|

市場調查報告書

商品編碼

2055604

抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場:趨勢與預測(至2035年)-按產品類型、有效載荷類型、有效載荷/彈頭子類別和地區分類ADC Cytotoxic Payloads and Warheads Market: Trends and Forecast Til 2035 - Distribution Type of Product, Type of Payload, Sub-Category of Payload / Warhead and Geographical Regions |

||||||

抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場概述

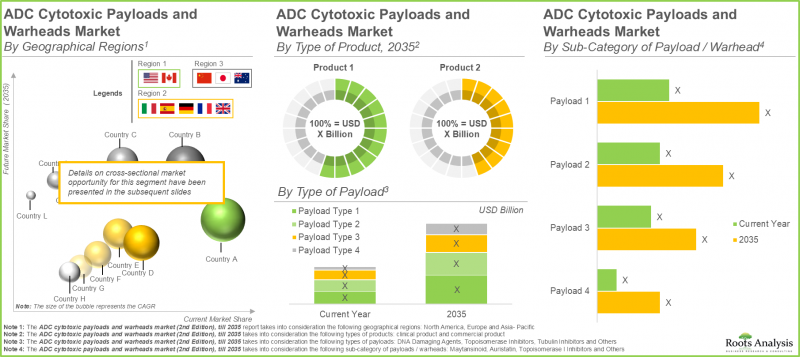

預計到 2035 年,ADC 細胞毒性有效載荷和彈頭市場將以 8.9% 的年複合成長率成長,從目前的 3.813 億美元成長到 2035 年的 4.693 億美元。

抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場-成長與趨勢

抗體藥物複合體(ADC),包括細胞毒性藥物和活性彈頭,是現代標靶癌症治療的重要組成部分,其研發目的是為了在降低整體毒性的同時,精準遞送高效化合物。化學最佳化和先進連接系統的引入提高了ADC的治療效果,使製藥公司能夠開發出更有效率、更具標靶性的癌症治療方法。

抗體藥物偶聯物(ADC)領域正透過利用有效載荷化學、偶聯技術和連接子技術的進步來提升安全性和有效性,從而實現快速成長。然而,該行業在ADC的大規模生產、有效載荷的選擇、藥物與抗體比例的調整以及符合臨床應用的嚴格法規和品質標準等方面仍然面臨挑戰。

確保成本效益和開發標準化表徵方法仍然是實現廣泛實用化的關鍵挑戰。然而,固體癌和血液系統惡性腫瘤領域應用的不斷增加,以及精準腫瘤學領域投資的不斷擴大,正在推動市場成長。

成長促進因素-市場擴張的策略促進因素

連接子穩定性、有效載荷效率和靶向遞送系統的持續改進正在提升抗體藥物偶聯物(ADC)的治療指數。這些進展使研究人員能夠在最大限度減少對健康組織損傷的同時,提高腫瘤清除率。這種精準的方法正在推動腫瘤學領域創新策略的出現,用於治療血液腫瘤和固體癌。

此外,對包括DNA損傷化合物和微管抑制劑在內的新一代有效載荷類別的需求不斷成長,正推動生物製藥領域取得顯著進展。對標靶癌症療法的投資增加以及偶聯技術的持續進步,正引領著抗體藥物偶聯物(ADC)有效載荷和彈頭領域的市場快速擴張。此外,新一代多彈頭抗體藥物複合體(ADC)的進步有望透過彌補現有ADC治療方法的不足,顯著促進市場成長。例如,Araris Biotech等公司已開發出專有的胜肽連接子技術,能夠在無需抗體修飾的情況下,透過單一製程將兩種或三種不同的細胞毒性藥物(彈頭)偶聯到單一抗體上。

市場挑戰-阻礙進展的主要障礙

由於能夠有效靶向癌細胞並最大限度降低脫靶毒性的高活性、高選擇性有效載荷的供應有限,抗體偶聯藥物(ADC)的細胞毒性有效載荷和彈頭市場面臨許多挑戰。複雜的生產流程、嚴格的法規要求以及專用有效載荷組分的供應鏈限制,都推高了研發成本和延長了研發週期。此外,有效載荷的穩定性、連接子相容性和抗藥性機制等問題也會影響治療效果。知識產權壁壘和持續創新的需求進一步加劇了市場競爭。

抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場—關鍵洞察

本報告對抗體偶聯藥物(ADC)細胞毒性有效載荷和彈頭市場的現狀進行了詳細分析,並指出了該行業的潛在成長機會。報告的主要發現包括:

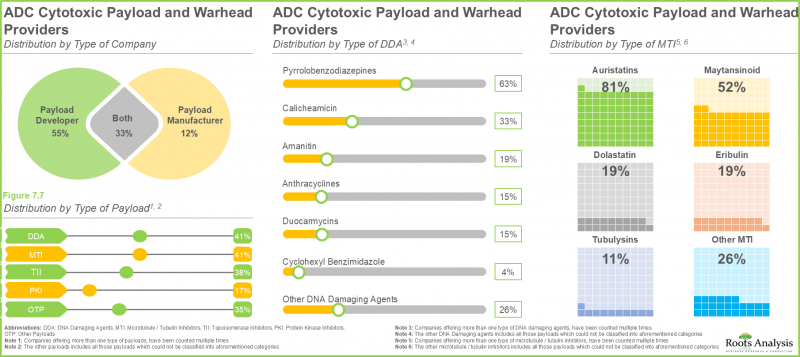

- 目前市場上約有 70 家供應商聲稱提供各種有效載荷,這些有效載荷正在各種治療領域中使用或測試。

- 大約25%的公司同時提供基於吡咯並苯二氮平類和奧瑞他汀的有效載荷。這是因為這些藥物效力極強,已被證明能有效誘導增殖細胞和非增殖細胞死亡。

- 近年來,各相關人員之間建立了多種多樣的合作關係,這反映出人們對該市場的興趣日益濃厚。事實上,近70%的交易都是在過去三年內完成的。

- 55% 的公司正在努力擴大生產能力,以加強其服務組合,從而滿足不斷成長的需求。

- 全球ADC有效載荷的生產能力均勻分佈在全球各地的工廠。其中大部分產能(40%)位於歐洲的工廠。

- 隨著多個臨床候選藥物預計將在全球各地實現商業化,對 ADC 有效載荷製造的需求可能會大幅增加。

- 受癌症發病率上升和有效載荷化學技術進步的推動,市場正在迅速發展,但同時也面臨嚴格的監管和穩定性挑戰。

- 目前,北美在 ADC 細胞毒性有效載荷和彈頭市場中佔據最大的市場佔有率,其次是歐洲和亞太地區。

- 受美國領先企業在抗體藥物偶聯物(ADC)有效載荷和彈頭領域快速成功的推動,ADC細胞毒性有效載荷和彈頭市場預計將以6.7%的年複合成長率成長。

- 預計本會計年度北美抗體偶聯藥物(ADC)細胞毒性有效載荷和彈頭市場規模將達到1.38億美元。此外,拓樸異構酶I抑制劑在該市場中佔據主導地位,佔有率較大。

抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場

市場規模和機會分析是根據以下參數進行細分的:

產品類型

- 市售ADC

- 臨床階段抗體藥物偶聯物

有效載荷類型

- 拓樸異構酶抑制劑

- 微管蛋白抑制劑

- DNA損傷劑

- 其他

酬載/彈頭子類別

- 拓樸異構酶 I 抑制劑

- 肌苷類化合物

- 奧瑞他汀

- 其他

地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 義大利

- 英國

- 西班牙

- 亞太地區

- 中國

- 日本

- 澳洲

抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場-關鍵細分市場

臨床抗體藥物偶聯物(ADC)的發展正在推動癌症治療。

依產品類型分類,抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場可分為市售ADC和臨床級ADC。市售ADC細分市場佔據主導地位(佔90%),這主要得益於市場對其療效和安全性的日益成長的需求。此外,臨床級ADC預計將呈現更高的年複合成長率(CAGR),這意味著在預測期內將有顯著的成長機會。這一成長主要由ADC核准數量的增加以及針對多種適應症的持續研究所推動。

拓樸異構酶抑制劑正在推動抗體藥物偶聯物(ADC)細胞毒性有效載荷領域的擴張。

依有效載荷類型分類,抗體偶聯藥物(ADC)細胞毒性有效載荷和彈頭市場可細分為拓撲異構酶抑制劑、微管蛋白抑制劑、DNA損傷劑和其他類型。全球市場也根據有效載荷類型進行細分,包括微管蛋白抑制劑、拓樸異構酶抑制劑、DNA損傷劑和其他類型。今年,拓樸異構酶抑制劑細分市場佔最大佔有率(約70%)。這主要歸功於其抑制癌細胞DNA複製的重要功能,以及癌症發生率的上升、精準腫瘤學的進步和該領域研發投入的增加。

拓樸異構酶 I 抑制劑正在推動抗體藥物偶聯物 (ADC) 有效載荷產業的發展。

在有效載荷/彈頭子類別中,抗體偶聯藥物(ADC)的細胞毒性有效載荷和彈頭市場細分為拓撲異構酶I抑制劑、肌毒素類藥物、奧瑞他汀類藥物和其他藥物。根據ADC細胞毒性有效載荷和彈頭市場預測,受單株抗體、基因療法和個人化醫療等創新治療方法日益廣泛的應用推動,拓樸異構酶I抑制劑預計將在今年佔據市場主導地位(超過70%)。拓樸異構酶I抑制劑細分市場的關鍵因素包括Enhertu(曲妥珠單抗德魯替康)和Trodelvi(沙妥珠單抗戈維替康)等ADC的核准,它們分別使用了拓樸異構酶I抑制劑德魯替康(DXd)和SN-38。這些有效載荷透過抑制DNA複製和修復發揮強效抗癌作用。

區域市場趨勢

歐洲在抗體偶聯藥物(ADC)細胞毒性有效載荷和彈頭市場中處於領先地位。

從區域上看,抗體偶聯藥物(ADC)細胞毒性有效載荷和彈頭市場分為北美、歐洲和亞太地區。預計到2035年,歐洲ADC細胞毒性有效載荷/彈頭市場將保持領先地位,佔約45%的市佔率。該地區主導地位的關鍵因素包括學術機構與企業之間的緊密合作、高效化合物生產方面的先進技術能力以及積極的智慧財產權活動。

第一次調查總結

本市場報告中提出的觀點和見解也受到與主要產業相關人員討論的影響。本市場報告包含與以下相關人員的詳細訪談記錄:

- 荷蘭小規模組織創辦人兼首席科學官

- 法國,大型機構,市場總監

此外,本市場報告還包含與以下第三方進行的討論記錄:

- 義大利某大型企業研發及GMP生產負責人

- 英國領先機構、科學業務發展經理及ADC負責人

- 美國某大企業政策分析師

抗體偶聯藥物(ADC)細胞毒性有效載荷和彈頭市場中的關鍵公司範例

- Abzena

- Axplora

- CARBOGEN AMCIS

- Cerbios-Pharma

- Eisai

- GeneQuantum

- Levena Biopharma

- MabPlex

- MilliporeSigma(Merck)

- NJ Bio

- Synaffix

- WuXi STA

抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場—研究範圍

- 市場規模和機會分析:本報告詳細分析了 ADC 細胞毒性有效載荷和彈頭市場,重點關注關鍵市場細分,例如 [A] 產品、[B] 有效載荷、[C] 有效載荷/彈頭子類別和 [D] 地區。

- 市場概覽:這是對當前市場狀況的詳細概述,包括對提供 ADC 細胞毒性有效載荷和彈頭的公司進行詳細評估,評估依據包括成立年份、公司規模、總部所在地、公司結構、有效載荷類型、DNA 損傷劑類型、微管/微管蛋白抑製劑類型、拓撲異構酶抑製劑類型、業務規模和治療酶抑製劑類型等多個相關參數。

- 企業競爭分析:我們根據供應商實力(從經驗年限和公司規模來看)、產品組合實力(從DNA損傷劑、微管/微管蛋白抑制劑、拓樸異構酶抑制劑、蛋白激酶抑制劑和其他有效載荷的數量以及治療領域類型來看)和業務規模,對關鍵地區的ADC細胞毒性有效載荷和彈頭供應商進行深入的企業競爭分析。

- 公司簡介:詳細介紹北美、歐洲和亞太地區從事胜肽類藥物生產市場的領先公司,依據包括[A]成立年份、[B]總部所在地、[C]ADC細胞毒性有效載荷和彈頭組合、[D]近期發展、以及[E]未來展望。

- 合作關係與合作研究:我們根據多個參數分析該行業相關人員之間建立的合作關係,包括[A] 合作年份,[B] 合作類型,[C] 產品類型,[D] 合作夥伴類型,以及[E] 最活躍的公司。

- 近期業務擴張:我們分析了每家公司近期旨在增強其與 ADC 細胞毒性有效載荷和彈頭相關的能力的近期業務擴張,分析依據包括 [A] 擴張年份,[B] 擴張類型(建立新設施、擴建設施、擴大生產能力),以及 [C] 擴張的地理位置。

- 需求分析:這是根據全球基因治療年度需求資訊所做的估計,其中考慮了各種估計值,例如目標患者群體、給藥頻率和劑量,以及評估市售 ADC 細胞毒性有效載荷和彈頭的臨床試驗。

- 生產能力分析:根據公開資訊和一手、二手調查的結果,本分析估算了業內各公司 ADC 細胞毒性有效載荷和彈頭的總生產能力。

- 市場影響分析:本報告詳細分析了可能影響抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場成長的因素,包括[A]關鍵促進因素、[B]潛在阻礙因素、[C]新興機會和[D]現有挑戰的識別和分析。

目錄

第1章:序言

第2章:調查方法

第3章 市場動態

第4章 宏觀經濟指標

第5章執行摘要

- 執行摘要:市場狀況

- 執行摘要:市場趨勢

- 執行摘要:市場預測與機會分析

第6章:引言

- 章節概要

- 抗體藥物複合體(ADC)概述

- ADC的關鍵組成部分

- 攜帶細胞毒性物質

- ADC製造的關鍵步驟

- 與ADC製造相關的技術挑戰

- 對ADC有效載荷/彈頭進行契約製造的需求

- 選擇合適的CD生產夥伴的指導原則

- 細胞毒性藥物生產中的監管考量

- 未來展望

第7章 市場概況:ADC(抗藥物抗體)細胞毒性有效載荷和彈頭供應商

- 章節概要

- 抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭供應商:市場狀況

第8章:企業競爭力分析:抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭供應商

- 章節概要

- 前提條件和關鍵參數

- 調查方法

- 企業競爭力分析:抗體藥物複合體物(ADC)細胞毒性有效載荷和彈頭供應商

- 北美洲

- 歐洲

- 亞太地區

第9章 公司簡介:ADC細胞毒性有效載荷和彈頭市場的主要參與者

- 章節概要

- CARBOGEN AMCIS

- Cerbios-Pharma

- Levena Biopharma

- MabPlex

- MilliporeSigma

- WuXi STA

第10章 公司簡介:ADC細胞毒性有效載荷和彈頭市場的其他主要參與者

- 章節概要

- Abzena

- Axplora

- Eisai

- GeneQuantum

- NJ Bio

- Synaffix

第11章夥伴關係與合作

- 章節概要

- 夥伴關係模式

- 抗體藥物複合體物(ADC)細胞毒性有效載荷和彈頭:夥伴關係與合作

第12章 近期擴張

- 章節概要

- 抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭:近期擴展

第13章 能力分析:ADC細胞毒性酬載與彈頭的製造

第14章 需求分析:ADC細胞毒性酬載與彈頭供應商

第15章 市場影響分析

- 市場促進因素

- 市場限制

- 市場機遇

- 市場挑戰

第16章:全球抗體偶聯藥物(ADC)細胞毒性有效載荷和彈頭市場

第17章:ADC細胞毒性有效載荷與彈頭市場(依產品類型分類)

第18章:ADC細胞毒性有效載荷和彈頭市場(按有效載荷類型分類)

第19章:ADC細胞毒性有效載荷和彈頭市場(按有效載荷/彈頭子類別分類)

第20章:ADC細胞毒性有效載荷和彈頭市場(按地區分類)

第21章 市場機會分析:北美

第22章 市場機會分析:歐洲

第23章 市場機會分析:亞太地區

第24章 結論

第25章:高階主管洞察

第26章附錄1:表格形式數據

第27章 附錄2:公司與組織列表

第26章附錄1:表格形式數據

第27章 附錄2:公司與組織列表

ADC Cytotoxic Payloads and Warheads Market: Overview

As per Roots Analysis, the ADC cytotoxic payloads and warheads market is estimated to grow from USD 381.3 million in the current year to USD 469.3 million by 2035, at a CAGR of 8.9% during the forecast period, till 2035.

ADC Cytotoxic Payloads and Warheads Market: Growth and Trends

Antibody-drug conjugate (ADC) cytotoxic agents and warheads are essential elements in contemporary targeted cancer treatments, developed to provide highly effective compounds accurately while reducing overall toxicity. Through the incorporation of chemical optimization and advanced linker systems, these payloads improve the therapeutic efficacy of ADCs, allowing pharmaceutical firms to develop more efficient and targeted cancer therapies.

The ADC payloads field is growing swiftly by utilizing advancements in payload chemistry, conjugation techniques, and linker technologies to enhance safety and efficacy profiles. Nonetheless, the industry still faces difficulties in large-scale ADC production, selecting payloads, and balancing drug-to-antibody ratios, as well as adhering to strict regulatory and quality standards for clinical use.

Obtaining cost-effectiveness and developing standardized characterization methods continue to be major challenges for broad implementation. Nonetheless, the rising uses in solid tumors and blood cancers, along with increasing investments in precision oncology, are driving market expansion.

Growth Drivers: Strategic Enablers of Market Expansion

Continuous improvements in linker stability, payload effectiveness, and targeted delivery systems are boosting the therapeutic index of ADCs. These advancements enable researchers to enhance tumor-eradicating effectiveness while reducing harm to healthy tissues. This precision method is driving innovative strategies in oncology for managing both blood cancers and solid tumors.

Moreover, the increasing requirement for next-generation payload categories, including DNA-damaging compounds and microtubule inhibitors, is prompting significant progress within the biopharmaceutical sector. The sector for ADC payloads and warheads is witnessing rapid market expansion due to increased investment in targeted cancer therapies and the ongoing advancement of conjugation technologies. Additionally, the advancement of next-generation multi-warhead antibody-drug conjugates (ADCs) is likely to greatly enhance market expansion by addressing shortcomings of existing ADC treatments. Comapnies such as Araris Biotech have developed unique peptide linker technology that allows for the attachment of two or three different cytotoxic agents or warheads to a single antibody in a single-step process without requiring antibody modification.

Market Challenges: Critical Barriers Impeding Progress

The ADC cytotoxic payloads and warheads market faces challenges related to the limited availability of highly potent and selective payloads that can effectively target cancer cells while minimizing off-target toxicity. Complex manufacturing processes, stringent regulatory requirements, and supply chain constraints for specialized payload components increase development costs and timelines. Additionally, concerns regarding payload stability, linker compatibility, and resistance mechanisms can impact therapeutic efficacy. Intellectual property barriers and the need for continuous innovation further intensify competitive pressures within the market.

ADC Cytotoxic Payloads and Warheads Market: Key Insights

The report delves into the current state of the ADC cytotoxic payloads and warheads market and identifies potential growth opportunities within industry. Some key findings from the report include:

- The current market landscape features a presence of close to 70 providers that claim to offer broad range of payloads, which are being used or tested across various therapeutic areas.

- Around 25% companies offer both pyrrolobenzodiazepine and auristatin payloads, owing to their exceptional potency and demonstrated ability to induce effective cell death in both dividing and non-dividing cells.

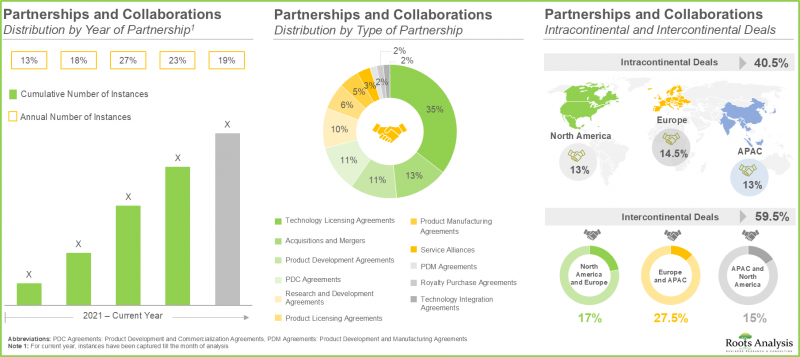

- The rising interest in this market is reflected in the diverse partnerships established among various stakeholders in the recent past; in fact, close to 70% of deals were inked in the last three years.

- 55% of the companies have undertaken capacity expansion initiatives to strengthen their service portfolio in order to keep pace with the growing demand.

- The global installed ADC payload manufacturing capacity is well distributed across different facilities worldwide; majority (40%) of this capacity is installed in facilities located in Europe.

- The demand for ADC payload manufacturing is likely to increase significantly as several clinical candidates are expected to be commercialized across various regions of the globe.

- Fueled by rising cancer prevalence and advancements in payload chemistry, the market is rapidly evolving while also contending with stringent regulations and stability challenges.

- Currently, North America captures the largest share within the ADC cytotoxic payloads and warheads market, followed by Europe and Asia-Pacific.

- Driven by the rapid success of ADC payloads and warheads by prominent players in the US, the ADC cytotoxic payloads and warheads market is expected to grow at CAGR of 6.7%.

- The ADC cytotoxic payloads and warheads market in North America is expected to be worth USD 138 million in the current year; further, within this market, topoisomerase I inhibitors dominates by capturing the majority share.

ADC Cytotoxic Payloads and Warheads Market

The market sizing and opportunity analysis has been segmented across the following parameters:

Type of Product

- Commercialized ADCs

- Clinical ADCs

Type of Payload

- Topoisomerase Inhibitors

- Tubulin Inhibitors

- DNA Damaging Agents

- Others

Sub-Category of Payload / Warhead

- Topoisomerase I inhibitors

- Maytansinoid

- Auristatin

- Others

Geographical Regions

- North America

- US

- Canada

- Europe

- Germany

- France

- Italy

- UK

- Spain

- Asia-Pacific

- China

- Japan

- Australia

ADC Cytotoxic Payloads and Warheads Market: Key Segments

Growth of Clinical ADCs is Propelling Cancer Treatment

In terms of type of product, the ADC cytotoxic payloads and warheads market is segmented across commercialized and clinical ADCs. The commercial ADCs sub-segment leads the market (90%), fueled by rising demand for marketed ADCs due to their effectiveness and safety characteristics. Additionally, clinical ADCs are expected to experience a greater CAGR, indicating significant growth opportunities throughout the forecast timeframe. This expansion results from the rising approval of ADCs and their continuous investigation across various target indications.

Topoisomerase Inhibitors Propel Expansion in ADC Cytotoxic Payload Sector

In terms of type of payload, the ADC cytotoxic payloads and warheads market is segmented across topoisomerase inhibitors, tubulin inhibitors, DNA damaging agents and others. The global market is segmented across different types of payloads, such as tubulin inhibitors, topoisomerase inhibitors, DNA damaging agents, and others. The topoisomerase inhibitors sub-segment holds the largest share (~70%) this year. This stems from their crucial function in interfering with DNA replication in cancer cells, combined with the increasing incidence of cancer, progress in precision oncology, and heightened investments in research and development in this field.

Topoisomerase I Inhibitors Leads the ADC Payload Industry

In terms of sub-category of payload / warhead, the ADC cytotoxic payloads and warheads market is segmented across topoisomerase I inhibitors, maytansinoid, auristatin and others. As per the ADC cytotoxic payloads and warheads market forecast, the growing use of innovative treatments, such as monoclonal antibodies, gene therapies, and personalized medicine, is expected to enable topoisomerase I inhibitors to lead (>70%) the market in the current year. A key factor in the topoisomerase I inhibitor sub-segment is the approval of ADCs like Enhertu (trastuzumab deruxtecan) and Trodelvy (sacituzumab govitecan), which utilize TOP1 inhibitors deruxtecan (DXd) and SN-38, respectively. These payloads serve as powerful anti-cancer agents by disrupting DNA replication and repair.

Market Regional Insights

Europe Dominates the ADC Cytotoxic Payloads and Warheads Market

In terms of geography, the ADC cytotoxic payloads and warheads market is segmented across North America, Europe and Asia-Pacific. By 2035, the market for ADC cytotoxic payloads / warheads in Europe is expected to lead, holding approximately 45% of the market share. Crucial factors that contribute to the dominance of the region include strong collaborations between academic institutions and businesses, advanced manufacturing abilities for effective compounds, and extensive activity in intellectual property.

Primary Research Overview

The opinions and insights presented in the market report were also influenced by discussions held with senior stakeholders in the industry. The market report includes detailed transcripts of interviews conducted with the following individuals:

- Founder and Chief Scientific Officer, Small Organization, Netherlands

- Market Director, Large Organization, France

In addition, the market report includes transcripts of the following other third-party discussions:

- Head of Development and GMP Manufacturing, Large Organization, Italy

- Scientific business development manager and ADC lead, Large Organization, United Kingdom

- Policy Analyst, Very Large Organization, United States

Example Players in ADC Cytotoxic Payloads and Warheads Market

- Abzena

- Axplora

- CARBOGEN AMCIS

- Cerbios-Pharma

- Eisai

- GeneQuantum

- Levena Biopharma

- MabPlex

- MilliporeSigma (Merck)

- NJ Bio

- Synaffix

- WuXi STA

ADC Cytotoxic Payloads and Warheads Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the ADC cytotoxic payloads and warheads market, focusing on key market segments, including [A] product, [B] payload, [C] sub-category of payload / warhead, and [D] geographical regions.

- Market Landscape: A detailed overview of the current market landscape of detailed assessment of companies offering ADC cytotoxic payloads and warheads, based on several relevant parameters, including year of establishment, company size, location of the headquarters, type of company, type of payload, type of DNA damaging agents, type of microtubule / tubulin inhibitors, type of topoisomerase inhibitors, scale of operation and type of therapeutic area.

- Company Competitiveness Analysis: An insightful company competitiveness analysis of ADC cytotoxic payloads and warheads providers (across key geographical regions), based on supplier strength (in terms of years of experience and company size), and portfolio strength (in terms of number of DNA damaging agents, microtubule / tubulin inhibitors, topoisomerase inhibitors, protein kinase inhibitors, other payloads, and type of therapeutic area) and scale of operation.

- Company Profiles: In-depth profiles of prominent players North America, Europe and Asia-Pacific that are engaged in the peptide therapeutics manufacturing market based on [A] year of establishment, [B] location of headquarters, [C] ADC cytotoxic payloads and warheads portfolio, [D] recent developments and [E] an informed future outlook.

- Partnerships and Collaborations: An analysis of the partnerships inked between stakeholders engaged in this industry, based on several parameters, such as [A] year of partnership, [B] type of partnership, [C] type of product, [D] type of partner and [E] most active players.

- Recent Expansions: An analysis of the recent expansions undertaken by various companies in order to augment their respective capabilities related to ADC cytotoxic payloads and warheads, based on several parameters, such as [A] year of expansion, [B] type of expansion (new facility establishment, facility expansion, and capacity expansion), and [C] geographical location of the expansion.

- Demand Analysis: an informed estimate of the global annual demand for gene therapies, taking into account the marketed ADC cytotoxic payloads and warheads and clinical trials evaluating ADC cytotoxic payloads and warheads, based on various parameters, such as target patient population, dosing frequency and dose strength.

- Capacity Analysis: an estimate of the overall, installed ADC cytotoxic payloads and warheads manufacturing capacity of industry players based on the information available in the public domain, and insights generated from both secondary and primary research.

- Market Impact Analysis: An in-depth analysis of the factors that can impact the growth of ADC cytotoxic payloads and warheads market. It also features identification and analysis of [A] key drivers, [B] potential restraints, [C] emerging opportunities, and [D] existing challenges.

Key Questions Answered in this Report

- Which are the leading companies in the ADC cytotoxic payloads and warheads market?

- Which region dominates the ADC cytotoxic payloads and warheads market?

- What are the key trends observed in the ADC cytotoxic payloads and warheads market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by ADC cytotoxic payloads and warheads developers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

- 5.1. Executive Summary: Market Landscape

- 5.2. Executive Summary: Market Trends

- 5.3. Executive Summary: Market Forecast and Opportunity Analysis

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Antibody Drug Conjugate (ADC)

- 6.3. Key Components of ADCs

- 6.4. Cytotoxin Payloads

- 6.5. Key Steps in ADC Manufacturing

- 6.6. Technical Challenges Associated with ADC Manufacturing

- 6.7. Need for Contract Manufacturing of ADC Payloads / Warheads

- 6.8. Guidelines for Selecting a Suitable Partner for Manufacturing CD

- 6.9. Regulatory Considerations for Cytotoxic Drugs Manufacturing

- 6.10. Future Outlook

7. MARKET LANDSCAPE: ADC CYTOTOXIC PAYLOAD AND WARHEAD PROVIDERS

- 7.1. Chapter Overview

- 7.2. ADC Cytotoxic Payload and Warhead Providers: Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters (Region)

- 7.2.4. Analysis by Location of Headquarters (Country)

- 7.2.5. Analysis by Location of Facilities

- 7.2.6. Analysis by Type of Company

- 7.2.7. Analysis by Type of DNA Damaging Agent

- 7.2.8. Analysis by Type of Microtubule / Tubulin Inhibitors

- 7.2.9. Analysis by Type of Topoisomerase Inhibitors

- 7.2.10. Analysis by Scale of Operation

- 7.2.11. Analysis by Type of Therapeutic Area

8. COMPANY COMPETITIVENESS ANALYSIS: ADC CYTOTOXIC PAYLOADS AND WARHEADS PROVIDERS

- 8.1. Chapter Overview

- 8.2. Assumptions and Key Parameters

- 8.3. Methodology

- 8.4. Company Competitiveness Analysis: ADC Cytotoxic Payloads and Warheads Providers

- 8.4.1. ADC Cytotoxic Payloads and Warheads Providers based in North America

- 8.4.2. ADC Cytotoxic Payloads and Warheads Providers based in Europe

- 8.4.3. ADC Cytotoxic Payloads and Warheads Providers based in Asia-Pacific

9. COMPANY PROFILES: LEADING PLAYERS IN THE ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET

- 9.1. Chapter Overview

- 9.2. CARBOGEN AMCIS

- 9.2.1. Company Overview

- 9.2.2. Financial Information

- 9.2.3. Recent Developments and Future Outlook

- 9.3. Cerbios-Pharma

- 9.3.1. Company Overview

- 9.3.2. Recent Developments and Future Outlook

- 9.4. Levena Biopharma

- 9.4.1. Company Overview

- 9.4.2. Recent Developments and Future Outlook

- 9.5. MabPlex

- 9.5.1. Company Overview

- 9.5.2. Recent Developments and Future Outlook

- 9.6. MilliporeSigma

- 9.6.1. Company Overview

- 9.6.2. Financial Information

- 9.6.3. Recent Developments and Future Outlook

- 9.7. WuXi STA

- 9.7.1. Company Overview

- 9.7.2. Financial Information

- 9.7.3. Recent Developments and Future Outlook

10. COMPANY PROFILES: OTHER LEADING PLAYERS IN THE ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET

- 10.1. Chapter Overview

- 10.2. Abzena

- 10.2.1. Company Overview

- 10.3. Axplora

- 10.3.1. Company Overview

- 10.4. Eisai

- 10.4.1. Company Overview

- 10.5. GeneQuantum

- 10.5.1. Company Overview

- 10.6. NJ Bio

- 10.6.1. Company Overview

- 10.7. Synaffix

- 10.7.1. Company Overview

11. PARTNERSHIPS AND COLLABORATIONS

- 11.1. Chapter Overview

- 11.2. Partnership Models

- 11.3. ADC Cytotoxic Payloads and Warheads: Partnerships and Collaborations

- 11.3.1. Analysis by Year of Partnership

- 11.3.2. Analysis by Type of Partnership

- 11.3.3. Analysis by Year and Type of Partnership

- 11.3.4. Analysis by Type of Partner

- 11.3.5. Most Active Players: Analysis by Number of Partnerships

- 11.3.6. Analysis by Geography

- 11.3.6.1. Analysis by Country

- 11.3.6.2. Analysis by Continent

12. RECENT EXPANSIONS

- 12.1. Chapter Overview

- 12.2. ADC Cytotoxic Payloads and Warheads: Recent Expansions

- 12.2.1. Analysis by Year of Expansion

- 12.2.2. Analysis by Type of Expansion

- 12.2.3. Analysis by Year and Type of Expansion

- 12.2.4. Most Active Players: Analysis by Number of Recent Expansions

- 12.2.5. Analysis by Location of Expansion

- 12.2.5.1. Analysis by Country

- 12.2.5.2. Analysis by Continent

13. CAPACITY ANALYSIS: ADC CYTOTOXIC PAYLOADS AND WARHEADS MANUFACTURING

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.2.1. Analysis by Range of Installed Capacity

- 13.2.2. Analysis by Scale of Operation

- 13.2.3. Analysis by Location of ADC Cytotoxic Payloads and Warheads Facility

14. DEMAND ANALYSIS: ADC CYTOTOXIC PAYLOADS AND WARHEADS PROVIDERS

- 14.1. Chapter Overview

- 14.2. Demand Drivers

- 14.3. Key Assumptions and Methodology

- 14.4. Global Annual Demand for ADC Payloads

- 14.4.1. Global Clinical Demand for ADC Payloads

- 14.4.1.1. Analysis by Type of Payload

- 14.4.1.2. Analysis by Phase of Development

- 14.4.2. Global Commercial Demand for ADC Payloads

- 14.4.1.1. Analysis by Payload

- 14.4.1.2. Analysis by Type of Payload

- 14.4.1.2. Analysis by Therapeutic Area

- 14.4.1.3. Analysis by Geographical Regions

- 14.4.1. Global Clinical Demand for ADC Payloads

15. MARKET IMPACT ANALYSIS

- 15.1. Market Drivers

- 15.2. Market Restraints

- 15.3. Market Opportunities

- 15.4. Market Challenges

16. GLOBAL ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET

- 16.1. Chapter Overview

- 16.2. Assumptions and Methodology

- 16.3. Global ADC Cytotoxic Payloads and Warheads Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 16.3.1. Scenario Analysis

- 16.3.1.1. Conservative Scenario

- 16.3.1.2. Optimistic Scenario

- 16.3.1. Scenario Analysis

- 16.4. Key Market Segmentations

17. ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET, BY TYPE OF PRODUCT

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Product

- 17.3.1. Commercialized ADC Cytotoxic Payloads and Warheads Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 17.3.2. Clinical ADC Cytotoxic Payloads and Warheads Market ADCs, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

18. ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET, BY TYPE OF PAYLOAD

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Payload

- 18.3.1. ADC Cytotoxic Payloads and Warheads Market for Tubulin inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.3.2. ADC Cytotoxic Payloads and Warheads Market for Topoisomerase Inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.3.3. ADC Cytotoxic Payloads and Warheads Market for DNA Damaging Agents, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 18.3.4. ADC Cytotoxic Payloads and Warheads Market for Others, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

19. ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET, BY SUB-CATEGORY OF PAYLOAD / WARHEAD

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. ADC Cytotoxic Payloads and Warheads Market: Distribution by Sub-Categories of Payload / Warhead

- 19.3.1. ADC Cytotoxic Payloads and Warheads Market for Topoisomerase I inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.3.2. ADC Cytotoxic Payloads and Warheads Market for Maytansinoid, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.3.3. ADC Cytotoxic Payloads and Warheads Market for Auristatin, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 19.3.4. ADC Cytotoxic Payloads and Warheads Market for Others, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

20. ADC CYTOTOXIC PAYLOADS AND WARHEADS MARKET, BY GEOGRAPHICAL REGIONS

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. ADC Cytotoxic Payloads and Warheads Market: Distribution by Geographical Regions

- 20.3.1. ADC Cytotoxic Payloads and Warheads Market in North America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.1.1. ADC Cytotoxic Payloads and Warheads Market in the US, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.1.2. ADC Cytotoxic Payloads and Warheads Market in Canada, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2. ADC Cytotoxic Payloads and Warheads Market in Europe, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.1. ADC Cytotoxic Payloads and Warheads Market in Germany, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.2. ADC Cytotoxic Payloads and Warheads Market in the UK, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.3. ADC Cytotoxic Payloads and Warheads Market in France, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.4. ADC Cytotoxic Payloads and Warheads Market in Italy, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.2.5. ADC Cytotoxic Payloads and Warheads Market in Spain, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.3. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.3.1. ADC Cytotoxic Payloads and Warheads Market in China, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.3.2. ADC Cytotoxic Payloads and Warheads Market in Japan, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.3.4. ADC Cytotoxic Payloads and Warheads Market in Australia, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

- 20.3.1. ADC Cytotoxic Payloads and Warheads Market in North America, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035)

21. MARKET OPPORTUNITY ANALYSIS: NORTH AMERICA

- 21.1. ADC Cytotoxic Payloads and Warheads Market in North America: Distribution by Type of Product

- 21.1.1. ADC Cytotoxic Payloads and Warheads Market in North America for Clinical Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.1.2. ADC Cytotoxic Payloads and Warheads Market in North America for Commercial Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.2. ADC Cytotoxic Payloads and Warheads Market in North America: Distribution by Type of Payload

- 21.2.1. ADC Cytotoxic Payloads and Warheads Market in North America for Tubulin inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.2.2. ADC Cytotoxic Payloads and Warheads Market in North America for Topoisomerase Inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.2.3. ADC Cytotoxic Payloads and Warheads Market in North America for DNA Damaging Agents, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.2.4. ADC Cytotoxic Payloads and Warheads Market in North America for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.3. ADC Cytotoxic Payloads and Warheads Market in North America: Distribution by Type of Payload / Warhead

- 21.3.1. ADC Cytotoxic Payloads and Warheads Market in North America for Topoisomerase I inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.3.2. ADC Cytotoxic Payloads and Warheads Market in North America for Maytansinoid, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.3.3. ADC Cytotoxic Payloads and Warheads Market in North America for Auristatin, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 21.3.4. ADC Cytotoxic Payloads and Warheads Market in North America for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

22. MARKET OPPORTUNITY ANALYSIS: EUROPE

- 22.1. ADC Cytotoxic Payloads and Warheads Market in Europe: Distribution by Type of Product

- 22.1.1. ADC Cytotoxic Payloads and Warheads Market in Europe for Clinical Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.1.2. ADC Cytotoxic Payloads and Warheads Market in Europe for Commercial Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.2. ADC Cytotoxic Payloads and Warheads Market in Europe: Distribution by Type of Payload

- 22.2.1. ADC Cytotoxic Payloads and Warheads Market in Europe for Tubulin inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.2.2. ADC Cytotoxic Payloads and Warheads Market in Europe for Topoisomerase Inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.2.3. ADC Cytotoxic Payloads and Warheads Market in Europe for DNA Damaging Agents, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.2.4. ADC Cytotoxic Payloads and Warheads Market in Europe for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.3. ADC Cytotoxic Payloads and Warheads Market in Europe: Distribution by Type of Payload / Warhead

- 22.3.1. ADC Cytotoxic Payloads and Warheads Market in Europe for Topoisomerase I inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.3.2. ADC Cytotoxic Payloads and Warheads Market in Europe for Maytansinoid, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.3.3. ADC Cytotoxic Payloads and Warheads Market in Europe for Auristatin, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 22.3.4. ADC Cytotoxic Payloads and Warheads Market in Europe for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

23. MARKET OPPORTUNITY ANALYSIS: ASIA-PACIFIC

- 23.1. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific: Distribution by Type of Product

- 23.1.1. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Clinical Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.1.2. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Commercial Product, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.2. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific: Distribution by Type of Payload

- 23.2.1. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Tubulin inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.2.2. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Topoisomerase Inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.2.3. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for DNA Damaging Agents, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.2.4. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.3. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific: Distribution by Type of Payload / Warhead

- 23.3.1. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Topoisomerase I inhibitors, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.3.2. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Maytansinoid, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.3.3. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Auristatin, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- 23.3.4. ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific for Others, Historical Trends (since 2023) and Forecasted Estimates (till 2035)

- *Detailed information on Chapter 21 to 23 is available in the Excel Data Packs shared along with the report**

24. CONCLUDING REMARKS

25. EXECUTIVE INSIGHTS

- 25.1 Chapter Overview

- 25.2. Company A (Mid-sized company, Netherlands)

- 25.2.1. Company Snapshot

- 25.2.2. Interview Transcript: Founder and Chief Scientific Officer

- 25.3. Company B (Small Company, US)

- 25.3.1. Company Snapshot

- 25.3.2. Interview Transcript: Founder and Chief Executive Officer

- 25.4. Company C (Small Company, France)

- 25.4.1. Company Snapshot

- 25.4.2. Interview Transcript: Co-founder and Chief Executive Officer

- 25.5. Company D (Large Company, Italy)

- 25.5.1. Company Snapshot

- 25.5.2. Interview Transcript: Chief Executive Officer and Technical Business Development Manager

- 25.6. Company E (Large Company, South Korea)

- 25.6.1. Company Snapshot

- 25.6.2. Interview Transcript: Chief Business Officer

26. APPENDIX 1: TABULATED DATA

27. APPENDIX 2: LIST OF COMPANIES AND ORGANIZATION

- 25.7. Company F (Large Company, Japan)

- 25.7.1. Company Snapshot

- 25.7.2. Interview Transcript: Executive Director and Chief Innovation Officer

- 25.8. Company G (Small Company, Netherlands)

- 25.8.1. Company Snapshot

- 25.8.2. Interview Transcript: Director, Business Development

- 25.9. Company H (Large Company, France)

- 25.9.1. Company Snapshot

- 25.9.2. Interview Transcript: Market Director

- 25.10. Company I (Small Company, Netherlands)

- 25.10.1. Company Snapshot

- 25.10.2. Interview Transcript: Vice President, Business Development

- 25.11. Company J (Mid-sized Company, Switzerland)

- 25.11.1. Company Snapshot

- 25.11.2. Interview Transcript: Business Development Manager

- 25.12. Company K (Mid-sized Company, UK)

- 25.12.1. Company Snapshot

- 25.12.2. Interview Transcript: Former Chief Executive Officer

- 25.13. Company L (Small Company, Switzerland)

- 25.13.1. Company Snapshot

- 25.13.2. Interview Transcript: Former Chief Business Officer

26. APPENDIX 1: TABULATED DATA

27. APPENDIX 2: LIST OF COMPANIES AND ORGANIZATIONS

List of Tables

- Table 7.1 List of ADC Cytotoxic Payloads and Warheads Providers

- Table 7.2 ADC Cytotoxic Payload and Warhead Providers: Information on Product Portfolio

- Table 11.1 List of Partnerships and Collaborations, Since 2021

- Table 12.1 List of Recent Expansions, Since 2020

- Table 13.1 Sample Dataset: Information on Service Providers Installed Capacity

- Table 23.1 ADC Cytotoxic Payload and Warhead Providers: Distribution by Year of Establishment

- Table 23.2 ADC Cytotoxic Payload and Warhead Providers: Distribution by Company Size

- Table 23.3 ADC Cytotoxic Payload and Warhead Providers: Distribution by Location of Headquarters (Region)

- Table 23.4 ADC Cytotoxic Payload and Warhead Providers: Distribution by Location of Headquarters (Country)

- Table 23.5 ADC Cytotoxic Payload and Warhead Providers: Distribution by Location of Manufacturing Facilities

- Table 23.6 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of Company

- Table 23.7 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of DNA Damaging Agent

- Table 23.8 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of Microtubule / Tubulin Inhibitors

- Table 23.9 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of Topoisomerase Inhibitors

- Table 23.10 ADC Cytotoxic Payload and Warhead Providers: Distribution by Scale of Operation

- Table 23.11 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of Therapeutic Area

- Table 23.12 Company Competitiveness Analysis: ADC Cytotoxic Payloads and Warheads Providers based in North America

- Table 23.13 Company Competitiveness Analysis: ADC Cytotoxic Payloads and Warheads Providers based in Europe

- Table 23.14 Company Competitiveness Analysis: ADC Cytotoxic Payloads and Warheads Providers based in Asia-Pacific

- Table 23.15 CARBOGEN AMCIS: Annual Revenues, Consolidated Financial Details, Since FY 2022 (INR Billion)

- Table 23.16 Merck: Annual Revenues, Consolidated Financial Details, Since FY 2022 (EUR Million)

- Table 23.17 WuXi AppTec: Annual Revenues, Consolidated Financial Details, Since FY 2022 (RMB Billion)

- Table 23.18 Partnerships and Collaborations: Cumulative Year-wise Trend, Since Pre-2021

- Table 23.19 Partnerships and Collaborations: Distribution by Type of Partnership

- Table 23.20 Partnerships and Collaborations: Distribution by Year and Type of Partnership, Since 2021

- Table 23.21 Partnerships and Collaborations: Distribution by Type of Partner

- Table 23.22 Most Active Players: Distribution by Number of Partnerships

- Table 23.23 Partnerships and Collaborations: Local and International Agreements

- Table 23.24 Partnerships and Collaborations: Intracontinental and Intercontinental Agreements

- Table 23.25 Recent Expansions: Cumulative Year-wise Trend, Since 2020

- Table 23.26 Recent Expansions: Distribution by Type of Expansion

- Table 23.27 Recent Expansions: Distribution by Year and Type of Expansion, Since 2020

- Table 23.28 Recent Expansions: Distribution by Location of Expansion (Country)

- Table 23.29 Recent Expansions: Distribution by Location of Expansion (Continent)

- Table 23.30 Most Active Players: Distribution by Number of Expansions

- Table 23.31 Global Installed ADC Cytotoxic Payloads and Warheads Manufacturing Capacity: Distribution by Range of Installed Capacity (in Liters)

- Table 23.32 Global Installed ADC Cytotoxic Payloads and Warheads Manufacturing Capacity: Distribution by Scale of Operation

- Table 23.33 Global Installed ADC Cytotoxic Payloads and Warheads Manufacturing Capacity: Distribution by Location of ADC Cytotoxic Payloads and Warheads Manufacturing Facility

- Table 23.34 Global Annual Demand for ADC Payloads (in Kg), Till 2035

- Table 23.35 Global Clinical Demand for ADC Payloads, Till 2035 (in KGs)

- Table 23.36 Global Commercial Demand for ADC Payloads, Till 2035 (in KGs)

- Table 23.37 Clinical Demand Analysis: Distribution by Type of Payload, Current Year and 2035

- Table 23.38 Clinical Demand Analysis: Distribution by Type of Payload, Till 2035

- Table 23.39 Clinical Demand Analysis: Distribution by Type of Phase of Development, Current Year and 2035

- Table 23.40 Clinical Demand Analysis: Distribution by Type of Phase of Development, Till 2035

- Table 23.41 Commercial Demand Analysis: Distribution by Payload, Till 2035

- Table 23.42 Commercia Demand Analysis: Distribution by Type of Payload, Till 2035

- Table 23.43 Commercia Demand Analysis: Distribution by Therapeutic Area, Till 2035

- Table 23.44 Commercia Demand Analysis: Distribution by Geographical Regions, Current Year and 2035

- Table 23.45 Commercia Demand Analysis: Distribution by Geographical Regions, Till 2035

- Table 23.46 ADC Cytotoxic Payloads and Warheads Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.47 ADC Cytotoxic Payloads and Warheads Market, Forecasted Estimates (Till 2035): Conservative Scenario (USD Million)

- Table 23.48 ADC Cytotoxic Payloads and Warheads Market, Forecasted Estimates (Till 2035): Optimistic Scenario (USD Million)

- Table 23.49 ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Product, Current Year, 2030 and 2035

- Table 23.50 ADC Cytotoxic Payloads and Warheads Market for Clinical Product, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.51 ADC Cytotoxic Payloads and Warheads Market for Commercial Product, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.52 ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Payload, Current Year, 2030 and 2035

- Table 23.53 ADC Cytotoxic Payloads and Warheads Market for Tubulin inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.54 ADC Cytotoxic Payloads and Warheads Market for Topoisomerase Inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.55 ADC Cytotoxic Payloads and Warheads Market for DNA Damaging Agents, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.56 ADC Cytotoxic Payloads and Warheads Market for Others, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.57 ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Payload / Warhead, Current Year, 2030 and 2035

- Table 23.58 ADC Cytotoxic Payloads and Warheads Market for Topoisomerase I inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.59 ADC Cytotoxic Payloads and Warheads Market for Maytansinoid, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.60 ADC Cytotoxic Payloads and Warheads Market for Auristatin, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.61 ADC Cytotoxic Payloads and Warheads Market for Others, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.62 ADC Cytotoxic Payloads and Warheads Market: Distribution by Geographical Regions, Current Year, 2030 and 2035

- Table 23.63 ADC Cytotoxic Payloads and Warheads Market in North America: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.64 ADC Cytotoxic Payloads and Warheads Market in the US: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.65 ADC Cytotoxic Payloads and Warheads Market in Canada: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.66 ADC Cytotoxic Payloads and Warheads Market in Europe: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.67 ADC Cytotoxic Payloads and Warheads Market in Germany: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.68 ADC Cytotoxic Payloads and Warheads Market in the UK: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.69 ADC Cytotoxic Payloads and Warheads Market in France: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.70 ADC Cytotoxic Payloads and Warheads Market in Italy: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.71 ADC Cytotoxic Payloads and Warheads Market in Spain: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.72 ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.73 ADC Cytotoxic Payloads and Warheads Market in China: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.74 ADC Cytotoxic Payloads and Warheads Market in Japan: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Table 23.75 ADC Cytotoxic Payloads and Warheads Market in Australia: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

List of Figures

- Figure 2.1 Research Methodology: Project Methodology

- Figure 2.2 Research Methodology: Data Sources for Secondary Research

- Figure 2.3 Research Methodology: Robust Quality Control

- Figure 3.1 Market Dynamics: Forecast Methodology

- Figure 3.2 Market Dynamics: Market Assessment Framework

- Figure 4.1 Lessons Learnt from Past Recessions

- Figure 5.1 Executive Summary: Market Landscape

- Figure 5.2 Executive Summary: Market Trends

- Figure 5.3 Executive Summary: Market Sizing and Opportunity Analysis

- Figure 6.1 Key Components of ADCs

- Figure 7.1 ADC Cytotoxic Payload and Warhead Providers: Distribution by Year of Establishment

- Figure 7.2 ADC Cytotoxic Payload and Warhead Providers: Distribution by Company Size

- Figure 7.3 ADC Cytotoxic Payload and Warhead Providers: Distribution by Location of Headquarters (Region)

- Figure 7.4 ADC Cytotoxic Payload and Warhead Providers: Distribution by Location of Headquarters (Country)

- Figure 7.5 ADC Cytotoxic Payload and Warhead Providers: Distribution by Location of Manufacturing Facilities

- Figure 7.6 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of Company

- Figure 7.7 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of DNA Damaging Agent

- Figure 7.8 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of Microtubule / Tubulin Inhibitors

- Figure 7.9 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of Topoisomerase Inhibitors

- Figure 7.10 ADC Cytotoxic Payload and Warhead Providers: Distribution by Scale of Operation

- Figure 7.11 ADC Cytotoxic Payload and Warhead Providers: Distribution by Type of Therapeutic Area

- Figure 8.1 Company Competitiveness Analysis: ADC Cytotoxic Payloads and Warheads Providers based in North America

- Figure 8.2 Company Competitiveness Analysis: ADC Cytotoxic Payloads and Warheads Providers based in Europe

- Figure 8.3 Company Competitiveness Analysis: ADC Cytotoxic Payloads and Warheads Providers based in Asia-Pacific

- Figure 9.1 CARBOGEN AMCIS: Annual Revenues, Consolidated Financial Details, Since FY 2022 (INR Billion)

- Figure 9.2 Merck: Annual Revenues, Consolidated Financial Details, Since FY 2022 (EUR Million)

- Figure 9.3 WuXi AppTec: Annual Revenues, Consolidated Financial Details, Since FY 2022 (RMB Billion)

- Figure 11.1 Partnerships and Collaborations: Cumulative Year-wise Trend, Since Pre-2021

- Figure 11.2 Partnerships and Collaborations: Distribution by Type of Partnership

- Figure 11.3 Partnerships and Collaborations: Distribution by Year and Type of Partnership, Since Pre-202

- Figure 11.4 Partnerships and Collaborations: Distribution by Type of Partner

- Figure 11.5 Most Active Players: Distribution by Number of Partnerships

- Figure 11.6 Partnerships and Collaborations: Local and International Agreements

- Figure 11.7 Partnerships and Collaborations: Intracontinental and Intercontinental Agreements

- Figure 12.1 Recent Expansions: Cumulative Year-wise Trend, Since 2020

- Figure 12.2 Recent Expansions: Distribution by Type of Expansion

- Figure 12.3 Recent Expansions: Distribution by Year and Type of Expansion, Since 2020

- Figure 12.4 Recent Expansions: Distribution by Location of Expansion (Country)

- Figure 12.5 Recent Expansions: Distribution by Location of Expansion (Continent)

- Figure 12.6 Most Active Players: Distribution by Number of Expansions

- Figure 13.1 Global Installed ADC Cytotoxic Payloads and Warheads Manufacturing Capacity: Distribution by Range of Installed Capacity (in Liters)

- Figure 13.2 Global Installed ADC Cytotoxic Payloads and Warheads Manufacturing Capacity: Distribution by Scale of Operation

- Figure 13.3 Global Installed ADC Cytotoxic Payloads and Warheads Manufacturing Capacity: Distribution by Location of ADC Cytotoxic Payloads and Warheads Manufacturing Facility

- Figure 14.1 Global Annual Demand for ADC Payloads (in Kg), Till 2035

- Figure 14.2 Global Clinical Demand for ADC Payloads, Till 2035 (in KGs)

- Figure 14.3 Global Commercial Demand for ADC Payloads, Till 2035 (in KGs)

- Figure 14.4 Clinical Demand Analysis: Distribution by Type of Payload, Current Year and 2035

- Figure 14.5 Clinical Demand Analysis: Distribution by Type of Payload, Till 2035

- Figure 14.6 Clinical Demand Analysis: Distribution by Type of Phase of Development, Current Year and 2035

- Figure 14.7 Clinical Demand Analysis: Distribution by Type of Phase of Development, Till 2035

- Figure 14.8 Commercial Demand Analysis: Distribution by Payload, Till 2035

- Figure 14.9 Commercial Demand Analysis: Distribution by Type of Payload, Till 2035

- Figure 14.10 Commercial Demand Analysis: Distribution by Therapeutic Area, Till 2035

- Figure 14.11 Commercial Demand Analysis: Distribution by Geographical Regions, Current Year and 2035

- Figure 14.12 Commercial Demand Analysis: Distribution by Geographical Regions, Till 2035

- Figure 16.1 ADC Cytotoxic Payloads and Warheads Market, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 16.2 ADC Cytotoxic Payloads and Warheads Market, Forecasted Estimates (Till 2035): Conservative Scenario (USD Million)

- Figure 16.3 ADC Cytotoxic Payloads and Warheads Market, Forecasted Estimates (Till 2035): Optimistic Scenario (USD Million)

- Figure 17.1 ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Product, Current Year, 2030 and 2035

- Figure 17.2 ADC Cytotoxic Payloads and Warheads Market for Clinical Product, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 17.3 ADC Cytotoxic Payloads and Warheads Market for Commercial Product, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 18.1 ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Payload, Current Year, 2030 and 2035

- Figure 18.2 ADC Cytotoxic Payloads and Warheads Market for Tubulin inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 18.3 ADC Cytotoxic Payloads and Warheads Market for Topoisomerase Inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 18.4 ADC Cytotoxic Payloads and Warheads Market for DNA Damaging Agents, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 18.5 ADC Cytotoxic Payloads and Warheads Market for Others, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 19.1 ADC Cytotoxic Payloads and Warheads Market: Distribution by Type of Payload / Warhead, Current Year, 2030 and 2035

- Figure 19.2 ADC Cytotoxic Payloads and Warheads Market for Topoisomerase I inhibitors, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 19.3 ADC Cytotoxic Payloads and Warheads Market for Maytansinoid, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 19.4 ADC Cytotoxic Payloads and Warheads Market for Auristatin, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 19.5 ADC Cytotoxic Payloads and Warheads Market for Others, Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.1 ADC Cytotoxic Payloads and Warheads Market: Distribution by Geographical Regions, Current Year, 2030 and 2035

- Figure 20.2 ADC Cytotoxic Payloads and Warheads Market in North America: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.3 ADC Cytotoxic Payloads and Warheads Market in the US: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.4 ADC Cytotoxic Payloads and Warheads Market in Canada: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.5 ADC Cytotoxic Payloads and Warheads Market in Europe: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.6 ADC Cytotoxic Payloads and Warheads Market in Germany: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.7 ADC Cytotoxic Payloads and Warheads Market in the UK: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.8 ADC Cytotoxic Payloads and Warheads Market in France: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.9 ADC Cytotoxic Payloads and Warheads Market in Italy: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.10 ADC Cytotoxic Payloads and Warheads Market in Spain: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.11 ADC Cytotoxic Payloads and Warheads Market in Asia-Pacific: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.12 ADC Cytotoxic Payloads and Warheads Market in China: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.13 ADC Cytotoxic Payloads and Warheads Market in Japan: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

- Figure 20.14 ADC Cytotoxic Payloads and Warheads Market in Australia: Historical Trends (Since 2023) and Forecasted Estimates (Till 2035) (USD Million)

抗體藥物複合體(ADC)市場-2026-2032年全球市場預測

抗體藥物複合體(ADC)市場-2026-2032年全球市場預測 抗體藥物複合體(ADC) 市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。

抗體藥物複合體(ADC) 市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。 抗體藥物複合體(ADC) 市場:按產品類型、目標抗原、有效載荷/技術、連接子類型、適應症和最終用戶分類 - 市場規模、行業動態、機會分析和預測 (2026–2035)抗體療法市場機會、成長要素、產業趨勢分析及2026-2035年預測

抗體藥物複合體(ADC) 市場:按產品類型、目標抗原、有效載荷/技術、連接子類型、適應症和最終用戶分類 - 市場規模、行業動態、機會分析和預測 (2026–2035)抗體療法市場機會、成長要素、產業趨勢分析及2026-2035年預測 抗體藥物複合體市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

抗體藥物複合體市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 全球ADC技術市場(第三版):依技術世代、接合方式、連接器類型和地區分類-產業趨勢及至2040年的預測

全球ADC技術市場(第三版):依技術世代、接合方式、連接器類型和地區分類-產業趨勢及至2040年的預測 奈米抗體市場規模、佔有率和成長分析:按抗體類型、來源生物類型、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

奈米抗體市場規模、佔有率和成長分析:按抗體類型、來源生物類型、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 抗體藥物複合體(ADC) 市場:按產品類型、連接子類型、應用、銷售管道和地區分類

抗體藥物複合體(ADC) 市場:按產品類型、連接子類型、應用、銷售管道和地區分類 抗體藥物複合體市場報告:按成分、標靶、應用、最終用戶和地區分類(2026-2034 年)PMO偶聯物市場報告:趨勢、預測和競爭分析(至2035年)

抗體藥物複合體市場報告:按成分、標靶、應用、最終用戶和地區分類(2026-2034 年)PMO偶聯物市場報告:趨勢、預測和競爭分析(至2035年)