|

市場調查報告書

商品編碼

1907314

歐洲軟包裝市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Europe Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

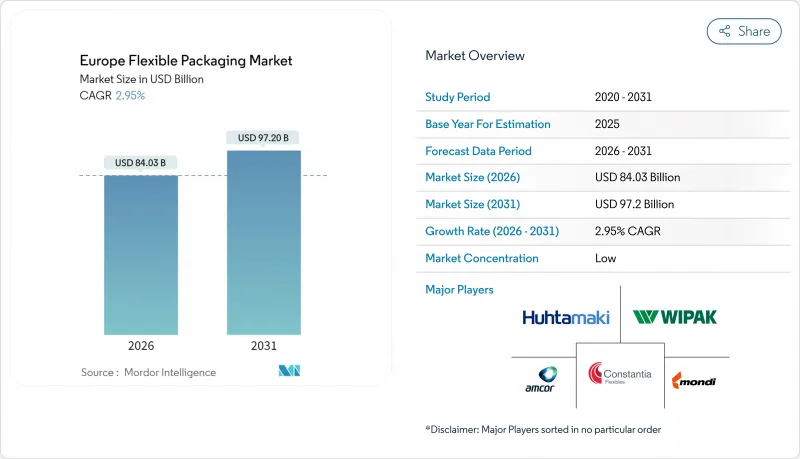

歐洲軟包裝市場預計到 2026 年價值將達到 840.3 億美元,高於 2025 年的 816.2 億美元。預計到 2031 年將達到 972 億美元,2026 年至 2031 年的複合年成長率為 2.95%。

這一成長趨勢主要受歐盟更嚴格的回收法規、不斷成長的電子商務包裹量以及消費者對保存期限長的便捷食品日益成長的需求所驅動。隨著《包裝和包裝廢棄物法規》(PPWR) 推動到2030年實現30%的再生塑膠含量,單一材料薄膜的創新正在加速,而可生物分解材料的選擇也在小規模擴張。品牌所有者繼續轉向輕包裝袋以降低物流成本,但由於薄膜和包裝紙在食品和工業產品線中的廣泛應用,它們仍然佔據銷售主導地位。市場競爭適中,前七大供應商的銷售額僅佔約四分之一,這為區域性專業企業在阻隔技術和數位印刷領域抓住利基市場機會創造了空間。

歐洲軟包裝市場趨勢與洞察

歐盟循環經濟目標推動對可再生單一材料薄膜的需求激增

包裝廢棄物指令 (PPWR) 要求到 2030 年,在歐洲銷售的所有包裝都必須可回收利用,這迫使加工商將多層結構重新設計為可機械回收的單一材料形式。雀巢公司報告稱,其用於寵物食品的聚丙烯殺菌袋的碳足跡減少了 60%,而 Cycaflex 計劃在 2025 年推出一系列完全可回收的產品,這些產品均採用消費後回收材料。由於紙張不受再生材料含量強制規定的約束,因此紙基替代品(例如科勒紙業的 NexPlus Barrier 系列)正日益受到青睞。為了彌補多層結構性能的下降,供應商正在測試無機塗層,例如 ORMOCER,它可以將聚丙烯基材上的氧氣透過率降低 95%。對不可可再生材料徵收生產者延伸責任成本加快了這一進程。

電子商務的快速成長推動了對軟性郵件包裝和保護的需求。

在許多歐盟市場,線上零售持續保持兩位數成長,推動了輕質郵寄袋和保護膜的普及,從而降低了每個小包裹的運輸成本。像HP Indigo 200K這樣的數位印刷機能夠實現個性化的包裝圖案,用於季節性和區域性促銷活動,並且與柔版印刷機相比,減少了設置廢棄物。 Uteco的混合平台Sapphire Aqua採用符合食品接觸法規的低遷移水性油墨,以1200 x 1200 dpi的解析度和150米/分鐘的速度進行列印。中小電商企業擴大將履約外包,並透過間接經銷商進行出貨,這些分銷商更傾向於使用與自動化包裝線相容的軟性包裝形式。

歐盟更嚴格的塑膠和包裝廢棄物法規增加了合規成本。

中小型加工商被迫在可回收性認證、再生樹脂整合和圖形重新設計方面投入巨資,以滿足統一的標籤標準。不合規包裝的生產者延伸責任(EPR)費用可能使交付成本增加50%以上,在新的生產線投入運作之前,利潤空間將被壓縮。 2026年生效的PFAS禁令將迫使食品包裝以防油塗層進行配方調整,而2028年生效的標籤規則將促使數千個SKU的圖案設計改變。

細分市場分析

到2025年,塑膠將佔歐洲軟包裝市場61.88%的佔有率,主要得益於聚乙烯在食品和電商領域的成本績效優勢。儘管石油基材仍主導,但隨著品牌商追求生產者延伸責任(PPWR)合規性,歐洲軟包裝市場對生物基和可堆肥薄膜的興趣日益濃厚,複合年成長率(CAGR)達到5.66%。紙張和紙板不受再生材料含量強制規定的約束,科勒紙業等供應商正在取得進展,其阻隔塗層等級的再生材料含量已達81.5%。金屬化結構在醫藥和高階食品應用領域仍然很受歡迎,因為這些領域對絕對阻隔性很高,但由於其小眾需求,受市場波動的影響較小。 PET的化學回收(包括解聚成與原生材料相當的原料)旨在確保到2027年食品級樹脂的穩定供應,這可能是PET在日益嚴格的回收目標下穩定市場地位的關鍵里程碑。

歐洲軟包裝市場目前正在測試一種混合複合材料,將傳統的聚烯層與可生物分解塗層結合。這種材料能夠加速污垢分解,同時在整個保存期限內保持密封完整性。雖然雙向拉伸聚丙烯(BOPP)仍然是透明零食薄膜的主要材料,但聚丙烯(CPP)因其優異的密封性能而成為蒸餾罐蓋的首選材料。儘管生質塑膠目前僅佔總產量的一小部分,但它們正從可堆肥購物袋發展成為由聚乳酸(PLA)、聚丁二烯丙基三丙烯酸酯(PBAT)和澱粉混合物製成的高阻隔結構。加工商預測,在2028年或之後,隨著相關法規的推出以推動需求和原料規模化生產,生物塑膠的成本競爭力將難以與化石基材料相提並論。

到2025年,薄膜和包裝膜將佔歐洲軟包裝市場43.92%的佔有率,主要面向烘焙產品、起司和工業零件等大眾消費品類別。然而,在適應便利消費生活方式的產品(例如可蒸餾的蒸餾食品包裝和微波爐即食食品)的推動下,軟包裝袋市場將持續成長,到2031年將維持6.55%的複合年成長率。自立式包裝形式能更好地利用貨架空間,提升品牌知名度,因此更受零售商青睞。雀巢的可回收高溫殺菌殺菌袋展示了其如何在保持性能的同時,與傳統包裝相比減少60%的碳足跡(《包裝摘要》)。

在農作物種子、肥料和DIY市場,由於重量限制,薄壁包裝的應用受到限制,因此軟包裝袋仍佔據主導地位。數位印刷技術的廣泛應用使得加工商能夠為5000件以下的小批量產品提供SKU級別的客製化服務,這鼓勵了小眾高階品牌在其產品生命週期的早期階段就採用軟包裝袋,而不會影響單位經濟效益。外包裝和收縮膜套標作為防篡改解決方案在飲料和製藥行業仍然十分重要,但其可回收性正受到越來越多的關注。歐洲PET塑膠擁有率的兩位數成長進一步推動了對殺菌袋袋和立式袋能夠確保產品的保鮮度和香氣。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 為回應歐盟循環經濟目標,對可再生單一材料薄膜的需求激增。

- 歐洲電子商務的加速成長正在推動對軟性郵寄袋和保護性包裝的需求。

- 消費者對便利性和份量控制產品的偏好推動了柔軟性袋的普及。

- 透過開發高阻隔共擠壓技術延長蒸餾食品的保存期限

- 數位印刷和混合印刷技術的日益普及,使得小批量生產和大規模客製化成為可能。

- 歐洲寵物食品產業利用蒸餾和立式袋快速擴張

- 市場限制

- 歐盟更嚴格的塑膠和包裝廢棄物法規增加了合規成本。

- 多層薄膜回收基礎設施有限,阻礙了循環經濟目標的實現。

- 能源危機後聚烯和鋁箔價格的波動將影響利潤率。

- 來自永續性的品牌的來自嚴格的再生替代品的競爭壓力

- 供應鏈分析

- 監理展望

- 技術展望

- 投資分析

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 依材料類型

- 塑膠

- 聚乙烯(PE)

- 雙軸延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 聚對苯二甲酸乙二醇酯(PET)

- 聚苯乙烯(PS)和發泡聚苯乙烯(EPS)

- 其他塑膠類型

- 紙和紙板

- 金屬

- 可生物分解和可堆肥材料

- 塑膠

- 依產品類型

- 小袋

- 包包

- 薄膜和包裝

- 其他產品類型

- 按最終用戶行業分類

- 食物

- 飲料

- 醫療和藥品

- 化妝品和個人護理

- 工業的

- 其他終端用戶產業

- 按發行格式

- 直銷

- 間接銷售

- 按國家/地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Amcor PLC

- Mondi Group

- Huhtamaki Oyj

- Constantia Flexibles GmbH

- Sealed Air Corporation

- Coveris Management GmbH

- ProAmpac LLC

- Novolex Holdings Inc.

- Sonoco Products Company

- Bischof+Klein SE & Co. KG

- Wipak Oy

- Schur International A/S

- Gualapack SpA

- ePac Holdings LLC

- Danaflex Group

- Cellografica Gerosa SpA

- Di Mauro Officine Grafiche SpA

- Bak Ambalaj Sanayi ve Ticaret AS

- Flextrus AB

- Sipospack Kft.

- Clondalkin Flexible Packaging

- Innovia Films Ltd.

- AR Packaging Group AB

- RKW Group

- Plastopil Hazorea Co. Ltd.

- Schur Flexibles Group

- Glenroy Inc.

- Leefung ASG Europe

第7章 市場機會與未來展望

Europe flexible packaging market size in 2026 is estimated at USD 84.03 billion, growing from 2025 value of USD 81.62 billion with 2031 projections showing USD 97.2 billion, growing at 2.95% CAGR over 2026-2031.

This trajectory follows tougher EU recycling mandates, expanding e-commerce parcel volumes, and accelerating demand for convenience foods that need extended shelf life. Mono-material film innovation is gathering pace as the Packaging and Packaging Waste Regulation (PPWR) pushes for 30% recycled plastic content by 2030, while biodegradable options are scaling from a small base. Brand owners continue to migrate toward lightweight pouches that cut logistics costs, yet films and wraps still dominate on volume thanks to their versatility in food and industrial lines. Moderate competitive intensity-as the seven largest suppliers together control only about one quarter of sales-creates room for regional specialists to capture niche opportunities in barrier technology and digital printing.

Europe Flexible Packaging Market Trends and Insights

Surge in Demand for Recyclable Mono-Material Films Driven by EU Circular Economy Targets

The PPWR obliges every package sold in Europe to be recyclable by 2030, prompting converters to redesign multilayer structures into mono-material formats that pass mechanical recycling streams. Nestle reports 60% carbon-footprint savings from polypropylene retort pouches for pet food, while Saica Flex plans a fully recyclable portfolio by 2025 that integrates post-consumer recyclate. Paper's exemption from recycled-content quotas gives a lift to paper-based alternatives such as Koehler Paper's NexPlus barrier line. To compensate for lost multilayer performance, suppliers are testing ORMOCER and other inorganic coatings that cut oxygen transmission rates by 95% on PP substrates. Extended Producer Responsibility fees now penalize non-recyclable materials, compressing timetables for adoption.

Accelerated Growth of E-Commerce Elevating Demand for Flexible Mailer & Protective Formats

Online retail continues to expand double-digit in many EU markets, spurring uptake of lightweight mailers and protective films that reduce freight cost per parcel. Digital presses such as HP Indigo 200K allow brands to personalize outer graphics for seasonal or regional promotions, while cutting set-up waste versus flexography. Uteco's SapphireAQUA hybrid platform prints 1,200 X 1,200 DPI at 150 mpm using low-migration, water-based inks that fulfil food-contact rules. Smaller e-commerce brands increasingly outsource fulfillment, channeling more volume through indirect distributors who favor flexible formats compatible with automated packing lines.

Stringent EU Plastics & Packaging-Waste Regulations Increasing Compliance Costs

Smaller converters face steep investments to certify recyclability, integrate recycled resin, and redesign graphics to meet harmonized labeling. Extended Producer Responsibility fees for non-compliant packs can add 50% or more to delivered cost, squeezing margins until new lines come on-stream. PFAS bans hitting in 2026 will force reformulation of grease-resistant coatings for food wraps, while labeling rules effective 2028 drive artwork changeovers across thousands of SKUs.

Other drivers and restraints analyzed in the detailed report include:

- Consumer Shift Toward Convenience & Portion-Control Products Boosting Flexible Pouch Adoption

- Technological Advances in High-Barrier Co-Extrusion Enhancing Shelf-Life for Ready Meals

- Limited Recycling Infrastructure for Multi-Layer Films Hampering Circularity Goals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics contributed 61.88% of Europe flexible packaging market share in 2025, powered by polyethylene's cost-to-performance edge in food and e-commerce lines. Petro-based substrates maintain leadership today, yet the Europe flexible packaging market is witnessing brisk interest in bio-based and compostable films expanding at a 5.66% CAGR as brand owners chase PPWR alignment. Paper and paperboard enjoy an exemption from recycled-content quotas, and suppliers such as Koehler Paper are making headway with barrier-coated grades that hit 81.5% recycling rates. Metalized structures still serve pharma and premium food where absolute barrier rules, but stand largely insulated from volume swings thanks to niche demand. Chemical recycling initiatives for PET, including depolymerization to virgin-like feedstock, aim to secure food-grade resin streams by 2027, a milestone that could stabilise PET's position amid rising recycled-content targets.

Europe flexible packaging market players are trialing hybrid laminates that pair traditional polyolefin layers with biodegradable coatings to accelerate soil decomposition while preserving seal integrity during shelf life. BOPP remains the workhorse for transparent snack films, whereas CPP is favoured for retortable lidding thanks to its sealability. Bioplastics, currently a sliver of overall tonnage, are moving beyond compostable shopping bags into high-barrier structures with blending of PLA, PBAT, and starch. Converters anticipate cost parity with fossil-based grades only after 2028, pending feedstock scale-up and mandates that spur demand.

Films and wraps carried 43.92% of Europe flexible packaging market share in 2025 because they serve high-volume categories such as bakery, cheese, and industrial components. Nonetheless, pouches are clocking a 6.55% CAGR through 2031, buoyed by retortable pet-food packs and microwaveable ready meals that fit on-the-go consumer lifestyles. Stand-up formats improve shelf utilisation and brand visibility, which retailers reward with premium placement. Nestle's recyclable retort pouch illustrates how brands can cut carbon footprints by 60% versus legacy structures while maintaining performance Packaging Digest.

Bag formats continue to dominate agricultural seeds, fertilizers, and DIY markets, where bulk weight limits the appeal of thin-wall alternatives. Digital printing's rise allows converters to offer SKU-level customisation in lot sizes below 5,000 units without compromising unit economics, encouraging niche gourmet brands to adopt pouch packaging earlier in their lifecycle. Overwraps and shrink sleeves remain relevant as tamper-evidence solutions in beverages and pharmaceuticals but face scrutiny over recyclability. Double-digit growth in European pet ownership further underpins demand for retort and stand-up pouches that guarantee product freshness and aroma protection.

The Europe Flexible Packaging Market Report is Segmented by Material Type (Plastics, Paper and Paperboard, and More), Product Type (Pouches, Bags, and More), End-User Industry (Food, Beverage, Healthcare and Pharmaceuticals, and More), Distribution (Direct Sales, Indirect Sales), and Country (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor PLC

- Mondi Group

- Huhtamaki Oyj

- Constantia Flexibles GmbH

- Sealed Air Corporation

- Coveris Management GmbH

- ProAmpac LLC

- Novolex Holdings Inc.

- Sonoco Products Company

- Bischof + Klein SE & Co. KG

- Wipak Oy

- Schur International A/S

- Gualapack SpA

- ePac Holdings LLC

- Danaflex Group

- Cellografica Gerosa SpA

- Di Mauro Officine Grafiche SpA

- Bak Ambalaj Sanayi ve Ticaret AS

- Flextrus AB

- Sipospack Kft.

- Clondalkin Flexible Packaging

- Innovia Films Ltd.

- AR Packaging Group AB

- RKW Group

- Plastopil Hazorea Co. Ltd.

- Schur Flexibles Group

- Glenroy Inc.

- Leefung ASG Europe

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Demand for Recyclable Mono-Material Films Driven by EU Circular Economy Targets

- 4.2.2 Accelerated Growth of E-Commerce Elevating Demand for Flexible Mailer & Protective Formats in Europe

- 4.2.3 Consumer Shift Toward Convenience & Portion-Control Products Boosting Flexible Pouch Adoption

- 4.2.4 Technological Advances in High-Barrier Co-Extrusion Enhancing Shelf-Life for Ready Meals

- 4.2.5 Rising Penetration of Digital & Hybrid Printing Enabling Short Runs and Mass Personalisation

- 4.2.6 Rapid Expansion of European Pet-Food Industry Using Retort & Stand-Up Pouches

- 4.3 Market Restraints

- 4.3.1 Stringent EU Plastics & Packaging-Waste Regulations Increasing Compliance Costs

- 4.3.2 Limited Recycling Infrastructure for Multi-Layer Films Hampering Circularity Goals

- 4.3.3 Volatile Polyolefin & Aluminium-Foil Prices Post-Energy Crisis Impacting Margins

- 4.3.4 Competitive Pressure from Rigid Recyclable Alternatives Among Sustainability-Minded Brands

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Investment Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Bi-orientated Polypropylene (BOPP)

- 5.1.1.3 Cast Polypropylene (CPP)

- 5.1.1.4 Polyethylene Terephthalate (PET)

- 5.1.1.5 Polystyrene (PS) and Expanded Polystyrene (EPS)

- 5.1.1.6 Other Plastics Types

- 5.1.2 Paper and Paperboard

- 5.1.3 Metal

- 5.1.4 Biodegradable and Compostable Materials

- 5.1.1 Plastics

- 5.2 By Product Type

- 5.2.1 Pouches

- 5.2.2 Bags

- 5.2.3 Films and Wraps

- 5.2.4 Other Product Type

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Industrial

- 5.3.6 Other End-Use Industries

- 5.4 By Distribution

- 5.4.1 Direct Sales

- 5.4.2 Indirect Sales

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Mondi Group

- 6.4.3 Huhtamaki Oyj

- 6.4.4 Constantia Flexibles GmbH

- 6.4.5 Sealed Air Corporation

- 6.4.6 Coveris Management GmbH

- 6.4.7 ProAmpac LLC

- 6.4.8 Novolex Holdings Inc.

- 6.4.9 Sonoco Products Company

- 6.4.10 Bischof + Klein SE & Co. KG

- 6.4.11 Wipak Oy

- 6.4.12 Schur International A/S

- 6.4.13 Gualapack SpA

- 6.4.14 ePac Holdings LLC

- 6.4.15 Danaflex Group

- 6.4.16 Cellografica Gerosa SpA

- 6.4.17 Di Mauro Officine Grafiche SpA

- 6.4.18 Bak Ambalaj Sanayi ve Ticaret AS

- 6.4.19 Flextrus AB

- 6.4.20 Sipospack Kft.

- 6.4.21 Clondalkin Flexible Packaging

- 6.4.22 Innovia Films Ltd.

- 6.4.23 AR Packaging Group AB

- 6.4.24 RKW Group

- 6.4.25 Plastopil Hazorea Co. Ltd.

- 6.4.26 Schur Flexibles Group

- 6.4.27 Glenroy Inc.

- 6.4.28 Leefung ASG Europe

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

軟性包裝市場:按材料、包裝形式、技術、結構、最終用戶和分銷管道分類-2026-2032年全球市場預測軟性工業包裝市場:按材料、產品類型、包裝形式、最終用途和分銷管道分類-2026-2032年全球市場預測

軟性包裝市場:按材料、包裝形式、技術、結構、最終用戶和分銷管道分類-2026-2032年全球市場預測軟性工業包裝市場:按材料、產品類型、包裝形式、最終用途和分銷管道分類-2026-2032年全球市場預測 軟包裝市場規模、佔有率、趨勢和預測:按產品類型、原料、印刷技術、應用和地區分類,2026-2034年非食品麥芽酚市場依用途、等級和形態分類,全球預測(2026-2032年)

軟包裝市場規模、佔有率、趨勢和預測:按產品類型、原料、印刷技術、應用和地區分類,2026-2034年非食品麥芽酚市場依用途、等級和形態分類,全球預測(2026-2032年) 軟性膠合板市場規模、佔有率和成長分析:按膠合板類型、產品厚度、等級、最終用戶產業和地區分類-2026-2033年產業預測

軟性膠合板市場規模、佔有率和成長分析:按膠合板類型、產品厚度、等級、最終用戶產業和地區分類-2026-2033年產業預測 軟性包裝市場分析及預測(至2035年):依類型、產品類型、材料類型、應用、技術、組件、最終用戶、功能及製程分類

軟性包裝市場分析及預測(至2035年):依類型、產品類型、材料類型、應用、技術、組件、最終用戶、功能及製程分類 亞太地區軟質包裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區軟質包裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 全球軟包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)軟包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年

全球軟包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)軟包裝市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年 2026年全球真空袋市場報告

2026年全球真空袋市場報告