|

市場調查報告書

商品編碼

1940735

西班牙電力:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Spain Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

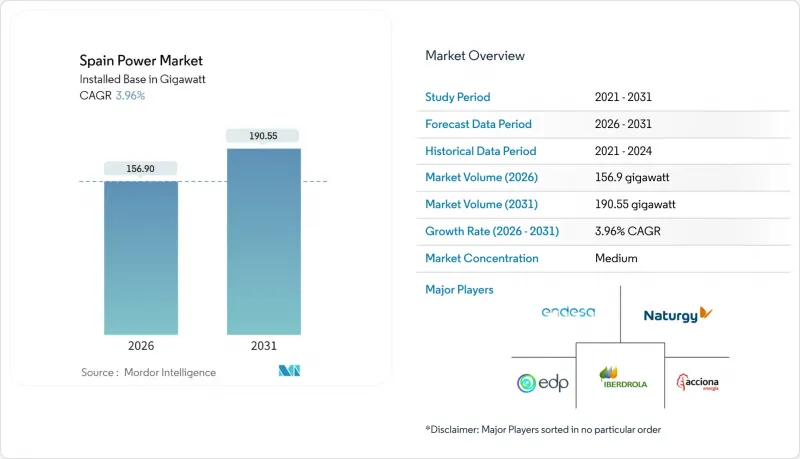

預計西班牙電力市場將從 2025 年的 150.93 吉瓦成長到 2026 年的 156.9 吉瓦,從 2026 年到 2031 年的複合年成長率為 3.96%,到 吉瓦。

這一成長得益於西班牙加速部署可再生能源、歐盟的脫碳指令以及企業對清潔電力購買協議的強勁需求。到2024年,太陽能光電發電將成為西班牙最大的單一電力來源,鞏固其向低碳發電的轉型。優先建造超高壓輸電走廊和歐盟支持的儲能資金的電網現代化計畫正在擴大間歇性發電的併網規模。同時,工業電氣化、促進電動車出行的措施以及資料中心的發展正在改變負載結構,從而維持對併網可再生的需求。最後,核能發電淘汰政策的轉變正在提高基本負載的韌性,並將容量充足性問題延後到電網升級改造完成後再進行。

西班牙電力市場趨勢與分析

加速興建併網太陽能發電廠

2024年,西班牙太陽能產業迎來里程碑式的一年,超越天然氣和風能,成為全國最大的能源來源。當局批准了2024年新增26,159.2兆瓦可再生能源項目,其中太陽能項目佔22,326.1兆瓦。這顯示成本下降、核准程序簡化,以及企業對可再生能源證書(REC)的需求不斷成長。卡斯蒂利亞-萊昂自治區、阿拉貢自治區和卡斯提爾-拉曼恰自治區獲得了最多的配額,這得益於其優越的日照條件和充足的土地資源。分散式屋頂光電系統也在工業園區迅速發展,有助於降低能源成本和範圍2排放。大型發電廠與現場發電設施之間的協同效應正在推動西班牙電力市場可再生能源滲透率的提高,並有助於實現2030年綠色電力佔比達到81%的目標。

由超大規模資料中心參與者主導的參與企業對企業購電協議

超大規模平台的需求正在重塑西班牙電力市場的收入模式。谷歌簽署的35兆瓦、為期10年的風電購電協議(PPA)、亞馬遜的469兆瓦太陽能計畫以及蘋果的105兆瓦協議,凸顯了由科技巨頭支持的、以開發商主導的建設模式轉變。資料中心容量到2026年可能達到600兆瓦,到2030年可能達到3000兆瓦,從而支撐起數吉瓦的可再生能源專案儲備。購電協議能夠提供穩定的現金流,降低資金籌措成本,並與超大規模資料中心業者的淨零排放策略相契合,加速其在傳統公用事業採購模式之外的部署。

增加資本支出(CAPEX)以加強電網

西班牙電網公司(Red Electrica)已為2026年前的電網加固工程累計65億歐元,但表示到2030年需要100億歐元,資金缺口達35億歐元。電價上限將年漲幅限制在15%,阻礙了成本回收。變電站建設中出現了土地問題,15座規劃中的400千伏變電站中有8座因法律糾紛而延誤了兩年。鋼鐵和銅價上漲導致輸電線路建設成本從2020年的每公里120萬歐元增加到2024年的每公里180萬歐元。如果不進行改革,到2028年,可再生能源發電量可能每年減少50億度,太陽能光電發電的有效利用率預計將降至22%。

細分市場分析

至2025年,可再生能源裝置容量將佔西班牙裝置容量的67.10%,年增率為6.95%。西班牙清潔能源市場規模將從2025年的101.27吉瓦擴大到2031年的150.66吉瓦。截至2025年1月,太陽能光電發電裝置容量已超過風電(32.0吉瓦),主要得益於較低的競標價格和24%的產能運轉率。陸域風電場改造將提高其發電效率,而無需佔用新的土地;同時,2吉瓦的浮體式海上風電租賃計畫將釋放尚未開發的海洋資源。水力發電裝置容量將維持穩定在17吉瓦,但水庫水位下降將限制抑低尖峰負載能力。預計2027年逐步淘汰燃煤電廠以及將燃氣電廠改造為可再生能源的調峰免稅容量,將進一步收緊風能和太陽能發電量不足時的備用容量。

預計到2025年,火電裝置容量將下降至總裝置容量的25.80%。 Endesa公司的煤炭淘汰計畫將減少2吉瓦的裝置容量,每年排放1,200萬噸二氧化碳排放。聯合循環燃氣發電的總裝置容量將維持在24吉瓦,但隨著可再生的擴張,運作時間將會減少。混合儲能系統將能夠應對長達四小時的輸出波動。核能發電將穩定在7.1吉瓦,直至2035年。此後,核電廠的關閉將造成50太瓦時的電力供應缺口,需要透過進口電力或電池儲能來填補。循環經濟獎勵將有助於生質能發電裝置容量從1.2吉瓦成長到2030年的1.8吉瓦。這些變化表明,儘管電網柔軟性面臨的挑戰日益嚴峻,但西班牙電力市場正在向低碳技術轉型。

西班牙電力市場報告按能源類型(火力發電、核能、可再生)和終端用戶(公用事業、工商業、住宅)進行細分。市場規模和預測以裝置容量(吉瓦)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 加速興建併網太陽能發電廠

- 對上世紀90年代和本世紀初建造的風力發電廠進行更新

- 超大規模資料中心參與企業主導的企業間購電協定 (PPA)

- 歐盟「適合55歲族群」計畫與國家能源與氣候計畫2030年脫碳義務

- 交通和暖氣的快速電氣化

- 歐盟為跨境高壓直流輸電線路提供資金

- 市場限制

- 電網升級改造的資本投資成本增加

- 延長環境和地方政府許可程序

- 資源豐富地區減產風險增加

- 當地居民反對在陸上位置風力發電廠

- 供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- PESTEL 分析

第5章 市場規模與成長預測

- 透過電源

- 熱感(煤炭、天然氣、石油和天然氣、柴油)

- 核能

- 可再生能源(太陽能、風能、水力、地熱能、生質能/廢棄物、潮汐能)

- 最終用戶

- 公共產業

- 商業和工業

- 住宅

- 按輸配電和電壓等級(僅定性分析)

- 高壓輸電(230千伏特或更高)

- 次級輸電(69 至 161 千伏特)

- 中壓配電(13.2 至 34.5 kV)

- 低壓配電(1kV或以下)

第6章 競爭情勢

- 市場集中度

- 策略性舉措(併購、夥伴關係、購電協議)

- 市場佔有率分析(主要企業的市場排名和佔有率)

- 公司簡介

- Endesa SA

- Iberdrola SA

- Naturgy Energy Group SA

- EDP Group(EDP HC Energia)

- Acciona Energia

- Repsol Electricidad y Gas

- Grupo Red Electrica

- Siemens Gamesa Renewable Energy

- Nordex SE

- TotalEnergies SE

- Enel Green Power Espana

- Vestas Mediterranean

- ABO Wind AG

- Engie Espana

- Capital Energy

- Forestalia Renovables

- Grenergy Renovables

- Hive Energy Spain

- Solarpack Corporacion Tecnologica

第7章 市場機會與未來展望

The Spain Power Market is expected to grow from 150.93 gigawatt in 2025 to 156.9 gigawatt in 2026 and is forecast to reach 190.55 gigawatt by 2031 at 3.96% CAGR over 2026-2031.

The expansion is propelled by the country's accelerated renewables build-out, EU decarbonization mandates, and strong corporate appetite for clean power purchase agreements. Solar PV became the nation's single largest power source in 2024, confirming Spain's pivot toward low-carbon generation. A grid-modernization agenda that prioritizes extra-high-voltage corridors, alongside EU-backed storage funding, is enabling ever-larger volumes of intermittent output to connect. Meanwhile, industrial electrification, e-mobility incentives, and data-center development are reshaping load profiles and sustaining demand for grid-connected renewables. Finally, the reversal of the nuclear phase-out adds baseload resilience and delays capacity-adequacy concerns while transmission upgrades catch up.

Spain Power Market Trends and Insights

Accelerating Grid-Connected Solar PV Build-Out

Spain's solar segment set a watershed in 2024 when it overtook gas and wind as the country's top power source. Authorities cleared 26,159.2 MW of renewable construction in 2024, 22,326.1 MW of which is PV, underscoring cost declines, streamlined permitting, and corporate REC demand. Castilla y Leon, Aragon, and Castilla-La Mancha garnered the largest quotas, benefiting from superior irradiation and land availability. Distributed rooftop systems are likewise proliferating across industrial estates, cutting energy bills and Scope-2 emissions. Together, utility-scale and on-site arrays are raising the Spain electricity market's renewable penetration, easing compliance with the 81% green-power target for 2030.

Corporate PPAs Led by Hyperscale Data-Center Entrants

Demand from hyperscale platforms is reshaping revenue models in the Spain electricity market. Google's 35 MW, 10-year wind PPA, Amazon's 469 MW solar commitment, and Apple's 105 MW deal illustrate a shift toward developer-financed build-outs backstopped by tech majors. Data-center capacity could hit 600 MW in 2026 and 3,000 MW by 2030, sustaining multi-gigawatt renewable pipelines. PPAs provide bankable cash flows, lower financing costs, and dovetail with hyperscalers' net-zero strategies, accelerating installations beyond traditional utility procurement volumes.

Escalating Transmission Upgrade CAPEX

Red Electrica budgets EUR 6.5 billion for reinforcements through 2026, yet identifies a EUR 10 billion need by 2030, leaving a EUR 3.5 billion gap. Tariff caps limit annual hikes to 15%, throttling cost recovery. Substation builds face land disputes, with 8 of 15 400-kV facilities delayed two years by legal appeals. Steel and copper inflation pushed line costs from EUR 1.2 million /km in 2020 to EUR 1.8 million /km in 2024. Absent reform, 5 TWh of renewable output could be shed each year by 2028, trimming effective solar utilization to 22%.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Electrification of Mobility & Heating

- EU Fit-for-55 & NECP-2030 Decarbonisation Mandates

- Lengthy Environmental & Municipal Permitting

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Renewables accounted for 67.10% of installed capacity in 2025, and their 6.95% yearly advance ensures the Spain power market size for clean sources rises from 101.27 GW in 2025 to 150.66 GW in 2031. Solar photovoltaic eclipsed wind at 32.0 GW versus 32.0 GW in January 2025, propelled by low auction tariffs and 24% capacity factors. Repowering lifts onshore wind productivity without new land, while 2 GW of floating offshore leases open an untapped marine resource. Hydropower remains steady at 17 GW but suffers from lower reservoir levels that curb peak-shaving ability. Coal's exit by 2027 and gas's shift to peaking duty-free capacity for renewables will yet tighten reserve margins on low-wind, low-sun days.

Thermal fleets fell to 25.80% of capacity in 2025. Endesa's coal phase-out removed 2 GW, slashing 12 million tpy of CO2. Combined-cycle gas totals 24 GW but runs fewer hours as renewables scale, with hybrid storage enabling four-hour ramps. Nuclear stays flat at 7.1 GW through 2035, after which closures leave a 50 TWh gap to fill with imports or batteries. Biomass grows from 1.2 GW to a projected 1.8 GW by 2030 under circular-economy incentives. Together, this transformation underlines how the Spain power market pivots toward carbon-free technologies even as grid flexibility challenges mount.

The Spain Power Market Report is Segmented by Power Source (Thermal, Nuclear, and Renewables) and End-User (Utilities, Commercial and Industrial, and Residential). The Market Sizes and Forecasts are Provided in Terms of Installed Capacity (GW).

List of Companies Covered in this Report:

- Endesa S.A.

- Iberdrola S.A.

- Naturgy Energy Group S.A.

- EDP Group (EDP HC Energia)

- Acciona Energia

- Repsol Electricidad y Gas

- Grupo Red Electrica

- Siemens Gamesa Renewable Energy

- Nordex SE

- TotalEnergies SE

- Enel Green Power Espana

- Vestas Mediterranean

- ABO Wind AG

- Engie Espana

- Capital Energy

- Forestalia Renovables

- Grenergy Renovables

- Hive Energy Spain

- Solarpack Corporacion Tecnologica

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating grid-connected solar PV build-out

- 4.2.2 Repowering of 1990s-2000s wind farms

- 4.2.3 Corporate PPAs led by hyperscale data-centre entrants

- 4.2.4 EU Fit-for-55 & NECP-2030 decarbonisation mandates

- 4.2.5 Rapid electrification of mobility & heating

- 4.2.6 EU funding for cross-border HVDC links

- 4.3 Market Restraints

- 4.3.1 Escalating transmission upgrade CAPEX

- 4.3.2 Lengthy environmental & municipal permitting

- 4.3.3 Rising curtailment risk in resource-rich regions

- 4.3.4 Local opposition to on-shore wind siting

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Power Source

- 5.1.1 Thermal (Coal, Natural Gas, Oil and Diesel)

- 5.1.2 Nuclear

- 5.1.3 Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal)

- 5.2 By End User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

- 5.3 By T&D Voltage Level (Qualitative Analysis only)

- 5.3.1 High-Voltage Transmission (Above 230 kV)

- 5.3.2 Sub-Transmission (69 to 161 kV)

- 5.3.3 Medium-Voltage Distribution (13.2 to 34.5 kV)

- 5.3.4 Low-Voltage Distribution (Up to 1 kV)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Endesa S.A.

- 6.4.2 Iberdrola S.A.

- 6.4.3 Naturgy Energy Group S.A.

- 6.4.4 EDP Group (EDP HC Energia)

- 6.4.5 Acciona Energia

- 6.4.6 Repsol Electricidad y Gas

- 6.4.7 Grupo Red Electrica

- 6.4.8 Siemens Gamesa Renewable Energy

- 6.4.9 Nordex SE

- 6.4.10 TotalEnergies SE

- 6.4.11 Enel Green Power Espana

- 6.4.12 Vestas Mediterranean

- 6.4.13 ABO Wind AG

- 6.4.14 Engie Espana

- 6.4.15 Capital Energy

- 6.4.16 Forestalia Renovables

- 6.4.17 Grenergy Renovables

- 6.4.18 Hive Energy Spain

- 6.4.19 Solarpack Corporacion Tecnologica

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

電力零售市場-全球產業規模、佔有率、趨勢、機會和預測:按市場結構、客戶類型、服務類型、支付方式、地區和競爭格局分類,2021-2031年

電力零售市場-全球產業規模、佔有率、趨勢、機會和預測:按市場結構、客戶類型、服務類型、支付方式、地區和競爭格局分類,2021-2031年 中國電力產業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國電力市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

中國電力產業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)美國電力市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 再生能源線路市場預測至2034年-能源來源、輸電網類型、最終用戶和地區分類的全球分析

再生能源線路市場預測至2034年-能源來源、輸電網類型、最終用戶和地區分類的全球分析 2026-2030年全球電力交易市場

2026-2030年全球電力交易市場 2026年人工智慧(AI)資料中心熱能儲存全球市場報告2026年全球太陽能人工智慧市場報告2026年全球可再生能源購電合約市場報告

2026年人工智慧(AI)資料中心熱能儲存全球市場報告2026年全球太陽能人工智慧市場報告2026年全球可再生能源購電合約市場報告 人工智慧在能源與電力市場的應用:策略性洞察與預測(2026-2031)

人工智慧在能源與電力市場的應用:策略性洞察與預測(2026-2031) 可調可再生能源市場規模、佔有率和趨勢分析報告:按技術、最終用途、地區和細分市場分類,預測至2026-2033年

可調可再生能源市場規模、佔有率和趨勢分析報告:按技術、最終用途、地區和細分市場分類,預測至2026-2033年