|

市場調查報告書

商品編碼

1939026

海運貨櫃:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Shipping Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

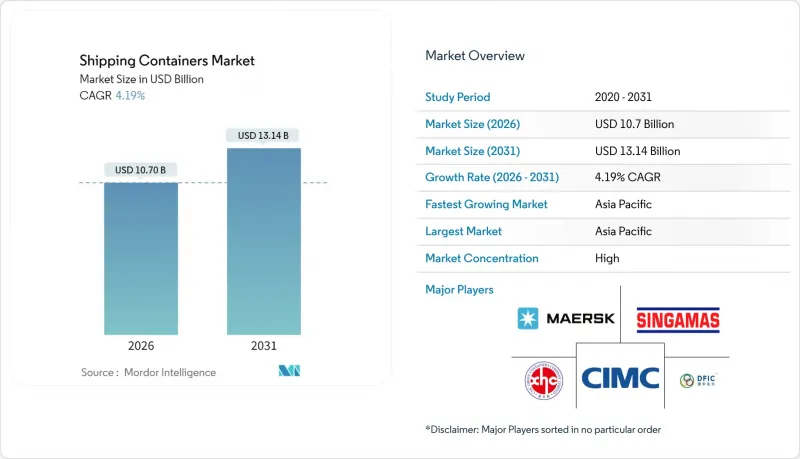

據估計,到 2026 年,海運貨櫃市場價值將達到 107 億美元,高於 2025 年的 102.7 億美元,預計到 2031 年將達到 131.4 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 4.19%。

電子商務履約、藥品低溫運輸的擴張以及多式聯運效率的提升,正在創造穩定的結構性需求。貨櫃運輸在全球貿易量中佔據90%的佔有率,為此成長提供了支撐。數位化追蹤工具和智慧設計使營運商能夠縮短港口停留時間,提高周轉率。永續性目標正推動材料創新,朝著更輕質複合材料的方向發展。航運公司之間聯盟的重新調整,正在重塑運力分配策略,更加重視規模更大、技術更先進的船隊。儘管地緣政治動盪只是短期因素,但也凸顯了多元化貿易路線的重要性以及動態路線規劃的必要性。

全球貨櫃市場趨勢與洞察

跨境電子商務的爆炸性成長要求24小時快速回應。

電子商務的蓬勃發展導致貨運頻率增加,但每次貨運量卻更小,因此港口吞吐速度比船舶運力更為重要。航運公司正在為高頻航線增添更多設備,港口也正在投資自動化起重機,以便在一個班次內完成船舶的裝卸作業。智慧追蹤技術使托運人能夠在貨物抵達港口前預先辦理清關手續並預訂鐵路貨運位。這些精簡措施縮短了庫存週期,並強化了對標準乾貨貨櫃的偏好,即使貿易量波動,標準乾貨貨櫃也能保持較高的運轉率。隨著線上市場滲透到新興經濟體,貨櫃市場在各種貿易路線上都保持著持續的潛在需求。

低溫運輸在全球的普及速度正在加快,對尖端冷藏貨櫃的訂單也不斷增加。

為了降低成本和排放,同時不影響溫度控制,製藥公司正將長途運輸從空運轉向海運。現代冷藏貨櫃的溫度精度可達±0.5°C,並整合遙測技術,能夠即時檢測偏差,從而在運輸途中採取糾正措施。生鮮食品出口商也採用類似技術,以最大限度地減少食品在送達遠距離消費者的過程中發生變質。提供雙燃料冷凍裝置的製造商透過降低能耗並符合低全球暖化潛值(GWP)法規,實現了更高的貨櫃售價。隨著食品電商拓展至新市場,對先進冷藏貨櫃的需求持續成長,超過了普通貨物運輸的成長速度。

疫情後貨櫃供應過剩導致運轉率下降

2021年至2023年創紀錄的新造船量造成了暫時的供應過剩,壓低了租賃價格,並導致營運商推遲新訂單。貿易疲軟導致門戶港口閒置庫存積壓,迫使堆場降低倉儲費並吸引調撥業務。製造商已採取措施應對,減少生產班次,並將產能轉向需求更為穩定的特殊設計。隨著老舊船隊的報廢和貿易恢復正常,預計這種調整將得到緩解。

細分市場分析

高立方貨櫃的需求日益成長,其比普通餘量高出13%的淨空高度,最大限度地提高了電商小包裹、輕型家電等貨物的容積有效負載容量。儘管40英尺標準貨櫃在2025年仍將佔據52.21%的市場佔有率,顯示其在海運領域持續受到歡迎,但預計到2031年,40英尺高立方貨櫃的年複合成長率將達到5.43%。高立方貨櫃的市場規模反映了托運人在不超出重量限制的情況下對更大運力的需求。

隨著港口基礎設施的改善,裝卸高度得以提升,碼頭營運商正在引入提升高度更高的正面吊運機,以有效處理這些貨櫃。物流整合商正在推廣40英尺軌距的貨櫃,以簡化鐵路貨車的分配並提高各堆場之間的互通性。 Triton Containers公司透過提供靈活的提貨選項的高箱租賃服務來鼓勵採用這種標準,從而降低搬遷成本。總體而言,托運人對容積效率和包裝整合的關注,正在推動主要貿易走廊對高箱需求的持續成長。

預計到2025年,乾貨貨櫃將佔貨運量的72.32%,鞏固其作為全球商品分銷支柱的地位。同時,受生鮮食品出口商和製藥公司海運業務擴張的推動,預計到2031年,冷藏貨櫃的複合年成長率將達到6.18%。目前,冷藏貨櫃佔據了貨櫃市場的高階領域,其租賃價格是乾貨貨櫃的兩到三倍。

技術創新包括變速壓縮機和太陽能輔助電源模組,從而降低了待機能耗。藥品托運商要求配備冗餘的溫度探頭和門感測器,並且能夠在異常情況發生後數秒內發出警報是區分不同製造商的關鍵因素。冷藏貨櫃也受益於脫碳,因為將對溫度敏感的貨物從空運轉移到海運可以減少高達 80% 的相關排放。

區域分析

預計亞太地區將引領貨櫃市場,2025年營收成長率將達到59.88%,並在2031年之前維持5.46%的複合年成長率。中國作為製造地的地位依然穩固,而隨著企業採購多元化,東南亞的需求也不斷成長。馬來西亞和印度的巨型港口計劃每年新增超過2500萬個標準箱的吞吐能力,不僅提升了區域貨物吞吐量,也刺激了支線網路的貨櫃需求。貨幣穩定和有利的貿易協定也透過區域租賃池推動了船隊的擴張。

北美正受益於近岸外包,即將電子產品和汽車組裝轉移到更靠近消費市場的地方。美國港口當局已核准數十億美元的疏浚和泊位電氣化計劃,加劇了與墨西哥和加拿大港口的競爭。中西部地區鐵路聯運網路的建設,使得連接大西洋和太平洋盆地的陸路運輸能夠在八天內實現,並促進了可堆疊貨櫃設計的應用。

歐洲貨櫃航運市場正經歷兩極化的成長趨勢。地緣政治緊張局勢迫使亞歐航線繞道非洲,導致儘管運輸時間延長,但地中海樞紐港口的停靠次數卻增加。倫敦門戶港和鹿特丹-馬斯弗拉克特港的自動化投資提高了起重機每小時的處理量,從而推高了單價。更嚴格的環保法規加速了老舊重型貨櫃的淘汰,並促使貨櫃轉向使用再生鋼材製造。儘管貿易量成長放緩,但這仍然支撐了貨櫃的更換需求。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 跨境電子商務的爆炸性成長使得標準乾貨貨櫃的交貨時間達到了24小時以內。

- 世界各地廣泛使用低溫運輸運輸生鮮食品和食材自煮包,加速了對先進冷藏箱的訂單。

- 直接面對消費者 (D2C) 的品牌正在尋求客製化帶有預印標誌的容器,用作行動快閃店和履約中心。

- 企業 ESG 政策促使托運人更傾向於使用可重複使用的多模態貨櫃,而不是一次性托盤包裝,從而推動了對替代品的需求。

- 採用物聯網技術的「智慧箱」可提供即時位置和狀態數據,進而提高托運人為優質設備付費的意願。

- 訂閱式和模組化住宅理念正在促進舊貨櫃的再利用,賦予它們第二次生命。

- 市場限制

- 疫情後紙箱供應過剩,降低了運轉率,抑制了對新建築的投資。

- 熱軋鋼卷鋼價格的波動為貨櫃買家的預算計劃帶來了不確定性。

- 從生產到處置,日益嚴格的監管和生產者延伸責任制 (EPR) 規則正在增加產品生命週期內的擁有成本。

- 可折疊和可壓縮容器替代品的迅速崛起正在蠶食傳統硬紙箱的需求。

- 價值/供應鏈分析

- 監管和技術趨勢

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 價格分析-標準貨櫃與特種貨櫃

- 專題報導:多式聯運和鐵路運輸的普及

- 全球貨櫃租賃市場概覽

- 地緣政治事件如何影響市場

第5章 市場規模與成長預測

- 按尺寸

- 20英尺(標準貨櫃)

- 40 英尺(FEU)

- 40英尺高立方貨櫃

- 其他(超過 45 英尺等)

- 按容器類型

- 乾式儲存(標準)

- 冷藏(冷藏車)

- 儲槽(ISO儲槽、低溫儲槽)

- 平板架和開放式頂部

- 特殊應用(側門、隧道、隔熱、折疊)

- 材料

- 耐候鋼

- 不銹鋼

- 鋁合金

- FRP和複合材料

- 其他

- 按最終用途行業分類

- 消費品和零售

- 食品/飲料

- 工業機械和汽車

- 化學品/石油產品

- 製藥和醫療保健

- 其他

- 透過交通工具

- 海洋/深海

- 近海/沿海路線

- 鐵路貨櫃運輸

- 陸路運輸和異地存儲

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美洲

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 亞太其他地區

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、產能擴充、租賃協議)

- 市佔率分析

- 公司簡介

- China International Marine Containers(CIMC)

- Dong Fang International Containers

- CXIC Group(CSSC)

- Maersk Container Industry A/S

- Singamas Container Holdings

- W&K Container

- Sea Box Inc.

- TLS Offshore Containers

- Storstac Inc.

- CARU Containers BV

- China Eastern Containers

- Valisons & Co.

- YMC Container Solutions

- American Intermodal Container Manufacturing

- Triton International

- Textainer Group Holdings

- Florens Container Services

- CAI International

- Touax Group

- UES International

第7章 市場機會與未來展望

Shipping Containers market size in 2026 is estimated at USD 10.7 billion, growing from 2025 value of USD 10.27 billion with 2031 projections showing USD 13.14 billion, growing at 4.19% CAGR over 2026-2031.

E-commerce fulfillment, pharmaceutical cold-chain expansion, and rising intermodal efficiency provide stable, structural demand. Containerization's role in handling 90% of global trade underpins this growth, while digital tracking tools and smarter designs help operators shorten port stays and boost asset turnover. Sustainability targets are pushing material innovation toward lighter composites, and alliance restructuring among carriers is reshaping capacity deployment strategies in favor of larger, technology-enabled fleets. Geopolitical disruptions add short-term volatility but also reinforce the importance of diversified trade lanes and dynamic routing.

Global Shipping Containers Market Trends and Insights

Explosive Growth of Cross-Border E-Commerce Creating 24-Hour Turnaround Expectations

E-commerce expansion drives more frequent, smaller shipments, shifting focus from vessel capacity toward port velocity. Carriers commit additional equipment to high-frequency loops, while ports invest in automated cranes that clear vessels inside one shift. Smart tracking allows shippers to pre-clear customs and book rail slots before docking. These operational gains shorten inventory cycles and reinforce preference for standard dry boxes, keeping utilization high even when trade volumes fluctuate. As online marketplaces penetrate emerging economies, the shipping container market sees sustained baseline demand across diverse trade lanes.

Worldwide Cold-Chain Penetration Accelerates Advanced Reefer Orders

Pharmaceutical producers are migrating long-haul shipments from air to ocean to cut costs and emissions without compromising temperature control. Modern reefers maintain +-0.5 °C accuracy and integrate telemetry that flags deviations in real time, allowing corrective actions mid-voyage. Fresh grocery exporters adopt similar technology to reach distant consumers with minimal spoilage. Manufacturers offering dual-fuel refrigeration units reduce energy consumption and meet low-GWP regulations, enabling higher price realisation per box. As grocery e-commerce extends to new markets, advanced reefer demand continues to outpace general cargo growth.

Post-Pandemic Oversupply of Boxes Eroding Utilization Rates

Record new builds made during 2021-2023 create a temporary surplus, pushing lease rates down and prompting operators to delay fresh orders. Idle inventories accumulate in gateway ports when trade softens, forcing depots to lower storage fees to attract repositioning business. Manufacturers adapt by trimming production shifts and redirecting capacity toward specialized designs with steadier demand. The correction is expected to resolve once scrappage catches up with ageing fleets and trade normalizes.

Other drivers and restraints analyzed in the detailed report include:

- Direct-to-Consumer Brands Demanding Bespoke, Logo-Printed Containers

- Corporate ESG Mandates Pushing Reusable Container Adoption

- Volatility in Hot-Rolled Coil Steel Prices Creating Budget Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-cube offerings are capturing incremental demand because their 13% extra headroom maximizes volumetric loads such as e-commerce parcels and lightweight consumer electronics. 40-ft formats generated 52.21% revenue in 2025, demonstrating entrenched popularity for ocean freight, whereas 40-ft high-cube units are forecast to grow at 5.43% CAGR to 2031. The shipping container market size for high-cube units reflects shipper preference for greater capacity without breaching weight restrictions.

Port infrastructure upgrades accommodate taller stacks, and terminal operators add reach-stackers with extended lifting heights to handle these units efficiently. Logistics integrators promote standardization on the 40-ft profile to streamline rail wagon allocation and depot interchange. Triton Containers markets high-cube leases with flexible pick-up options to reduce repositioning, reinforcing adoption. Overall, shipper focus on cubic efficiency and consolidation of packaging drives continued high-cube traction across primary trade corridors.

Dry storage boxes accounted for 72.32% of 2025 shipments, underscoring their status as the backbone of global commodity flows. In contrast, reefer units record a 6.18% CAGR to 2031 as fresh produce exporters and drug makers scale ocean routes. Refrigerated boxes currently represent the premium slice of the shipping container market, commanding rental rates two to three times higher than dry units.

Technology upgrades include variable-speed compressors and solar-assisted power modules that cut energy draw during idle periods. Pharmaceutical shippers require redundant temperature probes and door sensors that trigger alerts within seconds of deviation, driving differentiation among manufacturers. Reefers also benefit from decarbonization, as shifting temperature-sensitive goods from air to sea avoids up to 80% of related emissions.

The Shipping Container Market is Segmented by Size (20-Ft (TEU), 40-Ft (FEU) and More), by Container Type (Dry Storage (Standard), Refrigerated, and More), by Material (Corten Steel, Stainless Steel and More), End-Use Industry (Consumer Goods & Retail and More), by Mode of Transport (Maritime Deep-Sea and More), by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the shipping containers market with 59.88% revenue in 2025 and is set to grow at a 5.46% CAGR to 2031. China retains manufacturing leadership, yet Southeast Asia captures incremental volumes as firms diversify sourcing. Malaysian and Indian mega-port projects add more than 25 million TEU of annual capacity, anchoring regional throughput and stimulating container demand across feeder networks. Currency stability and supportive trade agreements also encourage regional leasing pools to expand their fleets.

North America benefits from nearshoring that shifts electronics and automotive assembly closer to consumption markets. United States port authorities approve multi-billion-dollar dredging and berth electrification programs, enhancing competitiveness against Mexican and Canadian gateways. The rail intermodal build-out across the Midwest unlocks cost-effective land bridges that connect Atlantic and Pacific basins in under eight days, driving uptake of stack-train compatible container designs.

Europe records mixed growth shipping container market as geopolitical tensions divert Asia-Europe sailings around Africa, extending transit times but also directing additional calls to Mediterranean hubs. Investments in automation at London Gateway and Rotterdam Maasvlakte raise throughput per crane hour, cushioning cost-per-box metrics. Stringent environmental regulations accelerate the retirement of older, heavier boxes in favor of recycled-content steel units, supporting replacement demand despite subdued trade volume growth.

- China International Marine Containers (CIMC)

- Dong Fang International Containers

- CXIC Group (CSSC)

- Maersk Container Industry A/S

- Singamas Container Holdings

- W&K Container

- Sea Box Inc.

- TLS Offshore Containers

- Storstac Inc.

- CARU Containers B.V.

- China Eastern Containers

- Valisons & Co.

- YMC Container Solutions

- American Intermodal Container Manufacturing

- Triton International

- Textainer Group Holdings

- Florens Container Services

- CAI International

- Touax Group

- UES International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of cross-border e-commerce creating 24-hour turnaround expectations for standard dry containers.

- 4.2.2 Worldwide cold-chain penetration of fresh grocery and meal-kit delivery accelerating orders for advanced reefer boxes.

- 4.2.3 Direct-to-consumer (D2C) brands demanding bespoke, logo-printed containers to double as mobile pop-up stores and fulfilment hubs.

- 4.2.4 Corporate ESG mandates pushing shippers toward reusable, multimodal containers over single-use pallet wrap, lifting replacement demand.

- 4.2.5 Adoption of IoT-enabled -smart- boxes providing real-time location & condition data, raising shipper's willingness to pay for premium units.

- 4.2.6 Subscription-based and modular housing concepts spurring second-life conversions of retired shipping containers.

- 4.3 Market Restraints

- 4.3.1 Post-pandemic oversupply of boxes eroding utilisation rates and discouraging new-build investment.

- 4.3.2 Volatility in hot-rolled coil steel prices creating budget uncertainty for container purchasers.

- 4.3.3 Stricter cradle-to-grave regulations and extended-producer-responsibility (EPR) rules inflating lifetime ownership costs.

- 4.3.4 Rapid emergence of foldable and collapsible container alternatives cannibalising demand for conventional rigid boxes.

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Pricing Analysis - Standard vs. Special Containers

- 4.8 Spotlight: Intermodal & Rail Uptake

- 4.9 Global Container Leasing Landscape

- 4.10 Impact of Geopolitical Events on the Market

5 Market Size & Growth Forecasts (Value, Volume)

- 5.1 By Size

- 5.1.1 20-ft (TEU)

- 5.1.2 40-ft (FEU)

- 5.1.3 40-ft High-Cube,

- 5.1.4 Others ( >45-ft, etc)

- 5.2 By Container Type

- 5.2.1 Dry Storage (Standard)

- 5.2.2 Refrigerated (Reefer)

- 5.2.3 Tank (ISO Tank, Cryogenic)

- 5.2.4 Flat-Rack & Open-Top

- 5.2.5 Special Purpose (Side-Door, Tunnel, Insulated, Collapsible)

- 5.3 By Material

- 5.3.1 Corten Steel

- 5.3.2 Stainless Steel

- 5.3.3 Aluminium Alloy

- 5.3.4 FRP & Composite

- 5.3.5 Others

- 5.4 By End-Use Industry

- 5.4.1 Consumer Goods & Retail

- 5.4.2 Food & Beverage

- 5.4.3 Industrial Machinery & Automotive

- 5.4.4 Chemicals & Petroleum

- 5.4.5 Pharmaceuticals & Healthcare

- 5.4.6 Others

- 5.5 By Mode of Transport

- 5.5.1 Maritime Deep-Sea

- 5.5.2 Short-Sea & Coastal

- 5.5.3 Rail Intermodal

- 5.5.4 Road Inland Haulage & Off-Site Storage

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Europe

- 5.6.4.1 United Kingdom

- 5.6.4.2 Germany

- 5.6.4.3 France

- 5.6.4.4 Spain

- 5.6.4.5 Italy

- 5.6.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.4.8 Rest of Europe

- 5.6.5 Middle East And Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Capacity Expansion, Leasing Deals)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 China International Marine Containers (CIMC)

- 6.4.2 Dong Fang International Containers

- 6.4.3 CXIC Group (CSSC)

- 6.4.4 Maersk Container Industry A/S

- 6.4.5 Singamas Container Holdings

- 6.4.6 W&K Container

- 6.4.7 Sea Box Inc.

- 6.4.8 TLS Offshore Containers

- 6.4.9 Storstac Inc.

- 6.4.10 CARU Containers B.V.

- 6.4.11 China Eastern Containers

- 6.4.12 Valisons & Co.

- 6.4.13 YMC Container Solutions

- 6.4.14 American Intermodal Container Manufacturing

- 6.4.15 Triton International

- 6.4.16 Textainer Group Holdings

- 6.4.17 Florens Container Services

- 6.4.18 CAI International

- 6.4.19 Touax Group

- 6.4.20 UES International

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

貨櫃改造市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、改造類型、應用、產業、地區和競爭格局分類,2021-2031年

貨櫃改造市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、改造類型、應用、產業、地區和競爭格局分類,2021-2031年 海運貨櫃市場:2026-2032年全球市場預測(按貨櫃類型、材質、尺寸、所有權、應用和最終用戶產業分類)

海運貨櫃市場:2026-2032年全球市場預測(按貨櫃類型、材質、尺寸、所有權、應用和最終用戶產業分類) 貨櫃船市場:按部件、燃料類型和地區分類貨物固定設備市場:2026-2032年全球市場預測(依產品、材料、應用及通路分類)

貨櫃船市場:按部件、燃料類型和地區分類貨物固定設備市場:2026-2032年全球市場預測(依產品、材料、應用及通路分類) 貨櫃船市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球智慧貨櫃市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球貨櫃市場規模、佔有率、趨勢和成長分析報告(2026-2034)

貨櫃船市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球智慧貨櫃市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球貨櫃市場規模、佔有率、趨勢和成長分析報告(2026-2034) 貨櫃市場報告:按產品、貨櫃尺寸、應用和地區分類(2026-2034 年)

貨櫃市場報告:按產品、貨櫃尺寸、應用和地區分類(2026-2034 年) 2026年全球貨櫃市場報告2026年全球鍋爐、儲槽和運輸貨櫃市場報告

2026年全球貨櫃市場報告2026年全球鍋爐、儲槽和運輸貨櫃市場報告