|

市場調查報告書

商品編碼

2073660

印度數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Digital Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

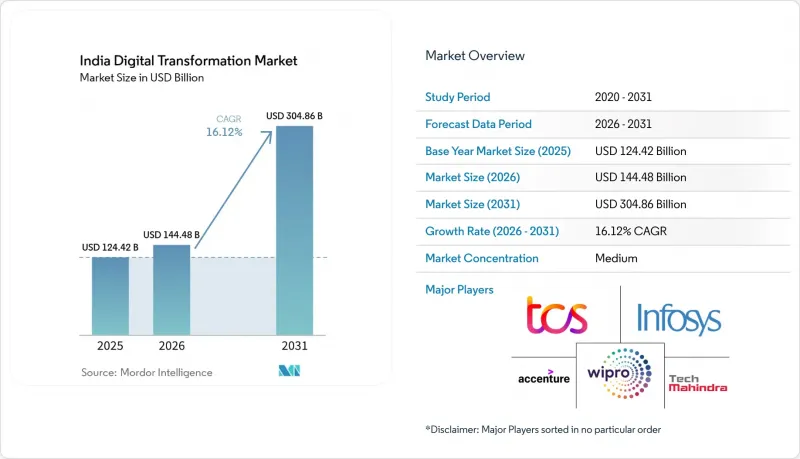

據 Mordor Intelligence 稱,印度數位轉型市場預計到 2026 年價值將達到 1,444.8 億美元,高於 2025 年的 1,244.2 億美元,預計到 2031 年將達到 3,048.6 億美元。

預計 2026 年至 2031 年的複合年成長率為 16.12%。

本報告按類型(分析、人工智慧/機器學習、擴增實境、物聯網、工業機器人、區塊鏈等)、元件(解決方案、服務)、部署模式(雲端、邊緣、本地部署)、組織規模(大型企業、中小企業)和最終用戶產業(製造業、零售業、運輸業、醫療保健業、銀行、金融服務業、電信業等)進行分類。市場預測以美元計價。

印度數位轉型市場的趨勢與洞察

政府主導的「數位印度」和「印度堆疊」計畫的勢頭強勁。

中央政府已將「數位印度」計畫的撥款增加至2026會計年度的1490.3兆印度盧比,重點投資於數位公共基礎設施建設、培訓62.5萬名IT專業人員以及培訓26.5萬名資訊安全專業人員。 「印度堆疊」(India Stack)的每一層,包括Aadhaar、UPI和DigiLocker,都在標準化身分驗證、支付和資料交換,從而降低企業在全國部署的整合成本。統一支付介面(UPI)在2021年處理了380億筆交易(總計71.95兆印度盧比),顯示交易層已趨於成熟。各邦政府也積極擁抱平台化思維;安得拉邦正透過其基於WhatsApp的管治系統「Mana Mitra」提供161項公共服務,從而擴大其「最後一公里」服務覆蓋範圍。此外,2025 年《數位個人資料保護條例》引入了明確的同意和資料受託人義務,為私營部門投資建立了監管確定性(印度新聞和資訊局)。

行動網際網路和智慧型手機的快速普及

價格親民的設備和極具競爭力的數據費率方案彌合了網路連線的鴻溝,使得印度在2023年至2025年間新增了1.2億4G用戶。到2025年,每位用戶平均每月數據消耗量將超過19GB,這將催生一個蓬勃發展的數位內容、OTT影片和行動遊戲生態系統,並推動對雲端配送網路和金融科技微服務的需求。智慧型手機普及率將超過73%,加速三線城市和農村地區全面數位支付的普及。電子商務、叫車和外送平台正在利用其不斷擴大的潛在基本客群,而通訊業者透過內容包和設備分期付款計劃,從高數據消耗用戶群體中獲利。這些正面影響也正輻射到印度的數位轉型市場,企業正在重新設計客戶旅程,打造行動優先的客戶體驗。

資料隱私和網路攻擊風險日益增加

預計到2025年,印度將記錄超過150萬起網路安全事件,其中詐騙、勒索軟體和網路詐騙造成的損失將高達2,000億印度盧比。光是銀行業在2024年下半年就報告了2500起定向攻擊,促使銀行、金融和保險(BFSI)以及醫療保健行業的網路安全預算增加了30%。政府已將2025會計年度的國家網路安全預算增加到190億印度盧比,但隨著企業採用多重雲端和邊緣架構,攻擊面正在擴大。 2024年,品牌冒用詐騙造成的損失高達900億印度盧比,削弱了消費者對數位管道的信心。風險意識的提高正在減緩敏感產業的數位轉型步伐,抑製印度數位轉型市場的短期成長。

細分市場分析

到2025年,雲端運算和邊緣運算將佔印度數位轉型市場佔有率的27.35%。這反映了大規模工作負載的遷移以及受監管產業對主權雲端的採用。在客戶服務聊天機器人自動化(具備語言模式、程式碼產生和敘事洞察等功能)以及商業智慧的推動下,生成式人工智慧驅動的分析正以23.25%的複合年成長率成長。預計到2031年,印度以人工智慧為中心的分析領域的數位轉型市場規模將超過293億美元,這主要得益於馬哈拉斯特拉邦和特倫甘納邦的超大規模資料中心業者GPU叢集的支持。工業機器人在汽車製造工廠的應用日益廣泛,例如現代汽車部署了2000台智慧機器人,將維護停機時間減少了5%。基於私有5G網路的物聯網感測器能夠實現對資產的即時監控,而擴增實境(XR)工具則為現場工作人員提供了遠端培訓。區塊鏈的應用仍處於小眾階段,主要集中在供應鏈可追溯性方面,而積層製造技術則在航太原型製作不斷擴展。網路安全工具擴大融合人工智慧技術,以應對進階持續性威脅(APT),從而建構一套完整的整合技術體系。

新參與企業正透過特定領域的AI模型、低程式碼物聯網平台和計量收費的機器人即服務(RaaS)來脫穎而出。柔軟性的定價和基於績效的合約對尋求快速投資回報的中型製造商極具吸引力。這些技術之間的協同效應提升了商業價值,並鞏固了印度作為全球整合數位轉型解決方案試驗場的地位。

到2025年,服務將佔印度數位轉型市場規模的53.05%,預計到2031年將以20.15%的複合年成長率成長,因為企業正在尋求諮詢、整合和管理服務方面的專業知識。大規模轉型專案包括多重雲端策略、增強網路安全以及可組合ERP系統的現代化改造,這些都需要跨職能的諮詢能力。其餘部分由解決方案(軟體和平台)構成,其中產業專用的應用在製造執行系統、遠端醫療以及銀行、金融和保險(BFSI)行業的監管報告等領域備受關注。

以塔塔諮詢服務公司 (TCS)、印孚瑟斯 (Infosys) 和威普羅 (Wipro)主導的印度成熟IT服務生態系統,正在加強與超大規模資料中心業者的合作,並共同開發產業專屬加速器。Accenture收購 TalentSprint,增強了其 LearnVantage 平台,並加速了其人工智慧和資料工程人才儲備的成長。對託管服務的需求激增,巴帝電信 (Bharti Airtel) 位於浦那的中心正在協助 2000 多家公司進行多重雲端管治。基於績效的合約將風險轉移給服務提供者,同時擴大了長期市場佔有率,並將供應商的報酬與降低流程故障率和減少客戶流失等關鍵績效指標 (KPI) 掛鉤。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府的「數位印度」和「印度堆疊」計畫勢頭強勁。

- 行動網際網路和智慧型手機的快速普及

- 透過企業雲端和人工智慧主導的解決方案提高效率

- 5G/寬頻基礎設施投資熱潮

- 建構超大規模GPU資料中心(IndiaAI叢集)

- GST 2.0電子帳單強制要求超過 600 萬家中小企業使用。

- 市場限制因素

- 資料隱私和網路攻擊風險日益增加

- 數位技能嚴重短缺

- 公共部門舊有系統的碎片化

- 三、四線城市電網不穩定

- 監理情勢

- 技術展望

- 波特五力分析

- 當前市場狀況和數位轉型實踐的演變

- 關鍵指標

- 科技支出趨勢

- 物聯網設備數量

- 網路攻擊總數

- 技術人員部署

- 網路普及率

- 數位競爭力

- 寬頻普及率

- 雲端採用

- 人工智慧實施

- 電子商務

第5章 市場規模與成長預測

- 按類型

- 分析、人工智慧、機器學習

- 擴增實境(XR)

- 物聯網 (IoT)

- 工業機器人

- 區塊鏈

- 雲端邊緣運算

- 其他(數位雙胞胎、移動性、連結性)

- 按組件

- 解決方案

- 服務

- 部署模式

- 雲

- 邊緣

- 現場

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 製造業

- 石油、天然氣和公共產業

- 零售與電子商務

- 運輸/物流

- 衛生保健

- BFSI

- 通訊/IT

- 政府/公共部門

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- Google LLC

- Siemens AG

- International Business Machines Corporation

- Microsoft Corporation

- Cognex Corporation

- Hewlett Packard Enterprise Company

- SAP SE

- Dell Technologies Inc.

- Oracle Corporation

- Adobe Inc.

- Amazon Web Services, Inc.

- Apple Inc.

- Salesforce, Inc.

- Cisco Systems, Inc.

- Infosys Limited

- Tata Consultancy Services Limited

- Wipro Limited

- Tech Mahindra Limited

- HCL Technologies Limited

- Larsen & Toubro Infotech Limited

- Zoho Corporation Private Limited

- Reliance Jio Infocomm Limited

- Bharti Airtel Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, india digital transformation market size in 2026 is estimated at USD 144.48 billion, growing from 2025 value of USD 124.42 billion with 2031 projections showing USD 304.86 billion, growing at 16.12% CAGR over 2026-2031.

This report is Segmented by Type (Analytics AI & ML, Extended Reality, IoT, Industrial Robotics, Blockchain and More), Component (Solutions, Services), Deployment Mode (Cloud, Edge, On-Premises), Organisation Size (Large Enterprises, SMEs), End-User Industry (Manufacturing, Retail, Transportation, Healthcare, BFSI, Telecom, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Digital Transformation Market Trends and Insights

Government-led Digital India and India Stack momentum

The central government extended Digital India funding to INR 14,903 crore through FY 2026, channeling resources toward digital public infrastructure, reskilling 625,000 IT professionals, and training 265,000 information-security specialists. India Stack layers, such as Aadhaar, UPI, and DigiLocker, standardize identity, payments, and data exchange, lowering integration costs for enterprises rolling out at a population scale. The Unified Payments Interface processed 38 billion transactions valued at INR 71.95 trillion in 2021, demonstrating transaction-layer maturity. State governments replicate platform thinking; Andhra Pradesh delivers 161 public services via "Mana Mitra" WhatsApp governance, widening last-mile reach. The Digital Personal Data Protection Rules 2025 introduce clear consent and data-fiduciary obligations, cementing regulatory certainty for private-sector investment, Press Information Bureau of India.

Rapid growth in mobile-internet and smartphone adoption

India added 120 million 4G subscribers between 2023 and 2025 as affordable handsets and aggressive data tariffs bridged the connectivity gap. With monthly average data consumption per user exceeding 19 GB in 2025, digital content, OTT video, and mobile gaming ecosystems flourish, propelling demand for cloud delivery networks and fintech micro-services. Smartphone penetration surpasses 73%, catalyzing inclusive digital-payment adoption in tier-3 towns and rural areas. E-commerce, ride-hailing, and food-delivery platforms leverage the expanding addressable base, while telcos monetize higher data-consumption tiers through bundled content and device financing. The positive spill-over benefits the India digital transformation market as enterprises redesign customer journeys for mobile-first engagement.

Escalating data-privacy & cyber-attack risks

India recorded more than 1.5 million cyber incidents in 2025, with projected losses of INR 20,000 crore to fraud, ransomware, and phishing scams. Banks reported 2,500 targeted attacks in H2 2024 alone, prompting a 30% rise in cybersecurity budgets across BFSI and healthcare. The government raised its national cybersecurity allocation to INR 1,900 crore for FY 2025, yet the attack surface expands as enterprises adopt multicloud and edge architectures. Brand-impersonation scams inflicted INR 9,000 crore losses in 2024, eroding consumer trust in digital channels. Heightened risk perception slows digital rollouts in sensitive sectors, tempering near-term growth for the India digital transformation market.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise push for cloud, AI, and efficiency gains

- Large-scale 5G and broadband capital outlays

- Acute digital-skills shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud & Edge Computing contributed 27.35% of the India digital transformation market share in 2025, reflecting large-scale workload migration and sovereign-cloud adoption for regulated industries. Generative-AI-driven analytics posts a 23.25% CAGR, as language models automate customer service chatbots, code generation, and business-intelligence narrative insights. The India digital transformation market size for AI-centric analytics is forecast to surpass USD 29.3 billion by 2031, underpinned by hyperscaler GPU clusters in Maharashtra and Telangana. Industrial robotics gains traction in automotive facilities, where Hyundai integrated 2,000 smart robots, cutting maintenance downtime by 5%. IoT sensors over private 5G enable real-time asset monitoring, while extended-reality tools facilitate remote training for shop-floor workers. Blockchain adoption remains niche, focused on supply-chain traceability, whereas additive manufacturing scales in aerospace prototyping. Cybersecurity tools increasingly embed AI to counter advanced persistent threats, rounding out a converged technology stack.

New market entrants differentiate through domain-specific AI models, low-code IoT platforms, and pay-per-use robotic-as-a-service offerings. Pricing flexibility and outcome-based contracts resonate with mid-market manufacturers seeking rapid ROI. Synergies among these technologies compound business value, reinforcing India's position as a global testbed for integrated digital-transformation solutions.

Services represented 53.05% of the India digital transformation market size in 2025 and are positioned to grow at a 20.15% CAGR to 2031 as enterprises seek consulting, integration, and managed-service expertise. Large transformation programs span multicloud strategy, cybersecurity hardening, and composable ERP modernization, requiring cross-functional advisory capabilities. Solutions (software and platforms) account for the balance, with verticalized applications gaining traction in manufacturing execution systems, tele-health, and regulatory reporting for BFSI.

India's established IT-services ecosystem, led by TCS, Infosys, and Wipro, deepens alliances with hyperscalers to co-develop industry accelerators. Accenture's acquisition of TalentSprint augments its LearnVantage platform, fostering AI and data-engineering talent pipelines. Managed-services demand surges as Bharti Airtel's Pune center supports more than 2,000 enterprises on multicloud governance. Outcome-linked contracts tie vendor remuneration to KPIs such as process-scrap reduction and customer-churn minimization, shifting risk to providers yet increasing long-term wallet share.

Complete Report Scope:

- By Type

- Analytics, AI and ML

- Extended Reality (XR)

- Internet of Things (IoT)

- Industrial Robotics

- Blockchain

- Cloud and Edge Computing

- Others (Digital Twin, Mobility and Connectivity)

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- Edge

- On-Premises

- By Organisation Size

- Large Enterprises

- Small and Mid-Sized Enterprises

- By End-User Industry

- Manufacturing

- Oil, Gas and Utilities

- Retail and E-commerce

- Transportation and Logistics

- Healthcare

- BFSI

- Telecom and IT

- Government and Public Sector

- Others

List of Companies Covered in this Report:

- Accenture plc

- Google LLC

- Siemens AG

- International Business Machines Corporation

- Microsoft Corporation

- Cognex Corporation

- Hewlett Packard Enterprise Company

- SAP SE

- Dell Technologies Inc.

- Oracle Corporation

- Adobe Inc.

- Amazon Web Services, Inc.

- Apple Inc.

- Salesforce, Inc.

- Cisco Systems, Inc.

- Infosys Limited

- Tata Consultancy Services Limited

- Wipro Limited

- Tech Mahindra Limited

- HCL Technologies Limited

- Larsen & Toubro Infotech Limited

- Zoho Corporation Private Limited

- Reliance Jio Infocomm Limited

- Bharti Airtel Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government "Digital India" and India Stack momentum

- 4.2.2 Rapid mobile-internet and smartphone penetration

- 4.2.3 Enterprise cloud- and AI-led efficiency push

- 4.2.4 5G / broadband CAPEX boom

- 4.2.5 Hyperscale GPU datacentre build-out (IndiaAI clusters)

- 4.2.6 GST 2.0 e-invoicing mandate for >6 M SMEs

- 4.3 Market Restraints

- 4.3.1 Escalating data-privacy and cyber-attack risks

- 4.3.2 Acute digital-skills shortage

- 4.3.3 Legacy-system fragmentation in public sector

- 4.3.4 Power-grid instability in tier-3/4 cities

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Current Market Scenario and Evolution of DX Practices

- 4.8 Key Metrics

- 4.8.1 Technology Spending Trends

- 4.8.2 Number of IoT Devices

- 4.8.3 Total Cyber-attacks

- 4.8.4 Technology Staffing

- 4.8.5 Internet Penetration

- 4.8.6 Digital Competitiveness

- 4.8.7 Broadband Coverage

- 4.8.8 Cloud Adoption

- 4.8.9 AI Adoption

- 4.8.10 E-commerce

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Analytics, AI and ML

- 5.1.2 Extended Reality (XR)

- 5.1.3 Internet of Things (IoT)

- 5.1.4 Industrial Robotics

- 5.1.5 Blockchain

- 5.1.6 Cloud and Edge Computing

- 5.1.7 Others (Digital Twin, Mobility and Connectivity)

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 Edge

- 5.3.3 On-Premises

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Mid-Sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Manufacturing

- 5.5.2 Oil, Gas and Utilities

- 5.5.3 Retail and E-commerce

- 5.5.4 Transportation and Logistics

- 5.5.5 Healthcare

- 5.5.6 BFSI

- 5.5.7 Telecom and IT

- 5.5.8 Government and Public Sector

- 5.5.9 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level overview, Market-level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Google LLC

- 6.4.3 Siemens AG

- 6.4.4 International Business Machines Corporation

- 6.4.5 Microsoft Corporation

- 6.4.6 Cognex Corporation

- 6.4.7 Hewlett Packard Enterprise Company

- 6.4.8 SAP SE

- 6.4.9 Dell Technologies Inc.

- 6.4.10 Oracle Corporation

- 6.4.11 Adobe Inc.

- 6.4.12 Amazon Web Services, Inc.

- 6.4.13 Apple Inc.

- 6.4.14 Salesforce, Inc.

- 6.4.15 Cisco Systems, Inc.

- 6.4.16 Infosys Limited

- 6.4.17 Tata Consultancy Services Limited

- 6.4.18 Wipro Limited

- 6.4.19 Tech Mahindra Limited

- 6.4.20 HCL Technologies Limited

- 6.4.21 Larsen & Toubro Infotech Limited

- 6.4.22 Zoho Corporation Private Limited

- 6.4.23 Reliance Jio Infocomm Limited

- 6.4.24 Bharti Airtel Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

美國數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印尼數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)IT產業的循環經濟平台:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

美國數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印尼數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)IT產業的循環經濟平台:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 2026-2030年全球石油天然氣產業數位轉型市場

2026-2030年全球石油天然氣產業數位轉型市場 技術創新正在改變機場:市場展望(2025-2035 年)

技術創新正在改變機場:市場展望(2025-2035 年) 數位轉型市場規模、佔有率和趨勢分析報告:按類型、部署模式、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

數位轉型市場規模、佔有率和趨勢分析報告:按類型、部署模式、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 鐵路貨運數位轉型市場分析與預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、實施、最終用戶和解決方案分類

鐵路貨運數位轉型市場分析與預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、實施、最終用戶和解決方案分類 數位轉型市場:依產品類型、部署模式、組織規模、業務職能與產業分類-2026-2032年全球市場預測

數位轉型市場:依產品類型、部署模式、組織規模、業務職能與產業分類-2026-2032年全球市場預測 2026年全球數位轉型諮詢服務市場報告

2026年全球數位轉型諮詢服務市場報告 數位轉型市場規模、佔有率、趨勢和預測:按類型、部署模式、企業規模、最終用戶產業和地區分類,2026-2034 年

數位轉型市場規模、佔有率、趨勢和預測:按類型、部署模式、企業規模、最終用戶產業和地區分類,2026-2034 年