|

市場調查報告書

商品編碼

1911727

馬來西亞行動通訊業者(MNO)市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Malaysia Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

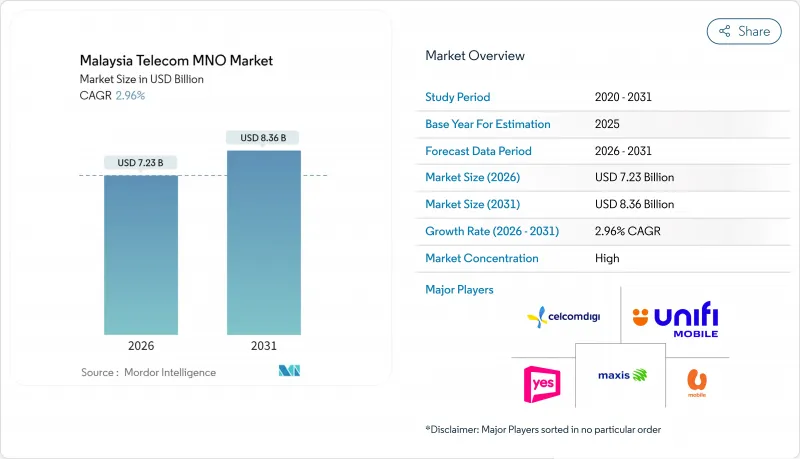

預計到 2025 年,馬來西亞行動通訊業者(MNO) 市值將達到 70.2 億美元,到 2026 年將成長至 72.3 億美元,到 2031 年將成長至 83.6 億美元,在預測期(2026-2031 年)內將成長至 2.96%。

這一穩定成長主要受三大關鍵趨勢驅動:向雙網路5G架構轉型、大規模光纖部署以及企業數位化進程的推進。通訊業者正果斷地摒棄傳統的以語音為中心的經營模式,轉而優先發展數據優先戰略,將全國範圍的5G覆蓋範圍與雲端運算、內容和邊緣運算領域的夥伴關係相結合。諸如JENDELA和國家光纖化與連接計劃等政府項目,透過保障基地台升級和回程傳輸光纖的成本,顯著降低了所需資本支出的風險,使營運商能夠將資金重新分配到更高價值的企業提案中。同時,無限資料方案套餐的價格戰持續擠壓消費者的利潤空間,迫使通訊業者尋求高商機,例如私有5G、物聯網和固網行動融合(FMC)。在此背景下,馬來西亞的行動網路營運商(MNO)市場正從規模競爭演變為以網路切片、人工智慧驅動的自動化和產業專用的解決方案等差異化能力決定競爭優勢的格局。

馬來西亞電信行動網路營運商市場趨勢與洞察

利用 JENDELA 和雙網機型擴展 5G 覆蓋範圍

從單一發網路向競爭性雙網路結構的轉型將重塑各通訊業者的基礎設施經濟格局。 Digital National計畫在2024年12月前達到80.2%的人口覆蓋率,而U Mobile建置第二張全國性網路的義務將引入冗餘機制,從而降低批發資費並提升服務品質。 U Mobile與中國移動國際合作,承諾在18個月內部署5000至7000個5G基地台。這項積極的部署計畫將加快部署速度,同時緩解壟斷瓶頸帶來的擔憂。雙網路部署也將釋放頻譜資源用於私有5G切片,從而支援對延遲敏感的應用,例如工業領域的機器視覺檢測和自動化物料搬運。單一來源限制的消除將為馬來西亞電信行動網路營運商(MNO)市場參與企業提供更多空間,使其能夠在差異化5G收費系統和服務等級協定(SLA)方面進行創新,而不僅僅依賴價格競爭。

人均行動數據消費量增加和ARPU值上升

在4K影片串流、雲端遊戲和人工智慧增強型行動應用程式的推動下,預計每月數據使用量將從2024年的21.6GB飆升至2029年的51.9GB。為了抓住這一成長機遇,通訊業者正逐步淘汰限速的「無限流量」套餐,轉而推出分級5G套餐,以實現不限速帶來的收益。 OTT合作,例如Astro與Netflix和Disney+Hotstar的捆綁銷售,建立了一個強大的內容生態系統,有助於提高客戶留存率並降低客戶解約率。然而,通訊業者正努力尋求微妙的平衡。目前所有網路均提供的價格低於馬幣的無限資料方案,如果速度差異化不足,則可能危及ARPU(每位用戶平均收入)的成長潛力。成功的關鍵在於引導用戶升級到高速套餐,同時將邊緣託管遊戲和超高清體育賽事串流等專屬服務功能保留給價格更高的套餐用戶。

無限資料方案價格競爭加劇,對利潤率帶來壓力。

價格低於馬幣的無限流量套餐設定了最低價格門檻,在5G資本支出達到高峰之際,這給營運商的盈利帶來了壓力。 U Mobile僅限週末使用的5G預付套餐(馬幣)和CelcomDigi同價位的3Mbps套餐迫使競爭對手推出類似促銷活動。由此造成的利潤率壓力顯著。當無限流量包含在基礎費用中時,速度加價就不存在了。雖然在約200GB流量使用後會實施公平使用限制,這有助於緩解網路堵塞,但客戶越來越傾向於將速度降低視為違約行為,導致用戶流失率上升,並在社群媒體上引發強烈抗議。為了恢復收入來源,通訊業者目前正將重心轉向企業訂閱、內容包和金融科技相關服務,這些領域的需求彈性較低,且用戶支付意願較高。

細分市場分析

到2025年,數據和網路服務將佔馬來西亞行動網路營運商(MNO)市場佔有率的53.62%,並在2031年之前以2.99%的複合年成長率成長。超高清串流媒體、下一代人工智慧智慧型手機和雲端遊戲帶來的流量成長正推動營運商升級回程傳輸並部署營運商級邊緣節點。語音服務將繼續佔馬來西亞MNO市場佔有率的19.18%,這主要得益於漫遊需求的復甦和麵向企業的整合通訊捆綁銷售,但其複合年成長率將落後於數據主導型業務,僅為2.70%。通訊、附加價值服務和批發傳輸服務總合將佔總收入的16.04%,複合年成長率為2.98%,這主要得益於超大規模資料中心營運商不斷成長的頻寬需求。

物聯網和機器對機器(M2M)業務僅佔總收入的5.05%,但其複合年成長率(CAGR)高達3.11%,主要得益於工業4.0藍圖和JENDELA走廊內的智慧城市試點計畫。隨著製造業企業轉向依賴密集感測器網路的預測維修系統,預計物聯網模組在馬來西亞行動網路營運商(MNO)通訊業者的規模將進一步擴大。 OTT和付費電視服務佔總營收的6.11%,成長率為3.05%。 Astro與Netflix和Disney+Hotstar的直接收費合作,正是通訊業者透過內容聚合提高每用戶平均收入(ARPU)的例證。

馬來西亞電信行動網路營運商(MNO)市場按服務類型(語音服務、數據/網際網路服務、通訊服務、物聯網/機器對機器通訊服務、OTT/付費電視服務等)和最終用戶(企業、消費者)進行細分。市場預測以價值(美元)和用戶數量(用戶數)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 監理與政策框架

- 頻譜環境與競爭格局

- 通訊業生態系統

- 宏觀經濟與外在因素

- 波特五力分析

- 競爭對手之間的競爭

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 領先行動網路營運商的關鍵績效指標(2020-2025)

- 獨立行動用戶和滲透率

- 行動網路使用者數量和普及率

- 按接入技術分類的SIM卡連線數和滲透率

- 蜂巢式物聯網/M2M連接

- 寬頻連線(移動/固定)

- ARPU(每位用戶平均收入)

- 用戶平均每月數據使用量(GB/月)

- 市場促進因素

- 利用 JENDELA 和雙網機型擴展 5G 覆蓋範圍

- 人均行動數據消費量和ARPU值均有所成長

- 政府主導的光纖部署計畫(NFCP,JENDELA)

- 製造業叢集對專用5G和物聯網解決方案的需求

- 通訊業者和OTT內容商品搭售付費電視和數據提升銷售

- 透過遊客和移民的eSIM套餐增加預付收入

- 市場限制

- 無限資料方案的價格競爭日益激烈,對利潤率帶來壓力。

- 高昂的頻譜使用費和普遍服務義務(USO)稅費正給現金流帶來壓力。

- 巴生谷地區以外的光纖回程傳輸瓶頸

- 關於賣出DNB股份的政策不確定性

- 技術展望

- 電信業主要經營模式分析

- 定價模型和定價分析

第5章 市場規模與成長預測

- 通訊總收入和每位用戶平均收入

- 服務類型

- 語音服務

- 數據和網際網路服務

- 通訊服務

- 物聯網和機器對機器服務

- OTT和付費電視服務

- 其他服務(附加價值服務、漫遊/國際服務、企業/批發服務等)

- 最終用戶

- 公司

- 一般消費者

第6章 競爭情勢

- 市場集中度

- 主要供應商的策略性舉措與投資,2023-2025 年

- 2024年行動網路營運商市場佔有率分析

- Product Benchmarking Analysis for mobile network services

- MNO snapshot(subscribers, churn rate, ARPU, etc.)

- 行動網路營運商公司簡介*

- CelcomDigi

- Maxis

- U Mobile

- Yes(YTL Communications)

- Unifi Mobile(Telekom Malaysia)

第7章 市場機會與未來展望

The Malaysia Telecom MNO Market was valued at USD 7.02 billion in 2025 and estimated to grow from USD 7.23 billion in 2026 to reach USD 8.36 billion by 2031, at a CAGR of 2.96% during the forecast period (2026-2031).

The transition to a dual-network 5G regime, large-scale fiber build-outs, and rising enterprise digitization are the three forces most responsible for this steady uplift. Operators have moved decisively away from legacy voice-centric business models, prioritizing data-first strategies that blend nationwide 5G coverage with partnerships in cloud, content, and edge computing. Government programs such as JENDELA and the National Fiberisation and Connectivity Plan have de-risked much of the required capital outlay by underwriting tower upgrades and backhaul fiber, enabling operators to redeploy cash toward value-added enterprise propositions. At the same time, price-led competition in unlimited data plans continues to compress consumer margins, compelling carriers to chase higher-yield opportunities in private 5G, IoT, and fixed-mobile convergence. Against this backdrop, the Malaysia telecom MNO market is evolving from a scale game to one where differentiated capabilities in network slicing, AI-driven automation, and vertical-specific solutions define competitive advantage.

Malaysia Telecom MNO Market Trends and Insights

5G Coverage Expansion Under JENDELA & Dual-Network Model

The leap from a single wholesale network to a competitive dual-network structure rewrites infrastructure economics for every carrier. Digital Nasional Berhad achieved 80.2% population coverage by December 2024, and U Mobile's mandate to erect a second nationwide grid introduces redundancy that should narrow wholesale fees and improve quality of service. U Mobile pledges 5,000-7,000 5G sites within 18 months in partnership with China Mobile International, an aggressive schedule that accelerates adoption while mitigating the prior fear of a bottlenecked monopoly. The dual-track rollout also unlocks spectrum for private 5G slices, positioning industrial zones for latency-sensitive applications such as machine-vision inspection and autonomous material handling. By removing single-supplier constraints, Malaysia telecom MNO market participants gain room to innovate on differentiated 5G tariffs and service-level agreements rather than competing solely on price.

Rising Per-Capita Mobile Data Consumption & ARPU Uplift

Monthly data usage is projected to jump from 21.6 GB in 2024 to 51.9 GB by 2029, propelled by 4K video streaming, cloud gaming, and AI-enhanced mobile apps. To capture this surge, carriers are phasing out throttled "unlimited" offers in favor of tiered 5G packages that monetize uncapped speeds. OTT alliances, typified by Astro's bundle with Netflix and Disney+Hotstar, deliver sticky content ecosystems that lengthen tenure and combat churn. Operators nevertheless navigate a delicate balance; unlimited data plans below RM 50, now common across all networks, threaten to dilute potential ARPU gains if speed-based differentiation is poorly executed. Success hinges on migrating subscribers to premium speed tiers while reserving exclusive service features-such as edge-hosted gaming or UHD sports streams-for higher-priced plans.

Aggressive Unlimited-Data Price Wars Compressing Margins

Unlimited plans under RM 50 have set a low watermark that squeezes profitability just as 5G capex peaks. U Mobile's prepaid offer with 5G-enabled weekends at RM 25 and CelcomDigi's 3 Mbps plan at the same price have forced every carrier to replicate similar promotions. The resulting margin squeeze is stark: speed-based premiums vanish when baseline tariffs include uncapped data. Fair-usage throttling helps to limit network congestion after roughly 200 GB of use, yet customers increasingly view speed reductions as broken promises, risking churn and social-media backlash. To restore economics, operators now pivot toward enterprise contracts, content bundling and fintech adjacencies where elasticity is lower and willingness to pay is higher.

Other drivers and restraints analyzed in the detailed report include:

- Government-Backed Fiber Rollout Programs (NFCP, JENDELA)

- Manufacturing Clusters' Demand for Private 5G & IoT Solutions

- High Spectrum Fees & USO Levies Straining Cash Flow

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data and internet services captured 53.62% of Malaysia telecom MNO market share in 2025, running ahead at a 2.99% CAGR through 2031. Growing traffic from UHD streaming, Gen-AI smartphones, and cloud gaming drives operators to upscale backhaul and deploy carrier-grade edge nodes. Voice remains a 19.18% slice of Malaysia telecom MNO market size, cushioned by roaming recovery and unified-communications bundles sold into enterprise accounts, yet its 2.70% CAGR lags data-led verticals. Messaging, value-added services, and wholesale transit combine for 16.04% of revenue and post a 2.98% growth clip, buoyed by rising demand for bandwidth from hyperscale datacenter operators.

IoT & M2M stands at only 5.05% of total receipts but records the highest 3.11% CAGR, propelled by Industry 4.0 roadmaps and smart-city pilots within JENDELA corridors. The Malaysia telecom MNO market size for IoT modules is forecast to expand as manufacturing supervisors switch to predictive maintenance systems that rely on high-density sensor grids. OTT and Pay-TV services contribute 6.11% of revenue on a 3.05% trajectory; Astro's direct billing partnerships with Netflix and Disney+Hotstar illustrate how carriers secure incremental ARPU via content aggregation.

The Malaysia Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and More), and End User (Enterprises, and Consumers). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- CelcomDigi

- Maxis

- U Mobile

- Yes (YTL Communications)

- Unifi Mobile (Telekom Malaysia)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Regulatory and Policy Framework

- 4.3 Spectrum Landscape & Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic & External Drivers

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers & Penetration Rate

- 4.7.2 Mobile Internet Users & Penetration Rate

- 4.7.3 SIM Connections by Access Technology & Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile & Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 5G coverage expansion under JENDELA & dual-network model

- 4.8.2 Rising per-capita mobile data consumption & ARPU uplift

- 4.8.3 Government-backed fibre rollout programmes (NFCP, JENDELA)

- 4.8.4 Manufacturing clusters' demand for private 5G & IoT solutions

- 4.8.5 Telco-OTT content bundling boosting Pay-TV & data upsell

- 4.8.6 e-SIM tourist & migrant plans adding incremental prepaid revenue

- 4.9 Market Restraints

- 4.9.1 Aggressive unlimited-data price wars compressing margins

- 4.9.2 High spectrum fees & USO levies straining cash flow

- 4.9.3 Fibre backhaul bottlenecks outside Klang Valley

- 4.9.4 Policy uncertainty over DNB stake divestment

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom Sector

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming & International Services, Enterprise & Wholesale Services, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 Product Benchmarking Analysis for mobile network services

- 6.5 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.6 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.6.1 CelcomDigi

- 6.6.2 Maxis

- 6.6.3 U Mobile

- 6.6.4 Yes (YTL Communications)

- 6.6.5 Unifi Mobile (Telekom Malaysia)

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space & Unmet-Need Assessment

行動虛擬網路營運商 (MVNO) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類

行動虛擬網路營運商 (MVNO) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類 亞太地區行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)美國行動虛擬網路營運商:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)美國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年)西班牙電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)越南電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)美國行動虛擬網路營運商:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)美國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年)西班牙電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)越南電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 虛擬行動服務業者(MVNO)市場-2026-2031年預測

虛擬行動服務業者(MVNO)市場-2026-2031年預測