|

市場調查報告書

商品編碼

1693417

歐洲聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Europe Polyurethane Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

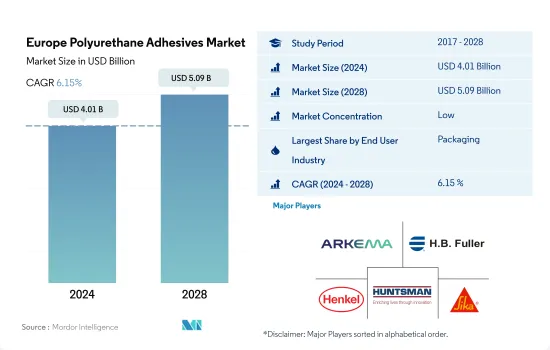

預計 2024 年歐洲聚氨酯接著劑市場規模為 40.1 億美元,到 2028 年將達到 50.9 億美元,預測期內(2024-2028 年)的複合年成長率為 6.15%。

新興建築和包裝終端用途產業預計將推動歐洲聚氨酯接著劑的消費

- 聚氨酯接著劑廣泛應用於包裝產業,包括食品和飲料包裝、容器包裝、功能阻隔應用的最終包裝以及金屬包裝。英國是全球最大的包裝市場之一。該國的設計改進和技術創新,加上轉向使用可回收材料進行包裝,預計將為市場成長提供大量機會,為市場上的新產品推出創造機會。英國包裝製造業的年營業額為110億英鎊,這可能會推動該地區的包裝黏合劑市場的發展。

- 2021年,建築業對聚氨酯膠粘劑的需求呈指數級成長,這得益於歐盟委員會在2020年聚氨酯接著劑導致的經濟放緩後訂定的復甦計劃,例如“下一代歐盟”計劃,該計劃向建築建設產業撥款,使歐洲建築更加綠色環保,減少資源浪費。 2021 年聚氨酯建築膠黏劑的整體需求成長在其他歐洲國家地區最高,因為丹麥等北歐國家的建築產量增加了 17.8%。

- 在歐洲,德國擁有最大的醫療保健產業。據估計,該國每年在醫療衛生方面的支出超過 3,750 億歐元(不包括健身和保健費用)。在人口變化數位化趨勢的推動下,醫療保健支出的持續成長預計將在預測期內推動該地區聚氨酯接著劑市場的發展。

歐洲建築、包裝和汽車產業的蓬勃發展可能會推動未來對聚氨酯接著劑的需求

- 2017年至2021年期間,歐洲地區產生的需求在所有地區中排名第二。由於汽車、航太、建築等終端用戶產業的製造能力強,該地區的黏合劑需求一直佔全球需求的 24-25%。採用熱熔和水溶性技術的聚氨酯接著劑滿足了該地區的大部分需求。

- 2017年至2019年期間,該地區對黏合劑的需求以1.85%的複合年成長率成長。聚氨酯接著劑需求成長放緩的原因是該地區建設活動成長放緩和汽車產量下降。在此期間,這些終端用戶產業的需求分別以 0.44% 和 -0.50% 的複合年成長率下降。

- 2020年,營運、勞動力、原料、供應鏈和其他領域的限制導致全部區域所有終端用戶的需求減少。在該地區所有國家的所有行業中,德國的製鞋業和法國的汽車業受到的打擊最為嚴重,與去年同期相比,出口量分別下降了37.89%和35.94%。

- 預計2021年該地區所有國家對聚氨酯接著劑的需求都將開始復甦,並在2022年超過疫情前的需求水準。義大利的銷量增幅最高,與前一年同期比較去年同期成長8.38%。預計這一成長趨勢將在預測期內持續下去。預計預測期內全部區域的需求將以 3.83% 的複合年成長率成長。

歐洲聚氨酯接著劑市場趨勢

歐洲食品飲料產業蓬勃發展,帶動包裝產業擴張

- 包裝是歐洲地區的關鍵產業之一。該地區是繼亞太地區之後全球第二大包裝產品生產地區,約佔全球包裝產量的24%。德國、俄羅斯、西班牙和英國是歐洲主要的包裝產品生產國。受新冠疫情影響,預計2020年包裝產量較2019年下降7.14%。今年,多個國家實施了全國封鎖,導致該地區的生產設施關閉了三到四個月。

- 俄羅斯是包裝產品主要生產國,2021年產量為2.138億噸,位居歐洲第一。近年來,俄羅斯包裝產業的發展很大程度上受到食品和飲料產業快速成長的推動。俄羅斯是全球主要食品出口國,進一步影響包裝銷售,以滿足一系列終端產業對複雜包裝的需求。

- 德國是歐洲領先的塑膠包裝生產國。 2021年塑膠包裝將佔包裝產量的約79%。塑膠包裝行業主要受到國內食品和飲料行業快速成長的推動。由於生活方式更加忙碌、消費能力增強及相關因素,該地區對快速和便攜包裝產品的需求正在增加。未來幾年,這一趨勢在歐洲包裝產品中將會成長。

新建築的激增和不斷成長的重建需求正在推動該行業的發展

- 受新冠疫情影響,2020年建設業整體收益大幅下降。

- 歐洲建築業的銷售額呈現驚人的成長勢頭,2021與前一年同期比較率與 2020 年相比最高。這得歸功於歐盟委員會的舉措和措施的成功,例如在名為「下一代歐盟」的新冠疫情復甦計劃下向所有行業注資 7500 億歐元。根據歐盟下一代計劃,建築業獲得了最大的投資,因為歐洲對建築的綠色化和數位化目標導致現有建築和結構的年度維修增加。

- 根據 EUROCONSTRUCT 報告,在基於歐盟政治區域的細分市場中,中歐和東歐預計將以 6.4% 的複合年成長率成長,其次是西歐,複合年成長率為 6.1%。

- 歐盟和國家層面的政策制定者正在透過各種政策(包括《建築能源性能指令》)優先考慮新建築和現有建築的能源效率。這些政策將在預測期內提高整體建築收益。

歐洲聚氨酯接著劑產業概況

歐洲聚氨酯接著劑市場分散,前五大公司佔25.72%的市佔率。該市場的主要企業有:阿科瑪集團、HB Fuller 公司、漢高股份公司、亨斯邁國際有限責任公司和西卡股份公司(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 包裝

- 木製品和配件

- 法律規範

- EU

- 俄羅斯

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木製品和配件

- 其他最終用戶產業

- 科技

- 熱熔膠

- 反應性

- 溶劑型

- 紫外線固化膠合劑

- 水

- 國家

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲國家

第6章 競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- 3M

- Arkema Group

- Beardow Adams

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Jowat SE

- MAPEI SpA

- Sika AG

- Soudal Holding NV

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、限制因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92476

The Europe Polyurethane Adhesives Market size is estimated at 4.01 billion USD in 2024, and is expected to reach 5.09 billion USD by 2028, growing at a CAGR of 6.15% during the forecast period (2024-2028).

Emerging construction and packaging end-use sector expected to boost the consumption of polyurethane adhesives in Europe

- Polyurethane adhesives are widely used in the packaging industry for food and beverage packaging, container packaging, end-of-line packaging for functional barrier applications, and metal packaging. The United Kingdom is one of the largest packaging markets in the country. The country's designed improvements and innovation, combined with a shifting focus toward the usage of recyclable materials for packaging, are expected to offer numerous opportunities for market growth, thus, creating opportunities for the launch of new products into the market. The UK packaging manufacturing industry records annual sales of GBP 11 billion, which is likely to drive the market for packaging adhesives in the region.

- The demand for polyurethane adhesives in the construction industry grew tremendously in 2021 because of the European Union's Commission's recovery plan post an economic slowdown due to the COVID-19 pandemic in 2020, such as Next Generation EU in which a fund has been allocated for the construction sector to make European buildings environmentally benign and reduce the wastage of resources. The overall growth in demand for polyurethane construction adhesives was the highest in 2021 for the Rest of Europe regional segment because of the Nordic countries, such as Denmark, which witnessed a 17.8% growth in their construction output.

- In Europe, Germany accounts for the largest healthcare industry. The annual expenditure on health in the country is estimated to be more than EUR 375 billion, excluding fitness and wellness. Owing to its demographic changes and digitalization trends, healthcare expenditure is expected to continue rising and drive the polyurethane adhesives market in the region over the forecast period.

Rising construction, packaging and automotive industries in Europe likely to propel the demand for polyurethane adhesives in the future

- In the period 2017 to 2021, the demand generated from the Europe region ranked 2rd among all regions. The share of adhesive demand from this region has consistently occupied 24-25% of the global demand because of the high manufacturing capacity of end-user industries, like automotive, aerospace, building and construction, and other industries in the region. Polyurethane adhesives with hot melt and water-borne technologies generate most of the demand in the region.

- From 2017 to 2019, the demand for adhesives from this region increased with a CAGR of 1.85%. The slow growth in the demand for polyurethane adhesives has resulted in slow growth in construction activities and a decrease in Automotive production in the region. The demand from these end-user industries declined with a CAGR of 0.44% and -0.50%, respectively, during this period.

- In 2020, due to constraints in operations, labor, raw material, supply chain, and other areas, the demand from all end users across the region declined. Among all Industries from all countries in the region, the footwear industry in Germany and the automotive industry in France took the worst hit, declining by 37.89% and 35.94%, respectively, in Y-o-Y volume terms.

- In 2021, the demand for polyurethane adhesives started to recover from all countries in the region and is expected to outgrow pre-pandemic demand volume by 2022. The demand from Italy has witnessed the highest Y-o-Y growth of 8.38% in volume terms. This growth trend is expected to continue during the forecast period. The overall demand from the Europe region is expected to increase with a CAGR of 3.83% during the forecast period.

Europe Polyurethane Adhesives Market Trends

Significant growth of food & beverage industry in Europe to escalate packaging industry

- Packaging is one of the major sectors of Europe region. The region is the second-largest producer of packaging products in the world, which holds about 24% of global packaging production after the Asia-Pacific region. Germany, Russia, Spain, and the United Kingdom are major producers of packaging products in Europe. It is seen that packaging production reduced by 7.14% in 2020 compared to 2019 due to the impact of the COVID-19 pandemic. During the year, a nationwide lockdown imposed by several countries halted the production facilities for three to four months in the region.

- Russia is a leading producer of packaging products producing 213.8 million tons in 2021, which is the highest in Europe. The Russian packaging industry has majorly been driven by the rapid growth of the food and beverages industry in recent years. Russia is a major exporter of food products worldwide, which further influences packaging sales to meet the need for sophisticated packaging across various-end use industries.

- Germany is the major producer of plastic packaging in Europe. Plastic packaging which nearly accounts for around 79% of the packaging produced in 2021. The plastic packaging industry is majorly driven by the rapid growth of the food and beverages industry in the country. With the rise in busier lifestyles, greater spending power, and related factors in the region, the demand for quick and on-the-go packaged products is increasing. This trend will rise in packaging products in the coming years in Europe.

Rapid growth of new construction along with rising need for renovation activities will drive the industry

- The overall revenue of construction showed a steep decrement in 2020 because of the impact of the pandemic situation due to COVID-19, which led to an overall recovery slowdown and social distancing measures on work sites.

- The overall revenue of the construction sector in Europe grew tremendously, with the highest year-on-year growth in 2021 compared to that of 2020 because of the initiatives and measures taken by the EU Commission, such as the infusion of EUR 750 billion for all sectors under the COVID recovery plan named Next Generation EU. Under the Next Generation EU plan, the construction sector received the maximum investment because of the European objective of green and digital transition in buildings which led to growth in the annual renovation rate of existing buildings and structures.

- As per the EUROCONSTRUCT report, among the segments of the European Union based on political geography, Central and Eastern Europe are expected to register a CAGR of 6.4%, followed by Western Europe at a CAGR of 6.1% in 2022-2024.

- The policymakers at European Union and national level are prioritizing the construction of new buildings and conversion of existing buildings to be energy efficient through various policies including Energy Performance of Buildings Directive and others. These policies will lead to an increase in overall revenue for construction in the forecast period.

Europe Polyurethane Adhesives Industry Overview

The Europe Polyurethane Adhesives Market is fragmented, with the top five companies occupying 25.72%. The major players in this market are Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 EU

- 4.2.2 Russia

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Country

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Beardow Adams

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Huntsman International LLC

- 6.4.7 Jowat SE

- 6.4.8 MAPEI S.p.A.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

聚氨酯黏合劑市場:按類型、固化機制、終端用戶產業、應用和分銷管道分類-2026-2032年全球市場預測

聚氨酯黏合劑市場:按類型、固化機制、終端用戶產業、應用和分銷管道分類-2026-2032年全球市場預測 全球聚氨酯接著劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚氨酯接著劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球聚氨酯接著劑市場報告

2026年全球聚氨酯接著劑市場報告 電子產業用聚氨酯(PU)黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

電子產業用聚氨酯(PU)黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球聚氨酯接著劑市場(按類型、技術、應用和地區分類)- 預測至 2030 年

全球聚氨酯接著劑市場(按類型、技術、應用和地區分類)- 預測至 2030 年 聚氨酯接著劑的全球市場:類別,各技術,各終端用戶業界,各地區,機會,預測,2018年~2032年亞太聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)中東和非洲聚氨酯(PU)黏合劑市場佔有率分析、產業趨勢和成長預測(2025-2030)聚氨酯接著劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

聚氨酯接著劑的全球市場:類別,各技術,各終端用戶業界,各地區,機會,預測,2018年~2032年亞太聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)中東和非洲聚氨酯(PU)黏合劑市場佔有率分析、產業趨勢和成長預測(2025-2030)聚氨酯接著劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

▼