|

市場調查報告書

商品編碼

2073659

美國數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)United States Digital Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

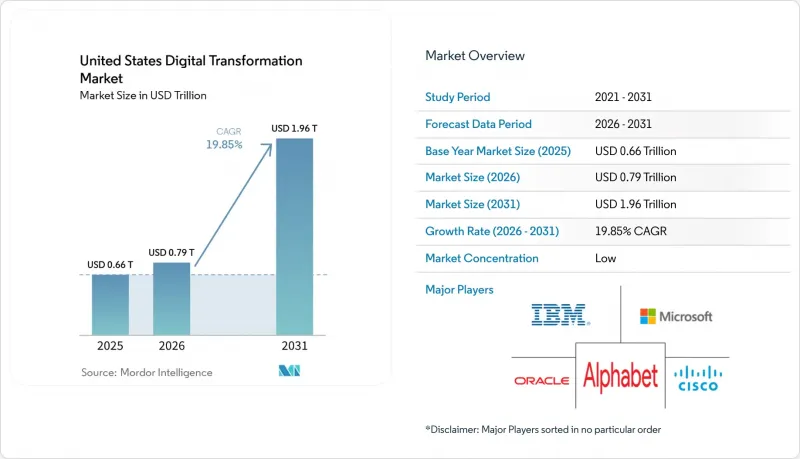

據 Mordor Intelligence 稱,2025 年美國數位轉型市場價值 6,600 億美元,預計到 2031 年將達到 1.96 兆美元,而 2026 年為 7,900 億美元,預測期(2026-2031 年)的複合年成長率為 19.85%。

本報告按組件(解決方案、服務)、部署模式(雲端、本地部署、混合部署)、企業規模(大型企業、中小企業)、類型(分析、人工智慧和機器學習、擴增實境(XR) 等)、最終用戶產業(銀行、金融服務和保險 (BFSI)、醫療保健和生命科學、製造業等)以及地區進行細分。市場預測以美元 (USD) 為單位。

美國數位轉型市場的趨勢與洞察

聯邦政府的「雲端智慧」和「FedRAMP 20x」計畫正在蓬勃發展。

FedRAMP 20x 將使聯邦政府的雲端遷移速度提升 60%,因為它無需政府對低影響工作負載提供資金支持,並實現了安全審查的自動化。在 2025 年的私人 IT 支出中,740 億美元將用於現代化改造,其中 127 億美元將用於網路安全。根據 FedRAMP 授權法預先認證其解決方案的供應商將獲得優先供應商地位,並帶動對州和地方政府機構的需求。

引進生成式人工智慧,打造高度個人化的客戶體驗 (CX)

目前,78%的美國公司已採用生成式人工智慧,隨著財富500強企業不斷擴大對OpenAI驅動的聊天和設計工具的使用,投資報酬率已達到3.7倍。到2025年底,25%的公司計劃在前線營運中實施基於代理的自動化。針對醫療保健、金融和零售業的產業專用的大規模語言模型正在提高服務質量,同時確保合規性。

各州隱私法規的差異(例如,CPRA)

已有19個州頒布了全面的隱私法,加州、德克薩斯州和維吉尼亞的執法團隊正在增加合規風險。由於缺乏統一的聯邦框架,在多個州運營的公司合規成本增加了30%至50%,這給中小企業帶來了相對較高的成本負擔。

細分市場分析

預計到2025年,在美國數位轉型市場中,解決方案將佔據67.40%的主導佔有率,這主要得益於企業對雲端運算、網路安全和分析平台的投資。同時,服務業預計將以20.74%的複合年成長率成長,因為企業擴大將整合、人工智慧模型調優和營運管理外包給顧問公司。 53%的IT領導者指出,資料科學技能缺口日益擴大,進一步推動了對外部專業知識的需求。

在持續最佳化需求的驅動下,服務組合正從一次性部署轉向基於結果的合約。服務提供者正在將變革管理和人工智慧管治的諮詢服務打包,以加速價值實現。隨著數位化成熟度的提高,預計到2031年,美國數位轉型市場的服務板塊將縮小與解決方案板塊的收入差距。

到2025年,本地部署平台將占美國數位轉型市場50.12%的佔有率,這反映了銀行、金融和保險(BFSI)以及醫療保健行業日益嚴格的數據主權監管。雲端解決方案正以20.35%的複合年成長率快速成長,受益於FedRAMP的簡化和混合雲端藍圖的建構。 Oracle和Google之間的互聯將使企業能夠並行運行OCI資料庫和Google Analytics,而無需支付跨雲端費用。

混合架構透過結合本地控制和公共雲端的強大運算能力,在支援人工智慧工作負載的同時,也能緩解延遲和合規性方面的擔憂。到 2031 年,隨著雲端安全性的增強和關鍵任務型工作負載逐步從傳統架構遷移,各種部署模式預計將達到平衡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 聯邦政府的「雲端智慧」和「聯邦風險評估和授權計畫」(FedRAMP)正在蓬勃發展。

- 引進生成式人工智慧,打造高度個人化的客戶體驗 (CX)

- CMS支援為醫療保健行業的「數位化入口網站」提供資金。

- 美國製造業回流浪潮正在推動物聯網數位雙胞胎。

- 美國證券交易委員會氣候變遷法規推動了對ESG數據平台的投資。

- 5G SA部署支援邊緣運算應用場景。

- 市場限制因素

- 各州隱私法規的差異(例如,CPRA)

- 一級銀行對傳統大型主機的鎖定

- 雲端安全人員短缺導致整體擁有成本上升。

- 疫情時代的技術債阻礙了融合

- 價值供應鏈分析

- 產業生態系分析

- 當前市場狀況和慣例變化

- 關鍵指標

- 科技支出趨勢

- 物聯網設備數量

- 網路攻擊次數

- 雲端採用率

- 數位競爭力排名

- 監管和技術展望

- 關鍵變革性技術

- 量子計算

- Manufacturing-as-a-Service(MaaS)

- 認知過程自動化

- 奈米科技

- 波特五力模型

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 部署模式

- 現場

- 雲

- 混合

- 按公司規模

- 大公司

- 中小企業

- 按類型

- 分析、人工智慧、機器學習

- 物聯網 (IoT)

- 網路安全

- 雲端邊緣運算

- 擴增實境(XR)

- 區塊鏈

- 工業機器人

- 積層製造/3D列印

- 按最終用戶行業分類

- BFSI

- 醫療保健和生命科學

- 製造業

- 零售與電子商務

- 運輸/物流

- 石油、天然氣和公共產業

- 通訊和資訊科技服務

- 政府/公共部門

- 其他

- 按地區

- 東北

- 中西部

- 南

- 西方

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- IBM Corporation

- Google LLC(Alphabet Inc.)

- Cisco Systems, Inc.

- Oracle Corp.

- Amazon Web Services, Inc.

- Accenture plc

- Adobe Inc.

- SAP SE

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- ServiceNow, Inc.

- Salesforce, Inc.

- Cognizant Technology Solutions

- Capgemini SE

- Infosys Ltd.

- Deloitte Touche Tohmatsu Ltd.

- PwC LLP

- DXC Technology Co.

- Tata Consultancy Services Ltd.

- Schneider Electric SE

- Siemens AG

- NTT DATA Corp.

- Ericsson AB

- KPMG LLP

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states digital transformation market size was valued at USD 0.66 trillion in 2025 and estimated to grow from USD 0.79 trillion in 2026 to reach USD 1.96 trillion by 2031, at a CAGR of 19.85% during the forecast period (2026-2031).

This report is Segmented by Component (Solutions, Services), Deployment Mode (Cloud, On-Premise, Hybrid), Enterprise Size (Large Enterprises, Small and Medium Enterprises), Type (Analytics, AI and ML, Extended Reality (XR), and More), End-User Industry (BFSI, Healthcare and Life Sciences, Manufacturing, and More) and by Region. The Market Forecasts are Provided in Terms of Value (USD).

United States Digital Transformation Market Trends and Insights

Surge in Federal Cloud-Smart & FedRAMP Programs

FedRAMP 20x removes agency-sponsorship for low-impact workloads and automates security reviews, enabling federal cloud migrations to finish 60% faster. Civilian IT outlays allocate USD 74 billion for modernization in 2025, with USD 12.7 billion ring-fenced for cybersecurity. Vendors that pre-certify solutions under the codified FedRAMP Authorization Act gain preferred-supplier status, driving spillover demand across state and local agencies.

Generative-AI Adoption for Hyper-Personalized CX

Seventy-eight percent of U.S. firms now embed generative AI, producing a 3.7X ROI as Fortune 500 groups scale OpenAI-powered chat and design tools. By end-2025, 25% of enterprises plan agent-based deployments that automate frontline tasks. Sector-specific large-language models in healthcare, finance, and retail sustain compliance while boosting service quality.

State-Level Privacy Patchwork (CPRA etc.)

Nineteen states have enacted comprehensive privacy statutes, and enforcement teams in California, Texas, and Virginia elevate compliance risk. Compliance spending rises 30-50% for multi-state businesses, with SMEs bearing higher proportional costs in the absence of a single federal framework.

Other drivers and restraints analyzed in the detailed report include:

- CMS-Backed "Digital Front Door" Funding in Healthcare

- IoT & Digital-Twin Uptake from U.S. Reshoring Wave

- Legacy Mainframe Lock-in across Tier-1 Banks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for a dominant 67.40% of the United States digital transformation market share in 2025, underpinned by enterprise investments in cloud, cybersecurity, and analytics platforms. The services arena, however, is forecast to post a 20.74% CAGR as firms turn to consultancies for integration, AI model tuning, and managed operations. A widening data-science skills gap-cited by 53% of IT leaders-reinforces demand for external expertise.

Demand for continuous optimization is reshaping services portfolios from one-time installs to outcome-based contracts. Providers bundle change-management and AI-governance advisories that accelerate time-to-value. As digital maturity grows, the United States digital transformation market size for services is expected to close the revenue gap with solutions by 2031.

On-premise platforms retained 50.12% of the United States digital transformation market size in 2025, reflecting strict data-sovereignty rules in BFSI and healthcare. Cloud solutions, climbing at a 20.35% CAGR, benefit from FedRAMP streamlining and hybrid-cloud blueprints. Oracle-Google interconnects let firms run OCI databases alongside Google Analytics without cross-cloud fees.

Hybrid architectures combine on-premise control with elastic public-cloud compute, mitigating latency and compliance concerns while supporting AI workloads. By 2031, equilibrium between deployment models is plausible as cloud security hardens and mission-critical workloads gradually exit legacy stacks.

Complete Report Scope:

- By Component

- Solutions

- Services

- By Deployment Mode

- On-premise

- Cloud

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Mid-sized Enterprises (SMEs)

- By Type

- Analytics, AI and ML

- Internet of Things (IoT)

- Cyber-security

- Cloud and Edge Computing

- Extended Reality (XR)

- Blockchain

- Industrial Robotics

- Additive Manufacturing / 3-D Printing

- By End-User Industry

- BFSI

- Healthcare and Life Sciences

- Manufacturing

- Retail and E-commerce

- Transportation and Logistics

- Oil, Gas and Utilities

- Telecom and IT Services

- Government and Public Sector

- Others

- By Region

- Northeast

- Midwest

- South

- West

List of Companies Covered in this Report:

- Microsoft Corporation

- IBM Corporation

- Google LLC (Alphabet Inc.)

- Cisco Systems, Inc.

- Oracle Corp.

- Amazon Web Services, Inc.

- Accenture plc

- Adobe Inc.

- SAP SE

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- ServiceNow, Inc.

- Salesforce, Inc.

- Cognizant Technology Solutions

- Capgemini SE

- Infosys Ltd.

- Deloitte Touche Tohmatsu Ltd.

- PwC LLP

- DXC Technology Co.

- Tata Consultancy Services Ltd.

- Schneider Electric SE

- Siemens AG

- NTT DATA Corp.

- Ericsson AB

- KPMG LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Federal Cloud-Smart and FedRAMP Programs

- 4.2.2 Generative-AI Adoption for Hyper-Personalized CX

- 4.2.3 CMS-Backed "Digital Front Door" Funding in Healthcare

- 4.2.4 IoT and Digital-Twin Uptake from U.S. Reshoring Wave

- 4.2.5 ESG Data-Platform Investments Driven by SEC Climate Rules

- 4.2.6 5G SA Roll-outs Unlocking Edge-Computing Use Cases

- 4.3 Market Restraints

- 4.3.1 State-Level Privacy Patchwork (CPRA etc.)

- 4.3.2 Legacy Mainframe Lock-in across Tier-1 Banks

- 4.3.3 Cloud-Security Talent Shortage Inflating TCO

- 4.3.4 Pandemic-Era Technical Debt Hindering Integration

- 4.4 Value / Supply-Chain Analysis

- 4.5 Industry Ecosystem Analysis

- 4.6 Current Market Scenario and Evolution of Practices

- 4.7 Key Metrics

- 4.7.1 Technology Spending Trends

- 4.7.2 Number of IoT Devices

- 4.7.3 Cyber-attack Volume

- 4.7.4 Cloud-Adoption Rate

- 4.7.5 Digital Competitiveness Ranking

- 4.8 Regulatory and Technological Outlook

- 4.9 Key Transformative Technologies

- 4.9.1 Quantum Computing

- 4.9.2 Manufacturing-as-a-Service (MaaS)

- 4.9.3 Cognitive Process Automation

- 4.9.4 Nanotechnology

- 4.10 Porter's Five Forces

- 4.10.1 Competitive Rivalry

- 4.10.2 Bargaining Power of Buyers

- 4.10.3 Bargaining Power of Suppliers

- 4.10.4 Threat of New Entrants

- 4.10.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-sized Enterprises (SMEs)

- 5.4 By Type

- 5.4.1 Analytics, AI and ML

- 5.4.2 Internet of Things (IoT)

- 5.4.3 Cyber-security

- 5.4.4 Cloud and Edge Computing

- 5.4.5 Extended Reality (XR)

- 5.4.6 Blockchain

- 5.4.7 Industrial Robotics

- 5.4.8 Additive Manufacturing / 3-D Printing

- 5.5 By End-User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Manufacturing

- 5.5.4 Retail and E-commerce

- 5.5.5 Transportation and Logistics

- 5.5.6 Oil, Gas and Utilities

- 5.5.7 Telecom and IT Services

- 5.5.8 Government and Public Sector

- 5.5.9 Others

- 5.6 By Region

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 IBM Corporation

- 6.4.3 Google LLC (Alphabet Inc.)

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Oracle Corp.

- 6.4.6 Amazon Web Services, Inc.

- 6.4.7 Accenture plc

- 6.4.8 Adobe Inc.

- 6.4.9 SAP SE

- 6.4.10 Dell Technologies Inc.

- 6.4.11 Hewlett Packard Enterprise Co.

- 6.4.12 ServiceNow, Inc.

- 6.4.13 Salesforce, Inc.

- 6.4.14 Cognizant Technology Solutions

- 6.4.15 Capgemini SE

- 6.4.16 Infosys Ltd.

- 6.4.17 Deloitte Touche Tohmatsu Ltd.

- 6.4.18 PwC LLP

- 6.4.19 DXC Technology Co.

- 6.4.20 Tata Consultancy Services Ltd.

- 6.4.21 Schneider Electric SE

- 6.4.22 Siemens AG

- 6.4.23 NTT DATA Corp.

- 6.4.24 Ericsson AB

- 6.4.25 KPMG LLP

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

印尼數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)IT產業的循環經濟平台:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

印尼數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)IT產業的循環經濟平台:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 2026-2030年全球石油天然氣產業數位轉型市場

2026-2030年全球石油天然氣產業數位轉型市場 技術創新正在改變機場:市場展望(2025-2035 年)

技術創新正在改變機場:市場展望(2025-2035 年) 數位轉型市場規模、佔有率和趨勢分析報告:按類型、部署模式、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

數位轉型市場規模、佔有率和趨勢分析報告:按類型、部署模式、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 鐵路貨運數位轉型市場分析與預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、實施、最終用戶和解決方案分類

鐵路貨運數位轉型市場分析與預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、實施、最終用戶和解決方案分類 數位轉型市場:依產品類型、部署模式、組織規模、業務職能與產業分類-2026-2032年全球市場預測

數位轉型市場:依產品類型、部署模式、組織規模、業務職能與產業分類-2026-2032年全球市場預測 2026年全球數位轉型諮詢服務市場報告

2026年全球數位轉型諮詢服務市場報告 數位轉型市場規模、佔有率、趨勢和預測:按類型、部署模式、企業規模、最終用戶產業和地區分類,2026-2034 年

數位轉型市場規模、佔有率、趨勢和預測:按類型、部署模式、企業規模、最終用戶產業和地區分類,2026-2034 年