|

市場調查報告書

商品編碼

1885801

肉類副產品蛋白水解物市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)Meat by-product Protein Hydrolysates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

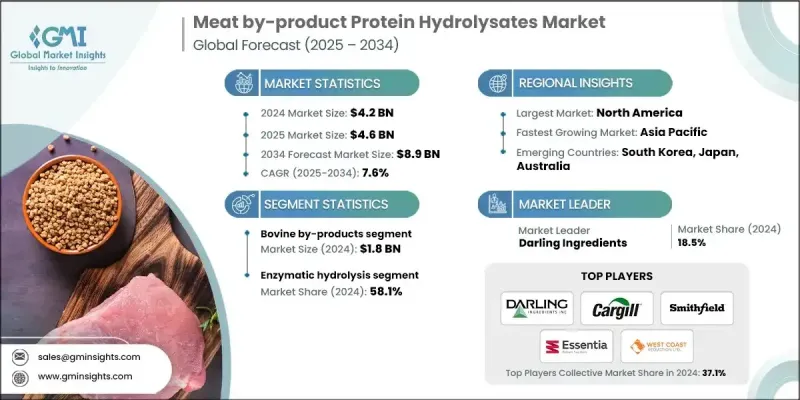

2024 年全球肉類副產品蛋白水解物市場價值為 42 億美元,預計到 2034 年將以 7.6% 的複合年成長率成長至 89 億美元。

這些水解物是源自動物副產品(如骨骼、羽毛和內臟)酶解的生物活性胜肽。它們具有優異的消化率、高生物利用度和在動物營養方面的功能優勢,正推動其作為傳統蛋白質來源的替代品而廣泛應用。隨著世界各國政府大力倡導減少浪費和提高資源效率,對永續蛋白質解決方案的需求不斷成長,進一步推動了市場發展。將肉類副產品轉化為蛋白質水解物不僅可以減少浪費,還能提供一種經濟高效的優質飼料添加劑,符合全球永續發展目標。監管激勵措施,尤其是在歐洲等地區,旨在最佳化廢棄物利用,從而直接支持市場擴張。寵物食品和牲畜飼料產業對動物健康和營養的日益關注,也持續推動市場需求。北美目前憑藉先進的製造基礎設施、強力的監管支持和較高的市場接受度佔據主導地位,而亞太地區則是成長最快的市場,這主要得益於肉類消費量的成長、城市化進程的加快以及對永續動物營養的日益重視。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 42億美元 |

| 預測值 | 89億美元 |

| 複合年成長率 | 7.6% |

2024年,牛副產品創造了18億美元的市場價值,繼續保持市場主導地位。這些原料來源豐富且富含蛋白質,是生產肉類副產品蛋白水解物的經濟高效且可靠的原料。其營養成分有助於動物生長和免疫健康,因此在動物飼料和水產養殖領域中廣泛應用。萃取和水解技術的進步簡化了牛副產品的加工流程,進一步鞏固了其市場地位。

2024年,酵素水解法佔了58.1%的市佔率。此方法之所以備受青睞,是因為它能產生高品質、高生物利用度且具有特定功能特性的蛋白質水解物。酵素能選擇性地將蛋白質分解成具有更高消化率和生物活性的成分,同時最大限度地減少化學殘留,使該製程更安全、更環保。因此,酵素水解法在配製天然和有機動物飼料產品中具有很高的價值。

預計2025年至2034年間,北美肉類副產品蛋白水解物市場將以7.7%的複合年成長率成長。市場對促進環境保護和永續農業實踐的飼料原料的需求不斷成長。消費者的環保意識日益增強,產業參與者也更重視負責任的畜牧業。天然、可生物分解和永續的蛋白水解物正日益受到歡迎。包括酵素水解、發酵和生物技術進步在內的技術創新,在提高產品品質和安全性的同時,也降低了生產成本。

全球肉類副產品蛋白水解物市場的主要參與者包括 Titan Biotech、West Coast Reduction Ltd、Cargill、Hormel Foods Corporation、Essentia Protein Solutions、Smithfield Foods Inc、Novonesis、National Beef Packing Company、Sanimax 和 Darling Ingredients。這些企業正透過技術創新、擴大產能和加大研發投入來提升水解物質量,從而鞏固其市場地位。策略合作和併購有助於它們拓展分銷網路並進入新興市場。此外,企業也致力於永續發展,例如利用廢棄物和開發環保加工方法,以提升品牌信譽。

目錄

第1章:方法論與範圍

第2章:執行概要

第3章:行業洞察

- 產業生態系分析

- 供應商格局

- 利潤率

- 每個階段的價值增加

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 成長促進因素

- 對永續蛋白質來源的需求不斷成長

- 循環經濟在食品加工的應用

- 寵物食品和動物飼料產業蓬勃發展

- 產業陷阱與挑戰

- 品質標準化挑戰

- 供應鏈中斷脆弱性

- 市場機遇

- 與替代蛋白質價值鏈的整合

- 新興生物活性胜肽的應用

- 成長促進因素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 技術與創新格局

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 來源

- 未來市場趨勢

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 合作夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估算與預測:依來源分類,2021-2034年

- 主要趨勢

- 牛副產品

- 豬副產品

- 家禽副產品

- 其他

第6章:市場估算與預測:依製程分類,2021-2034年

- 主要趨勢

- 酵素水解

- 化學水解

- 微生物發酵

第7章:市場估計與預測:依應用領域分類,2021-2034年

- 主要趨勢

- 餐飲

- 增味劑

- 蛋白質強化劑

- 其他

- 動物飼料

- 寵物食品

- 牲畜飼料

- 其他

- 臨床營養

- 運動營養

- 嬰兒營養

- 膳食補充劑

- 其他

第8章:市場估算與預測:依地區分類,2021-2034年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Cargill

- Darling Ingredients

- Essentia Protein Solutions

- Hormel Foods Corporation

- National Beef Packing Company

- Novonesis

- Sanimax

- Smithfield Foods Inc

- Titan Biotech

- West Coast Reduction Ltd

The Global Meat by-product Protein Hydrolysates Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 8.9 billion by 2034.

These hydrolysates are bioactive peptides derived from the enzymatic breakdown of animal by-products such as bones, feathers, and offal. Their exceptional digestibility, high bioavailability, and functional benefits in animal nutrition are driving their adoption as an alternative to traditional protein sources. Rising demand for sustainable protein solutions is further boosting the market, as governments worldwide promote waste reduction and resource efficiency. Transforming meat by-products into protein hydrolysates not only reduces waste but also offers a cost-effective, high-quality feed additive, aligning with global sustainability goals. Regulatory incentives, particularly in regions like Europe, are focused on optimizing waste usage, directly supporting market expansion. Increasing attention to animal health and nutrition in the growing pet food and livestock feed sectors continues to fuel demand. North America currently dominates the market due to advanced manufacturing infrastructure, robust regulatory support, and high adoption rates, while the Asia-Pacific region is the fastest-growing market, driven by rising meat consumption, urbanization, and a growing focus on sustainable animal nutrition.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $8.9 Billion |

| CAGR | 7.6% |

In 2024, the bovine by-products generated USD 1.8 billion, maintaining a dominant position in the market. These sources are abundant and protein-rich, offering a cost-effective and reliable raw material for producing meat by-product protein hydrolysates. Their nutritional profile supports growth and immune health, making them popular in animal feed and aquaculture applications. Advances in extraction and hydrolysis techniques have simplified processing from bovine sources, further strengthening their market position.

The enzymatic hydrolysis segment accounted for a 58.1% share in 2024. This method is preferred because it produces high-quality, bioavailable protein hydrolysates with targeted functional properties. Enzymes selectively break down proteins into fractions with enhanced digestibility and bioactivity while minimizing chemical residues, making the process safer and more environmentally friendly. As a result, enzymatic hydrolysis is highly valued in formulating natural and organic animal feed products.

North America Meat by-product Protein Hydrolysates Market is expected to grow at a CAGR of 7.7% between 2025 and 2034. Demand is rising for feed ingredients that promote environmental conservation and sustainable farming practices. Awareness among consumers is increasing, and industry players are emphasizing responsible animal husbandry. Natural, biodegradable, and sustainable protein hydrolysates are gaining popularity. Technological innovations, including enzymatic hydrolysis, fermentation, and biotechnology advancements, are enhancing product quality and safety while reducing production costs.

Key players in the Global Meat by-product Protein Hydrolysates Market include Titan Biotech, West Coast Reduction Ltd, Cargill, Hormel Foods Corporation, Essentia Protein Solutions, Smithfield Foods Inc, Novonesis, National Beef Packing Company, Sanimax, and Darling Ingredients. Companies in the Meat by-product Protein Hydrolysates Market are adopting strategies to strengthen their market presence through technological innovation, expanding production capacities, and investing in R&D to improve hydrolysate quality. Strategic partnerships and mergers allow them to extend distribution networks and reach emerging markets. Focused efforts on sustainability, such as utilizing waste products and developing environmentally friendly processing methods, enhance brand credibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source trends

- 2.2.2 Process trends

- 2.2.3 Application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable protein sources

- 3.2.1.2 Circular economy implementation in food processing

- 3.2.1.3 Growing pet food & animal feed industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Quality standardization challenges

- 3.2.2.2 Supply chain disruption vulnerabilities

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with alternative protein value chains

- 3.2.3.2 Emerging bioactive peptide applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By source

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bovine by-products

- 5.3 Porcine by-products

- 5.4 Poultry by-products

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Process, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Enzymatic hydrolysis

- 6.3 Chemical hydrolysis

- 6.4 Microbial fermentation

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.2.1 Flavor enhancers

- 7.2.2 Protein fortifiers

- 7.2.3 Others

- 7.3 Animal feed

- 7.3.1 Pet food

- 7.3.2 Livestock feed

- 7.3.3 Others

- 7.4 Clinical nutrition

- 7.5 Sports nutrition

- 7.6 Infant nutrition

- 7.7 Dietary supplements

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Cargill

- 9.2 Darling Ingredients

- 9.3 Essentia Protein Solutions

- 9.4 Hormel Foods Corporation

- 9.5 National Beef Packing Company

- 9.6 Novonesis

- 9.7 Sanimax

- 9.8 Smithfield Foods Inc

- 9.9 Titan Biotech

- 9.10 West Coast Reduction Ltd

食品加工市場報告:趨勢、預測與競爭分析(至2035年)

食品加工市場報告:趨勢、預測與競爭分析(至2035年) 食品工業熱處理設備市場機會、成長要素、產業趨勢分析及2026-2035年預測超音波食品加工技術市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)酵素法食品加工解決方案市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

食品工業熱處理設備市場機會、成長要素、產業趨勢分析及2026-2035年預測超音波食品加工技術市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)酵素法食品加工解決方案市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年) 全球食品加工自動化市場全球植物來源食品加工設備市場全球食品切碎機市場攜帶式切碎機市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測食品切碎機市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 年

全球食品加工自動化市場全球植物來源食品加工設備市場全球食品切碎機市場攜帶式切碎機市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測食品切碎機市場機會、成長促進因素、產業趨勢分析與預測 2024 - 2032 年 食品加工的全球市場規模:各類型,各用途,各地區,範圍及預測

食品加工的全球市場規模:各類型,各用途,各地區,範圍及預測