|

市場調查報告書

商品編碼

1937382

越南汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Automotive Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

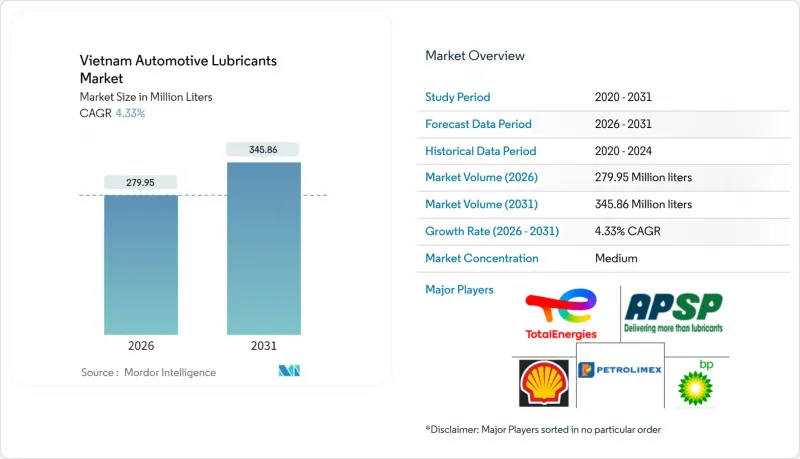

越南汽車潤滑油市場在 2025 年的價值為 2.6834 億公升,預計到 2031 年將達到 3.4586 億公升,而 2026 年為 2.7995 億公升。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.33%。

強勁的貨運活動、老化的車輛以及不斷擴大的電商車隊正在支撐市場成長。同時,電氣化政策正在重塑長期需求結構。 Petrolimex 的經銷網路優勢,加上殼牌、BP/嘉實多和摩特等公司在本地配方方面的投資,在維持供應韌性的同時,也促進了市場差異化競爭。優質合成油的快速普及、汽車製造商對延長保養週期的強制性要求以及對仿冒品的更嚴格打擊,正在推高平均售價並擴大利潤率。同時,河內即將禁止石化燃料摩托車在環城公路一號線內行駛,以及胡志明市引入低排放氣體區的舉措,都預示著傳統摩托車的需求將面臨監管壓力。

越南汽車潤滑油市場趨勢及分析

車隊規模的擴大和車齡的增加將繼續推動對潤滑油的需求。

越南的車輛登記數量持續增加。車齡超過七年的車型比例不斷上升,由於劣化和竄氣等問題,需要更頻繁地更換機油。卡車運輸仍然高度分散,大多數商用車輛的噸位低於五噸,每家公司的平均車隊規模僅為五輛車,導致維修事故頻繁發生。儘管面臨電氣化趨勢帶來的不利影響,但上述因素共同推動越南汽車潤滑油市場維持銷售成長的趨勢。

摩托車市場動態影響都市區潤滑油的消費

預計越南將在2025年成為全球第二大電動摩托車市場,而本田預計同年將售出220萬輛內燃機摩托車。遍布路邊的洗車場提供的定期機油保養服務導致潤滑油消耗量龐大。儘管一些監管禁令,例如河內市計劃於2026年禁止石化燃料摩托車在1號環城公路上行駛,開始降低都市區的需求,但其他地區龐大的車輛運作量預計將確保越南的汽車潤滑油市場在2030年之前繼續得到摩托車需求的銷售量。

電動車的普及將加速內燃機的淘汰。

VinFast計劃在2024年交付97,399輛電池式電動車,並力爭在2025年達到150,700輛。由於純電動車無需使用引擎油,並降低了變速箱油的需求,越南汽車潤滑油市場正面臨結構性需求下滑,尤其是在都市區車隊領域。然而,溫度控管冷卻液和專用電子潤滑脂正在開闢新的高附加價值細分市場。

細分市場分析

截至2025年,汽車機油佔越南汽車潤滑油市場佔有率的52.88%。其在乘用車、摩托車和卡車中的廣泛應用使其保持了銷量主導。然而,自動變速箱油(ATF)的成長速度最快,年複合成長率達4.52%,這主要得益於乘用車自動變速箱普及率的提高以及零件保固範圍的擴大。手排變速箱油在輕型卡車領域仍然佔據相當大的佔有率,而煞車油則保持著穩定的、中等偏上的個位數市場佔有率。

猖獗的假冒仿冒品迫使品牌製造商在高級產品中加入可見和不可見的安全標記,雖然增加了成本,但卻維護了品牌價值。調配商也正在將III類基礎油與高性能添加劑混合,以滿足API SP和歐盟6標準。摩特(Motul)位於越南的工廠已開始對再生基礎油混合物進行商業試驗,預計與全新II類基礎油相比,這些混合物將減少碳排放。這些技術創新增強了競爭優勢,並與越南汽車潤滑油產業日益成長的OEM夥伴關係相契合。

越南汽車潤滑油市場報告按產品類型(汽車引擎油(0W-XX、5W-XX、10W-XX、15W-XX、單一黏度等級機油及其他等級)、手動變速箱油、自動變速箱油、煞車油、汽車潤滑脂及其他產品類型)和車輛類型(乘用車、商用車、摩托車)進行細分。市場預測以公升為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 車輛擁有量和平均年齡的成長

- 摩托車在都市區交通中佔據主導地位

- 電子商務物流車輛數量快速成長

- 依原廠規定加長排水間距

- 共乘單車租賃業務快速成長

- 市場限制

- 電動車在乘用車領域的滲透率不斷提高

- 對價格敏感的消費者往往喜歡品質較低的礦物油。

- 假冒潤滑油貿易日益猖獗

- 價值鍊和通路分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

- 法律規範

- 汽車產業的趨勢

第5章 市場規模與成長預測

- 依產品類型

- 汽車引擎油

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 單黏度油

- 其他年級

- 手排變速箱油(MTF)

- 自排變速箱油(ATF)

- 煞車油

- 汽車潤滑脂

- 其他產品類型(動力方向盤機油等)

- 汽車引擎油

- 按車輛類型

- 搭乘用車

- 商用車輛

- 摩托車

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- AP SAIGON PETRO

- BP plc

- Chevron Corporation

- Exxon Mobil Corporation

- Fuchs Petrolub SE

- GS Caltex Corporation

- Idemitsu Kosan Co. Ltd

- Mekong Petrochemical Jsc

- Motul

- Petrolimex(PLX)

- PETRONAS Lubricants International

- PVOIL

- Repsol Vietnam

- Shell Plc

- TotalEnergies

- Wolf Oil Corporation

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

The Vietnam Automotive Lubricants Market was valued at 268.34 million liters in 2025 and estimated to grow from 279.95 million liters in 2026 to reach 345.86 million liters by 2031, at a CAGR of 4.33% during the forecast period (2026-2031).

Robust freight activity, an aging vehicle parc, and expanding e-commerce fleets underpin this growth, even as electrification policies begin to reshape long-term demand. Distribution dominance by Petrolimex, combined with localized blending investments from Shell, BP/Castrol, and Motul, sustains supply resiliency while intensifying competitive differentiation. The rapid adoption of premium synthetics, longer drain intervals mandated by OEMs, and stricter crackdowns on counterfeit products are increasing average selling prices and encouraging margin expansion. At the same time, Hanoi's impending ban on fossil-fuel motorcycles inside Ring Road 1 and Ho Chi Minh City's Low Emission Zone signal regulatory pressure on legacy two-wheeler demand.

Vietnam Automotive Lubricants Market Trends and Insights

Rising Vehicle Parc and Average Age Drive Sustained Lubricant Demand

National vehicle registrations continue to rise. A growing proportion of models are seven years or older, requiring more frequent oil replacements due to degradation and blow-by. Trucking remains fragmented; the majority of commercial vehicles are under 5 tons and average just five trucks per firm, which magnifies service incidents. These factors collectively sustain the Vietnam automotive lubricants market on an upward volume trajectory, despite the headwinds from the electrification trend.

Two-Wheeler Market Dynamics Shape Urban Lubricant Consumption

Although Vietnam became the world's second-largest electric two-wheeler market in 2025, Honda still projects selling 2.2 million ICE motorcycles that year. Routine oil services conducted at ubiquitous roadside washes yield high-frequency lubricant turnover. Legislated bans, such as Hanoi's 2026 exclusion of fossil-fuel motorcycles inside Ring Road 1, begin to narrow urban demand yet leave a vast in-use fleet elsewhere, allowing the Vietnam automotive lubricants market to retain two-wheeler volume support into 2030.

Electric Vehicle Adoption Accelerates ICE Displacement

VinFast shipped 97,399 battery EVs in 2024 and targets 150,700 units in 2025. Because BEVs eliminate engine oil usage and reduce transmission-fluid needs, the Vietnam automotive lubricants market faces structural demand erosion, especially in urban car fleets. Yet thermal-management coolants and specialized e-greases open new high-value niches.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Logistics Fleet Expansion Drives Commercial Lubricant Growth

- OEM Extended-Drain Interval Specifications Reshape Product Mix

- Growing Counterfeit Lubricant Trade Undermines Market Integrity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive engine oil accounted for 52.88% of the Vietnam automotive lubricants market share in 2025. Embedded usage across cars, motorcycles, and trucks ensures volume leadership. However, automatic transmission fluid (ATF) displays the steepest growth trajectory at a 4.52% CAGR, benefiting from rising passenger-car automatic transmission penetration and intensified parts-warranty compliance. Manual transmission fluid still holds a share in light-duty trucks, whereas brake fluids maintain steady mid-single-digit contributions.

Persistent counterfeit activity forces branded suppliers to embed overt and covert security markers on premium SKUs, adding costs but preserving brand equity. Blenders also incorporate Group III base oils and high-performance additive chemistries to comply with API SP and Euro 6 requirements. Motul's Vietnamese plant has begun commercial trials of Re-Refined Base Oil blends, promising a reduction in carbon footprint compared to virgin Group II stocks. These innovations reinforce competitive positioning and align with evolving OEM partnerships inside the Vietnam automotive lubricants industry.

The Vietnam Automotive Lubricants Market Report is Segmented by Product Type (Automotive Engine Oil (0W-XX, 5W-XX, 10W-XX, 15W-XX, Monogrades, and Other Grades), Manual Transmission Fluids, Automatic Transmission Fluids, Brake Fluids, Automotive Greases, and Other Product Types), and Vehicle Type (Passenger Vehicles, Commercial Vehicles, and Two-Wheelers). The Market Forecasts are Provided in Terms of Volume (Litres).

List of Companies Covered in this Report:

- AP SAIGON PETRO

- BP p.l.c.

- Chevron Corporation

- Exxon Mobil Corporation

- Fuchs Petrolub SE

- GS Caltex Corporation

- Idemitsu Kosan Co. Ltd

- Mekong Petrochemical Jsc

- Motul

- Petrolimex (PLX)

- PETRONAS Lubricants International

- PVOIL

- Repsol Vietnam

- Shell Plc

- TotalEnergies

- Wolf Oil Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising vehicle parc and average age

- 4.2.2 Two-wheeler dominance in urban mobility

- 4.2.3 Surge in e-commerce logistics fleets

- 4.2.4 OEM extended-drain interval specifications

- 4.2.5 Rapid growth of ride-hailing motorbike rentals

- 4.3 Market Restraints

- 4.3.1 Rising EV adoption in passenger-car segment

- 4.3.2 Price-sensitive consumer base favouring low-grade mineral oils

- 4.3.3 Growing counterfeit lubricant trade

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Regulatory Framework

- 4.7 Automotive Industry Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.1.1 0W-XX

- 5.1.1.2 5W-XX

- 5.1.1.3 10W-XX

- 5.1.1.4 15W-XX

- 5.1.1.5 Monogrades

- 5.1.1.6 Other Grades

- 5.1.2 Manual Transmission Fluids (MTF)

- 5.1.3 Automatic Transmission Fluids (ATF)

- 5.1.4 Brake Fluids

- 5.1.5 Automotive Greases

- 5.1.6 Other Product Types (Power Steering Fluid etc.)

- 5.1.1 Automotive Engine Oil

- 5.2 By Vehicle Type

- 5.2.1 Passenger Vehicles

- 5.2.2 Commercial Vehicles

- 5.2.3 Two-Wheelers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%) /Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Production Capacity, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AP SAIGON PETRO

- 6.4.2 BP p.l.c.

- 6.4.3 Chevron Corporation

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 Fuchs Petrolub SE

- 6.4.6 GS Caltex Corporation

- 6.4.7 Idemitsu Kosan Co. Ltd

- 6.4.8 Mekong Petrochemical Jsc

- 6.4.9 Motul

- 6.4.10 Petrolimex (PLX)

- 6.4.11 PETRONAS Lubricants International

- 6.4.12 PVOIL

- 6.4.13 Repsol Vietnam

- 6.4.14 Shell Plc

- 6.4.15 TotalEnergies

- 6.4.16 Wolf Oil Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

汽車潤滑油市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材質類型、介紹形式、最終用戶、功能

汽車潤滑油市場分析及預測(至2035年):類型、產品、服務、技術、應用、形式、材質類型、介紹形式、最終用戶、功能 汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國汽車潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球汽車潤滑油市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球汽車潤滑油市場規模、佔有率、趨勢和成長分析報告(2026-2034) 三輪車潤滑油市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、銷售管道、產品類型、地區及競爭格局分類,2021-2031年)商用車潤滑油市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、銷售管道、產品類型、地區及競爭格局分類,2021-2031年)摩托車潤滑油市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、銷售管道、產品類型、地區及競爭格局分類,2021-2031年)汽車潤滑油市場-全球產業規模、佔有率、趨勢、競爭格局、機會及預測(依車輛類型、銷售管道、產品類型、地區及競爭狀況分類,2021-2031年)乘用車潤滑油市場-全球產業規模、佔有率、趨勢、機會及預測,依車輛類型、銷售通路、產品類型、地區及競爭格局分類,2021-2031年預測

三輪車潤滑油市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、銷售管道、產品類型、地區及競爭格局分類,2021-2031年)商用車潤滑油市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、銷售管道、產品類型、地區及競爭格局分類,2021-2031年)摩托車潤滑油市場-全球產業規模、佔有率、趨勢、機會及預測(依車輛類型、銷售管道、產品類型、地區及競爭格局分類,2021-2031年)汽車潤滑油市場-全球產業規模、佔有率、趨勢、競爭格局、機會及預測(依車輛類型、銷售管道、產品類型、地區及競爭狀況分類,2021-2031年)乘用車潤滑油市場-全球產業規模、佔有率、趨勢、機會及預測,依車輛類型、銷售通路、產品類型、地區及競爭格局分類,2021-2031年預測 北美乘用車潤滑油售後市場 - 區域和國家分析:按應用、產品和地區分類 - 分析和預測(2025-2035年)

北美乘用車潤滑油售後市場 - 區域和國家分析:按應用、產品和地區分類 - 分析和預測(2025-2035年)