|

市場調查報告書

商品編碼

1939144

汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

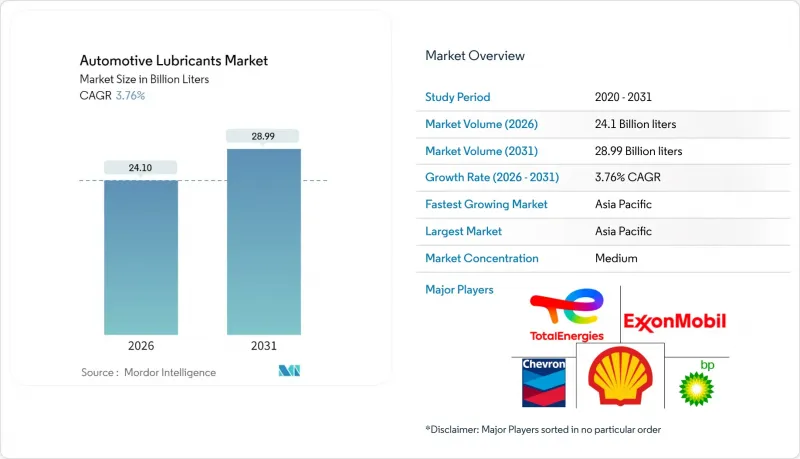

2025年汽車潤滑油市場價值為232.3億公升,預計到2031年將達到289.9億公升,高於2026年的241億公升。

預計在預測期(2026-2031 年)內,複合年成長率將達到 3.76%。

全球已開發地區汽車保有量的老化、新興經濟體摩托車和商用車的持續湧入,以及產業向燃油經濟性更佳、換油週期更長的優質合成油轉型,共同推動了市場成長。亞太地區憑藉著不斷上升的汽車保有量和本地製造業投資,仍然是核心需求中心;而北美和歐洲則依靠更長的車輛使用壽命來維持售後市場銷售。市場競爭強度依然適中:殼牌在2024年連續第18年保持市場領先地位,但區域性調配商正透過提升本地產能和定製配方來擴大市場佔有率。電動車(EV)的快速普及(截至2024年,中國電動車保有量將達到3,140萬輛)以及汽車製造商強制要求的更長換油週期等不利因素,被API SQ標準及同類低黏度合成油更高的單價所抵消。

全球汽車潤滑油市場趨勢與洞察

主要經濟體的平均車輛車齡不斷增加

車輛使用壽命的延長正在改變潤滑油的需求模式。在美國,半導體短缺和通貨膨脹減緩了車輛的更換速度,促使車主增加換油頻率並投資購買高品質合成機油。歐洲車輛的車齡較長,西歐平均車齡為18.1年,東歐為28.4年,導致車輛維修頻率較高,單車潤滑油消耗量也較大。老舊引擎容易出現密封件劣化、熱應力和污染等問題,這些都會加速機油劣化,從而推高對高品質基礎油的需求。車齡在6至15年之間的車輛,其維修成本在短短一年內就從514美元上漲至537美元,凸顯了車齡與維修成本之間的關聯。報廢率已降至4.20%,為20年來的最低水平,從而擴大了售後市場的收入來源。隨著車主尋求長期保護和更低的整體擁有成本,高價值合成機油正逐漸成為維修廠的主流選擇。

新興市場全球汽車保有量成長

新興經濟體正在抵消成熟市場電動車相關下滑的影響。預計2024年,中國汽車保有量將新增3,583萬輛,達到4.53億輛。在印度和東南亞,受緩解都市區擁擠和尋求經濟實惠的出行方式的需求驅動,摩托車保有量持續成長。營運電商和最後一公里配送的商用車輛行駛里程更高,換油頻率也更高。這些地區的本土汽車製造商正與當地潤滑油調配商合作,快速開發適用於各種燃油品質和極端氣候條件的低成本潤滑油。因此,儘管全球經濟成長放緩,汽車潤滑油市場仍維持成長動能。

加速電動車普及

電動車的廣泛普及將使曲軸箱油和許多其他傳動系統油液從保養項目中消失。到2024年底,中國將有3,140萬輛新能源汽車上路,比上年成長51.49%。國際能源總署(IEA)預測,到2030年,全球電動車保有量將超過2.5億輛,屆時石油需求將減少高達430萬桶/日。然而,電動車也催生了新的細分市場,例如用於馬達軸承的酯類潤滑脂、介電冷卻液以及針對高轉速和電磁相容性最佳化的齒輪潤滑脂。供應商面臨的挑戰是如何從追求銷售轉向追求價值,因為特種油液的價格是傳統機油的兩到三倍。

細分市場分析

到2025年,機油將佔汽車潤滑油市場規模的58.24%,由於其在火星點火式和壓燃式引擎中的廣泛應用,將支撐整個汽車潤滑油市場。輕型卡車和非公路機械的大容量油底殼進一步擴大了機油的市場佔有率。變速箱油、液壓油和齒輪油的應用範圍相對有限,但對於手排變速箱、濕式煞車和動力方向盤系統仍然至關重要。潤滑脂在汽車潤滑油市場中所佔佔有率雖小,但成長速度最快,複合年成長率達4.12%,這主要得益於電動車(EV)對專用軸承潤滑脂的需求不斷成長,因為電動車需要高轉速和應對電點蝕。供應商透過在產品中添加合成酯和聚脲增稠劑來提高導電性和熱穩定性,從而提升產品價值。

隨著符合API SQ標準的潤滑油的廣泛應用,該細分市場的收入正向合成潤滑油轉移。超低黏度配方,例如0W-16和0W-12潤滑油,使汽車製造商能夠滿足車隊平均二氧化碳排放目標,尤其是在日本和歐洲。在重質燃油領域,從15W-40到5W-30潤滑油的轉變,清楚地表明了市場對低黏度、高高溫高剪切黏度(HTHS)混合油的需求,這類混合油有助於降低燃油成本。隨著黏度等級範圍的縮小,添加劑配方也日趨多樣化。硼酯、二硫化鉬和無灰清潔劑被視為下一代產品的關鍵技術。汽車潤滑油市場正在努力平衡銷售下滑與單位利潤率提升之間的關係。

汽車潤滑油市場報告按產品類型(引擎油、變速箱油和齒輪油、液壓油、潤滑脂)、車輛類型(乘用車、商用車、摩托車)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行分析。

區域分析

預計到2025年,亞太地區將以42.10%的市佔率引領汽車潤滑油市場,並在2031年之前維持4.10%的年均成長率。光是中國一地,2024年汽車保有量就將達到4.53億輛,新增註冊量將達3,583萬輛。龐大的工廠加註需求以及龐大的市場規模正在推動市場成長。東協各國政府正致力於發展電動車組裝基地,而泰國的東部經濟走廊計畫促使殼牌公司將泰國的潤滑脂產能提高了兩倍,從而確保了區域供應的穩定。在越南和印尼,摩托車擁有率超過70%,這支撐了對摩托車潤滑油的需求。

北美地區正推動著緩慢但穩定的成長。電動車年銷量超過140萬輛,但到2030年,其在汽車運作中的佔比仍將低於8%,內燃機汽車保有量仍將保持大規模。隨著汽車製造商推薦使用API SQ合成機油,並將換油週期延長至1萬英里以上,QuickLub連鎖店正在更新其庫存,引入黏度更低的機油配方。

在歐洲,車齡在18至28年之間的車輛將支撐潤滑油的需求,即便新車註冊量保持穩定。該地區在應對二氧化碳排放法規方面採取的先鋒措施,推動了符合PSA、VW 508/509和ACEA C6標準的0W-20和0W-16機油的普及。長達3萬公里的保養週期將透過鼓勵消費者購買高階機油,在一定程度上抵消銷售量下滑的影響。

中東、非洲和南美洲目前在全球整體銷售量中所佔比例較小,但成長潛力巨大。 VivoEnergy將自有品牌潤滑油產品拓展至23個非洲國家,以及殼牌收購印度Raj Petro,都凸顯了南南競爭的動態。基礎設施建設、農業機械化和採礦計劃催生了對能夠耐受多塵和高溫環境的液壓油和重型引擎油的需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 主要經濟體的平均車輛車齡不斷增加

- 新興市場全球汽車保有量成長

- 疫情後OEM工廠灌裝量的恢復情形

- 快速過渡到低黏度合成油

- 在非洲和東南亞的本地配方投資

- 市場限制

- 加速推廣電動車

- 假冒和摻假的機油

- OEM長期更換週期規範

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 依產品類型

- 機油

- 變速箱油和齒輪油

- 油壓

- 潤滑脂

- 按車輛類型

- 搭乘用車

- 商用車輛

- 摩托車

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 泰國

- 馬來西亞

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 埃及

- 奈及利亞

- 南非

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AMSOIL Inc.

- Bharat Petroleum Corporation Limited

- BP plc(Castrol)

- Chevron Corporation

- China National Petroleum Corporation(CNPC)

- China Petroleum & Chemical Corporation

- ENEOS

- Exxon Mobil Corporation

- FUCHS

- Gazprom Neft PJSC

- Gulf Oil International Ltd

- Hindustan Petroleum Corporation Limited

- Idemitsu Kosan Co.,Ltd.

- Indian Oil Corporation Ltd

- Lukoil

- Motul

- Petrobras

- PETRONAS Lubricants International

- Phillips 66 Company

- PT Pertamina Lubricants

- Repsol

- Saudi Arabian Oil Co.

- Shell plc

- SK Lubricants Co. Ltd.

- TotalEnergies

- Veedol International

第7章 市場機會與未來展望

The Automotive Lubricants Market was valued at 23.23 billion liters in 2025 and estimated to grow from 24.1 billion liters in 2026 to reach 28.99 billion liters by 2031, at a CAGR of 3.76% during the forecast period (2026-2031).

Growth is anchored by an aging global vehicle parc in developed regions, a steady influx of two-wheelers and commercial vehicles in emerging economies, and the sector's pivot toward premium synthetics that improve fuel economy and extend drain intervals. Asia-Pacific remains the core demand center thanks to rising ownership levels and local manufacturing investments, while North America and Europe rely on vehicle longevity to sustain aftermarket sales. Competitive intensity stays moderate: Shell led for the 18th straight year in 2024, but regional blenders gain ground through local capacity additions and tailored formulations. Headwinds such as accelerating electric-vehicle (EV) penetration-31.4 million units on Chinese roads in 2024-and OEM-specified long-drain intervals are mitigated by the higher unit values of API SQ and similar low-viscosity synthetics.

Global Automotive Lubricants Market Trends and Insights

Growing Average Vehicle Age in Major Economies

Vehicle longevity is reshaping lubricant demand profiles. Semiconductor shortages and inflation have slowed vehicle replacement rates in the US, prompting owners to increase oil-change frequency and invest in higher-quality synthetic oils. Europe's fleet is even older-18.1 years in the West and 28.4 years in the East-driving more workshop visits and raising per-vehicle lubricant consumption. Older engines suffer seal degradation, thermal stress, and contamination, all of which accelerate oil degradation and spur demand for premium base stocks. Maintenance outlays for vehicles aged 6-15 years rose from USD 514 to USD 537 in just one year, underscoring the link between age and spend. Scrappage has fallen to 4.20%, the lowest in two decades, prolonging aftermarket revenue streams. Higher-value synthetics now dominate service bays as owners seek extended protection and lower total cost of ownership.

Rising Global Vehicle Parc in Emerging Markets

Emerging economies offset EV-related volume erosion in mature markets. China's motor-vehicle stock reached 453 million units, supported by 35.83 million new registrations in 2024. Two-wheeler ownership continues to surge in India and Southeast Asia, propelled by urban congestion relief and affordable mobility. Commercial fleets running e-commerce and last-mile delivery routes accumulate higher mileage, boosting drain-frequency multiples. Domestic automakers in these regions collaborate with local blenders, allowing agile development of cost-effective oils tailored to varied fuel quality and climate extremes. As a result, the automotive lubricants market keeps expanding even amid global moderation.

Accelerating EV Penetration

EVs remove crankcase oils and many driveline fluids from service menus. China logged 31.4 million new-energy vehicles on its roads by end-2024, up 51.49% year-on-year. The IEA projects global stock could eclipse 250 million by 2030, cutting oil demand by up to 4.3 million bbl/d. Nonetheless, EVs introduce new niches: esters for e-motor bearings, dielectric coolants, and gear greases optimized for high RPM and electromagnetic compatibility. For suppliers, the challenge shifts from volume to value as specialized fluids command two-to-three-fold price premiums over conventional engine oil.

Other drivers and restraints analyzed in the detailed report include:

- OEM Factory-Fill Volume Recovery Post-Pandemic

- Local Blending Investments in Africa and SE Asia

- OEM Long-Drain Interval Specifications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Engine oil held 58.24% of 2025 volumes, anchoring the automotive lubricants market through ubiquitous use in spark-ignition and compression-ignition engines. Larger sump capacities in light trucks and off-highway machinery amplify its share. Transmission fluids, hydraulic oils, and gear oils serve narrower applications yet remain vital for manual boxes, wet brakes, and power-steering circuits. Greases, though just a fraction of the automotive lubricants market size, are the fastest riser at a 4.12% CAGR as EVs require dedicated bearing greases that handle high RPM and electrical pitting. Suppliers blend synthetic esters and polyurea thickeners to deliver conductivity control and thermal stability, elevating product mix value.

The segment's revenue mix swings toward synthetics as API SQ-compliant oils gain traction. Ultra-low viscosity formulations such as 0W-16 and 0W-12 enable OEMs to meet fleet-average CO2 targets, especially in Japan and Europe. Even within heavy-duty oils, the shift from 15W-40 to 5W-30 illustrates demand for thinner, high-HTHS blends that cut fuel costs. As viscosity grades narrow, additive packages diversify-boron esters, molybdenum disulfide, and ashless detergents become cornerstones in next-generation SKUs. The automotive lubricants market therefore balances declining unit volumes against richer per-unit margins.

The Automotive Lubricants Market Report is Segmented by Product Type (Engine Oil, Transmission and Gear Oil, Hydraulic Fluids, Greases), Vehicle Type (Passenger Vehicles, Commercial Vehicles, Motorcycles), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa).

Geography Analysis

Asia-Pacific dominated the automotive lubricants market with a 42.10% share in 2025 and is forecast to grow 4.10% per year through 2031. China alone hosts 453 million vehicles and recorded 35.83 million new registrations in 2024, pairing vast factory-fill demand with a colossal service marketplace. ASEAN governments nurture EV assembly hubs; Thailand's Eastern Economic Corridor plans drove Shell to triple Thai grease capacity, ensuring regional supply resilience. Two-wheeler penetration surpasses 70% of households in Vietnam and Indonesia, bolstering motorcycle-oil volumes.

North America contributes to stable if modest growth. EV sales exceed 1.40 million units annually yet remain below 8% of in-service vehicles, preserving a sizeable internal-combustion fleet through 2030. OEMs emphasize API SQ synthetics with drain intervals topping 10,000 miles, prompting quick-lube chains to upgrade inventories to low-viscosity formulations.

Europe's 18-28 year car fleet sustains lubricant demand despite flat new-car registrations. The continent pioneers CO2 cap compliance, spurring adoption of 0W-20 and 0W-16 oils backed by PSA, VW 508/509, and ACEA C6 specifications. Extended-service intervals of up to 30,000 km partially offset volume loss by encouraging premium-grade purchases.

The Middle East & Africa and South America jointly contribute a smaller share of the global volume today but deliver outsized upside. Vivo Energy's branded-lube expansion across 23 African nations and Shell's Raj Petro acquisition in India highlight a south-south competitive trend. Infrastructure build-out, agricultural mechanization, and mining projects generate demand for hydraulic fluids and heavy-duty engine oils resilient to dust and high ambient temperatures.

- AMSOIL Inc.

- Bharat Petroleum Corporation Limited

- BP p.l.c. (Castrol)

- Chevron Corporation

- China National Petroleum Corporation (CNPC)

- China Petroleum & Chemical Corporation

- ENEOS

- Exxon Mobil Corporation

- FUCHS

- Gazprom Neft PJSC

- Gulf Oil International Ltd

- Hindustan Petroleum Corporation Limited

- Idemitsu Kosan Co.,Ltd.

- Indian Oil Corporation Ltd

- Lukoil

- Motul

- Petrobras

- PETRONAS Lubricants International

- Phillips 66 Company

- PT Pertamina Lubricants

- Repsol

- Saudi Arabian Oil Co.

- Shell plc

- SK Lubricants Co. Ltd.

- TotalEnergies

- Veedol International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing average vehicle age in major economies

- 4.2.2 Rising global vehicle parc in emerging markets

- 4.2.3 OEM factory-fill volume recovery post-pandemic

- 4.2.4 Rapid shift toward lower-viscosity synthetics

- 4.2.5 Local blending investments in Africa and SE Asia

- 4.3 Market Restraints

- 4.3.1 Accelerating EV penetration

- 4.3.2 Counterfeit and adulterated engine oils

- 4.3.3 OEM long-drain interval specifications

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Engine Oil

- 5.1.2 Transmission and Gear Oil

- 5.1.3 Hydraulic Fluids

- 5.1.4 Greases

- 5.2 By Vehicle Type

- 5.2.1 Passenger Vehicles

- 5.2.2 Commercial Vehicles

- 5.2.3 Motorcycles

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Thailand

- 5.3.1.7 Malaysia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 AMSOIL Inc.

- 6.4.2 Bharat Petroleum Corporation Limited

- 6.4.3 BP p.l.c. (Castrol)

- 6.4.4 Chevron Corporation

- 6.4.5 China National Petroleum Corporation (CNPC)

- 6.4.6 China Petroleum & Chemical Corporation

- 6.4.7 ENEOS

- 6.4.8 Exxon Mobil Corporation

- 6.4.9 FUCHS

- 6.4.10 Gazprom Neft PJSC

- 6.4.11 Gulf Oil International Ltd

- 6.4.12 Hindustan Petroleum Corporation Limited

- 6.4.13 Idemitsu Kosan Co.,Ltd.

- 6.4.14 Indian Oil Corporation Ltd

- 6.4.15 Lukoil

- 6.4.16 Motul

- 6.4.17 Petrobras

- 6.4.18 PETRONAS Lubricants International

- 6.4.19 Phillips 66 Company

- 6.4.20 PT Pertamina Lubricants

- 6.4.21 Repsol

- 6.4.22 Saudi Arabian Oil Co.

- 6.4.23 Shell plc

- 6.4.24 SK Lubricants Co. Ltd.

- 6.4.25 TotalEnergies

- 6.4.26 Veedol International

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車懸吊系統潤滑油市場規模、佔有率和成長分析:按產品類型、應用、車輛類型、最終用戶和地區分類-2026-2033年產業預測

汽車懸吊系統潤滑油市場規模、佔有率和成長分析:按產品類型、應用、車輛類型、最終用戶和地區分類-2026-2033年產業預測 汽車潤滑油市場:2026-2032年全球市場預測(依產品類型、基礎油類型、黏度等級、包裝、車輛類型及通路分類)非公路設備潤滑油市場:依產品類型、基礎油類型、設備類型、最終用途產業、應用與銷售管道分類-2026-2032年全球市場預測

汽車潤滑油市場:2026-2032年全球市場預測(依產品類型、基礎油類型、黏度等級、包裝、車輛類型及通路分類)非公路設備潤滑油市場:依產品類型、基礎油類型、設備類型、最終用途產業、應用與銷售管道分類-2026-2032年全球市場預測 汽車潤滑油市場規模、佔有率、趨勢和預測:按產品類型、車輛類型和地區分類,2026-2034年乘用車潤滑油市場:2026-2032年全球市場預測(依產品類型、基礎油類型、黏度等級、車輛類型及通路分類)商用車潤滑油市場:2026-2032年全球市場預測(依基礎油類型、潤滑油類型、車輛類型、黏度等級、應用與銷售管道)

汽車潤滑油市場規模、佔有率、趨勢和預測:按產品類型、車輛類型和地區分類,2026-2034年乘用車潤滑油市場:2026-2032年全球市場預測(依產品類型、基礎油類型、黏度等級、車輛類型及通路分類)商用車潤滑油市場:2026-2032年全球市場預測(依基礎油類型、潤滑油類型、車輛類型、黏度等級、應用與銷售管道) 汽車潤滑油市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

汽車潤滑油市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 汽車潤滑油市場:依產品類型、通路、車輛類型、國家及地區分類-產業分析、市場規模、市場佔有率及2025年至2032年預測

汽車潤滑油市場:依產品類型、通路、車輛類型、國家及地區分類-產業分析、市場規模、市場佔有率及2025年至2032年預測 汽車潤滑油市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材質類型、介紹形式、最終用戶、功能

汽車潤滑油市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材質類型、介紹形式、最終用戶、功能 美國汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)