 6.4.5 Europcar Mobility Group

- 6.4.6 Lumi Rental Company

- 6.4.7 Theeb Rent A Car

- 6.4.8 Yelo

- 6.4.9 Fast Rent A Car

- 6.4.10 Al Talaa International Transportation Co (Hanco)

- 6.4.11 Telgani Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

租車市場:2026年至2032年全球市場預測(依租賃期限、燃料類型、服務功能、用戶層、車輛類型及預訂方式分類)汽車租賃市場:2026-2032年全球市場預測(依租賃期限、驅動方式、車輛等級、車輛類型、銷售管道及客戶類型分類)

租車市場:2026年至2032年全球市場預測(依租賃期限、燃料類型、服務功能、用戶層、車輛類型及預訂方式分類)汽車租賃市場:2026-2032年全球市場預測(依租賃期限、驅動方式、車輛等級、車輛類型、銷售管道及客戶類型分類) 2026年全球自駕汽車租賃市場報告2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告

2026年全球自駕汽車租賃市場報告2026年全球乘用車租賃市場報告2026年全球汽車租賃市場報告 2026-2034年全球汽車麥克風市場規模、佔有率、趨勢和成長分析報告租車及租賃市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類)

2026-2034年全球汽車麥克風市場規模、佔有率、趨勢和成長分析報告租車及租賃市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測租車及租賃市場:2026年至2032年全球預測(依車輛類型、型號、租賃時長、動力系統、應用領域、最終用戶及預訂模式分類) 2026-2030年全球汽車租賃市場

2026-2030年全球汽車租賃市場 汽車租賃市場分析及預測(至2035年):依類型、產品類型、服務、技術、最終用戶、部署類型、用途、模式及功能分類

汽車租賃市場分析及預測(至2035年):依類型、產品類型、服務、技術、最終用戶、部署類型、用途、模式及功能分類