|

市場調查報告書

商品編碼

2061474

抗體療法市場機會、成長要素、產業趨勢分析及2026-2035年預測Antibody Therapy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

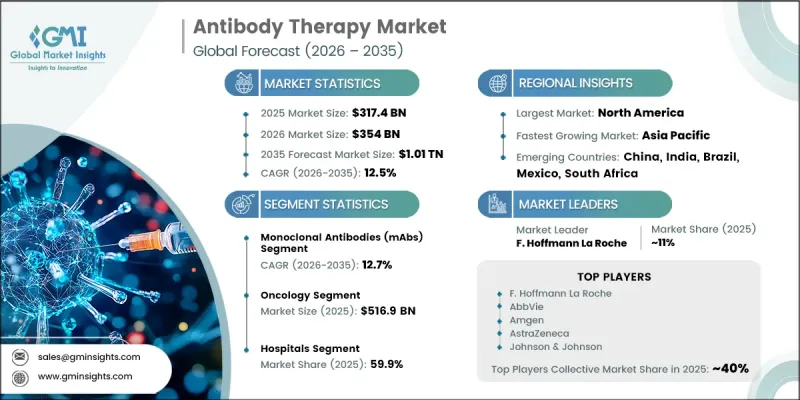

預計到 2025 年,全球抗體療法市場價值將達到 3,174 億美元,到 2035 年將達到 1.01 兆美元,年複合成長率為 12.5%。

由於包括腫瘤、自體免疫疾病、感染疾病和神經系統疾病在內的多個治療領域中,基於抗體的先進治療方法的商業化和法規核准不斷推進,該市場正經歷著顯著成長。對生物目標療法的需求不斷成長,加上單株抗體、雙特異性抗體和抗體藥物偶聯物(ADC)技術的快速創新,正顯著加速產業擴張。強大的抗體療法臨床研發管線,以及對生技藥品研發和藥物創新投入的不斷增加,持續為市場參與企業創造著充滿希望的機會。此外,有利的監管支持和不斷增加的已通過核准抗體療法也推動了全球市場的發展。隨著醫療機構日益重視精準醫療和標靶治療策略,抗體療法正成為現代疾病管理的重要組成部分。重組生物技術、蛋白質工程和新一代生物製劑平台的技術進步也在提高治療效果,改善患者預後,並增強市場的長期潛力。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 3174億美元 |

| 預計金額 | 1.01兆美元 |

| 複合年成長率 | 12.5% |

抗體療法是一種高度標靶的治療方法,它利用單株抗體來識別並結合與致病細胞或病原體相關的特定抗原。由於其精準性、療效和安全性均有所提高,抗體療法被廣泛應用於癌症治療、發炎性疾病、自體免疫疾病和感染疾病控制。透過選擇性地靶向異常細胞並最大限度地減少對健康組織的損傷,抗體療法已成為精準醫療和先進生物治療方法的重要組成部分。人們對個人化醫療解決方案和標靶治療性介入的日益關注,進一步推動了抗體療法在全球醫療系統中的應用。

預計到2025年,單株抗體市場將以12.7%的複合年成長率成長。該市場的成長主要得益於單株抗體在治療癌症、自體免疫疾病、感染疾病和遺傳性疾病等慢性疾病的廣泛應用。單株抗體具有高度精準的治療效果,同時也能誘發強效的免疫反應,進而提高療效和臨床結果。重組DNA技術、抗體工程、蛋白質修飾技術和先進生技藥品生產平台的持續發展,正加速新一代單株抗體療法的問世。這些創新不僅持續推動該市場的強勁成長,也提升了抗體療法在整體醫療保健領域的臨床效用。

預計到2035年,腫瘤領域市場規模將達5,169億美元。由於單株抗體、抗體藥物偶聯物(ADC)和雙特異性抗體在癌症治療中的應用日益廣泛,該領域在抗體治療市場中繼續保持主導地位。全球癌症發生率的上升以及對安全性和有效性更高的標靶治療的需求不斷成長,推動了基於抗體的腫瘤治療的廣泛應用。腫瘤領域研發投入的大幅增加、癌症特異性臨床管線的快速擴張以及創新生技藥品的持續獲得監管部門批准,進一步促進了該領域的成長。此外,基於生物標記的治療方法和精準腫瘤學的進步,正在提高抗體療法在癌症治療中的療效和應用率。

預計到2025年,北美抗體療法市佔率將達到41.5%。該地區的成長主要得益於生技藥品研發的強勁投入、有利的法規環境以及領先的生物技術和製藥公司不斷推進的創新抗體療法研發。先進的醫療基礎設施、完善的醫保報銷體係以及先進生物治療方法的快速普及,持續鞏固北美在該市場的主導地位。此外,全部區域慢性病、癌症、自體免疫疾病和發炎性疾病的日益普遍,也推動了對抗體治療方法的持續需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 工業生態系分析

- 影響產業的因素

- 促進因素

- 全球慢性病和感染疾病的盛行率不斷上升。

- 活性化研發活動

- 美國和歐洲的高採納率和批准率

- 快速發展的生物製藥產業

- 抗體療法的應用範圍不斷擴大

- 產業潛在風險與挑戰

- 某些單株抗體療法的高成本

- 複雜的製造流程與物流挑戰

- 市場機遇

- 新一代抗體形式的開發

- 新興市場和未開發市場中的成長機會

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術與創新展望

- 最新科技趨勢

- 單株抗體(mAbs)的設計與最佳化

- 抗體藥物偶聯物(ADC)平台技術

- 新技術

- 雙特異性和多特異性抗體平台

- 放射性標記和高標靶抗體療法

- 最新科技趨勢

- 正在研發中的產品

- 單株抗體

- 抗體-藥物偶聯物

- 價格分析

- 人工智慧和生成式人工智慧對市場的影響

- 波特的分析

- PESTLE分析

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估計與預測:依類型分類,2022-2035年

- 單株抗體(mAbs)

- 抗體藥物偶聯物(ADC)

- 其他

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 腫瘤學

- 感染疾病

- 神經系統疾病

- 自體免疫/發炎性疾病

- 其他

第7章 市場估計與預測:依產地分類,2022-2035年

- 嵌合體

- 老鼠

- 完全人類

- 人性化

第8章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院

- 專業醫療中心

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AbbVie

- Amgen

- AstraZeneca

- Bristol Myers Squibb Company

- Eli Lilly and Company

- F. Hoffmann La Roche

- GlaxoSmithKline

- Johnson & Johnson

- Merck & Co.

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Seagen

- Takeda Pharmaceutical Company

The Global Antibody Therapy Market was valued at USD 317.4 billion in 2025 and is estimated to grow at a CAGR of 12.5% to reach USD 1.01 trillion by 2035.

The market is experiencing substantial growth due to the increasing commercialization and regulatory approval of advanced antibody-based treatments across multiple therapeutic areas, including oncology, autoimmune disorders, infectious diseases, and neurological conditions. Growing demand for targeted biologic therapies, combined with rapid innovation in monoclonal antibodies, bispecific antibodies, and antibody-drug conjugates (ADCs), is significantly accelerating industry expansion. The strong clinical pipeline for antibody therapeutics, along with rising investments in biologics research and pharmaceutical innovation, continues to create lucrative opportunities for market participants. In addition, favorable regulatory support and the increasing number of approved antibody therapies are reinforcing market development globally. As healthcare providers increasingly prioritize precision medicine and targeted treatment strategies, antibody therapies are becoming a critical component of modern disease management. Technological advancements in recombinant biotechnology, protein engineering, and next-generation biologic platforms are also enhancing treatment effectiveness, improving patient outcomes, and strengthening long-term market potential.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $317.4 Billion |

| Forecast Value | $1.01 Trillion |

| CAGR | 12.5% |

Antibody therapy represents a highly targeted treatment approach that uses monoclonal antibodies to identify and attach to specific antigens linked to disease-causing cells or pathogens. These therapies are extensively utilized across cancer treatment, inflammatory diseases, autoimmune conditions, and infectious disease management because of their precision, therapeutic efficiency, and improved safety profile. By selectively targeting abnormal cells while reducing damage to healthy tissues, antibody-based therapies have become an essential element of precision medicine and advanced biologic treatment approaches. The growing focus on personalized healthcare solutions and targeted therapeutic interventions is further supporting widespread adoption of antibody therapies across global healthcare systems.

The monoclonal antibodies segment is anticipated to register a CAGR of 12.7% during 2025. Segment growth is largely driven by the expanding use of monoclonal antibodies in treating chronic illnesses, including cancer, autoimmune diseases, infectious disorders, and genetic conditions. Monoclonal antibodies provide highly precise therapeutic activity while generating strong immune-mediated responses that improve treatment effectiveness and clinical outcomes. Ongoing developments in recombinant DNA technologies, antibody engineering, protein modification techniques, and advanced biologic manufacturing platforms are accelerating the introduction of next-generation monoclonal antibody therapies. These innovations continue to support strong growth within the segment while increasing the clinical relevance of antibody-based therapeutics across healthcare applications.

The oncology segment is projected to reach USD 516.9 billion by 2035. The segment continues to dominate the antibody therapy market due to increasing use of monoclonal antibodies, antibody-drug conjugates, and bispecific antibodies in cancer treatment. Rising global cancer incidence and growing demand for highly targeted therapies with improved safety and efficacy profiles are driving widespread adoption of antibody-based oncology treatments. Significant investments in oncology research and development, rapid expansion of cancer-focused clinical pipelines, and continuous regulatory approvals for innovative biologic therapies are further strengthening segment growth. In addition, advancements in biomarker-based treatment approaches and precision oncology are improving the effectiveness and utilization of antibody therapies within cancer care settings.

North America Antibody Therapy Market accounted for 41.5% share in 2025. Regional growth is supported by strong investment in biologics research, a favorable regulatory environment, and increasing development of innovative antibody therapeutics by major biotechnology and pharmaceutical companies. The presence of advanced healthcare infrastructure, strong reimbursement frameworks, and rapid adoption of advanced biologic treatments continues to reinforce North America's leadership position in the market. Additionally, the increasing prevalence of chronic diseases, cancer, autoimmune disorders, and inflammatory conditions throughout the region is contributing to sustained demand for antibody-based therapies.

Major companies operating in the Global Antibody Therapy Market include Pfizer, AstraZeneca, AbbVie, Bristol Myers Squibb Company, Eli Lilly and Company, Regeneron Pharmaceuticals, Novartis, Johnson & Johnson, Takeda Pharmaceutical Company, Merck & Co., GlaxoSmithKline, F. Hoffmann La Roche, Amgen, Sanofi, and Seagen. Companies operating in the antibody therapy market are adopting multiple strategic initiatives to strengthen their competitive position and expand their global presence. Leading pharmaceutical and biotechnology firms are increasing investments in research and development to accelerate the discovery of next-generation antibody therapies, including bispecific antibodies and antibody-drug conjugates. Strategic collaborations, licensing agreements, and acquisitions are being widely utilized to strengthen product pipelines and expand technological capabilities. Many companies are also focusing on expanding manufacturing capacity and improving biologics production efficiency to meet growing global demand. In addition, organizations are prioritizing precision medicine strategies, biomarker-driven therapies, and advanced clinical trial programs to improve treatment outcomes and regulatory success rates.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Application trends

- 2.2.4 Source trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic and infectious disease worldwide

- 3.2.1.2 Growing R&D activities

- 3.2.1.3 High rate of adoption and approval in the U.S. and Europe

- 3.2.1.4 Booming biologics industry

- 3.2.1.5 Rising applications of antibody therapy

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of some monoclonal antibody therapeutics

- 3.2.2.2 Complex manufacturing processes and logistical challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into next-generation antibody formats

- 3.2.3.2 Growth opportunities in emerging and underpenetrated markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by Primary Research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape (Driven by Primary Research)

- 3.5.1 Current technological trends

- 3.5.1.1 Monoclonal antibody (mAb) engineering and optimization

- 3.5.1.2 Antibody-drug conjugate (ADC) platform technologies

- 3.5.2 Emerging technologies

- 3.5.2.1 Bispecific and multispecific antibody platforms

- 3.5.2.2 Radiolabeled and advanced targeted antibody therapeutics

- 3.5.1 Current technological trends

- 3.6 Pipeline products (Driven by Primary Research)

- 3.6.1 Monoclonal antibodies

- 3.6.2 Antibody drug conjugates

- 3.7 Pricing analysis

- 3.8 Impact of AI and Gen AI on the market

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 ($ Mn)

- 5.1 Key trends

- 5.2 Monoclonal antibodies (mAbs)

- 5.3 Antibody-drug conjugates (ADCs)

- 5.4 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Infectious diseases

- 6.4 Neurological diseases

- 6.5 Autoimmune & inflammatory diseases

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Sources, 2022-2035 ($ Mn)

- 7.1 Key trends

- 7.2 Chimeric

- 7.3 Murine

- 7.4 Fully human

- 7.5 Humanized

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty centers

- 8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East & Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Amgen

- 10.3 AstraZeneca

- 10.4 Bristol Myers Squibb Company

- 10.5 Eli Lilly and Company

- 10.6 F. Hoffmann La Roche

- 10.7 GlaxoSmithKline

- 10.8 Johnson & Johnson

- 10.9 Merck & Co.

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Regeneron Pharmaceuticals

- 10.13 Sanofi

- 10.14 Seagen

- 10.15 Takeda Pharmaceutical Company

抗體藥物複合體(ADC)市場-2026-2032年全球市場預測

抗體藥物複合體(ADC)市場-2026-2032年全球市場預測 抗體藥物複合體(ADC) 市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。

抗體藥物複合體(ADC) 市場機會、成長要素、產業趨勢分析及 2026-2035 年預測。 抗體藥物複合體(ADC) 市場:按產品類型、目標抗原、有效載荷/技術、連接子類型、適應症和最終用戶分類 - 市場規模、行業動態、機會分析和預測 (2026–2035)

抗體藥物複合體(ADC) 市場:按產品類型、目標抗原、有效載荷/技術、連接子類型、適應症和最終用戶分類 - 市場規模、行業動態、機會分析和預測 (2026–2035) 抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場:趨勢與預測(至2035年)-按產品類型、有效載荷類型、有效載荷/彈頭子類別和地區分類

抗體藥物偶聯物(ADC)細胞毒性有效載荷和彈頭市場:趨勢與預測(至2035年)-按產品類型、有效載荷類型、有效載荷/彈頭子類別和地區分類 抗體藥物複合體市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年全球ADC技術市場(第三版):依技術世代、接合方式、連接器類型和地區分類-產業趨勢及至2040年的預測

抗體藥物複合體市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年全球ADC技術市場(第三版):依技術世代、接合方式、連接器類型和地區分類-產業趨勢及至2040年的預測 奈米抗體市場規模、佔有率和成長分析:按抗體類型、來源生物類型、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

奈米抗體市場規模、佔有率和成長分析:按抗體類型、來源生物類型、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測 抗體藥物複合體(ADC) 市場:按產品類型、連接子類型、應用、銷售管道和地區分類

抗體藥物複合體(ADC) 市場:按產品類型、連接子類型、應用、銷售管道和地區分類 抗體藥物複合體市場報告:按成分、標靶、應用、最終用戶和地區分類(2026-2034 年)PMO偶聯物市場報告:趨勢、預測和競爭分析(至2035年)

抗體藥物複合體市場報告:按成分、標靶、應用、最終用戶和地區分類(2026-2034 年)PMO偶聯物市場報告:趨勢、預測和競爭分析(至2035年)