|

市場調查報告書

商品編碼

2038674

空調系統市場機會、成長要素、產業趨勢分析及2026-2035年預測。Air Conditioning System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

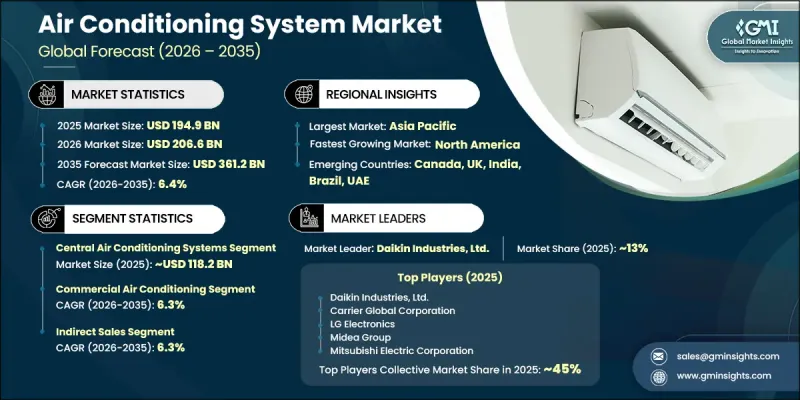

預計到 2025 年,全球空調系統市場價值將達到 1,949 億美元,並以 6.4% 的複合年成長率成長,到 2035 年將達到 3,612 億美元。

受全球氣溫上升和氣候模式變化的影響,各大主要地區對冷凍解決方案的依賴性顯著增強,導致市場擴張。除了熱浪強度和頻率不斷增加外,更長的暖季和不斷上升的平均氣溫也使空調從可有可無的配置轉變為確保室內溫度舒適度和業務連續性的必需品。在都市區,熱島效應進一步推高了環境溫度,加速了冷氣需求。住宅、商業和工業基礎設施越來越依賴空調系統來維持室內舒適度和生產力。同時,收入水準和生活水準的提高也推動了需求成長,尤其是在新興經濟體,消費者正從基本的製冷方式轉向更先進、更節能的系統。亞太地區、中東和非洲以及拉丁美洲等地區的中產階級壯大、資金籌措管道的增加以及快速的城市化進程,進一步推動了空調的普及。隨著全球氣候變遷持續加劇,預計在整個預測期內,對高效、永續和可靠的空調系統的需求將保持強勁成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 1949億美元 |

| 預測金額 | 3612億美元 |

| 複合年成長率 | 6.4% |

預計到2025年,中央空調系統市場規模將達到1,182億美元,並在2026年至2035年間以6.5%的複合年成長率成長。城市基礎設施的不斷完善和大規模建設活動正推動各類建築快速採用集中式冷凍解決方案。商業設施、醫療設施、交通樞紐、住宿設施、資料處理中心和高密度住宅專案的不斷湧現,增加了對集中式系統的需求,以確保均勻的溫度控制、改善空氣品質管理並降低噪音水平。此外,人們對能源效率和環境永續性的日益關注,也推動了現代化集中式系統的普及,這些系統採用先進的冷卻器、變速技術和智慧控制機制,與分散式冷凍系統相比,能夠降低能耗和運行成本。

預計到2025年,間接分銷管道將佔據68.6%的市場佔有率,並在2035年之前以6.3%的複合年成長率成長。這些通路包括經銷商、經銷商、批發商、零售商以及不斷擴展的線上平台,使製造商能夠觸及不同地理的更廣泛客戶群。在直銷網路有限的新興都市區和郊區市場,間接分銷管道也發揮著至關重要的作用。這種流通結構使客戶能夠輕鬆獲得多個品牌、具有競爭力的價格、本地化的產品供應以及捆綁式的安裝和維護服務。這些優勢使得間接分銷在住宅和小規模商業應用領域特別有效,因為在這些領域,便利性和服務可近性對購買決策有顯著的影響。

美國暖通空調(HVAC)市場預計到2025年將達到434億美元,並在2026年至2035年間以6.5%的複合年成長率成長。氣溫上升、熱浪頻繁以及冷凍季節延長,正顯著推動住宅、商業和工業領域的冷卻需求成長。消費者強勁的購買力和較高的可支配收入也促進了標準型和高階暖通空調系統的普及。除了需要更換老化的暖通空調基礎設施外,對更節能解決方案的升級需求也進一步擴大了全國範圍內的市場規模。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 全球暖化與氣候變遷

- 可支配所得增加及生活水準提高

- 技術進步和智慧功能

- 產業潛在風險與挑戰

- 高能耗和營運成本

- 前期實施成本高

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 各地區價格波動

- 按最終用戶群體分類的價格敏感度

- 貿易數據分析(基於初步調查)

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 對貿易政策的影響

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- 針對特定領域的生成式人工智慧應用案例和實施藍圖

- 風險、限制和監管考量

- 波特五力分析

- PESTEL 分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 中央空調系統

- 分離式空調系統

- 窗型冷氣

- 無管道迷你分離式系統

第6章 市場估計與預測:依冷氣量分類,2022-2035年

- 低容量(低於 12,000 BTU)

- 中等容量(12,000-24,000 BTU)

- 高容量(24,000-60,000 BTU)

- 超高容量(超過 60,000 BTU)

第7章 市場估計與預測:依冷媒類型分類,2022-2035年

- R-410A(標準)

- R-32(低全球暖化潛勢值)

- R-290(丙烷/天然冷媒)

- 下一代低全球暖化潛值冷媒

第8章 市場估算與預測:依能源效率等級分類,2022-2035年

- 標準效率

- 高效率

- 超高效率

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅空調

- 商用空調

- 工業空調

第10章 市場估價與預測:依銷售管道分類,2022-2035年

- 直銷

- 間接銷售

第11章 市場估價與預測:按地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第12章:公司簡介

- Blue Star Limited

- Bosch

- Carrier Global Corporation

- Daikin Industries Ltd.

- Gree Electric Appliances Inc.

- Haier Group Corporation

- Johnson Controls

- LG Electronics

- Midea Group

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Rheem Manufacturing Company

- Samsung Electronics Co., Ltd.

- Trane Technologies(Ingersoll Rand)

- Voltas Limited

The Global Air Conditioning System Market was valued at USD 194.9 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 361.2 billion by 2035.

The market is expanding as rising global temperatures and shifting climate patterns significantly increase dependence on cooling solutions across all major regions. Growing intensity and frequency of heatwaves, along with extended warm seasons and higher average temperatures, are transforming air conditioning from a discretionary purchase into an essential requirement for thermal comfort and operational continuity. Urban environments are experiencing even stronger demand due to the heat island effect, which further elevates ambient temperatures and accelerates cooling needs. Residential, commercial, and industrial infrastructures are increasingly reliant on air conditioning systems to maintain indoor comfort and productivity levels. At the same time, improving income levels and rising living standards are reinforcing demand, particularly in emerging economies where consumers are upgrading from basic cooling alternatives to more advanced and energy-efficient systems. Expanding middle-class populations, easier access to financing, and rapid urban development across regions such as Asia-Pacific, the Middle East, Africa, and Latin America are further strengthening adoption rates. As climate variability continues to intensify globally, the demand for efficient, sustainable, and reliable air conditioning systems is expected to remain structurally strong over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $194.9 Billion |

| Forecast Value | $361.2 Billion |

| CAGR | 6.4% |

The central air conditioning systems segment accounted for USD 118.2 billion in 2025 and is projected to grow at a CAGR of 6.5% from 2026 to 2035. Increasing urban infrastructure development and large-scale construction activities are driving strong adoption of centralized cooling solutions across various building types. Rising construction of commercial complexes, healthcare facilities, transportation hubs, hospitality establishments, data processing centers, and high-density residential projects is boosting demand for centralized systems that ensure uniform temperature control, improved air quality management, and reduced noise levels. Additionally, the growing focus on energy efficiency and environmental sustainability is supporting the transition toward modern centralized systems equipped with advanced chillers, variable speed technologies, and intelligent control mechanisms that reduce energy consumption and operating expenses compared to decentralized cooling setups.

The indirect distribution channel held a 68.6% share in 2025 and is expected to grow at a CAGR of 6.3% through 2035. This channel includes distributors, dealers, wholesalers, retailers, and expanding online platforms that collectively enable manufacturers to reach a wider consumer base across diverse geographic regions. It plays a crucial role in penetrating emerging urban and semi-urban markets where direct sales networks are limited. The channel structure provides customers with easier access to multiple brands, competitive pricing options, localized product availability, and bundled installation and maintenance services. These advantages make indirect distribution especially effective in residential and light commercial applications, where convenience and service accessibility strongly influence purchasing decisions.

U.S. Air Conditioning System Market accounted for USD 43.4 billion in 2025 and is anticipated to grow at a CAGR of 6.5% from 2026 to 2035. Increasing temperatures, recurring heatwave events, and longer cooling seasons are significantly raising cooling demand across residential, commercial, and industrial sectors. Strong consumer purchasing power and high disposable income levels are also supporting widespread adoption of both standard and premium air conditioning systems. Replacement demand for aging HVAC infrastructure, along with upgrades to more energy-efficient solutions, is further reinforcing market expansion across the country.

Major players operating in the Global Air Conditioning System Industry include Panasonic Corporation, LG Electronics, Haier Group Corporation, Daikin Industries, Ltd., Carrier Global Corporation, Mitsubishi Electric Corporation, Samsung Electronics Co., Ltd., Johnson Controls, Bosch, Blue Star Limited, Gree Electric Appliances Inc., Midea Group, Trane Technologies (Ingersoll Rand), Voltas Limited, and Rheem Manufacturing Company. Key companies in the Air Conditioning System Market are focusing on enhancing energy efficiency through the development of inverter-based and smart HVAC technologies that reduce power consumption and improve operational performance. They are investing heavily in research and development to integrate IoT-enabled controls, predictive maintenance, and AI-driven climate management systems. Expansion of manufacturing facilities and strengthening of global supply chains are helping companies improve production capacity and reduce delivery timelines. Strategic collaborations with construction firms, real estate developers, and commercial infrastructure projects are increasing product adoption in large-scale installations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Cooling capacity

- 2.2.4 Refrigerant type

- 2.2.5 Energy efficiency class

- 2.2.6 End-use

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global temperatures and climate change

- 3.2.1.2 Growing disposable income and improved living standards

- 3.2.1.3 Technological advancements and smart features

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High energy consumption and operating costs

- 3.2.2.2 High initial installation costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Pricing analysis (driven by primary research)

- 3.7.1 Historical price trend analysis

- 3.7.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.7.3 Regional price variations

- 3.7.4 Price sensitivity by end-user segment

- 3.8 Trade data analysis (driven by primary research)

- 3.8.1 Import/export volume & value trends

- 3.8.2 Key trade corridors & tariff impact

- 3.8.3 Trade policy implications

- 3.9 Capacity & production landscape (driven by primary research)

- 3.9.1 Installed capacity by region & key producer

- 3.9.2 Capacity utilization rates & expansion pipelines

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Central air conditioning systems

- 5.3 Split air conditioning systems

- 5.4 Window unit air conditioning system

- 5.5 Ductless mini-split systems

Chapter 6 Market Estimates & Forecast, By Cooling Capacity, 2022 - 2035, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low capacity (Less than 12,000 BTU)

- 6.3 Medium capacity (12,000 - 24,000 BTU)

- 6.4 High capacity (24,000 - 60,000 BTU)

- 6.5 Ultra-high capacity (Over 60,000 BTU)

Chapter 7 Market Estimates & Forecast, By Refrigerant Type, 2022 - 2035, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 R-410A (Standard)

- 7.3 R-32 (Lower GWP)

- 7.4 R-290 (Propane/Natural Refrigerant)

- 7.5 Next-gen low-GWP refrigerants

Chapter 8 Market Estimates & Forecast, By Energy Efficiency Class, 2022 - 2035, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Standard Efficiency

- 8.3 High Efficiency

- 8.4 Ultra-High Efficiency

Chapter 9 Market Estimates & Forecast, By End-Use, 2022 - 2035, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Residential air conditioning

- 9.3 Commercial air conditioning

- 9.4 Industrial air conditioning

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Million Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Blue Star Limited

- 12.2 Bosch

- 12.3 Carrier Global Corporation

- 12.4 Daikin Industries Ltd.

- 12.5 Gree Electric Appliances Inc.

- 12.6 Haier Group Corporation

- 12.7 Johnson Controls

- 12.8 LG Electronics

- 12.9 Midea Group

- 12.10 Mitsubishi Electric Corporation

- 12.11 Panasonic Corporation

- 12.12 Rheem Manufacturing Company

- 12.13 Samsung Electronics Co., Ltd.

- 12.14 Trane Technologies (Ingersoll Rand)

- 12.15 Voltas Limited

盒式空調:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)窗型冷氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)空調設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

盒式空調:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)窗型冷氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)空調設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 空調系統市場:2026-2032年全球市場預測(依產品類型、技術、冷氣、組件、冷媒類型、能源效率、應用和銷售管道)北美暖通空調市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年)

空調系統市場:2026-2032年全球市場預測(依產品類型、技術、冷氣、組件、冷媒類型、能源效率、應用和銷售管道)北美暖通空調市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031 年) 空調系統市場規模、佔有率和趨勢分析報告:按類型、技術、應用、地區和細分市場預測(2026-2033 年)

空調系統市場規模、佔有率和趨勢分析報告:按類型、技術、應用、地區和細分市場預測(2026-2033 年) 立式空調市場:按類型、應用、最終用戶和地區分類空調市場:2026-2032年全球市場預測(依銷售管道、技術、冷氣量、產品類型及最終用戶分類)

立式空調市場:按類型、應用、最終用戶和地區分類空調市場:2026-2032年全球市場預測(依銷售管道、技術、冷氣量、產品類型及最終用戶分類) 全球空調系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)空調系統市場:按類型、技術、最終用戶和地區分類

全球空調系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)空調系統市場:按類型、技術、最終用戶和地區分類