|

市場調查報告書

商品編碼

1910886

歐洲施工機械租賃市場:市場佔有率分析、行業趨勢、統計數據和成長預測(2026-2031 年)Europe Construction Machinery Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

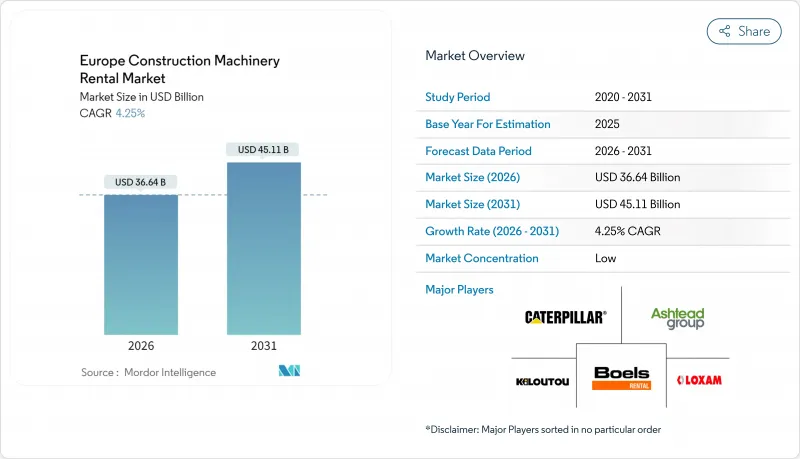

歐洲施工機械租賃市場預計將從 2025 年的 351.5 億美元成長到 2026 年的 366.4 億美元,預計到 2031 年將達到 451.1 億美元,2026 年至 2031 年的複合年成長率為 4.25%。

這一穩步成長反映了對租賃機械的強勁需求、設備即服務 (EaaS) 合約的擴張以及全部區域因排放氣體法規而進行的車隊更新。歐洲施工機械租賃市場受益於歐盟支持的基礎設施獎勵策略、快速的電氣化強制措施以及降低永續車隊資本成本的 ESG 相關融資。營運商優先考慮透過遠端資訊處理技術提高運轉率,而各國政府則透過綠色交通走廊和數位連接計劃來刺激需求。隨著原始設備製造商 (OEM) 建立直接租賃部門、傳統租賃巨頭加快在歐洲的收購步伐以及數位市場降低搜尋和與承包商交易的成本,競爭日益激烈。

歐洲施工機械租賃市場趨勢與洞察

歐盟基礎設施獎勵策略規模擴大(2025年及以後)

歐洲投資銀行已承諾在2030年投入1.1兆歐元用於氣候友善基礎設施建設,而交通和數位走廊的計劃帶動了對挖土機、鋪路機和塔式起重機租賃的持續需求。德國正大力推動基礎設施和數位化能力的現代化。未來幾年,德國已獲得大量投資,用於升級交通網路並加速數位轉型,催生了對專用土方車輛的需求。與以往週期不同,目前的預算撥款專注於可再生能源和光纖部署,迫使租賃公司採購諸如電纜犁和風力發電機機安裝起重機等專用設備。供應緊張導致運轉率上升,並引發短期價格上漲。經濟獎勵策略的連鎖反應也正蔓延至交通樞紐周邊的私人住宅和商業建設領域。

加速推進車輛電氣化

歐盟委員會的「Fit for 55」計畫要求到2030年將排放減少55%,迫使租賃公司從柴油動力系統轉向電池氫動力系統。 JCB的氫燃料引擎計畫目前正在11個國家進行試點,這是原始設備製造商(OEM)應對這項挑戰的一個例證。瑞典和挪威的領先利用補貼來彌補更高的購買成本,並將這些溢價轉讓給旨在進入零排放區的承包商。此強制性要求還鼓勵對充電站、技術人員再培訓和數位化監控系統進行同步投資,從而在提高資本密集度的同時降低生命週期成本。

非道路移動機械引入中的不協調之處 第五階段

非道路移動機械第五階段排放法規於2019年生效,但各成員國的處罰力度不一,迫使租賃車隊業者應對雙重合規標準。跨境營運的公司為了確保每台設備都符合最嚴格的區域標準,正面臨日益成長的物流和改裝成本。

細分市場分析

截至2025年,土木機械佔歐洲施工機械租賃市場的41.88%,預計到2031年,該類別將以4.55%的複合年成長率成長。履帶挖土機尤其在主導,而輪式挖土機則為都市區交通提供支援。滑移裝載機在需要緊湊型移動性的維修計劃中需求日益成長。平地平土機和推土機則協助東歐高速公路網的擴建。歐洲施工機械租賃市場中挖掘和平整領域的規模也是電氣化試點計畫的重點,例如日立計畫於2027年推出的1.7噸電池驅動挖土機。

隨著建築公司在不影響性能的前提下尋求滿足城市排放法規,該行業的電氣化進程正在加速。原始設備製造商 (OEM) 正在試驗可更換電池組以減少充電運作,而租賃公司則引入行動充電器以維持運轉率。領先的租賃公司正在將土木機械與現場電源裝置捆綁銷售,以提供整合式增值解決方案。

由於液壓系統擁有久經考驗的可靠性和廣泛的服務網路,預計到2025年,其在歐洲施工機械租賃市場仍將佔據77.95%的佔有率。然而,在北歐國家補貼政策和都市區低排放區不斷擴大的推動下,純電動驅動系統預計將實現11.85%的複合年成長率。柴油-電動混合動力系統則提供了一種過渡方案,既能節省燃油,又能避免在偏遠地區出現續航里程焦慮。

歐洲施工機械租賃市場不同機型的普及速度各不相同。小型挖土機和剪式升降機正迅速完成運作,因為電池能量密度的提升使其能夠實現全班作業。而大型設備則在等待下一代固態電池和氫燃料電池的到來,JCB正在進行的試驗顯示其具有長期發展潛力。租賃公司正透過引入可在柴油和電力驅動系統之間切換的模組化車隊來分散風險。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐盟基礎設施獎勵策略大幅成長(2025年及以後)

- 加速車隊電氣化強制措施

- 透過與環境、社會及公司治理(ESG)相關的融資方式降低資本支出(CAPEX)。

- 轉向設備即服務模式

- 重點關注歐盟分類法中的碳含量報告

- 用於零空轉運轉的現場安裝式模組化電源單元

- 市場限制

- 非道路移動機械(NRMM)第五階段實施中的不協調

- 由於操作人員短缺,人事費用不斷上升。

- 由於柴油資產過時,次市場供應過剩

- 老舊機隊遙測改造高成本

- 價值/供應鏈分析

- 監管環境

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

5. 市場規模及成長預測(價值,百萬美元)

- 按機器類型

- 土木工程施工機械

- 挖土機

- 履帶

- 帶輪子的

- 裝載機

- 滑移裝載機

- 車輪

- 後鏟

- 平土機機

- 推土機

- 挖土機

- 起重和物料輸送

- 起重機

- 移動式起重機

- 塔式起重機

- 伸縮臂堆高機

- 高空作業平台

- 起重機

- 道路施工機械

- 攤舖機

- 壓路機

- 瀝青攪拌機

- 其他機器類型

- 土木工程施工機械

- 按驅動類型

- 油壓

- 柴油-電力混合動力

- 全電動

- 氫燃料電池

- 透過使用

- 建築施工

- 住宅

- 商業的

- 產業

- 基礎設施建設

- 公路/高速公路

- 鐵路

- 飛機場

- 能源基礎設施

- 採礦和採石

- 災害/緊急救援

- 其他用途

- 建築施工

- 按負載容量

- 輕型車輛(小於3噸)

- 中型(3至10噸)

- 大型(10至30噸)

- 超大型(超過30噸)

- 按國家/地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 瑞典

- 波蘭

- 俄羅斯

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Loxam Group

- Ashtead Group(Sunbelt Rentals)

- Kiloutou Group

- Boels Rental

- Cramo(Renta Group)

- Zeppelin Rental

- Ahern Rentals

- Ramirent

- Ardent Hire Solutions

- Mateco

- Caterpillar Inc.

- Deere & Company

- Komatsu Ltd

- Hitachi Construction Machinery

- Liebherr Group

- JCB

- Manitou Group

- MECALAC

- Wacker Neuson

- Yanmar CE

第7章 市場機會與未來展望

The European construction machinery rental market is expected to grow from USD 35.15 billion in 2025 to USD 36.64 billion in 2026 and is forecast to reach USD 45.11 billion by 2031 at 4.25% CAGR over 2026-2031.

This steady climb reflects resilient demand for rented machinery, expanding equipment-as-a-service agreements, and emission-driven fleet renewal across the region. The European construction equipment rental market benefits from EU-backed infrastructure stimulus, rapid electrification mandates, and ESG-linked lending that lowers capital costs for sustainable fleets. Operators prioritize telematics-enabled utilization gains, while governments reinforce demand with green transport corridors and digital connectivity projects. Competitive intensity is growing as OEMs form direct rental units, traditional rental giants accelerate pan-European acquisitions, and digital marketplaces shrink search and transaction costs for contractors.

Europe Construction Machinery Rental Market Trends and Insights

Surging EU Infrastructure Stimulus (Post-2025)

The European Investment Bank has earmarked EUR 1.1 trillion for climate-aligned infrastructure through 2030, triggering a sustained uptick in rentals of excavators, pavers, and tower cranes as projects break ground across transport and digital corridors . Germany is making a bold push to modernize its infrastructure and digital capabilities. A substantial investment commitment has been set aside to upgrade transport networks and accelerate digital transformation over the coming years, creating demand for specialized earthmoving fleets. Unlike past cycles, current allocations stress renewable energy and fiber rollout, forcing rental companies to secure niche machinery such as cable plows and wind-turbine erection cranes. Supply tightness amplifies utilization rates and elevates short-term pricing. Stimulus-driven linkages also ripple into private housing and commercial builds around upgraded transit hubs.

Accelerated Fleet Electrification Mandates

The European Commission's Fit for 55 package requires a 55% emissions cut by 2030, pressuring rental firms to pivot from diesel to battery and hydrogen powertrains . JCB's hydrogen engine program, now trialed in 11 countries, exemplifies OEM response. Early adopters in Sweden and Norway leverage subsidies to recoup higher purchase prices and pass premium rates to contractors looking to enter zero-emission zones. The mandate stimulates parallel investment in charging depots, technician retraining, and digital monitoring systems, raising capital intensity yet lowering lifecycle costs.

Disharmony in NRMM Stage V Adoption

Non-Road Mobile Machinery Stage V rules entered force in 2019 yet penalty rigor differs by member state, compelling rental fleets to juggle dual compliance standards. Companies operating across borders incur surging logistics and refitting costs to ensure each unit meets the strictest locale.

Other drivers and restraints analyzed in the detailed report include:

- ESG-Linked Financing Lowering CAPEX

- EU Taxonomy Focus on Embodied-Carbon Reporting

- Secondary Market Glut from Diesel Obsolescence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Earthmoving equipment accounted for 41.88% of the European construction equipment rental market share in 2025, and this category is forecast to grow at a 4.55% CAGR through 2031. Excavators, particularly crawler variants, dominate heavy civil works while wheeled models support urban mobility. Skid-steer loaders gain traction in refurbishment projects that demand compact maneuverability. Motor graders and dozers sustain demand from Eastern Europe's expanding highway corridors. The European construction equipment rental market size within earthmoving is also a focal point for electrification pilots such as Hitachi's 1.7-ton battery excavator slated for 2027 rollout.

The segment's electrification cadence accelerates as contractors seek to meet city-center emission caps without compromising performance. OEMs experiment with swappable battery packs to mitigate charging downtime, and rental houses deploy mobile chargers to keep utilization high. Tier-one rental firms bundle earthmoving packages with on-site power units to capture higher value from integrated offerings.

Hydraulic systems retained 77.95% share of the European construction equipment rental market size in 2025 because of their proven reliability and wide service network. Yet purely electric drives are posting a 11.85% CAGR, aided by Nordic subsidies and expanding urban low-emission zones. Diesel-electric hybrids offer a transitional path, providing fuel savings without range anxiety on remote sites.

The European construction equipment rental market registers divergent adoption curves by equipment class. Compact excavators and scissor lifts shift first as battery energy density now supports full-shift operation. Heavier equipment awaits next-generation solid-state batteries or hydrogen fuel cells, where JCB's ongoing trials signal longer-term promise. Rental firms hedge by procuring modular fleets that can swap between diesel and electric drivelines.

The Europe Construction Machinery Rental Market Report is Segmented by Machinery Type (Earthmoving, and More), Drive Type (Hydraulic, Diesel-Electric Hybrid, and More), Application (Building Construction, and More), End-User Industry (Construction Contractors, and More), Payload Capacity (Light-Duty, Medium-Duty, and Heavy-Duty), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Loxam Group

- Ashtead Group (Sunbelt Rentals)

- Kiloutou Group

- Boels Rental

- Cramo (Renta Group)

- Zeppelin Rental

- Ahern Rentals

- Ramirent

- Ardent Hire Solutions

- Mateco

- Caterpillar Inc.

- Deere & Company

- Komatsu Ltd

- Hitachi Construction Machinery

- Liebherr Group

- JCB

- Manitou Group

- MECALAC

- Wacker Neuson

- Yanmar CE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging EU Infrastructure Stimulus (Post-2025)

- 4.2.2 Accelerated Fleet Electrification Mandates

- 4.2.3 ESG-Linked Financing Lowering CAPEX

- 4.2.4 Shift Toward Equipment-as-a-Service Models

- 4.2.5 EU Taxonomy Focus on Embodied-Carbon Reporting

- 4.2.6 On-Site Modular Power Units Enabling Zero-Idle Use

- 4.3 Market Restraints

- 4.3.1 Disharmony in NRMM Stage V Adoption

- 4.3.2 Operator Talent Shortage Inflating Labor Costs

- 4.3.3 Secondary Market Glut from Diesel Asset Obsolescence

- 4.3.4 High Telemetry Retrofit Cost for Legacy Fleets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD Million)

- 5.1 By Machinery Type

- 5.1.1 Earthmoving Machinery

- 5.1.1.1 Excavators

- 5.1.1.1.1 Crawler

- 5.1.1.1.2 Wheeled

- 5.1.1.2 Loaders

- 5.1.1.2.1 Skid-Steer

- 5.1.1.2.2 Wheel

- 5.1.1.2.3 Backhoe

- 5.1.1.3 Motor Graders

- 5.1.1.4 Dozers

- 5.1.1.1 Excavators

- 5.1.2 Lifting and Material-Handling

- 5.1.2.1 Cranes

- 5.1.2.1.1 Mobile Cranes

- 5.1.2.1.2 Tower Cranes

- 5.1.2.2 Telescopic Handlers

- 5.1.2.3 Aerial Work Platforms

- 5.1.2.1 Cranes

- 5.1.3 Road Construction Equipment

- 5.1.3.1 Pavers

- 5.1.3.2 Road Rollers

- 5.1.3.3 Asphalt Mixers

- 5.1.4 Other Machinery Types

- 5.1.1 Earthmoving Machinery

- 5.2 By Drive Type

- 5.2.1 Hydraulic

- 5.2.2 Diesel-Electric Hybrid

- 5.2.3 Fully Electric

- 5.2.4 Hydrogen Fuel Cell

- 5.3 By Application

- 5.3.1 Building Construction

- 5.3.1.1 Residential

- 5.3.1.2 Commercial

- 5.3.1.3 Industrial

- 5.3.2 Infrastructure Construction

- 5.3.2.1 Road and Highway

- 5.3.2.2 Rail

- 5.3.2.3 Airport

- 5.3.2.4 Energy Infrastructure

- 5.3.3 Mining and Quarrying

- 5.3.4 Disaster and Emergency Relief

- 5.3.5 Other Applications

- 5.3.1 Building Construction

- 5.4 By Payload Capacity

- 5.4.1 Light-Duty (Below 3 tons)

- 5.4.2 Medium-Duty (3-10 tons)

- 5.4.3 Heavy-Duty (10-30 tons)

- 5.4.4 Super Heavy-Duty (Above 30 tons)

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Sweden

- 5.5.8 Poland

- 5.5.9 Russia

- 5.5.10 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Loxam Group

- 6.4.2 Ashtead Group (Sunbelt Rentals)

- 6.4.3 Kiloutou Group

- 6.4.4 Boels Rental

- 6.4.5 Cramo (Renta Group)

- 6.4.6 Zeppelin Rental

- 6.4.7 Ahern Rentals

- 6.4.8 Ramirent

- 6.4.9 Ardent Hire Solutions

- 6.4.10 Mateco

- 6.4.11 Caterpillar Inc.

- 6.4.12 Deere & Company

- 6.4.13 Komatsu Ltd

- 6.4.14 Hitachi Construction Machinery

- 6.4.15 Liebherr Group

- 6.4.16 JCB

- 6.4.17 Manitou Group

- 6.4.18 MECALAC

- 6.4.19 Wacker Neuson

- 6.4.20 Yanmar CE

7 Market Opportunities & Future Outlook

施工機械市場規模、佔有率、趨勢和預測:按解決方案類型、機器類型、應用、行業和地區分類,2026-2034年

施工機械市場規模、佔有率、趨勢和預測:按解決方案類型、機器類型、應用、行業和地區分類,2026-2034年 2026年全球挖溝機市場報告2026年全球施工機械售後市場報告2026年全球水泥和砂漿測試設備市場報告

2026年全球挖溝機市場報告2026年全球施工機械售後市場報告2026年全球水泥和砂漿測試設備市場報告 施工機械市場:2026-2032年全球市場預測(依產品類型、功率輸出、燃料類型、設計類型、運作小時數、銷售管道和最終用戶分類)橡膠壓機市場:依橡膠類型、壓機類型、操作模式、產能、應用及通路分類-全球預測,2026-2032年電動施工機械市場:依設備類型、推進系統和應用分類-全球預測,2026-2032年自動液壓機市場:按壓機類型、控制類型、操作模式和終端用戶產業分類,全球預測,2026-2032年

施工機械市場:2026-2032年全球市場預測(依產品類型、功率輸出、燃料類型、設計類型、運作小時數、銷售管道和最終用戶分類)橡膠壓機市場:依橡膠類型、壓機類型、操作模式、產能、應用及通路分類-全球預測,2026-2032年電動施工機械市場:依設備類型、推進系統和應用分類-全球預測,2026-2032年自動液壓機市場:按壓機類型、控制類型、操作模式和終端用戶產業分類,全球預測,2026-2032年 2026 年至 2035 年施工機械輪胎市場的商業機會、成長要素、產業趨勢分析與預測。

2026 年至 2035 年施工機械輪胎市場的商業機會、成長要素、產業趨勢分析與預測。 中國施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中國施工機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)