|

市場調查報告書

商品編碼

1911387

印尼設施管理市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Indonesia Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

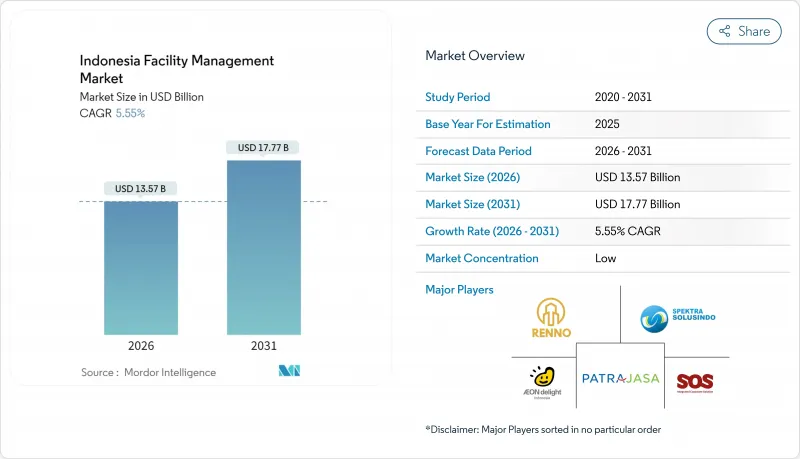

預計印尼設施管理市場將從 2025 年的 128.6 億美元成長到 2026 年的 135.7 億美元,到 2031 年將達到 177.7 億美元,2026 年至 2031 年的複合年成長率為 5.55%。

加速的都市化、31.7億美元的基礎建設資金籌措計畫以及政府設定的8%年經濟成長目標,是推動印尼設施管理市場成長要素。雅加達及其他大都會圈商業房地產活動的活性化,不斷推高了對綜合服務的需求;同時,2022年332億美元的工業投資也增加了對技術專長支援的需求。外包趨勢的興起、物聯網平台的普及以及與永續性相關的強制性要求,正在重塑營運模式。同時,薪資上漲、監管日益複雜以及人才流失加劇,都給服務提供者的利潤率帶來了壓力。因此,技術賦能的差異化和基於績效的契約,正成為印尼設施管理市場的關鍵競爭策略。

印尼設施管理市場趨勢與洞察

主要都會區的都市化

印尼城市人口的快速成長正在重塑其設施管理市場,住宅、辦公室和交通計劃激增,資產績效要求也日益嚴格。雅加達1,130萬居民給現有設施帶來了越來越大的壓力,而以公共交通為導向的開發項目(TOD)正推動房地產價值上漲高達10%,刺激了對先進維護、基於物聯網的入住率監控和預測性服務模式的需求。居住者的湧入提高了服務品質標準,迫使服務提供者在安全、衛生和數位化報告通訊協定達到全球標準。

入住率最佳化方面的進展

混合辦公模式正迫使業主和租戶釋放潛在的占地面積利用效率。設施管理人員正在部署感測器網路和分析平台,將人員佔用數據與暖通空調、照明和安防系統連接起來,從而實現可衡量的節能效果,例如PT Aspex Kumbong位於茂物(Bogor)的工廠實現了8.5%的節能。薪酬結構與績效的關聯日益增強,資料驅動型文化正在印尼的設施管理市場中興起。

主要企業面臨利潤壓力

對價格敏感的顧客和不斷上漲的工資給盈利帶來了壓力。索迪斯設施服務業務在2025年第一季成長了2.4%,印證了這一趨勢。增值稅(VAT)於2025年1月上調至12%,進一步推高了營運成本,對協商價格構成壓力。主要企業正透過自動化工單管理、精簡員工隊伍以及重新談判契約,轉向基於績效的收費系統來應對這項挑戰。

細分市場分析

到2025年,硬性服務將佔印尼設施管理市場58.42%的佔有率,這主要得益於基礎建設的擴張和大型計劃嚴格的安全標準。機電管道(MEP)工程建設佔據主導地位,這主要受熱帶氣候下空調需求增加以及緊急系統審核日益增加的推動。與新建收費公路、港口和鐵路走廊相關的資產管理項目也為穩定的費用收入提供了保障。軟性服務預計到2031年將以每年6.78%的速度成長,這主要得益於租戶對使用者體驗和衛生狀況的重視。保安、清潔和餐飲營運商正在利用智慧攝影機、機器人清潔設備和營養分析來提高效率並滿足ESG(環境、社會和治理)報告指標。醫療保健和酒店業不斷提高的服務期望正在擴大高階外包的機會,並逐步重新平衡印尼設施管理市場的收入結構。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 目前運轉率

- 主要FM業者的盈利能力

- 勞動指標 - 勞動參與率

- 按服務類型分類的設施管理市場佔有率(%)

- 以硬性服務分類的設施管理市場佔有率(%)

- 按軟體服務分類的設施管理市場佔有率(%)

- 主要都會區的都市化和人口成長

- 印尼基礎設施發展計畫中的產業投資優先事項

- 勞動和安全標準的監管促進因素

- 市場促進因素

- 主要都會區的都市化

- 最佳化運轉率的進展

- 基礎建設管道投資

- 勞動與安全法規

- ESG相關貸款的激增有利於獲得綠色認證的設施。

- 區域城市混合用途大型開發案迅速增加

- 市場限制

- 主要企業面臨利潤壓力

- 技術純熟勞工短缺

- 對進口建築自動化設備的依賴

- 分散的州級法律規範

- 價值鏈分析

- PESTEL 分析

- 新參與企業的監管和法律體制

- 宏觀經濟指標對FM需求的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

- 投資與資金籌措分析

第5章 市場規模與成長預測

- 按服務類型

- 硬服務

- 資產管理

- 機電及暖通空調服務

- 消防設備和安全措施

- 其他硬體維修服務

- 軟服務

- 辦公室支援與安全

- 清潔服務

- 餐飲服務

- 其他軟性調頻服務

- 硬服務

- 按規定表格

- 內部管理

- 外包

- 單頻調頻

- 綜合設施管理

- 綜合設施管理(綜合FM)

- 按最終用戶行業分類

- 商業設施(IT/通訊、零售/倉儲等)

- 餐飲服務業(飯店、餐廳、大型餐廳)

- 公共及公共基礎設施(政府機構、教育機構、交通運輸)

- 醫療保健(公立和私立機構)

- 工業和流程(製造業、能源業、採礦業)

- 其他終端用戶產業(多用戶住宅、娛樂、運動和休閒)

第6章 競爭情勢

- 市場集中度

- 策略發展與夥伴關係

- 市佔率分析

- 公司簡介

- PT. SGS Indonesia(Societe Generale de Surveillance SA(SGS SA))

- OCS Group Holdings Ltd

- PT Shield On Service Tbk(SOS)

- Sodexo Group

- ISS A/S

- PT Patra Jasa

- PT. Spektra Solusindo

- Titan Facility Services

- Astra Property Services

- Angkasa Pura Supports

- Colliers

- Renno Indonesia

- AEON Deligh Indonesia

- Indoservice

- Atalian Global Services

第7章 市場機會與未來展望

The Indonesia facility management market is expected to grow from USD 12.86 billion in 2025 to USD 13.57 billion in 2026 and is forecast to reach USD 17.77 billion by 2031 at 5.55% CAGR over 2026-2031.

Accelerating urbanisation, a USD 3.17 billion infrastructure financing pipeline, and the government's goal of 8% annual economic expansion are the primary growth catalysts. Commercial real-estate activity in Jakarta and other metros continues to spur demand for integrated services, while industrial investments worth USD 33.2 billion in 2022 amplify requirements for technically specialised support. Outsourcing momentum, the adoption of Internet-of-Things (IoT) platforms, and sustainability-linked mandates are reshaping operating models. Meanwhile, wage inflation, regulatory complexity and an intensifying talent drain put pressure on provider margins. Technology-enabled differentiation and outcome-based contracts therefore emerge as pivotal competitive strategies within the Indonesia facility management market.

Indonesia Facility Management Market Trends and Insights

Urbanisation in Major Metros

Soaring city populations reconfigure the Indonesia facility management market as surging housing, office and transit projects tighten asset-performance requirements. Jakarta's 11.3 million residents intensify pressure on existing stock, while transport-oriented developments raise property values by up to 10 %, triggering demand for advanced maintenance, IoT-based occupancy monitoring and predictive service models. Expatriate inflows heighten service-quality benchmarks, pushing providers toward globally aligned safety, hygiene and digital reporting protocols.

Rising Occupancy Optimisation

Hybrid work policies oblige landlords and tenants to unlock latent floor-space efficiencies. Facility managers deploy sensor networks and analytics platforms that knit occupancy data to HVAC, lighting and security systems, delivering measured energy savings such as the 8.5 % electricity reduction achieved at PT Aspex Kumbong's Bogor plant. Compensation structures are increasingly tied to utilisation outcomes, cementing a data-driven culture across the wider Indonesia facility management market.

Margin Pressure on Leading Firms

Price-sensitive clients and rising wages compress profitability. Sodexo's Q1 2025 facilities-services growth of 2.4 % underscores the trend. A January 2025 VAT rise to 12 % further heightens operating costs, squeezing negotiated rates. Key players counter by automating work-order management, consolidating labour pools and renegotiating contracts toward performance-linked fee structures.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Pipeline Investment

- Labour and Safety Regulation

- Skilled Labour Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard Services held 58.42 % of the Indonesia facility management market share in 2025, driven by infrastructure build-out and stringent safety codes across mega-projects. Mechanical, electrical and plumbing (MEP) work dominates, backed by tropical-climate HVAC demand and stricter emergency-system audits. Asset-management programmes attached to new toll roads, ports and rail corridors underpin stable fee income. Soft Services, forecast to expand 6.78 % annually to 2031, gain momentum as occupants prioritise user experience and hygiene. Security, cleaning and catering providers leverage smart cameras, robotic cleaners and nutritional analytics to improve efficiency and satisfy ESG reporting metrics. Elevated service expectations in healthcare and hospitality amplify premium outsourcing opportunities, gradually rebalancing revenue weightings within the wider Indonesia facility management market.

The Indonesia Facility Management Market Report is Segmented by Service Type (Hard Services, and Soft Services), Offering Type (In-House, and Outsourced), and End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- PT. SGS Indonesia (Societe Generale de Surveillance SA (SGS SA))

- OCS Group Holdings Ltd

- PT Shield On Service Tbk (SOS)

- Sodexo Group

- ISS A/S

- PT Patra Jasa

- PT. Spektra Solusindo

- Titan Facility Services

- Astra Property Services

- Angkasa Pura Supports

- Colliers

- Renno Indonesia

- AEON Deligh Indonesia

- Indoservice

- Atalian Global Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.1.1 Current Occupancy Rates

- 4.1.2 Profitability Rates of Major FM Players

- 4.1.3 Workforce Indicators - Labor Participation

- 4.1.4 Facility Management Market Share (%), by Service Type

- 4.1.5 Facility Management Market Share (%), by Hard Services

- 4.1.6 Facility Management Market Share (%), by Soft Services

- 4.1.7 Urbanization and Population Growth in Major Metros

- 4.1.8 Sector Investment Priorities in Indonesia's Infrastructure Pipeline

- 4.1.9 Regulatory Drivers Specific to Labour and Safety Standards

- 4.2 Market Drivers

- 4.2.1 Urbanisation in Major Metros

- 4.2.2 Rising Occupancy Optimisation

- 4.2.3 Infrastructure Pipeline Investment

- 4.2.4 Labour and Safety Regulation

- 4.2.5 Surge in ESG-linked Financing Favoring Green-Certified Facilities

- 4.2.6 Proliferation of Mixed-Use Mega-Developments in Secondary Cities

- 4.3 Market Restraints

- 4.3.1 Margin Pressure on Leading Firms

- 4.3.2 Skilled Labour Shortages

- 4.3.3 Dependency on Imported Building Automation Hardware

- 4.3.4 Fragmented Provincial Regulatory Oversight

- 4.4 Value Chain Analysis

- 4.5 PESTEL Analysis

- 4.6 Regulatory and Legislative Framework for Market Entrants

- 4.7 Impact of Macroeconomic Indicators on FM Demand

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Services

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard FM Services

- 5.1.2 Soft Services

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Soft FM Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM

- 5.3 By End-user Industry

- 5.3.1 Commercial (IT and Telecom, Retail and Warehouses, etc.)

- 5.3.2 Hospitality (Hotels, Eateries, Large-scale Restaurants)

- 5.3.3 Institutional and Public Infrastructure (Govt, Education, Transportation)

- 5.3.4 Healthcare (Public and Private Facilities)

- 5.3.5 Industrial and Process (Manufacturing, Energy, Mining)

- 5.3.6 Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Partnerships

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 PT. SGS Indonesia (Societe Generale de Surveillance SA (SGS SA))

- 6.4.2 OCS Group Holdings Ltd

- 6.4.3 PT Shield On Service Tbk (SOS)

- 6.4.4 Sodexo Group

- 6.4.5 ISS A/S

- 6.4.6 PT Patra Jasa

- 6.4.7 PT. Spektra Solusindo

- 6.4.8 Titan Facility Services

- 6.4.9 Astra Property Services

- 6.4.10 Angkasa Pura Supports

- 6.4.11 Colliers

- 6.4.12 Renno Indonesia

- 6.4.13 AEON Deligh Indonesia

- 6.4.14 Indoservice

- 6.4.15 Atalian Global Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Technology-led Integrated FM (IoT, BMS, AI-based Predictive Maintenance)

- 7.3 ESG-compliant FM Solutions Demand

- 7.4 Future Service-Model Shifts (Outcome-based Contracts)

綜合設施管理市場:按服務類型、部署模式和最終用戶分類 - 2026-2032年全球預測菸草綜合設施管理市場:按服務類型、設施類型、合約類型、組織規模和最終用戶分類 - 2026-2032 年全球預測

綜合設施管理市場:按服務類型、部署模式和最終用戶分類 - 2026-2032年全球預測菸草綜合設施管理市場:按服務類型、設施類型、合約類型、組織規模和最終用戶分類 - 2026-2032 年全球預測 2026年設施管理領域十大成長機遇亞太地區設施管理市場,2026-2031年

2026年設施管理領域十大成長機遇亞太地區設施管理市場,2026-2031年 機器人即服務 (RaaS) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類設施管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類電腦輔助設施管理 (CAFM) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和模組分類

機器人即服務 (RaaS) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和功能分類設施管理市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、功能及解決方案分類電腦輔助設施管理 (CAFM) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和模組分類 亞太地區設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)