|

市場調查報告書

商品編碼

1937381

美國汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Automotive Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

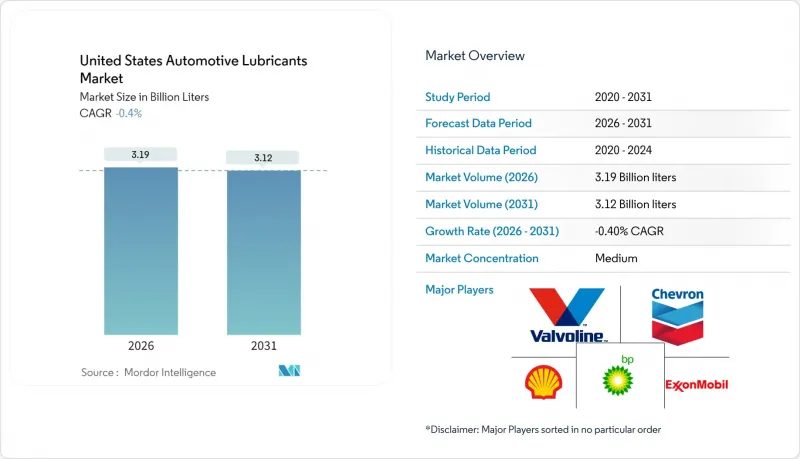

預計到 2026 年,美國汽車潤滑油市場規模將達到 31.9 億公升。

預計這一數字將從 2025 年的 32 億公升下降到 2031 年的 31.2 億公升,2026 年至 2031 年的年複合成長率(CAGR)為 -0.40%。

更嚴格的燃油經濟性法規、延長換油週期技術以及加速發展的電氣化趨勢,正推動產品結構向利潤更高的合成油傾斜,同時持續抑制總需求。商用車隊正採用預測分析技術,將換油週期從3000英里延長至15,000英里。這降低了散裝油的需求,同時提高了高階配方油的單升收益。原始設備製造商(OEM)正將自身的潤滑油標準納入車輛保固條款,並與擁有強大研發能力的供應商簽訂工廠填充合約。 III類和IV類基礎油的供應瓶頸和添加劑短缺,壓縮了調配商的利潤空間,但也增強了能夠保證品質和供應穩定性的成熟品牌的定價權。同時,由勝牌、雪佛龍、殼牌和嘉實多等公司組成的潤滑油包裝管理協會(LPMA)等行業合作表明,合規性已成為共用成本,而非競爭優勢。

美國汽車潤滑油市場趨勢與洞察

嚴格的CAFE/GHG標準推動低黏度合成油的過渡

企業平均燃油經濟性 (CAFE) 法規要求到 2026 年,所有車輛的燃油經濟性每年提高 5%,這迫使汽車製造商從 5W-30 機油過渡到 0W-20 甚至 0W-16 機油。這些機油等級都高度依賴 III 或 IV 類合成油,以在更薄的油膜厚度下保持磨損保護。這種過渡最大限度地減少了內部摩擦損失,並降低了每輛車的潤滑油需求。然而,這些超低黏度機油固有的較高原料成本和先進添加劑配方推高了平均售價,從而為能夠配製出符合 OEM核准的化學配方的生產商創造了價值。鑑於加州新車註冊量佔比龐大,其提前實施該法規將加速區域發展。埃克森美孚和殼牌等主要供應商正在投資研發先進的抗氧化劑和摩擦改進劑,以保持領先於不斷變化的標準。最終形成了一個高利潤、低銷售量的環境,獎勵創新和監管前瞻性。

OEM工廠灌裝規格推動了對優質潤滑油的需求

汽車製造商擴大將特定品牌的潤滑油要求納入保固條款,並將部分品質保證工作委託給值得信賴的潤滑油合作夥伴。通用汽車的Dexos認證和福特的WSS-M2C系列認證等項目要求供應商在核准前必須經過廣泛的台架測試、引擎測功機測試和現場測試。例如,嘉實多供應全球約四分之三的OEM原廠潤滑油,並利用其品牌優勢實現高利潤的售後服務加註。混合動力傳動系統的出現使情況更加複雜,因為其需要添加防腐蝕添加劑,而這些添加劑在頻繁的啟動停止循環中可能會導致水汽凝結。雪佛龍最近獲得了一項針對混合動力引擎此類化學添加劑的歐洲專利。這些技術壁壘阻礙了新市場進入,並加強了OEM與現有配方商之間的聯繫,因為這些配方商能夠滿足專門的測試標準。

電動動力傳動系統的普及將從根本上降低對內燃機油的需求。

電池式電動車(BEV) 的銷量顯著成長,佔據了國內輕型汽車銷量的相當大佔有率,並徹底消除了此類車輛對曲軸箱潤滑油的需求。插電混合動力汽車由於部分里程依靠電力驅動,進一步降低了潤滑油的需求,減少了 30% 至 50% 的潤滑油用量。各州的零排放法規,特別是加州到 2035 年實現 100% 零排放汽車銷售的目標,正在加速需求成長。用於電池冷卻和電力驅動橋齒輪的特殊潤滑油正在出現,但其用量仍遠低於傳統內燃機的用量。為了規避這一風險,多個領域的供應商正在將業務多元化,進入工業和船舶潤滑油領域,或開拓新興的電動汽車潤滑油細分市場,這些市場需要矽基冷卻液和介電潤滑脂。

細分市場分析

截至2025年,汽車機油占美國汽車潤滑油市場的60.10%。儘管汽油和柴油引擎的裝置量有所下降,但其龐大的基數確保了對曲軸箱定期保養的持續需求。混合動力汽車也消耗少量引擎油,從而維持了其核心需求。同時,汽車製造商強制要求使用0W-20和0W-16黏度等級的機油,推高了每誇脫機油的平均價格。在這一類別中,同時滿足低黏度和長壽命要求的全合成機油成長最快。同時,由於現代多速變速箱結構複雜,需要使用獨特的摩擦改進劑配方,美國汽車潤滑油市場中自動變速箱油(ATF)的市場規模預計只會略有萎縮。手排變速箱油 (MTF) 和煞車油雖然絕對噸位較小,但也會經歷類似的下降,其中 DOT 3 和 DOT 4 油的需求保持穩定,因為混合動力汽車和純電動車 (BEV) 仍然需要液壓煞車系統。

合成潤滑脂的應用逆勢而上,盧卡斯石油公司於2024年在印第安納州新增了25,000平方英尺的潤滑脂產能,專注於其「Red & Tacky」系列磺酸磺酸鹽增稠劑的生產,該系列產品可規避鋰皂的供應限制。此次擴建不僅將緩解疫情期間的供不應求,還將促進售後市場從通用鋰基潤滑脂向非公路用車輛專用重型潤滑脂的轉換。同時,新興的電動車溫度控管液細分市場,例如奈米填充的乙二醇基冷卻液,將開闢新的研發途徑,但對總銷量的貢獻甚微,這凸顯了未來成長領域與現有領域衰退之間的不對稱性。

美國汽車潤滑油市場報告按產品類型(汽車引擎油、手排變速箱油、自動變速箱油、煞車油、汽車潤滑脂及其他產品類型)和車輛類型(乘用車、商用車和摩托車)進行細分。市場預測以公升為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 嚴格的CAFE/GHG標準推動低黏度合成油的過渡

- 由於OEM工廠填充規格的擴大,對優質潤滑油的需求增加。

- 船隊數位化輔助數據驅動油品延壽服務

- 與遠端資訊處理技術相關的維護合約推動了售後市場需求。

- 生物基添加劑創新降低廢油毒性

- 市場限制

- 電動車動力傳動系統的普及從根本上降低了對內燃機引擎油的需求。

- 延長換油週期可降低每輛車的潤滑油消耗。

- 原料價格波動對攪拌機的利潤率帶來壓力。

- 價值鍊和通路分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- 法律規範

- 汽車產業的趨勢

第5章 市場規模與成長預測

- 依產品類型

- 汽車引擎油

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 單黏度油

- 其他年級

- 手排變速箱油(MTF)

- 自排變速箱油(ATF)

- 煞車油

- 汽車潤滑脂

- 其他產品類型(動力方向盤機油等)

- 汽車引擎油

- 按車輛類型

- 搭乘用車

- 商用車輛

- 摩托車

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AMSOIL INC.

- Bardahl Manufacturing Corporation

- BP plc

- Chevron Corporation

- CITGO Petroleum Lubricants

- ENEOS Corporation

- ExxonMobil Corporation

- FUCHS

- Gulf Oil International

- HollyFrontier(Petro-Canada Lubricants)

- Idemitsu Lubricants America

- Lucas Oil Products, Inc.

- Motul

- Phillips 66 Company

- Shell plc

- TotalEnergies

- Saudi Arabian Co. Ltd

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

United States Automotive Lubricants Market size in 2026 is estimated at 3.19 billion liters, growing from 2025 value of 3.20 billion liters with 2031 projections showing 3.12 billion liters, growing at -0.40% CAGR over 2026-2031.

A combination of aggressive fuel-economy mandates, extended oil-drain technologies, and accelerating electrification continues to pressure total volumes even as it shifts the product mix toward high-margin synthetics. Commercial fleets deploy predictive analytics that can stretch oil-change intervals from 3,000 miles to as high as 15,000 miles, a move that reduces bulk demand but increases revenue per liter due to premium formulations. Original-equipment manufacturers (OEMs) embed proprietary lube standards in vehicle warranties, locking in factory-fill contracts for suppliers with deep research capabilities. Supply bottlenecks for Group III and Group IV base oils, combined with additive shortages, squeeze blender margins but also reinforce the pricing power of established brands that can guarantee quality and continuity of supply. Meanwhile, collaborative industry responses, such as the Lubricant Packaging Management Association formed by Valvoline, Chevron, Shell, and Castrol, illustrate how regulatory compliance has become a shared cost center rather than a competitive wedge

United States Automotive Lubricants Market Trends and Insights

Stringent CAFE/GHG Standards Driving Shift to Low-Viscosity Synthetics

Corporate Average Fuel Economy (CAFE) rules require fleet-wide efficiency improvements of 5% annually through 2026, prompting automakers to transition from 5W-30 to 0W-20 and even 0W-16 grades, each of which relies heavily on Group III or Group IV synthetics to maintain wear protection at thinner film thicknesses. The transition reduces per-vehicle lubricant demand by minimizing internal friction losses. However, the higher raw-material costs and sophisticated additive recipes inherent in these ultralow viscosities raise average selling prices, enhancing value capture for producers able to formulate to OEM-approved chemistries. California's early enforcement adds a regional accelerator, given its large share of new-vehicle registrations. Key suppliers such as ExxonMobil and Shell invest in advanced antioxidants and friction modifiers to stay ahead of specification upgrades. The net result is a margin-rich but volume-light environment that rewards innovation and regulatory foresight.

OEM Factory-Fill Specifications Expanding Premium Lubricant Demand

Vehicle makers increasingly embed branded fluid requirements into warranty language, effectively outsourcing part of their quality assurance to trusted lubricant partners. Programs such as General Motors' Dexos and Ford's WSS-M2C series force suppliers through extensive bench, engine-dyno, and field trials before approval. Castrol, for instance, supplies roughly three-quarters of global OEM factory fills, leveraging the brand advantage into high-margin service-fill sales. Hybrid powertrains complicate matters further by introducing water condensation during repeated start-stop cycles, requiring corrosion-inhibiting additive blends; Chevron recently secured a European patent covering such chemistry for hybrid engines. These technical hurdles deter new entrants and tighten the bond between OEMs and the established formulators capable of meeting exotic test matrices.

EV Power-Train Adoption Structurally Reducing ICE Engine-Oil Volumes

Battery-electric vehicle (BEV) sales increased significantly, accounting for a considerable share of national light-duty sales, eliminating crankcase oil demand in those cars outright. Plug-in hybrids further dilute the need by relying on electric drive for a portion of miles traveled, trimming lubricant usage by 30-50%. State zero-emission mandates, notably California's 2035 target for 100% ZEV sales, pull demand forward. Although specialized fluids for battery cooling and e-axle gears emerge, their unit volumes remain a fraction of what internal-combustion engines historically absorbed. To hedge, multi-segment suppliers diversify into industrial and marine lubricants or chase nascent EV fluid niches that demand silicon-based coolants and dielectric greases.

Other drivers and restraints analyzed in the detailed report include:

- Fleet Digitalization Enabling Data-Driven Oil-Life Extension Services

- Telematics-Linked Maintenance Contracts Boosting Aftermarket Volumes

- Extended Drain Intervals Cutting Per-Vehicle Lubricant Consumption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive engine oil retained 60.10% of the US automotive lubricants market share in 2025. The large installed base of gasoline and diesel engines guarantees a continuing, if tapering, need for routine crankcase service. Hybrid vehicles still consume engine oil, though in smaller quantities, preserving a core demand bedrock while OEM mandates for 0W-20 and 0W-16 grades lift the average price per quart. Within this category, full synthetics expand fastest because they meet low-viscosity and extended-life requirements simultaneously. In parallel, the US automotive lubricants market size for automatic transmission fluids contracts only slightly, buoyed by the complexity of modern multi-speed gearboxes that rely on proprietary friction-modifier blends. Manual transmission fluids and brake fluids, though smaller in absolute tonnage, decline at similar rates because hybrids and BEVs still require hydraulic brake systems that maintain stable demand for DOT 3 and DOT 4 fluids.

Synthetic grease applications bucked the downtrend after Lucas Oil brought an additional 25,000 square feet of grease capacity online in Indiana in 2024, focusing on calcium-sulfonate thickened Red 'N' Tacky products that bypassed lithium-soap supply constraints. The expansion not only alleviates pandemic-era shortages but also catalyzes aftermarket conversions from multipurpose lithium grease to higher-load alternatives favored by off-highway fleets. Meanwhile, the emerging niche for EV thermal-management fluids-glycol-based coolants augmented with nano-fillers-creates new research and development pathways but contributes little to headline volume, illustrating the asymmetry between future growth pockets and legacy decline.

The US Automotive Lubricants Market Report is Segmented by Product Type (Automotive Engine Oil, Manual Transmission Fluids, Automatic Transmission Fluids, Brake Fluids, Automotive Greases, and Other Product Types), and Vehicle Type (Passenger Vehicles, Commercial Vehicles, and Two-Wheelers). The Market Forecasts are Provided in Terms of Volume (Litres).

List of Companies Covered in this Report:

- AMSOIL INC.

- Bardahl Manufacturing Corporation

- BP p.l.c.

- Chevron Corporation

- CITGO Petroleum Lubricants

- ENEOS Corporation

- ExxonMobil Corporation

- FUCHS

- Gulf Oil International

- HollyFrontier (Petro-Canada Lubricants)

- Idemitsu Lubricants America

- Lucas Oil Products, Inc.

- Motul

- Phillips 66 Company

- Shell plc

- TotalEnergies

- Saudi Arabian Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent CAFE/GHG standards driving shift to low-viscosity synthetics

- 4.2.2 OEM factory-fill specifications expanding premium lubricant demand

- 4.2.3 Fleet digitalisation enabling data-driven oil-life extension services

- 4.2.4 Telematics-linked maintenance contracts boosting aftermarket volumes

- 4.2.5 Bio-based additive breakthroughs lowering toxicity of spent oils

- 4.3 Market Restraints

- 4.3.1 EV power-train adoption structurally reducing ICE engine-oil volumes

- 4.3.2 Extended drain intervals cutting per-vehicle lubricant consumption

- 4.3.3 Volatile base-oil feedstock prices squeezing blender margins

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Regulatory Framework

- 4.7 Automotive Industry Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.1.1 0W-XX

- 5.1.1.2 5W-XX

- 5.1.1.3 10W-XX

- 5.1.1.4 15W-XX

- 5.1.1.5 Monogrades

- 5.1.1.6 Other Grades

- 5.1.2 Manual Transmission Fluids (MTF)

- 5.1.3 Automatic Transmission Fluids (ATF)

- 5.1.4 Brake Fluids

- 5.1.5 Automotive Greases

- 5.1.6 Other Product Types (Power Steering Fluid etc.)

- 5.1.1 Automotive Engine Oil

- 5.2 By Vehicle Type

- 5.2.1 Passenger Vehicles

- 5.2.2 Commercial Vehicles

- 5.2.3 Two-Wheelers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Production Capacity, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AMSOIL INC.

- 6.4.2 Bardahl Manufacturing Corporation

- 6.4.3 BP p.l.c.

- 6.4.4 Chevron Corporation

- 6.4.5 CITGO Petroleum Lubricants

- 6.4.6 ENEOS Corporation

- 6.4.7 ExxonMobil Corporation

- 6.4.8 FUCHS

- 6.4.9 Gulf Oil International

- 6.4.10 HollyFrontier (Petro-Canada Lubricants)

- 6.4.11 Idemitsu Lubricants America

- 6.4.12 Lucas Oil Products, Inc.

- 6.4.13 Motul

- 6.4.14 Phillips 66 Company

- 6.4.15 Shell plc

- 6.4.16 TotalEnergies

- 6.4.17 Saudi Arabian Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

汽車懸吊系統潤滑油市場規模、佔有率和成長分析:按產品類型、應用、車輛類型、最終用戶和地區分類-2026-2033年產業預測

汽車懸吊系統潤滑油市場規模、佔有率和成長分析:按產品類型、應用、車輛類型、最終用戶和地區分類-2026-2033年產業預測 汽車潤滑油市場:2026-2032年全球市場預測(依產品類型、基礎油類型、黏度等級、包裝、車輛類型及通路分類)非公路設備潤滑油市場:依產品類型、基礎油類型、設備類型、最終用途產業、應用與銷售管道分類-2026-2032年全球市場預測

汽車潤滑油市場:2026-2032年全球市場預測(依產品類型、基礎油類型、黏度等級、包裝、車輛類型及通路分類)非公路設備潤滑油市場:依產品類型、基礎油類型、設備類型、最終用途產業、應用與銷售管道分類-2026-2032年全球市場預測 汽車潤滑油市場規模、佔有率、趨勢和預測:按產品類型、車輛類型和地區分類,2026-2034年乘用車潤滑油市場:2026-2032年全球市場預測(依產品類型、基礎油類型、黏度等級、車輛類型及通路分類)商用車潤滑油市場:2026-2032年全球市場預測(依基礎油類型、潤滑油類型、車輛類型、黏度等級、應用與銷售管道)

汽車潤滑油市場規模、佔有率、趨勢和預測:按產品類型、車輛類型和地區分類,2026-2034年乘用車潤滑油市場:2026-2032年全球市場預測(依產品類型、基礎油類型、黏度等級、車輛類型及通路分類)商用車潤滑油市場:2026-2032年全球市場預測(依基礎油類型、潤滑油類型、車輛類型、黏度等級、應用與銷售管道) 汽車潤滑油市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

汽車潤滑油市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 汽車潤滑油市場:依產品類型、通路、車輛類型、國家及地區分類-產業分析、市場規模、市場佔有率及2025年至2032年預測

汽車潤滑油市場:依產品類型、通路、車輛類型、國家及地區分類-產業分析、市場規模、市場佔有率及2025年至2032年預測 汽車潤滑油市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材質類型、介紹形式、最終用戶、功能

汽車潤滑油市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材質類型、介紹形式、最終用戶、功能 汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)