|

市場調查報告書

商品編碼

1907006

軟包裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

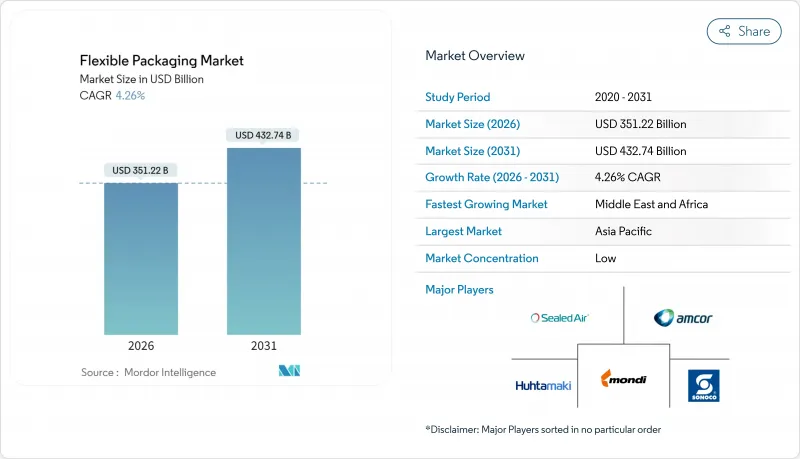

預計軟性包裝市場將從 2025 年的 3,368.7 億美元成長到 2026 年的 3,512.2 億美元,到 2031 年將達到 4,327.4 億美元,2026 年至 2031 年的複合年成長率為 4.26%。

對永續性的需求、電子商務的快速發展以及品牌對輕質阻隔性包裝的需求,都為軟包裝產業帶來了新的機會。材料科學的進步,特別是單組分結構的創新,正在減輕掩埋的壓力,並為加工商開闢新的循環收入來源。數位印刷縮短了小眾產品的上市週期,而準時制工作流程則緩解了聚烯價格波動所帶來的收入波動。從區域來看,亞太地區不斷壯大的中產階級和日益成長的製造業規模鞏固了其主導地位,而中東和非洲包裝基礎設施的快速發展則推動了該地區的追趕式成長。

全球軟包裝市場趨勢與洞察

電子商務對輕便防護郵袋的需求快速成長

預計到2024年,北美線上銷售額將成長15.4%,這將推動零售商採用軟性氣泡信封,這種信封可降低高達30%的體積重量費用。亞馬遜在印度減少了9100噸塑膠的使用,並擴大採用再生紙泡沫袋,這表明企業減少碳排放的承諾正在引導其採購轉向纖維薄膜混合產品。加工商的訂單現在優先考慮使用高再生塑膠含量薄膜製成的郵袋,這些薄膜可以與生活垃圾一起收集,美國和墨西哥的產能擴張正在進行中。由於歐洲更嚴格的尺寸限制法規,需求也在成長,亞洲的小包裹網路也採用類似的經濟高效的包裝形式。這種協同效應正在推動對聚乙烯塗層信封的需求持續成長,並將軟性包裝產業推向傳統快速消費品應用之外的領域。

亞洲快速消費品品牌正轉型使用單一材料可回收薄膜

印度2025年塑膠廢棄物管理規則要求品牌所有者證明其包裝材料的量化回收性能,迫使大型食品和口腔清潔用品公司從多層複合材料轉向單一材料聚烯薄膜。例如,Wipf AG的PP基WICOFILM等解決方案可以無縫整合到現有的回收流程中,同時保持氧氣和香氣阻隔性。東協個人護理品牌也在進行類似的轉變,利用單一材料包裝袋來滿足零售商的回收計劃並保持商店吸引力。供應側創新正在亞太地區全部區域,幫助該地區維持45.24%的軟包裝市場佔有率。隨著大多數生產者延伸責任(EPR)成本逐年上漲,擴大單一材料產能的加工商更有利於獲得利潤豐厚的合約並穩定利潤率。

聚烯價格波動擠壓加工商利潤空間

預計2024年原料價格波動將達到兩位數,這將對加工商的息稅折舊攤銷前利潤(EBITDA)構成壓力,因為其與季度價格合約掛鉤。亞洲地區聚乙烯(PE)和聚丙烯(PP)供應過剩以及運輸中斷加劇了價格波動。為了緩解對利潤率的影響,主要加工商正透過採用更薄的薄膜、實現庫存計劃數位化以及探索生質能基石腦油合約等方式分散風險。雖然這些控制措施是暫時的,但它們正在加速價格穩定並向更高再生材料轉型,從而間接推動軟包裝產業供應鏈的現代化。

細分市場分析

到2025年,聚乙烯將佔軟包裝產業的34.12%,其低成本和良好的防潮性能將繼續支撐其在食品包裝領域的核心應用。聚乙烯樹脂的易得性和成熟的回收系統將使其繼續保持作為穀物內襯、冷凍食品薄膜和清潔劑包裝袋標準材料的地位。然而,隨著零售商推出可家庭堆肥的自有品牌產品,以及市政當局擴大有機廢棄物處理項目,可生物分解和可堆肥聚合物將在2026年至2031年間以7.65%的複合年成長率(CAGR)實現最快成長。這一成長動能正推動研發預算重新分配到基於PLA(聚乳酸)和PHA(聚羥基烷酯)的共擠出技術上,這些技術強度與LDPE相當,但可在工業堆肥循環中分解。紙質複合材料將在需要中等水蒸氣滲透性的領域重新流行,而鋁箔將在需要近乎零氧氣滲透性的特定領域繼續發揮作用。 EVOH雖然目前僅以微層形式使用,但對於無菌培養基和營養補充凝膠仍然至關重要。整體而言,材料組合正朝著既能減少範圍3排放又不影響加工性能的解決方案轉變,進而推動軟包裝市場轉型為循環經濟。

受日常消費品(FMCG)脫碳藍圖和掩埋轉移成本的推動,可生物分解軟包裝市場預計將從2026年的336億美元成長到2031年的486億美元。儘管聚乙烯目前仍是使用量最大的材料,但隨著消費品類別中最低再生材料含量標準的製定,其主導地位預計將逐漸下降。雙向拉伸聚丙烯(BOPP)的透明度和剛性使其在休閒食品領域保持領先地位,而聚對苯二甲酸乙二醇酯(CPP)的熱封可靠性則確保了其在蒸餾和扭結包裝中的應用。樹脂生產商正在加大對化學回收技術的投資,以回收聚丙烯(PP)和聚乙烯(PE)單體,從而實現真正的聚合物到聚合物循環,以保持材料性能。隨著這些努力的擴展,加工商預計將開發出機械、化學和生物分解回收路線的組合方案,每種方案都旨在滿足軟包裝行業不同管道的需求。

到2025年,軟包裝袋將佔總收入的46.05%,其優勢在於能夠以輕70%的形式取代玻璃瓶和易拉罐,並減少運輸排放。立式袋擴大了廣告空間,並促進了調味品和寵物食品的衝動性購買。高解析度噴墨印刷機的出現顯著減少了生產過程中的廢棄物,從而能夠擴展季節性口味的SKU,支援D2C品牌和自有品牌的重新上市。儘管薄膜和包裝紙的貨架佔有率較低,但隨著商店的降低而又不犧牲抗穿刺性,其複合年成長率將達到5.61%,成為成長最快的包裝形式。奈米黏土和二氧化矽阻隔塗層正在取代鋁層,從而提高了分類和回收率。

同時,受化肥、水泥和寵物食品等產業需求的支撐,袋裝軟包裝市場規模將保持穩定。小袋和條狀包裝將繼續滲透到單份營養補充劑和即溶飲料市場,尤其是在東南亞地區,該地區的即食消費正在成長。未來五年,數位印刷速度、無溶劑運作和電子束固化技術的協同作用預計將把前置作業時間從數週縮短至數天。這將迫使加工商重新思考其工廠佈局。最終,他們需要一種能夠實現靈活營運的產品組合,能夠在大規模餐飲服務生產和麵向網紅合作的小批量生產之間靈活切換。

這份軟包裝市場報告按材料類型(塑膠、紙張、鋁箔、可生物分解材料)、產品類型(包裝袋、薄膜及其他)、終端用戶行業(食品、飲料、醫藥、化妝品、工業及其他)、分銷管道(直銷、間接)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

區域分析

到2025年,亞太地區將繼續維持其在軟包裝產業44.70%的主導地位,這主要得益於都市化、可支配收入的成長以及製造業扶持政策。中國的智慧工廠投資和印度針對食品加工的生產關聯激勵(PLI)計畫正在推動國內樹脂和薄膜產能的提升。 UFlex公司將其聚酯切片產量加倍,並運作了一家消費後聚合酶鍊式反應(PCR)工廠,從而強化了其循環供應提案。區域加工商也主導推廣單一材料產品,以因應即將到來的生產者延伸責任制(EPR)所帶來的成本增加,進一步鞏固了該地區的成長動能。同時,東南亞國家正利用免稅貿易叢集擴大立式袋出口,活性化區域內貿易流動。

北美是第二個關鍵樞紐,這主要得益於電子商務信封的日益普及和醫藥低溫運輸的成長。零售商正在推動How2Recycle認證包裝袋的普及,並提高PE薄膜的可回收性。原始設備製造商(OEM)透過整合數位化檢測和確保符合FDA標準的可追溯性來加強市場誠信。歐洲正將歐盟塑膠廢棄物指令(PPWR)作為核心策略,投資建造化學回收試點工廠和纖維基軟性包裝。 Mondi和Huhtamäki分別擴大了其可回收蒸餾線和Blue Loop產品組合,以大規模可回收設計原則。

預計到2031年,中東和非洲地區將以6.03%的複合年成長率實現最高成長,這主要得益於沙烏地阿拉伯和埃及在外國直接投資(FDI)支持下建立的食品中心。非洲包裝市場預計到2031年將達到560.2億美元,其中軟包裝市場到2033年預計將超過33.8億美元。現代零售連鎖店對在乾旱氣候下保存期限長的包裝袋的需求,推動了高阻隔薄膜的進口。南美洲專門食品咖啡的蓬勃發展提振了對真空閥包裝袋的需求,而匯率波動則使得通用軟包裝比硬質玻璃和金屬包裝更具吸引力。在各個地區,監管主導的回收目標正在統一加工商的研發工作,並推動單一材料藍圖的發展。

其他福利:

- Excel格式的市場預測(ME)表

- 分析師支持(3個月)

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 北美電商對輕便防護郵袋的需求激增

- 亞洲快速消費品品牌紛紛轉向使用單一材料可回收薄膜,以滿足生產者責任延伸制度的要求。

- 歐洲即食食品領域中,殺菌袋迅速普及。

- 南美的咖啡和特產飲料品牌正在轉向使用高阻隔薄膜

- 投資數位印刷技術,實現化妝品包裝的大規模客製化

- 低溫運輸生技藥品泡殼需求成長推動了藥品軟包裝的發展

- 市場限制

- 聚烯價格波動擠壓加工商利潤空間

- 歐盟和美國多層複合材料回收基礎設施分散

- 加強主要新興經濟體(如印度、肯亞)對一次性塑膠製品的監管

- 在中東地區,硬質寶特瓶阻礙了立式袋在碳酸飲料領域的應用。

- 供應鏈分析

- 監理展望

- 技術展望

- 貿易場景(依相關HS編碼)

- 波特五力分析

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 回收和永續性趨勢

第5章 市場規模與成長預測

- 依材料類型

- 塑膠

- 聚乙烯(PE)

- 雙軸延伸聚丙烯(BOPP)

- 澆鑄聚丙烯(CPP)

- 聚氯乙烯(PVC)

- 乙烯-乙烯醇共聚物(EVOH)

- 其他軟質塑膠

- 紙

- 鋁箔

- 可生物分解和可堆肥材料

- 塑膠

- 依產品類型

- 小袋

- 袋子和麻袋

- 薄膜和包裝

- 其他產品類型

- 按最終用途行業分類

- 食物

- 冷凍食品

- 乳製品

- 肉類和魚貝類

- 烘焙點心和糖果甜點

- 生鮮食品

- 其他食品

- 飲料

- 果汁和花蜜

- 乳製品飲料

- 其他飲料

- 製藥

- 化妝品和個人護理

- 產業

- 其他終端用戶產業

- 食物

- 透過分銷管道

- 銷售管道

- 間接銷售管道

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 亞太地區

- 中國

- 日本

- 印度

- ASEAN

- 韓國

- 澳洲

- 紐西蘭

- 南美洲

- 巴西

- 阿根廷

- 智利

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東地區

- 非洲

- 南非

- 肯亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Amcor plc

- Sealed Air Corporation

- Mondi plc

- Huhtamaki Oyj

- Constantia Flexibles Group GmbH

- Sonoco Products Company

- ProAmpac LLC

- Coveris Management GmbH

- Uflex Ltd.

- Sigma Plastics Group

- Schur Flexibles Holding

- Wipf AG

- Glenroy Inc.

- Printpack Inc.

- Clondalkin Flexible Packaging

- American Packaging Corporation

- FlexPak Services LLC

- Arabian Flexible Packaging LLC

- Gulf East Paper & Plastic Industries LLC

- Plastipak Packaging Inc.

第7章 市場機會與未來展望

The Flexible Packaging market is expected to grow from USD 336.87 billion in 2025 to USD 351.22 billion in 2026 and is forecast to reach USD 432.74 billion by 2031 at 4.26% CAGR over 2026-2031.

Rising sustainability mandates, rapid e-commerce expansion, and brand demand for lightweight, high-barrier formats are widening the flexible packaging industry opportunity. Material science breakthroughs, particularly in mono-material structures, are reducing landfill pressure and unlocking new circular revenue streams for converters. Digital printing is compressing launch cycles for niche products, while just-in-time workflows mitigate the earnings volatility caused by polyolefin price swings. Regionally, Asia Pacific's expanding middle class and manufacturing scale underpin its leadership, whereas the Middle East and Africa's packaging infrastructure boom is accelerating its catch-up growth.

Global Flexible Packaging Market Trends and Insights

Surge in e-commerce demand for lightweight protective mailers

North American online sales expanded by 15.4% in 2024, pushing retailers to adopt flexible bubble mailers that cut dimensional-weight fees up to 30%. Amazon's removal of 9,100 metric tons of plastic in India and its wider rollout of recyclable paper padded bags illustrate how corporate carbon pledges are steering procurement toward fiber-and-film hybridsConverter order books now favor curbside-recyclable mailers with high recycled-content films, spawning capacity additions across the United States and Mexico. Volumes are also spilling into Europe as right-sizing mandates tighten, while Asian parcel networks replicate these cost-efficient formats. The net effect is a sustained uplift in poly-coated mailer demand that lifts the flexible packaging industry beyond traditional FMCG end uses.

Shift of Asian FMCG brands toward mono-material recyclable films

India's Plastic Waste Management Rules in FY 2025 require brand owners to demonstrate quantifiable recycling of their packaging footprints, compelling leading food and oral-care players to replace multilayer laminates with polyolefin-only films. Solutions such as PP-based WICOFILM from Wipf AG preserve oxygen and aroma barriers yet flow seamlessly through existing recycling streams. ASEAN personal-care brands echo this switch, leveraging mono-material pouches to secure shelf appeal while satisfying retailer take-back schemes. Supply-side innovation is spreading across Asia Pacific, helping the region reinforce its 45.24% hold on the flexible packaging industry. With most EPR fees escalating annually, converters that scale mono-material capacity are positioned to secure premium contracts and margin resilience.

Volatile polyolefin prices squeezing converter margins

Feedstock volatility reached double-digit spreads in 2024, eroding EBITDA for converters locked into quarterly price agreements. Asian PE and PP oversupply and shipping disruptions amplify the swings. To blunt margin shocks, leading converters deploy thinner gauge films, digitalize inventory planning, and explore biomass-based naphtha contracts to diversify risk exposure. This restraint remains transitory yet accelerates the shift toward materials that provide price stability and recycled content, indirectly modernizing the flexible packaging industry supply base.

Other drivers and restraints analyzed in the detailed report include:

- Rapid adoption of retort pouches for ready-to-eat meals

- Coffee and specialty-drink brands' switch to high-barrier films

- Fragmented recycling infrastructure for multilayer laminates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene underpinned 34.12% of flexible packaging industry share in 2025, leveraging its low cost and moisture barrier attributes to anchor core food applications. Its wide resin availability and established recycling streams keep it the default choice for cereal liners, frozen food films, and detergent pouches. However, biodegradable and compostable polymers exhibit the fastest 7.65% CAGR from 2026-2031 as retailers introduce home-compostable private-label lines and municipalities upgrade organic waste programs. This momentum realigns R&D budgets toward PLA- and PHA-based coextrusions that mimic LDPE toughness yet break down within industrial composting cycles. Paper laminates also resurge where water vapor requirements are moderate, while aluminum foil defends niche roles that demand near-zero oxygen transmission. EVOH, albeit used in microlayer form, remains critical for aseptic broths and nutraceutical gels. Collectively, the material portfolio is pivoting toward solutions that reduce Scope 3 emissions without forfeiting machinability, reinforcing the flexible packaging market's pivot to circularity.

The flexible packaging industry size for biodegradable materials is projected to climb from USD 33.6 billion in 2026 to USD 48.6 billion in 2031, fueled by FMCG decarbonization roadmaps and landfill diversion fees. Polyethylene still commands the volume crown, yet its dominance is expected to edge down as consumer-facing categories impose minimum recycled-content thresholds. BOPP's clarity and stiffness uphold its presence in snack foods, while CPP's heat-seal reliability ensures its inclusion in retort and twist-wrap packs. Resin makers are investing in chemical recycling to recapture PP and PE monomers, enabling true polymer-to-polymer loops that preserve material performance. As these initiatives scale, converters foresee a blended portfolio where mechanical, chemical, and bio-degradation pathways coexist, each serving distinct channel needs within the flexible packaging industry.

Pouches generated 46.05% of 2025 revenue, spotlighting their ability to replace glass jars and tins with 70% lighter formats that lower freight emissions. Stand-up pouches enhance billboard space, driving impulse purchases in condiments and pet food. The advent of high-definition inkjet presses slashes make-ready waste and enables SKU proliferation for seasonal flavors, supporting D2C brands and private-label refreshes. Films and wraps, while less visible on shelf, register the sharpest 5.61% CAGR by trimming gauge thicknesses without sacrificing puncture resistance. Nanoclay and silicon oxide barrier coatings now substitute aluminum layers, improving sortability and stream recyclability.

Meanwhile, the flexible packaging industry size for bags and sacks holds steady, buoyed by fertilizer, cement, and dog-food demand. Sachets and stick packs continue to penetrate single-serve nutraceuticals and instant beverages, particularly in Southeast Asia where on-the-go consumption is rising. Over the next five years the interplay between digital press uptime, solvent-less lamination, and e-beam curing is expected to compress lead times from weeks to days, pushing converters to rethink plant layouts. The end result is a product mix that rewards agile operations able to toggle between long food-service runs and micro batches for influencer collaborations.

The Flexible Packaging Market Report is Segmented by Material Type (Plastic, Paper, Aluminum Foil, Biodegradable Materials), Product Type (Pouches, Bags, Films, Others), End-Use Industry (Food, Beverage, Pharmaceutical, Cosmetics, Industrial, Others), Distribution Channels (Direct, Indirect), and Geography (North America, Europe, Asia Pacific, South America, MEA). Market Forecasts are in Value (USD).

Geography Analysis

Asia Pacific retained a commanding 44.70% share of the flexible packaging industry in 2025 due to urbanization, rising disposable incomes, and pro-manufacturing policies. China's smart-factory investments and India's Production Linked Incentive scheme for food processing underpin domestic resin and film capacity. UFlex doubled polyester chip output and commissioned a PCR plant to integrate post-consumer feedstock, fortifying a circular supply proposition. Local converters also spearhead mono-material rollouts to comply with forthcoming EPR fees, reinforcing the region's trajectory. Meanwhile, Southeast Asian nations leverage duty-free trade clusters to export stand-up pouches, lifting intraregional trade flows.

North America is the second-largest node, propelled by e-commerce mailer adoption and pharmaceutical cold-chain growth. Retailers press for How2Recycle-certified pouches, prompting PE film recyclability upgrades. OEMs integrate digital inspection to guarantee FDA-grade traceability, reinforcing market integrity. Europe anchors its strategy around the EU PPWR, channeling funds into chemical-recycling pilot plants and fiber-based flexibles. Mondi and Huhtamaki expand recyclable retort lines and blueloop portfolios, respectively, embedding design-for-recycling principles at scale.

The Middle East & Africa is forecast to post the fastest 6.03% CAGR to 2031, aided by FDI-backed food hubs in Saudi Arabia and Egypt. Africa's packaging sector is on course to hit USD 56.02 billion by 2031, of which flexible formats could surpass USD 3.38 billion by 2033. Modern retail chains require extended-shelf-life pouches for arid climates, stimulating imports of high-barrier films. South America's specialty coffee boom strengthens demand for degassing valve pouches, while currency volatility makes the lighter flexible packaging industry more attractive than rigid glass or metal. Across regions, a common thread is regulatory-driven recycling targets that unify converter R&D roadmaps toward mono-materials.

- Amcor plc

- Sealed Air Corporation

- Mondi plc

- Huhtamaki Oyj

- Constantia Flexibles Group GmbH

- Sonoco Products Company

- ProAmpac LLC

- Coveris Management GmbH

- Uflex Ltd.

- Sigma Plastics Group

- Schur Flexibles Holding

- Wipf AG

- Glenroy Inc.

- Printpack Inc.

- Clondalkin Flexible Packaging

- American Packaging Corporation

- FlexPak Services LLC

- Arabian Flexible Packaging LLC

- Gulf East Paper & Plastic Industries LLC

- Plastipak Packaging Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in e-commerce demand for lightweight protective mailers in North America

- 4.2.2 Shift of Asian FMCG brands toward mono-material recyclable films to meet EPR mandates

- 4.2.3 Rapid adoption of retort pouches for ready-to-eat meals in Europe

- 4.2.4 Coffee and specialty-drink brands' switch to high-barrier films in South America

- 4.2.5 Investments in digital printing enabling mass customization for cosmetics packs

- 4.2.6 Growth in cold-chain biologics blister demand boosting pharma flexible packaging

- 4.3 Market Restraints

- 4.3.1 Volatile polyolefin prices squeezing converter margins

- 4.3.2 Fragmented recycling infrastructure for multilayer laminates in EU and US

- 4.3.3 Stricter single-use plastic bans in key emerging economies (e.g., India, Kenya)

- 4.3.4 Rigid PET bottles limiting stand-up pouch penetration in Middle-East CSD segment

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Trade Scenario (Under Relevant HS Code)

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Recycling and Sustainability Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Biaxially Oriented Polypropylene (BOPP)

- 5.1.1.3 Cast Polypropylene (CPP)

- 5.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.1.5 Ethylene-Vinyl Alcohol (EVOH)

- 5.1.1.6 Other Flexible Plastic

- 5.1.2 Paper

- 5.1.3 Aluminum Foil

- 5.1.4 Biodegradable and Compostable Materials

- 5.1.1 Plastic

- 5.2 By Product Type

- 5.2.1 Pouches

- 5.2.2 Bags and Sacks

- 5.2.3 Films and Wraps

- 5.2.4 Other Product Types

- 5.3 By End-use Industry

- 5.3.1 Food

- 5.3.1.1 Frozen Food

- 5.3.1.2 Dairy Based Products

- 5.3.1.3 Meat and Seafood

- 5.3.1.4 Baked Snacks and Confectionery

- 5.3.1.5 Fresh Produce

- 5.3.1.6 Other Food Products

- 5.3.2 Beverage

- 5.3.2.1 Juice and Nectare

- 5.3.2.2 Dairy Based Drinks

- 5.3.2.3 Other Beverages

- 5.3.3 Pharmaceutical

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Industrial

- 5.3.6 Other End -Use Industry

- 5.3.1 Food

- 5.4 By Distribution Channels

- 5.4.1 Direct Sales Channel

- 5.4.2 Indirect Sales Channel

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordics

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 ASEAN

- 5.5.3.5 South Korea

- 5.5.3.6 Australia

- 5.5.3.7 New Zealand

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Kenya

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Amcor plc

- 6.3.2 Sealed Air Corporation

- 6.3.3 Mondi plc

- 6.3.4 Huhtamaki Oyj

- 6.3.5 Constantia Flexibles Group GmbH

- 6.3.6 Sonoco Products Company

- 6.3.7 ProAmpac LLC

- 6.3.8 Coveris Management GmbH

- 6.3.9 Uflex Ltd.

- 6.3.10 Sigma Plastics Group

- 6.3.11 Schur Flexibles Holding

- 6.3.12 Wipf AG

- 6.3.13 Glenroy Inc.

- 6.3.14 Printpack Inc.

- 6.3.15 Clondalkin Flexible Packaging

- 6.3.16 American Packaging Corporation

- 6.3.17 FlexPak Services LLC

- 6.3.18 Arabian Flexible Packaging LLC

- 6.3.19 Gulf East Paper & Plastic Industries LLC

- 6.3.20 Plastipak Packaging Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

非食品麥芽酚市場依用途、等級和形態分類,全球預測(2026-2032年)

非食品麥芽酚市場依用途、等級和形態分類,全球預測(2026-2032年) 軟性膠合板市場規模、佔有率和成長分析:按膠合板類型、產品厚度、等級、最終用戶產業和地區分類-2026-2033年產業預測

軟性膠合板市場規模、佔有率和成長分析:按膠合板類型、產品厚度、等級、最終用戶產業和地區分類-2026-2033年產業預測 軟性包裝市場分析及預測(至2035年):依類型、產品類型、材料類型、應用、技術、組件、最終用戶、功能及製程分類

軟性包裝市場分析及預測(至2035年):依類型、產品類型、材料類型、應用、技術、組件、最終用戶、功能及製程分類 亞太地區軟質包裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區軟質包裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 全球軟包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球軟包裝市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球真空袋市場報告2026年全球軟包裝市場報告

2026年全球真空袋市場報告2026年全球軟包裝市場報告 金屬化軟質包裝市場規模、佔有率和趨勢分析報告:按產品、包裝類型、最終用途、地區和細分市場預測(2026-2033 年)

金屬化軟質包裝市場規模、佔有率和趨勢分析報告:按產品、包裝類型、最終用途、地區和細分市場預測(2026-2033 年) 軟性包裝紙市場:按紙張類型、應用、阻隔技術、塗裝類型和地區分類多層軟性包裝市場-2026-2031年預測

軟性包裝紙市場:按紙張類型、應用、阻隔技術、塗裝類型和地區分類多層軟性包裝市場-2026-2031年預測