|

市場調查報告書

商品編碼

1911722

德國行動通訊業者(MNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Germany Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

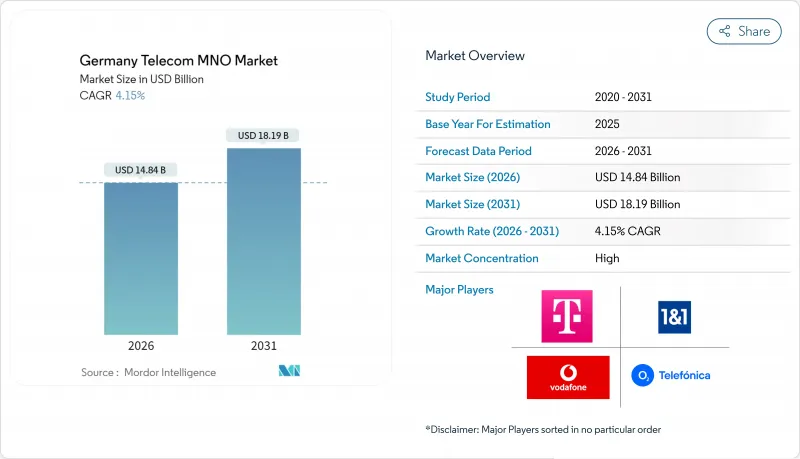

2025年德國行動通訊業者(MNO)市場價值為142.5億美元,預計到2031年將達到181.9億美元,高於2026年的148.4億美元。

預計在預測期(2026-2031 年)內,複合年成長率將達到 4.15%。

到2030年,網路現代化投資將接近500億歐元,聯邦Gigabit戰略以及5G獨立組網的快速部署,即便經濟成長放緩,仍保持強勁勢頭。營運商正優先推進光纖到戶(FTTH)覆蓋範圍的擴展、固移融合套餐以及人工智慧驅動的網路自動化,以提高每用戶平均收入(ARPU)並降低營運成本。企業數位化,尤其是在製造業和汽車產業叢集中,正在推動對高階連接的需求。同時,受串流媒體需求的驅動,消費者數據流量持續成長。包括嚴格的能源效率法規和覆蓋範圍強制性要求在內的監管壓力,正在重新調整資本配置的優先順序,並促使中小型業者選擇合作或退出市場。

德國行動通訊業者(MNO)市場趨勢與分析

光纖到府(FTTH)的快速擴張和政府的Gigabit目標

德國的Gigabit策略旨在2025年實現50%的家庭光纖接入,並在2030年實現近乎全國範圍的覆蓋,為此制定了一項雄心勃勃的資本計劃。聯邦政府的Gigabit支持計畫「Gigabitforderung 2.0」提供的30億歐元補貼正在加速服務欠缺地區的建設。同時,德國電信的目標是到2030年新增1,000萬多條光纖線路,沃達豐則計畫利用UnityMedia的資產為2,500萬戶家庭提供服務。擁有更廣泛光纖網路的營運商可以透過多業務組合和高階商務線路實現更高的每用戶平均收入(ARPU)。雖然早期部署會造成暫時的市場碎片化,並使光纖覆蓋率高的地區受益,但全國範圍的部署對於長期競爭力仍然至關重要。此策略的成功將透過提升數據密集型服務的容量,直接推動德國電信市場的收入成長。

快速部署5G SA將推動eMBB需求

德國三大通訊業者已實現2024年99%的網路覆蓋目標,德國電信計畫在2025年實現99%的人口覆蓋。獨立組網架構(SA)支援低延遲網路切片,這對寶馬、梅賽德斯-奔馳和大眾的製造工廠和汽車園區至關重要。預計消費者收入也將成長。通訊業者的行動數據使用量年增30-34%,並透過高容量和無限流量套餐推動營收成長。通訊業者透過逐步淘汰傳統核心網路和整合頻寬來提高效率,同時降低每GB成本並改善用戶體驗。在此背景下,5G SA的早期採用者可望獲得永續的競爭優勢,並推動德國電信市場的成長。

MDU有線電視法案削減固定收入

2024年7月「公用事業豁免」(Nebenkostenprivileg)的取消,使得有線電視費用不再自動計入租金。這使得沃達豐的多用戶住宅用戶群面臨直接競爭,導致其用戶數量從850萬驟降至400萬。整個產業約有8億歐元的年收入面臨風險,而Telecolumbus在短短幾個月內就流失了40%的電視用戶。 Netflix、Amazon Prime、 擦拭巾和Zatu等串流平台無需承擔網路成本,便與營運商爭奪同一批用戶,加劇了價格競爭。為了保住市場佔有率,營運商必須重新評估電視服務在融合套餐中的定位,但短期內用戶解約率的激增和EBITDA的壓縮仍然令人擔憂。

細分市場分析

預計到2025年,數據和網路服務市場規模將達到61.5億美元(佔德國電信市場佔有率的43.12%),並在2031年之前以4.33%的複合年成長率成長,這主要得益於對影片串流媒體和企業雲端連接的強勁需求。營運商的行動數據流量成長顯著:沃達豐成長34%至18億GB,德國電信成長30%至24億GB,O2的行動數據流量超過30億GB。同時,固定線路的流量消費量超過1,210億GB,平均每個家庭每月使用量為275GB。 5G獨立組網和光纖升級支援差異化的服務層級,為尋求網路切片保障的工業用戶提供了高價位選擇。因此,預計德國電信市場規模將繼續在細分市場層面超越傳統類別。

語音服務在2025年仍將創造39.1億美元的收入(佔27.45%),但由於向OTT(網路電視)的轉型以及計劃在2028年前逐步淘汰2G服務,預計這一數字將逐漸下降。德國電信(Telefónica Deutschland)已將其80%的通話路由至VoLTE,德國電信(Deutsche Telekom)和沃達豐(Vodafone)也在將頻寬重新分配給5G。物聯網(IoT)和機器對機器(M2M)服務在2025年將達到13.6億美元,複合年成長率(CAGR)高達4.45%,是成長最快的領域,這反映了德國在連網工廠和車用通訊系統領域的主導地位。付費電視和其他附加價值服務面臨來自串流媒體服務的直接競爭,但隨著國際旅行的復甦,漫遊和批發流量正在回升。隨著以數據為中心的產品超越語音服務,整體產品組合正向高成長、利潤率更高的類別轉變。

德國通訊業者市場按服務類型(語音服務、數據和網際網路服務、通訊服務、物聯網和機器對機器通訊服務、OTT和付費電視服務等)和最終用戶(企業、消費者)進行細分。市場預測以價值(美元)和數量(用戶數)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 監理與政策框架分析

- 當前頻寬擁有情形及競爭所有權

- 通訊業生態系統

- 宏觀經濟與外在因素

- 波特五力分析

- 競爭對手之間的競爭

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 領先行動網路營運商的關鍵績效指標(2020-2025)

- 獨立行動用戶和滲透率

- 行動網路使用者數量和普及率

- 按接入技術分類的SIM卡連線數和滲透率

- 蜂巢式物聯網/M2M連接

- 寬頻連線(移動和固定)

- ARPU(每位用戶平均收入)

- 每用戶平均數據使用量(GB/月)

- 市場促進因素

- 光纖到戶部署的快速擴張和政府的Gigabit目標

- 快速部署 5G SA 推動 eMBB 需求

- 企業數位化與校園網路實施

- 固移融合套餐提升每位用戶平均收入

- 透過基於人工智慧的網路自動化降低營運成本(不太常見)

- 頻譜共用增加和中立主機模式(不太突出)

- 市場限制

- 根據《多戶住宅有線電視法》減少固定收入

- 由於嚴格的節能法規,資本投資增加。

- 光纖和5G設備領域新加入經營者的投資負擔加重(這個問題很少受到關注)

- 由於向OTT語音轉型而導致的傳統收入下滑(一個鮮為人知的問題)

- 技術展望

- 電信業主要經營模式分析

- 定價模型和定價分析

第5章 市場規模與成長預測

- 通訊總收入和每位用戶平均收入

- 服務類型

- 語音服務

- 數據和網際網路服務

- 通訊服務

- 物聯網和機器對機器服務

- OTT和付費電視服務

- 其他服務類型(附加價值服務、漫遊和國際服務、企業/批發服務等)

- 最終用戶

- 公司

- 一般消費者

第6章 競爭情勢

- 市場集中度

- 主要供應商的策略與投資動向(2023-2025)

- 2024年行動網路營運商市場佔有率分析

- 行動網路營運商概況(用戶數、流失率、ARPU 等)

- MNO公司簡介

- Deutsche Telekom

- Vodafone Germany

- O2 Telefonica Deutschland

- 1&1 AG

第7章 市場機會與未來展望

The Germany Telecom MNO Market was valued at USD 14.25 billion in 2025 and estimated to grow from USD 14.84 billion in 2026 to reach USD 18.19 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031).

Network-modernization investments approaching EUR 50 billion through 2030, the federal Gigabit Strategy, and swift 5G standalone roll-outs are sustaining momentum even as economic growth moderates. Operators are prioritizing fiber-to-the-home coverage, fixed-mobile convergence bundles, and AI-enabled network automation to strengthen average revenue per user (ARPU) and cut operating costs. Enterprise digitalization, particularly in manufacturing and automotive clusters, is accelerating premium connectivity demand, while consumer data traffic keeps climbing on the back of streaming. Regulatory pressure, including stringent energy-efficiency rules and spectrum-coverage obligations, is reshaping capital-allocation priorities and nudging smaller players toward partnership or exit.

Germany Telecom MNO Market Trends and Insights

Surging FTTH Build-out and Government Gigabit Targets

Germany's Gigabit Strategy requires 50% of premises to be fiber-connected by 2025 and near-universal coverage by 2030, spurring aggressive capital programs. EUR 3 billion in federal Gigabitforderung 2.0 subsidies accelerates builds in underserved districts, while Deutsche Telekom aims for 10 million additional fiber lines by 2030 and Vodafone leverages Unitymedia assets to pass 25 million homes. Operators with deeper fiber footprints command higher ARPU through multi-play bundles and premium enterprise links. Early deployments create temporary market fragmentation favoring fiber-rich localities, yet nationwide roll-out remains a prerequisite for long-term competitiveness. Successful execution directly lifts German telecom market revenue trajectories by expanding capacity for data-heavy services.

Rapid 5G SA Roll-outs Powering eMBB Demand

All three national carriers met initial 99% coverage targets by 2024, and Deutsche Telekom plans 99% population reach in 2025. Standalone architecture unlocks low-latency network slicing crucial for manufacturing and automotive campuses at BMW, Mercedes-Benz, and Volkswagen sites. Consumers are also driving revenue uplift as mobile data usage rose 30-34% year-over-year across operators, monetized via larger allowances and unlimited plans. Operators gain efficiency from retiring legacy cores and converging frequency layers, which lowers per-gigabyte costs while improving user experience. Early 5G SA adopters therefore secure durable competitive advantages and stimulate incremental German telecom market growth.

MDU Cable-TV Law Slashing Fixed Revenue

The July 2024 repeal of the Nebenkostenprivileg removed automatic inclusion of cable TV in rental bills, exposing Vodafone's MDU subscriber base to direct competition and slashing the cohort from 8.5 million to 4 million accounts. An estimated EUR 800 million in annual revenue is at risk sector-wide, with Tele Columbus losing 40% of TV customers in mere months. Streaming platforms such as Netflix, Amazon Prime, Waipu, and Zattoo now vie for the same households without bearing network costs, intensifying price pressure. Operators must reposition TV within convergent bundles to defend share, yet short-term churn spikes and EBITDA compression remain likely.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Digitalization and Campus-Network Uptake

- Fixed-Mobile Convergence Bundles Boosting ARPU

- Stringent Energy-Efficiency Rules Raising Capex

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data and Internet Services delivered USD 6.15 billion in 2025, 43.12% of the German telecom market share, and are CAGR-forecast at 4.33% through 2031 on buoyant video streaming and enterprise cloud connectivity. Operators documented mobile data surges-Vodafone 34% to 1.8 billion GB, Deutsche Telekom 30% to 2.4 billion GB, and O2 beyond 3 billion GB-while fixed consumption surpassed 121 billion GB with average household loads of 275 GB monthly. 5G standalone and fiber upgrades underpin differentiated service tiers that fetch premium pricing from industrial users seeking network-slice guarantees. Consequently, German telecom market size gains at the segment level will continue to eclipse legacy categories.

Voice Services still produced USD 3.91 billion (27.45% share) in 2025, but OTT migration and planned 2G shutdowns by 2028 portend gradual contraction. Telefonica Deutschland already routes 80% of calls via VoLTE, and both Deutsche Telekom and Vodafone are reallocating spectrum to 5G. IoT and M2M Services, worth USD 1.36 billion in 2025, exhibit the fastest 4.45% CAGR, reflecting Germany's leadership in connected-factory and automotive telematics. Pay-TV and other value-added services face direct streaming competition, yet roaming and wholesale traffic are recovering alongside international travel. As data-centric products outpace voice, overall portfolio mix shifts toward higher-growth, margin-accretive categories.

The Germany Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and More), and End User (Enterprises, and Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Deutsche Telekom

- Vodafone Germany

- O2 Telefonica Deutschland

- 1&1 AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 Market Landscape

- 4.1 Market Overview

- 4.2 Regulatory And Policy Framework

- 4.3 Spectrum Landscape And Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic And External Drivers

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers And Penetration Rate

- 4.7.2 Mobile Internet Users And Penetration Rate

- 4.7.3 SIM Connections by Access Technology And Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile And Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 Surging FTTH Build-out and Government Gigabit Targets

- 4.8.2 Rapid 5G SA Roll-outs Powering eMBB Demand

- 4.8.3 Enterprise Digitalization And Campus-Network Uptake

- 4.8.4 Fixed-Mobile Convergence Bundles Boosting ARPU

- 4.8.5 AI-based Network Automation Cutting OPEX (Under-the-radar)

- 4.8.6 Rising Spectrum-Sharing And Neutral-Host Models (Under-the-radar)

- 4.9 Market Restraints

- 4.9.1 MDU Cable-TV Law Slashing Fixed Revenue

- 4.9.2 Stringent Energy-Efficiency Rules Raising Capex

- 4.9.3 High Fibre And 5G Capex Burden on Challengers (Under-the-radar)

- 4.9.4 OTT Voice Migration Eroding Legacy Revenues (Under-the-radar)

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Service Types (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.5 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.5.1 Deutsche Telekom

- 6.5.2 Vodafone Germany

- 6.5.3 O2 Telefonica Deutschland

- 6.5.4 1&1 AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space And Unmet-Need Assessment

行動虛擬網路營運商 (MVNO) 市場:2026-2032 年全球市場預測(按服務類型、費率方案、銷售管道、最終用戶產業和應用程式分類)5G MVNO市場:按套餐類型、最終用戶、設備類型、銷售管道、產業和網路類型分類-2026-2032年全球市場預測

行動虛擬網路營運商 (MVNO) 市場:2026-2032 年全球市場預測(按服務類型、費率方案、銷售管道、最終用戶產業和應用程式分類)5G MVNO市場:按套餐類型、最終用戶、設備類型、銷售管道、產業和網路類型分類-2026-2032年全球市場預測 2026年全球行動虛擬網路營運商(MVNO)市場報告

2026年全球行動虛擬網路營運商(MVNO)市場報告 行動虛擬網路營運商 (MVNO) 市場規模、佔有率、趨勢和預測:按類型、商業模式、服務類型、用戶數量和地區分類,2026-2034 年

行動虛擬網路營運商 (MVNO) 市場規模、佔有率、趨勢和預測:按類型、商業模式、服務類型、用戶數量和地區分類,2026-2034 年 行動虛擬網路營運商 (MVNO) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類

行動虛擬網路營運商 (MVNO) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類 亞太地區行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)美國行動虛擬網路營運商:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

亞太地區行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)美國行動虛擬網路營運商:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)