|

市場調查報告書

商品編碼

1906212

義大利電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Italy Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

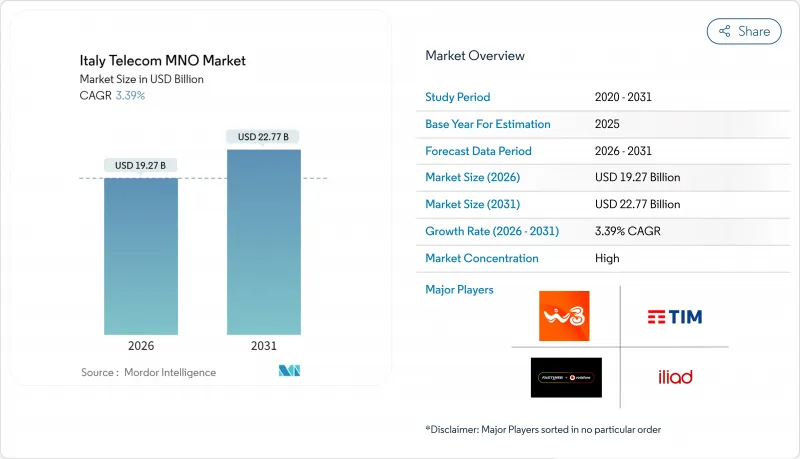

預計到 2026 年,義大利電信行動網路營運商 (MNO) 市場的規模將達到 192.7 億美元。

這代表著從 2025 年的 186.4 億美元成長到 2031 年的 227.7 億美元,2026 年至 2031 年的複合年成長率為 3.39%。

這一上升趨勢主要受數據消費量成長、5G覆蓋範圍擴大、政府支持的光纖部署以及固網行動融合服務的推動。整合舉措,尤其是瑞士電信以80億歐元(92.2億美元)收購沃達豐義大利以及KKR以188億歐元(216.6億美元)收購TIM的NetCo部門,正在重塑競爭格局,提高資本效率,並穩定每位用戶平均收入(ARPU)。儘管數據和網際網路服務佔據了最大的收入佔有率,但物聯網連接和企業數位化正在推動成長。通訊業者透過共用鐵塔和採購再生能源來降低電力成本,從而緩解了電費上漲帶來的壓力。總體而言,義大利行動網路營運商(MNO)市場正處於一個日趨成熟且可再生變革的環境中,這推動著其穩步、以價值為導向的擴張。

義大利電信行動網路營運商市場趨勢與洞察

5G用戶數量不斷增加

義大利的5G網路覆蓋率已超過90%,使其成為歐盟次世代接取的領導者。義大利電信(TIM)計畫在2026年將室外5G網路覆蓋率提升至95%,並將每GB流量成本較4G網路降低高達50%。國家復甦與韌性計畫(NRRP)提供的20.2億歐元(約23.3億美元)資金正用於補貼21,900個無線基地台的回程傳輸光纖網路建設,以填補商業性收入薄弱地區的空白。此外,工廠和港口正在部署專用5G網路,從而提升資料密集度和業務收益。因此,隨著5G技術的廣泛應用,義大利行動網路營運商(MNO)市場可望保持高速成長動能。

支援 ARPU 的融合套餐

將固定寬頻、行動服務和內容捆綁在一起,能夠提高客戶留存率並支撐平均收入水平,尤其是在較富裕的北部各州。 Fastweb 與 Vodafone 的合作預計將推出覆蓋全國的融合提案,從而降低解約率並促進交叉銷售。營運商正利用其光纖網路來提升銷售高階行動資料方案的銷量,並限制價格下滑。米蘭的早期成功案例表明,當光纖和 5G 聯合推廣時,多業務組合的訂閱率提高了 10 個百分點。這些措施正幫助義大利電信行動網路營運商 (MNO) 市場保持基於價值而非數量的成長。

激烈的行動網路業者價格競爭對利潤率造成壓力

自 Iliad 於 2018 年進入市場以來,激烈的價格競爭導致行動用戶平均收入 (ARPU) 下降,解約率上升。儘管由於行業整合,直接的價格戰有所減少,但低價服務仍然是競爭的主要來源,尤其是在預付市場。業者正透過內容捆綁和速度分級等提升銷售策略來應對。因此,預計在價格趨於一致之前,義大利電信行動網路營運商 (MNO) 市場的短期收入壓力將導致複合年成長率 (CAGR) 下降約 1 個百分點。

細分市場分析

到2025年,數據和網路服務將成為最大的收入驅動力,佔義大利電信行動網路營運商(MNO)市場佔有率的42.65%。儘管物聯網(IoT)和機器對機器(M2M)解決方案的絕對規模仍然小規模,但在工業自動化和智慧城市計劃的推動下,它們將實現最高的複合年成長率(CAGR),達到3.46%。隨著串流媒體、雲端遊戲和遠端辦公的普及,千兆位元組(GB)消費量不斷增加,義大利電信行動網路營運商以數據為中心的服務市場規模將穩步擴大。語音和簡訊使用量的下降持續釋放網路容量,用於更高價值的數據套餐,而OTT通訊則對傳統收入構成越來越大的壓力。通訊業者正透過分級5G套餐以及與Netflix、亞馬遜和DAZN等內容提供商的合作,將流量成長變現,從而提升用戶的平均消費水準。固移融合(FMC)將光纖回程傳輸與5G頻譜結合,進一步鞏固資料領域的領先地位,確保所有裝置都能提供一致的使用者體驗。

隨著WhatsApp和Telegram等應用程式以極低的額外成本滿足大多數消費者的需求,通訊和傳統語音業務的收入持續下滑。然而,通訊業者正利用進階通訊服務(RCS)和5G獨立組網(SA)功能,推出低延遲的企業級無線語音(VoNR)和關鍵任務型一鍵通話(PTT)服務。預計隨著物聯網(IoT)的發展,義大利的行動網路營運商(MNO)市場規模將同步成長,物流、智慧農業和公共產業等產業將廣泛應用窄帶物聯網(NB-IoT)技術,從而提供經濟高效且節能的連接。整體而言,基於數據生態系統的服務多元化將抵消傳統收入來源的下滑,確保均衡的成長結構。

義大利電信行動網路營運商 (MNO) 市場按服務類型(語音服務、數據和網路服務、通訊服務、物聯網和機器對機器 (M2M) 服務、OTT 和付費電視服務、其他服務)和最終用戶(企業、消費者)進行細分。市場預測以價值(美元)和用戶數量(用戶數)為單位。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 監理與政策框架

- 當前競爭格局中的頻寬狀況和擁有情形

- 通訊業生態系統

- 宏觀經濟與外在因素

- 波特五力分析

- 競爭對手之間的競爭

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 領先行動網路營運商的關鍵績效指標(2020-2025)

- 獨立行動用戶和滲透率

- 行動網路使用者數量和普及率

- 按接入技術分類的SIM卡連線數和滲透率

- 蜂巢式物聯網/M2M連接

- 寬頻連線(移動和固定)

- ARPU(每位用戶平均收入)

- 用戶平均每月數據使用量(GB/月)

- 市場促進因素

- 5G用戶數量不斷增加

- 維持ARPU值的融合套餐

- 義大利政府資助興建1Gbps光纖連接(FTTH)

- 企業對物聯網連結的需求日益成長。

- OTT影片的激增導致數據使用量增加

- 鐵塔共用/網路即服務 (NaaS) 可降低資本支出(低利率)

- 市場限制

- 行動網路營運商之間激烈的價格競爭導致利潤空間被壓縮

- 行動終端費監管減免

- 南方地區光纖普及度緩慢(這一因素很少受到關注)

- 網路能源成本不斷上漲與相互衝突的環境目標(一個被忽視的問題)

- 技術展望

- 電信業主要經營模式分析

- 定價模式和定價分析

第5章 市場規模與成長預測

- 電信總收入和每用戶平均收入

- 按服務類型

- 語音服務

- 數據和網際網路服務

- 通訊服務

- 物聯網和機器對機器服務

- OTT和付費電視服務

- 其他服務(例如附加價值服務、漫遊和國際服務、企業和批發服務)

- 最終用戶

- 公司

- 一般消費者

第6章 競爭情勢

- 市場集中度

- 主要供應商的策略與投資動向(2023-2025)

- 2024年行動網路營運商市場佔有率分析

- 行動網路營運商概況(用戶數、流失率、ARPU 等)

- MNO公司簡介

- Telecom Italia(TIM)

- WindTre

- Iliad Italia

- Fastweb+Vodafone

第7章 市場機會與未來展望

Italy Telecom MNO Market size in 2026 is estimated at USD 19.27 billion, growing from 2025 value of USD 18.64 billion with 2031 projections showing USD 22.77 billion, growing at 3.39% CAGR over 2026-2031.

This uptrend stems from rising data consumption, expanding 5G coverage, government-backed fiber rollouts, and the shift toward converged fixed-mobile offerings. Consolidation moves, notably Swisscom's EUR 8 billion (USD 9.22 billion) purchase of Vodafone Italia and KKR's EUR 18.8 billion (USD 21.66 billion) acquisition of TIM's NetCo, are reshaping the competitive landscape, improving capital efficiency, and stabilizing average revenue per user. Data and Internet services command the largest revenue share, while IoT connections and enterprise digitalization propel incremental growth. Operators are trimming energy bills through tower sharing and renewable sourcing, easing pressure from high electricity prices. Overall, a maturing yet reforming environment positions the Italy Telecom MNO market for steady, value-focused expansion.

Italy Telecom MNO Market Trends and Insights

Increasing 5G Subscriber Uptake

5G population coverage already exceeds 90%, placing Italy among the EU front-runners for next-generation access. TIM plans to raise outdoor 5G coverage to 95% by 2026, cutting cost per gigabyte by up to 50% compared with 4G operations. National Recovery and Resilience Plan (NRRP) funds worth EUR 2.02 billion (USD 2.33 billion) subsidize backhaul fiber to 21,900 radio sites, closing gaps where commercial returns are weak. Private 5G networks are gaining traction in factories and ports, raising data intensity and service revenues. Wider 5G adoption will therefore keep the Italy Telecom MNO market on a higher growth slope.

Convergent Bundles Sustaining ARPU

Bundling fixed broadband, mobile service, and content is lifting customer stickiness and supporting average revenue levels, particularly in affluent northern provinces. The Fastweb-Vodafone tie-up promises nationwide, converged propositions that reduce churn and spur cross-sell uptake. Operators leverage fiber footprints to upsell premium mobile data plans, limiting tariff erosion. Early success stories in Milan show a 10 percentage-point uplift in multi-play take-up when fiber and 5G are jointly promoted. Such dynamics keep the Italy Telecom MNO market on a value rather than volume footing.

Intense MNO Price Wars Compressing Margins

Fierce tariff battles since Iliad's 2018 arrival sliced mobile ARPU and pushed churn upward. Although consolidation is reducing head-to-head discounts, entry-level offers remain aggressive, especially in prepaid segments. Operators respond with upsell tactics such as content bundles and speed tiers. Near-term profitability pressure, therefore, reduces the Italy Telecom MNO market CAGR by almost one percentage point until price equilibrium is reached.

Other drivers and restraints analyzed in the detailed report include:

- Govt. Italia a 1 Gbps FTTH Funding

- Rising Enterprise IoT Connectivity Demand

- High Network Energy Costs vs. Green Targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data and Internet services represented the largest revenue slice, capturing 42.65% of Italy Telecom MNO market share in 2025. IoT and M2M solutions, while still small in absolute terms, deliver the highest 3.46% CAGR, underpinned by industrial automation and smart-city projects. The Italy Telecom MNO market size for data-centric services will expand steadily as streaming, cloud gaming, and remote work heighten gigabyte consumption. Declining voice and SMS uptake continues to free network capacity for richer data packages, while OTT messaging tightens pressure on legacy revenues. Operators monetize traffic growth through speed-tiered 5G plans and content tie-ups with Netflix, Amazon, and DAZN, strengthening average spending levels. Fixed-mobile convergence further cements data dominance by marrying fiber backhaul with 5G spectrum, ensuring robust user experience across devices.

Messaging and traditional voice revenues keep sliding because WhatsApp, Telegram, and similar applications meet most consumer needs at negligible incremental cost. Nonetheless, operators are leveraging rich communication services (RCS) and 5G standalone capabilities to introduce low-latency enterprise voice over New Radio (VoNR) and mission-critical push-to-talk. The Italy Telecom MNO market size, aligned with IoT gains, is expected to experience momentum in sectors such as logistics, smart agriculture, and utilities, where wide-area NB-IoT coverage provides economical and battery-efficient connectivity. Overall, service diversification based on data ecosystems will outweigh the contraction of legacy revenue lines and secure a balanced growth mix.

The Italy Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and Other Services), and End User (Enterprises, Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- Telecom Italia (TIM)

- WindTre

- Iliad Italia

- Fastweb + Vodafone

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 Market Landscape

- 4.1 Market Overview

- 4.2 Regulatory And Policy Framework

- 4.3 Spectrum Landscape And Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic And External Drivers

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers And Penetration Rate

- 4.7.2 Mobile Internet Users And Penetration Rate

- 4.7.3 SIM Connections by Access Technology And Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile And Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 Increasing 5G subscriber uptake

- 4.8.2 Convergent bundles sustaining ARPU

- 4.8.3 Govt. Italia a 1 Gbps-FTTH funding

- 4.8.4 Rising enterprise IoT connectivity demand

- 4.8.5 Surge in OTT video boosting data usage

- 4.8.6 Tower-sharing / NaaS lowering capex (under-the-radar)

- 4.9 Market Restraints

- 4.9.1 Intense MNO price wars compressing margins

- 4.9.2 Regulatory cuts to mobile termination rates

- 4.9.3 Rural South fiber take-up lag (under-the-radar)

- 4.9.4 High network energy costs vs. green targets (under-the-radar)

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.5 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.5.1 Telecom Italia (TIM)

- 6.5.2 WindTre

- 6.5.3 Iliad Italia

- 6.5.4 Fastweb + Vodafone

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space And Unmet-Need Assessment

行動虛擬網路營運商 (MVNO) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類

行動虛擬網路營運商 (MVNO) 市場分析及預測(至 2035 年):按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、解決方案和功能分類 亞太地區行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)美國行動虛擬網路營運商:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)美國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年)西班牙電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)越南電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)東協行動虛擬網路營運商(MVNO):市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)美國行動虛擬網路營運商:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)美國電信行動網路營運商:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031 年)西班牙電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)越南電信行動網路業者:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 虛擬行動服務業者(MVNO)市場-2026-2031年預測

虛擬行動服務業者(MVNO)市場-2026-2031年預測