|

市場調查報告書

商品編碼

1692574

聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)Polyurethane Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

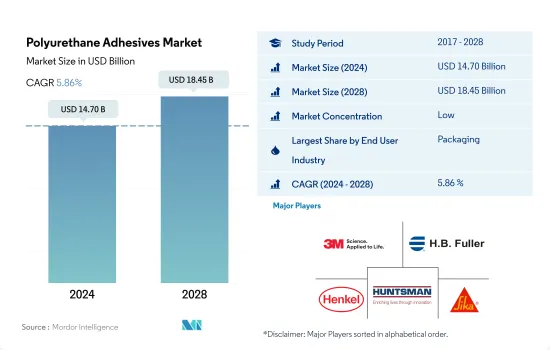

聚氨酯接著劑市場規模預計在 2024 年為 147 億美元,預計到 2028 年將達到 184.5 億美元,預測期內(2024-2028 年)的複合年成長率為 5.86%。

建築和包裝終端使用行業的成長預計將推動全球聚氨酯接著劑消費的成長

- 聚氨酯接著劑廣泛應用於包裝產業。聚氨酯接著劑用於食品和飲料包裝、容器包裝、功能性阻隔應用的生產線末端包裝以及金屬包裝。此外,根據包裝和加工技術協會發布的一份報告,受人口成長、對永續性的日益關注、發展中地區消費能力的提高以及對智慧包裝的需求不斷成長等因素推動,全球包裝行業規模預計將從 2016 年的 368 億美元成長至 2021 年的 422 億美元。

- 同樣,建築和施工領域在全球聚氨酯接著劑市場中佔有第二大佔有率。聚氨酯接著劑具有良好的內聚力、附著力、彈性、高黏結強度、柔韌性和基材的高彈性模量。根據聯合國的數據,全球約有 50% 的人口居住在都市區,預計到 2030 年將達到 60%。經濟和人口成長的速度必須與商業、住宅和機構建設的需求相符。到 2030 年,全球約 40% 的人口可能需要住宅,平均每天需要超過 96,150 套住房。因此,未來幾年建設活動的增加可能會推動聚氨酯接著劑市場的發展。

- 聚氨酯接著劑廣泛應用於電子、電氣設備的製造。預計全球整體電子和家用電器行業的複合年成長率將分別達到 2.51% 和 5.77%,從而導致預測期內(2022-2028 年)對聚氨酯接著劑的需求增加。

北美、歐洲和亞太地區投資和重建資金的增加預計將推動聚氨酯接著劑在全球各個終端用途領域的使用

- 由於存在大量建築和包裝活動、汽車、醫療設備、航太工業和其他成熟的終端用戶行業的生產能力,亞太地區在整個研究期間佔據了聚氨酯接著劑需求的最大佔有率。中國是全球最大的建築和汽車市場,滿足了亞太地區高達58%的需求。

- 2017年至2019年,聚氨酯接著劑的需求一直低迷。這是由於歐洲和亞太地區的成長放緩。全球主要終端用戶產業建築業和汽車業的需求下降限制了聚氨酯接著劑需求的整體成長。在此期間,這些產業的需求分別以-0.05%和-1.79%的複合年成長率下降。

- 2020年,新冠疫情導致所有終端用戶產業對聚氨酯接著劑的需求下降。在南非和巴西等一些國家,建設活動被視為必不可少的,並允許在疫情期間進行。這些因素減輕了全球影響,將2020年的降幅限制在8.96%。

- 由於美國、澳洲、歐盟國家等的紓困措施和支持計劃,需求將在 2021 年開始復甦,預計這一成長趨勢將在整個預測期內持續下去。預計歐洲、南美和亞太地區的投資和預算分配增加將成為這一成長的主要驅動力。

全球聚氨酯接著劑市場趨勢

開發中國家電子商務產業的快速成長增強了該產業

- 2020 年伊始,包裝產業出現了幾個長期趨勢,推動需求成長。隨著經濟活動轉向應對 COVID-19 疫情帶來的挑戰,包裝產業成長加速。該行業的強勁表現得益於食品飲料和醫療保健等主要終端市場的收益成長和擴張,同時也顯示了該行業在更廣泛的經濟不確定時期的整體穩定性。

- 2021 年,由於買家和賣家在疫情導致交易幾乎停滯之後急切地重返市場,包裝行業的併購活動激增。疫情期間包裝公司的強勁表現強化了這樣一種觀念:包裝產業在整體市場動盪期間提供了穩定性。疫情也增強了現有的順風因素,例如電子商務的快速擴張以及品牌所有者採用包裝來在超級市場貨架上區分其產品,為該行業更強勁的長期成長奠定了基礎。

- 截至目前,可溶解包裝、節省空間包裝和智慧包裝是包裝產業出現的一些創新。採用可食用包裝是一種有趣且創新的替代方案,它有可能減少對石化燃料的依賴並顯著減少碳足跡,並且由於其永續性而在整個食品行業中變得越來越普遍。這些因素為食品和飲料包裝行業創造了成長機會,並有望在預測期內推動包裝行業的成長。

建築業蓬勃發展,住宅和基礎建設不斷成長

- 建設產業呈現穩定成長,2017 年至 2019 年的複合年成長率為 2.6%。這一成長受到全球經濟活動好轉和獨棟住宅需求增加的推動。 2020年,新冠疫情對全球建築建設產業產生了重大影響。勞動力供應限制、建築融資和供應鏈中斷以及經濟不確定性對全球建設產業產生了負面影響。

- 雖然2021年呈現正成長,但疫情對供應鏈的衝擊導致原物料價格上漲,仍在困擾產業。不過,由於建築業對一個國家的經濟影響重大,北美和亞太國家都透過提供支持計畫來重新啟動經濟週期。支持計劃包括澳大利亞的HomeBuilder計劃和歐盟國家的經濟復甦計劃。

- 亞太地區是建設活動最多的地區,預計到 2028 年仍將是最大的建築市場,這得益於其龐大的人口、不斷加快的都市化進程以及中國、印度、日本、印尼和韓國等國家對基礎設施建設的投資不斷增加。

- 預計在預測期內,對綠色建築的日益重視和減少全球建設活動排放的努力將帶來更永續的營運程序。例如,法國已累計75億歐元用於建設產業轉型為低碳能源經濟。

聚氨酯接著劑產業概況

聚氨酯接著劑市場分散,前五大公司佔18.76%的市佔率。該市場的主要企業有:3M、HB Fuller Company、Henkel AG & Co. KGaA、Huntsman International LLC 和 Sika AG(按字母順序排列)

其他福利

- Excel 格式的市場預測 (ME) 表

- 3個月的分析師支持

目錄

第1章執行摘要和主要發現

第2章 報告要約

第3章 引言

- 研究假設和市場定義

- 研究範圍

- 調查方法

第4章 產業主要趨勢

- 最終用戶趨勢

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 包裝

- 木製品和配件

- 法律規範

- 阿根廷

- 澳洲

- 巴西

- 加拿大

- 中國

- EU

- 印度

- 印尼

- 日本

- 馬來西亞

- 墨西哥

- 俄羅斯

- 沙烏地阿拉伯

- 新加坡

- 南非

- 韓國

- 泰國

- 美國

- 價值鍊和通路分析

第5章市場區隔

- 最終用戶產業

- 航太

- 車

- 建築與施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 木製品和配件

- 其他最終用戶產業

- 科技

- 熱熔膠

- 反應性

- 溶劑型

- 紫外線固化膠合劑

- 水

- 地區

- 亞太地區

- 澳洲

- 中國

- 印度

- 印尼

- 日本

- 馬來西亞

- 新加坡

- 韓國

- 泰國

- 其他亞太地區

- 歐洲

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲地區

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地區

- 亞太地區

第6章競爭格局

- 關鍵策略趨勢

- 市場佔有率分析

- 商業狀況

- 公司簡介

- 3M

- Arkema Group

- Beijing Comens New Materials Co., Ltd.

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co. Ltd

- Huntsman International LLC

- Jowat SE

- Kangda New Materials(Group)Co., Ltd.

- MAPEI SpA

- NANPAO RESINS CHEMICAL GROUP

- Pidilite Industries Ltd.

- Sika AG

- Soudal Holding NV

第7章:CEO面臨的關鍵策略問題

第 8 章 附錄

- 全球黏合劑和密封劑產業概況

- 概述

- 五力分析框架(產業吸引力分析)

- 全球價值鏈分析

- 促進因素、限制因素和機會

- 資訊來源及延伸閱讀

- 圖片列表

- 關鍵見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92411

The Polyurethane Adhesives Market size is estimated at 14.70 billion USD in 2024, and is expected to reach 18.45 billion USD by 2028, growing at a CAGR of 5.86% during the forecast period (2024-2028).

Emerging construction and packaging end-use sector expected to boost the consumption of polyurethane adhesives, globally

- Polyurethane adhesives are widely used in the packaging industry. Polyurethane adhesives are used in food and beverage packaging, container packaging, end-of-line packaging for functional barrier applications, and metal packaging. Additionally, according to a report published by the Association for Packaging and Processing Technologies, growth in the global packaging industry reached USD 42.2 billion in 2021, which increased from USD 36.8 billion in 2016, owing to the increasing population, growing sustainability concerns, more spending power in developing regions, the rising demand for smart packaging, and others.

- Similarly, the building and construction segment occupies the second-highest share in the global polyurethane adhesives market. Polyurethane adhesives offer good cohesion, adhesion and elasticity, high cohesive strength, flexibility, and high elastic modulus of the substrate. According to the United Nations (UN), around 50% of the global population resides in urban cities, which is projected to touch 60% by 2030. The pace of economic and demographic growth must be in harmony with the demand for commercial, residential, and institutional construction activities. By 2030, around 40% of the global population is likely to need housing at the rate of over 96,150 houses per day. Thus, rising construction activities are likely to drive the market for polyurethane adhesives in the upcoming years.

- Polyurethane adhesives are widely used in electronics and electrical equipment manufacturing. The electronics and household appliances industries are expected to record a CAGR of 2.51% and 5.77%, respectively, globally, which will lead to an increase in demand for polyurethane adhesives during the forecast period (2022-2028).

Increased investments and recovery funds in North America, Europe and Asia-Pacific, projected to raise the global utilization of polyurethane adhesives in various end-use sectors

- The Asia Pacific has occupied the largest share of the demand for polyurethane adhesives throughout the entire study period because of the large number of construction and packaging activities, Automotive, Medical devices, and aerospace production capacities, and other well-established end-user industries in the region. China is the largest construction and automotive market globally and generates up to 58% of the demand from the Asia Pacific region.

- During 2017-19 the demand for polyurethane adhesives has been sluggish. This is because of slow growth in Europe and the Asia Pacific regions. The global decline in the demand from construction and automotive end-user industries, which are among the major end-user industries, has restricted the overall growth of polyurethane adhesives demand. The demand from these industries declined with CAGRs of -0.05% and -1.79% during this period.

- In 2020, the demand for polyurethane adhesives from all end-user industries declined because of the covid-19 pandemic. In some countries like South Africa, and Brazil among others construction activities were deemed essential and were allowed to operate during the pandemic. Factors like these have cushioned the global impact restricting the decline to 8.96% in 2020.

- In 2021, due to the relief packages and support schemes in countries like the United States, Australia, and countries in the EU among others, the demand started to recover and this growth trend is expected to continue throughout the forecast period. Increased investments and budget allotments witnessed in countries of Europe, South America, and the Asia Pacific regions are expected to be major driving factors for this growth.

Global Polyurethane Adhesives Market Trends

Fast paced growth of e-commerce industry in developing nations to augment the industry

- In 2020, the packaging industry started with multiple long-term trends driving higher demand, and growth accelerated as economic activity switched to address the challenges posed by the COVID-19 pandemic. The industry's robust performance supported rising revenues and the expansion of important end markets such as food and beverage and healthcare and also demonstrated the industry's general stability during a period of overall economic uncertainty.

- Packaging M&A activities soared in 2021, as buyers and sellers enthusiastically returned to the market after deal-making almost ceased during the pandemic in 2020. During the pandemic, the strong performance of packaging companies reinforced the idea that the industry offers stability during moments of general market turbulence. The pandemic also strengthened previously existing tailwinds, including rapid e-commerce expansion and brand owners employing packaging to differentiate their products on supermarket shelves, positioning the sector for stronger long-term growth.

- As of now, dissolvable packaging, space-saving packaging, and smart packaging are a few innovations that have come up in the packaging industry. The adoption of edible packaging, an interesting and innovative alternative that alleviates the reliance on fossil fuels and has the potential to significantly decrease the carbon footprint, is now becoming popular across the food industry owing to its sustainability. These factors have created a growth opportunity for the packaging industry in the food and beverage sector, which is expected to boost the packaging industry's growth during the forecast period.

Growing residential and infrastructural development to thrive the construction sector

- The building and construction industry witnessed steady growth, with a CAGR of 2.6% from 2017 to 2019. This growth was driven by the upswing in global economic activity and increasing demand for single-family homes. In 2020, the COVID-19 pandemic had a major impact on the global building and construction industry. Constraints in labor supply, disruptions in construction finances and the supply chain, and economic uncertainty negatively impacted the global building and construction industry.

- Though the industry showed positive growth in 2021, the pandemic's effect on supply chains, which resulted in a hike in raw material prices, is still plaguing the industry. However, as the construction industry heavily influences a nation's economy, countries in Europe, North America, and Asia-Pacific have used the construction industry to restart their economic cycles by offering support schemes. Some support schemes include the Homebuilder Programme in Australia and the economic recovery plan of EU countries.

- The Asia-Pacific region experiences the highest volume of construction activities, and it is expected to remain the largest construction market till 2028 due to its huge population, increasing urbanization, and increasing investments in infrastructural development in countries like China, India, Japan, Indonesia, and South Korea.

- Increasing emphasis on green buildings and efforts to reduce emissions from global construction activities are expected to result in more sustainable operational procedures during the forecast period. For example, France has sanctioned EUR 7.5 billion for the construction industry to transform itself into a low-carbon energy economy.

Polyurethane Adhesives Industry Overview

The Polyurethane Adhesives Market is fragmented, with the top five companies occupying 18.76%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Huntsman International LLC and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Footwear and Leather

- 4.1.5 Packaging

- 4.1.6 Woodworking and Joinery

- 4.2 Regulatory Framework

- 4.2.1 Argentina

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 EU

- 4.2.7 India

- 4.2.8 Indonesia

- 4.2.9 Japan

- 4.2.10 Malaysia

- 4.2.11 Mexico

- 4.2.12 Russia

- 4.2.13 Saudi Arabia

- 4.2.14 Singapore

- 4.2.15 South Africa

- 4.2.16 South Korea

- 4.2.17 Thailand

- 4.2.18 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Woodworking and Joinery

- 5.1.8 Other End-user Industries

- 5.2 Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured Adhesives

- 5.2.5 Water-borne

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 China

- 5.3.1.3 India

- 5.3.1.4 Indonesia

- 5.3.1.5 Japan

- 5.3.1.6 Malaysia

- 5.3.1.7 Singapore

- 5.3.1.8 South Korea

- 5.3.1.9 Thailand

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 United Kingdom

- 5.3.2.7 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Saudi Arabia

- 5.3.3.2 South Africa

- 5.3.3.3 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Beijing Comens New Materials Co., Ltd.

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Hubei Huitian New Materials Co. Ltd

- 6.4.8 Huntsman International LLC

- 6.4.9 Jowat SE

- 6.4.10 Kangda New Materials (Group) Co., Ltd.

- 6.4.11 MAPEI S.p.A.

- 6.4.12 NANPAO RESINS CHEMICAL GROUP

- 6.4.13 Pidilite Industries Ltd.

- 6.4.14 Sika AG

- 6.4.15 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

聚氨酯黏合劑市場:按類型、固化機制、終端用戶產業、應用和分銷管道分類-2026-2032年全球市場預測

聚氨酯黏合劑市場:按類型、固化機制、終端用戶產業、應用和分銷管道分類-2026-2032年全球市場預測 全球聚氨酯接著劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球聚氨酯接著劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球聚氨酯接著劑市場報告

2026年全球聚氨酯接著劑市場報告 電子產業用聚氨酯(PU)黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

電子產業用聚氨酯(PU)黏合劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球聚氨酯接著劑市場(按類型、技術、應用和地區分類)- 預測至 2030 年

全球聚氨酯接著劑市場(按類型、技術、應用和地區分類)- 預測至 2030 年 聚氨酯接著劑的全球市場:類別,各技術,各終端用戶業界,各地區,機會,預測,2018年~2032年亞太聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)中東和非洲聚氨酯(PU)黏合劑市場佔有率分析、產業趨勢和成長預測(2025-2030)聚氨酯接著劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

聚氨酯接著劑的全球市場:類別,各技術,各終端用戶業界,各地區,機會,預測,2018年~2032年亞太聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)歐洲聚氨酯接著劑:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030)中東和非洲聚氨酯(PU)黏合劑市場佔有率分析、產業趨勢和成長預測(2025-2030)聚氨酯接著劑和密封劑:市場佔有率分析、行業趨勢和成長預測(2025-2030 年)

▼