|

市場調查報告書

商品編碼

1766362

烘焙原料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Baking Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

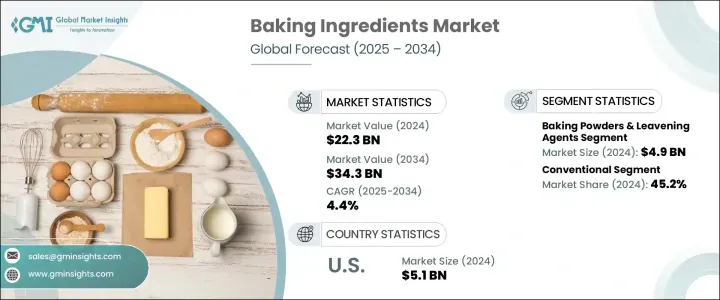

2024年,全球烘焙原料市場規模達223億美元,預計2034年將以4.4%的複合年成長率成長,達到343億美元。受全球各類烘焙產品需求不斷成長的推動,該市場呈現穩定成長態勢。營收和銷售均呈現持續成長,反映出全球消費模式的廣泛變化。促成這一趨勢的關鍵因素包括飲食習慣的轉變、城鎮化進程的加速以及人們對即食食品解決方案的日益偏好。包裝和便利烘焙食品日益流行,尤其是在新興地區,加速了對高性能烘焙原料的需求。同時,成熟經濟體的需求持續強勁,有助於維持整體市場動能。

不斷擴張的餐飲服務網路和有序的零售模式也提升了產品的可及性,從而增加了銷量,並提升了烘焙產品在市場上的多樣性。隨著現代零售店在城市和半城市地區的持續發展,消費者如今可以接觸到種類繁多的烘焙食品,從手工麵包到包裝簡便食品,應有盡有。這種便利性不僅促進了衝動性購買,也鼓勵了消費者嘗試新的產品類型和口味。此外,零售連鎖店和烘焙製造商之間的合作帶來了更佳的產品定位、促銷活動和店內烘焙專區,進一步提升了消費者的興趣,並推動了不同人群和消費場合的品類成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 223億美元 |

| 預測值 | 343億美元 |

| 複合年成長率 | 4.4% |

2024年,泡打粉和膨鬆劑市場規模達49億美元,預計2025年至2034年期間的複合年成長率將達到4.8%。這些原料在烘焙食品生產中仍然至關重要,因為它們能夠確保烘焙食品的透氣性、體積和質地的一致性。它們在工業烘焙和家庭烘焙中的廣泛應用鞏固了其市場主導地位。隨著城市人口的成長,尤其是在大城市,對加工和預包裝烘焙食品的需求持續成長,從而推動了膨鬆劑消費量的增加。此外,更新的清潔標籤產品和改進的配方在提供可靠效果的同時,也滿足了不斷變化的消費者需求。其成本效益使其成為小型烘焙店、商業廚房和餐飲服務機構不可或缺的一部分。

2024年,傳統配料市場價值達101億美元,預計到2034年將以4.6%的複合年成長率成長,佔據45.2%的市場佔有率。傳統產品的可靠性和價格實惠確保其仍然是滿足大量生產需求的首選。同時,人們對清潔標籤和非基因替代品的日益關注正在重塑市場格局,在注重健康的選擇和經濟高效的解決方案之間尋求平衡。越來越多的消費者出於對食品安全和環境影響的擔憂,開始轉向有機和可追溯的食品,這表明天然配料形式正日益受到青睞。

2024年,美國烘焙原料市場規模達51億美元,預計2025年至2034年期間的複合年成長率將達到4.2%。強勁的食品製造業基礎、消費者對加工烘焙食品日益成長的需求以及完善的供應鏈基礎設施,共同推動了這一穩健成長。原料配方的創新在維持市場成長方面發揮著重要作用,尤其對於滿足植物性、無麩質、低糖和純素食需求的產品而言。零售業的擴張以及全美各地消費者對包裝烘焙食品日益成長的偏好,進一步支撐了這一上升趨勢。

全球烘焙原料產業的主要參與者,包括焙樂道集團、樂斯福、嘉吉等,正在積極部署創新方法,以加強其全球影響力。這些公司優先考慮研發,推出符合現代飲食偏好的清潔標章、功能性和營養豐富的原料。與餐飲連鎖店和零售烘焙店的合作有助於他們擴大客戶覆蓋範圍。他們還投資區域生產中心,以確保供應鏈效率和對當地需求的回應能力。許多公司在產品開發和分銷方面採用數位化策略,以提高敏捷性和客戶參與度,鞏固其在工業和消費者細分市場的領導地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 簡便食品需求不斷成長

- 商業烘焙業的成長

- 增加可支配收入

- 改變消費者的生活方式

- 產業陷阱與挑戰

- 原物料價格波動

- 與添加劑有關的健康問題

- 市場機會

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- Pestel 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依成分類型,2021-2034

- 主要趨勢

- 泡打粉和膨鬆劑

- 乳化劑

- 酵素

- 油、脂肪和起酥油

- 甜味劑

- 顏色和口味

- 防腐劑

- 麵粉

- 澱粉

- 其他

第6章:市場估計與預測:依性質,2021-2034

- 主要趨勢

- 傳統的

- 有機的

- 清潔標籤

- 非基因改造

第7章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 麵包

- 蛋糕和糕點

- 餅乾和餅乾

- 麵包捲和餡餅

- 披薩餅皮

- 其他

第8章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 商業/工業麵包店

- 零售麵包店

- 手工麵包店

- 餐飲業

- 家庭/零售消費者

第9章:市場估計與預測:按配銷通路,2021-2034

- 主要趨勢

- B2B

- B2C

- 超市和大賣場

- 專賣店

- 便利商店

- 網路零售

- 其他

第10章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第 11 章:公司簡介

- AAK AB

- Archer Daniels Midland Company

- Associated British Foods plc

- Bakels Group

- BASF SE

- Cargill, Incorporated

- Corbion NV

- Dawn Food Products, Inc.

- DuPont de Nemours, Inc.

- DSM-Firmenich AG

- Flowers Foods, Inc.

- General Mills, Inc.

- Grupo Bimbo, SAB de CV

- Ingredion Incorporated

- Kerry Group plc

- Koninklijke DSM NV

- Lesaffre Group

- Mondelez International, Inc.

- Puratos Group

- Tate & Lyle PLC

The Global Baking Ingredients Market was valued at USD 22.3 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 34.3 billion by 2034. This market demonstrates stable growth, fueled by rising global demand across various categories of baked products. Both revenue and volume have shown consistent increases, reflecting widespread changes in consumption patterns worldwide. Key factors contributing to this trend include shifting dietary habits, growing urbanization, and a rising preference for ready-made food solutions. The growing popularity of packaged and convenience baked items, particularly in emerging regions, is accelerating the need for high-performance baking ingredients. At the same time, mature economies continue to show solid demand, helping to maintain overall market momentum.

Expanding food service networks and organized retail formats have also improved product accessibility, leading to increased sales volumes and broader diversification of baked offerings in the market. As modern retail outlets continue to grow in both urban and semi-urban areas, consumers now have greater exposure to a wide variety of baked goods, ranging from artisanal breads to packaged convenience items. This enhanced availability has not only boosted impulse purchases but has also encouraged experimentation with new product types and flavors. Additionally, partnerships between retail chains and bakery manufacturers have led to better product placement, promotional campaigns, and in-store bakery sections, further elevating consumer interest and driving category growth across multiple demographics and consumption occasions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.3 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 4.4% |

In 2024, the baking powders and leavening agents segment generated USD 4.9 billion and is forecast to grow at a 4.8% CAGR between 2025 and 2034. These ingredients remain vital in baked goods production due to their role in ensuring consistent aeration, volume, and texture. Their widespread use in both industrial and home baking reinforces their dominant market position. As urban populations grow, particularly in large cities, demand for processed and pre-packaged bakery items continues to rise-driving higher consumption of leavening agents. Additionally, newer clean-label options and improved formulations are catering to evolving consumer demands while delivering reliable results. Their cost-efficiency makes them an essential component across small bakeries, commercial kitchens, and food service operations.

The conventional ingredients segment was valued at USD 10.1 billion in 2024 and is projected to grow at a 4.6% CAGR through 2034, holding a 45.2% share. The reliability and affordability of conventional products ensure they remain a preferred option to meet high-volume production needs. Meanwhile, increased attention toward clean-label and non-GMO alternatives is reshaping market dynamics, offering a balance between health-conscious choices and cost-effective solutions. A growing segment of consumers is turning to organic and traceable options in response to concerns over food safety and environmental impact, signaling rising traction for natural ingredient formats.

United States Baking Ingredients Market was valued at USD 5.1 billion in 2024 and is expected to grow at a 4.2% CAGR from 2025 to 2034. This steady performance is driven by a strong food manufacturing base, rising consumer demand for processed baked items, and a robust supply chain infrastructure. Innovation in ingredient formulations plays a major role in sustaining market growth, especially for products tailored to meet demands for plant-based, gluten-free, sugar-reduced, and vegan options. Retail expansion and increasing preference for packaged baked goods across the country further support this upward trend.

Key players in the Global Baking ingredient industry, including Puratos Group, Lesaffre, Cargill, and others, are actively deploying innovative approaches to strengthen their global footprint. These companies are prioritizing research and development to introduce clean-label, functional, and nutrient-rich ingredients tailored to modern dietary preferences. Collaborations with food service chains and retail bakeries are helping them expand their customer reach. They are also investing in regional production hubs to ensure supply chain efficiency and responsiveness to local demands. Many are adopting digitalization strategies in product development and distribution to improve agility and customer engagement, reinforcing their market leadership across both industrial and consumer-facing segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Ingredient type

- 2.2.1.3 Nature

- 2.2.1.4 Application

- 2.2.1.5 End use

- 2.2.1.6 Distribution channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for convenience foods

- 3.2.1.2 Growth in commercial bakery sector

- 3.2.1.3 Increasing disposable income

- 3.2.1.4 Changing consumer lifestyles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Health concerns related to additives

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle east & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Ingredient Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Baking powders & leavening agents

- 5.3 Emulsifiers

- 5.4 Enzymes

- 5.5 Oils, fats & shortenings

- 5.6 Sweeteners

- 5.7 Colors & flavors

- 5.8 Preservatives

- 5.9 Flour

- 5.10 Starches

- 5.11 Others

Chapter 6 Market Estimates & Forecast, By Nature, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Organic

- 6.4 Clean label

- 6.5 Non-GMO

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bread

- 7.3 Cakes & pastries

- 7.4 Cookies & biscuits

- 7.5 Rolls & pies

- 7.6 Pizza crusts

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Commercial/industrial bakeries

- 8.3 Retail bakeries

- 8.4 Artisanal bakeries

- 8.5 Foodservice industry

- 8.6 Household/retail consumers

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 B2B

- 9.3 B2C

- 9.3.1 Supermarkets & hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Convenience stores

- 9.3.4 Online retail

- 9.3.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 AAK AB

- 11.2 Archer Daniels Midland Company

- 11.3 Associated British Foods plc

- 11.4 Bakels Group

- 11.5 BASF SE

- 11.6 Cargill, Incorporated

- 11.7 Corbion N.V.

- 11.8 Dawn Food Products, Inc.

- 11.9 DuPont de Nemours, Inc.

- 11.10 DSM-Firmenich AG

- 11.11 Flowers Foods, Inc.

- 11.12 General Mills, Inc.

- 11.13 Grupo Bimbo, S.A.B. de C.V.

- 11.14 Ingredion Incorporated

- 11.15 Kerry Group plc

- 11.16 Koninklijke DSM N.V.

- 11.17 Lesaffre Group

- 11.18 Mondelez International, Inc.

- 11.19 Puratos Group

- 11.20 Tate & Lyle PLC

全球活性餅狀乳化劑市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球活性餅狀乳化劑市場規模、佔有率、趨勢及成長分析報告(2026-2034) 烘焙原料市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)

烘焙原料市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年) 全球活性蛋糕乳化劑市場

全球活性蛋糕乳化劑市場 烘焙材料市場、規模、佔有率、趨勢、產業分析報告:依產品、最終用途、地區、市場預測2025-20342024 年至 2031 年烘焙食品配料市場(按產品、應用、分銷管道和地區劃分)

烘焙材料市場、規模、佔有率、趨勢、產業分析報告:依產品、最終用途、地區、市場預測2025-20342024 年至 2031 年烘焙食品配料市場(按產品、應用、分銷管道和地區劃分) 活性蛋糕乳化劑市場機會、成長動力、產業趨勢分析與預測 2024 - 2032烘焙原料市場:2022-2032年全球產業分析、規模、佔有率、成長、趨勢、預測

活性蛋糕乳化劑市場機會、成長動力、產業趨勢分析與預測 2024 - 2032烘焙原料市場:2022-2032年全球產業分析、規模、佔有率、成長、趨勢、預測 烘焙原料市場:依類型、形式和應用劃分 -2030年全球預測

烘焙原料市場:依類型、形式和應用劃分 -2030年全球預測