|

市場調查報告書

商品編碼

2073015

IT產業的循環經濟平台:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Circular Economy Platform For The IT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

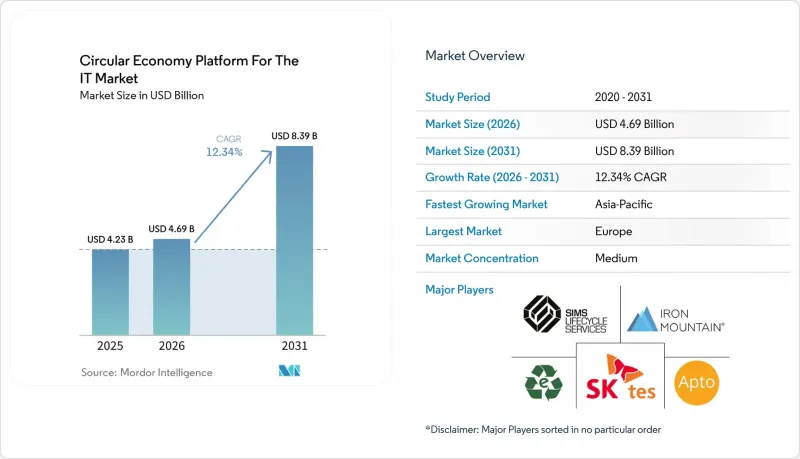

根據 Mordor Intelligence 預測,IT 循環經濟平台的市場規模預計將在 2025 年達到 42.3 億美元,2026 年達到 46.9 億美元,到 2031 年達到 83.9 億美元,2026 年至 2031 年的複合年成長率為 12.34%。

本報告按產品(軟體平台和服務)、部署模式(雲端、本地部署、混合部署)、企業規模(大型企業和中小企業)、循環經濟應用領域(資產再利用和重新部署、再生、IT資產處置(ITAD)、回收和再利用等)以及地區進行細分。市場預測以美元(USD)為單位。

全球以IT為中心的循環經濟平台市場趨勢與洞察

企業對IT資產可追溯性的需求日益成長

IT循環經濟平台的主要驅動力在於追蹤資產從部署到資料抹除和最終處置的整個過程。對於擁有多個辦公地點和供應商的大型企業而言,分散在電子表格中的記錄以及缺乏協調的服務供應商使得合規性、ESG績效或範圍3課責的證明變得不可能。一家供應商報告稱,在2025會計年度,其IT資產的再利用率達到了880萬,這一規模凸顯了隨著不同地區和設備類別的退役進程,保持一致的可追溯性的重要性。另一個平台能夠定位並自動視覺化伺服器和磁碟機上的序號資產,並繪製出父子關係圖。這表明,可追溯性不僅僅是一項附加功能,而是產品的核心差異化優勢。一旦建立了這種程度的可視性,企業就可以將廢棄硬體視為可衡量的回收來源,而不僅僅是處置成本。這也將改變採購團隊評估平台部署的方式。

對電子廢棄物報告和審計的監管壓力

人們對IT循環經濟平台的興趣日益濃厚,部分原因是主要經濟體對電子廢棄物報告和審計的監管日益細緻化。 2025年7月的報告指出,歐盟產生的近一半廢棄電子電氣設備(WEEE)仍未被收集,回收率僅40%,且只有23%的回收設施符合高品質的處理標準,這導致人們越來越希望加強監管。義大利已將2026年1月生效的歐盟指令(EU) 2024/884納入其國內法。這將改變WEEE框架的部分內容以及生產者延伸責任下的資金籌措責任。在德國,生產者定期報告仍然是強制性的,歐盟條例(EU) 2025/40將於2026年8月生效。因此,許多公司現在面臨跨司法管轄區的重疊文件義務。這些層層疊加的時間表推動了對軟體和受控工作流程的需求,這些軟體和工作流程無需人工核對即可協調報告、註冊和審計記錄。

資產數據分散在原有的 IT 環境中

IT循環經濟平台仍面臨許多營運難題。許多公司缺乏對其已部署硬體基礎設施的準確統一的記錄。序號、所有權歷史、安裝位置資料和退役狀態等資訊通常分散在不同的ERP、IT資產管理(ITAM)和區域系統中,導致部署流程延誤並增加成本。對於透過收購和系統遷移而擴張的大型企業而言,這個問題尤其突出,因為這些企業通常需要在啟動退役工作流程之前進行資產發現專案。一家供應商專門建立了一個資產發現層,以解決現場驗證資訊與客戶庫存管理系統中顯示的序號層級差異。這足以說明該問題的普遍性。在上游資料品質得到改善之前,許多買家將繼續面臨整合方面的負擔,這會延遲價值實現並限制平台部署後的使用。

細分市場分析

2025年,軟體平台在IT市場循環經濟平台佔有率中佔比高達68.74%。這顯示企業更傾向於集中式系統,以便整合資產發現、資料擦除記錄、處置路徑確定和ESG文件等功能。市場轉向這一方向的原因在於,人工流程和單獨的回收合約無法產生滿足當前合規要求所需的序號記錄。隨著GDPR、WEEE及相關揭露要求對資產層面的文件記錄提出更高要求,基於軟體的管理層已成為創建大規模、可操作審計追蹤的最便捷方式。此外,尤其是在硬體分佈於多個業務部門和國家的情況下,買家非常重視能夠在一個平台上查看設備狀態、證書和回收結果。因此,即使服務交付仍依賴實體回收、維修和轉售業務,軟體平台在經營模式中仍佔據核心地位。

服務是成長最快的交付模式,預計2026年至2031年間,該領域的IT循環經濟平台市場將以12.85%的複合年成長率成長。當企業缺乏內部ITAD(資訊科技資產處置)專業知識,或AI伺服器升級活動使處置週期管理變得困難時,它們擴大採用託管服務模式。 AI伺服器部署的數量已被認為是未來ITAD面臨的主要挑戰,凸顯了能夠提供安全移除、評級和恢復等持續服務的供應商的重要性。在安全性和回收方面擁有良好業績記錄的服務供應商也贏得了更多企業競標,因為買家要求由單一責任實體負責監管鏈、文件和管轄權報告。

預計到2025年,雲端運算將佔據65.12%的市場佔有率,這反映了其低初始基礎設施成本和跨地域快速部署的優勢。 「雲端優先」的IT循環經濟平台策略源自於許多組織希望在不擴展其本地IT架構的情況下,實現即時資產追蹤、自動化報告和多地點視覺性。這些優勢對於需要建立基礎設施但又不想營運本地平台的中型和新興科技公司尤其重要。然而,完全部署公共雲端並不適用於所有工作流程,因為資產記錄、資料擦除憑證和客戶資料通常儲存在受監管的環境中。因此,部署模式的選擇越來越受到合規性和資料處理要求的驅動,而不僅僅是架構偏好。

混合部署模式是成長最快的部署模式,IT市場的循環經濟平台細分領域預計將在2026年至2031年間以12.92%的複合年成長率成長。修訂後的標準強調了程序級文件和更嚴格的營運控制的重要性,使得混合部署更適合那些希望在本地管理敏感記錄,同時利用雲端進行報告和合作夥伴協作的組織。在歐洲,有關跨境合規和資料管理的嚴格法規進一步推動了這一趨勢。中國也正在透過電子產品資訊授權的國家標準,朝著更嚴格的管控方向發展。因此,混合設計正成為受監管行業買家和跨司法管轄區營運公司的事實標準。

區域分析

2025年,歐洲繼續保持其最大區域市場的地位,佔據IT循環經濟平台市場佔有率的34.56%。歐洲IT循環經濟平台市場的強勁地位源於其將廢棄電子電氣設備(WEEE)的回收、更廣泛的永續性資訊揭露壓力以及更嚴格的生產者責任整合於單一營運環境。根據2025年7月的評估,回收和處理成果仍未達到政策目標,凸顯了製定更嚴格的法規和更完善的報告體系的必要性。義大利於2026年1月將歐盟指令(EU) 2024/884納入國內法,加上德國引入的報告框架,在更廣泛的歐盟框架之外,也增加了國家層面的行政壓力。這種組合確保了歐洲繼續保持其主導地位,因為該地區的企業如果沒有正式平台的支持,幾乎沒有切實可行的方法來管理其廢棄的IT資產。

北美仍然是第二大市場,這主要得益於聯邦採購要求、企業廢棄物處理需求以及對媒體資料擦除日益成長的期望。美國IT循環經濟平台的發展也得益於NIST資料擦除框架的更新以及超大規模資料中心硬體更新周期的加速。 2026年第一季,資產生命週期管理收入達2.32億美元,年增92%。資料中心退役的內部成長超過100%,顯示該地區企業和超大規模資料中心業者中心業務的快速擴張。雖然南美市場規模較小且標準化程度較低,但隨著企業在預算緊張的情況下越來越依賴翻新、搬遷和託管處置來延長硬體價值,市場需求正在不斷成長。

亞太地區是成長最快的地區,預計到2031年,該地區IT市場的循環經濟平台規模將以13.12%的複合年成長率成長。儘管亞太市場正在快速擴張,但各國的促進因素卻各不相同。日本正在建立更強大的商業性夥伴關係,中國正在收緊資料清除和處理標準,而印度則在吸引新的處理能力。中國於2025年12月頒布的電子產品資訊清除強制性國家標準,為企業的資料抹除和處置流程提供了明確的合規動力。在日本,一項於2026年4月達成的資本與商業聯盟正在建構一條涵蓋採購、第三方維護、再行銷和IT資產處置(ITAD)的循環技術價值鏈。印度、澳洲和韓國仍處於採用曲線的早期階段,而中東和非洲仍處於起步階段,需求集中在沙烏地阿拉伯和阿拉伯聯合大公國等市場,主要集中在智慧城市、數位基礎設施和資料中心現代化項目上。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業對IT資產可追溯性的需求日益成長

- 對電子廢棄物報告和審計的監管壓力

- 安全資料擦除的要求不斷提高

- 推動循環採購的公司所追求的ESG目標

- 人工智慧驅動的資產估值和維修流程

- 涉及多家供應商的車隊日益複雜,這正在推動平台的普及。

- 市場限制因素

- 分散在傳統 IT 環境中的資產數據

- 全球各地的收集項目缺乏標準化

- 資料銷毀和儲存環節的信任缺失

- 與現有ITAD和經銷商合作夥伴的通路競爭

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體平台

- 服務

- 按部署模式

- 雲

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 循環經濟的應用

- 資產再利用和重新分配

- 回收利用

- ITAD

- 回收和收集

- 環境、社會及治理 (ESG) 和合規報告

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sims Lifecycle Services, Inc.

- Electronic Recyclers International, Inc.

- Iron Mountain Incorporated

- TES-Amm(Singapore)Pte Ltd.

- Apto Solutions, Inc.

- SK Tes Pte. Ltd.

- ERS International AG

- Ingram Micro Inc.

- Jabil Inc.

- Flex Ltd.

- Hewlett Packard Enterprise Company

- HP Inc.

- Dell Technologies Inc.

- Lenovo Group Limited

- Canon Inc.

- Kyocera Corporation

- Sharp Corporation

- Cisco Systems, Inc.

- Oracle Corporation

- SAP SE

第7章 市場機會與未來展望

According to Mordor Intelligence, the circular economy platform for the IT market is projected to reach USD 4.23 billion in 2025, USD 4.69 billion in 2026, and USD 8.39 billion by 2031, growing at a CAGR of 12.34% from 2026 to 2031.

This report is Segmented by Offering (Software Platform, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Circular Economy Application (Asset Reuse and Redeployment, Refurbishment, ITAD, Recycling and Recovery, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Circular Economy Platform For The IT Market Trends and Insights

Rising Enterprise Demand for IT Asset Traceability

The circular economy platform for the IT market is seeing its strongest push from the need to track assets from deployment through data erasure and final disposition. Large enterprises with multi-site and multi-vendor estates cannot demonstrate compliance, ESG performance, or Scope 3 accountability when records are scattered across spreadsheets and disconnected service providers. One provider reported repurposing 8.8 million IT assets in FY2025, a scale that underscores the importance of consistent traceability as decommissioning moves across regions and device classes. Another platform positioned serialized asset discovery and parent-child relationship mapping across servers and drives to automate visibility, reflecting how traceability has become a core product differentiator rather than a background feature. When that level of visibility is in place, enterprises can treat retired hardware as a measurable recovery stream rather than a disposal cost line, which changes how procurement teams value platform adoption.

Regulatory Pressure on E-Waste Reporting and Audits

The circular economy platform for the IT market is also moving higher because e-waste reporting and audit rules are becoming more detailed across major economies. In July 2025, it was reported that nearly half of WEEE generated in the EU remained uncollected, only 40% was recycled, and just 23% of recycling facilities applied high-quality treatment standards, which is increasing pressure for tighter oversight.Italy brought Directive (EU) 2024/884 into national law with effect from January 2026, which changed parts of the WEEE framework and financing responsibilities under extended producer responsibility. Germany's system continues to require recurring producer reporting, and Regulation (EU) 2025/40 will apply from August 2026, meaning many enterprises now face overlapping documentation duties across jurisdictions. These layered timelines are increasing the demand for software and managed workflows that can keep reporting, registration, and audit records aligned without manual reconciliation.

Fragmented Asset Data Across Legacy IT Environments

The circular economy platform for the IT market still faces a major operational barrier: many enterprises lack clean, unified records of their installed hardware base. Serial numbers, ownership history, location data, and end-of-life status often reside across different ERP, ITAM, and regional systems, which slows onboarding and increases its cost. The issue is most visible in large organizations that expanded through acquisitions or system migrations, because they often need a discovery project before disposition workflows can even start. One provider's asset discovery layer was built to reconcile serial-level gaps between what is found in the field and what appears in client inventory systems, which shows how common this problem remains. Until upstream data quality improves, many buyers will continue to face an integration burden that delays value realization and limits platform usage after deployment

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Secure Data Sanitization Requirements

- Corporate ESG Targets Driving Circular Procurement

- Limited Standardization Across Global Take-Back Programs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms accounted for 68.74% of the circular economy platform share in the IT market in 2025, indicating that enterprises favored centralized systems that could tie together asset discovery, data erasure records, disposition routing, and ESG documentation. The market moved in this direction because manual processes and separate recycling engagements did not produce the serialized records required to meet current compliance expectations. As GDPR, WEEE, and related disclosure requirements demand clearer asset-level documentation, software-based control layers have become the simplest way to create a usable audit trail at scale. Buyers also value the ability to view device status, certificates, and recovery outcomes in one place, especially when hardware is spread across multiple business units and countries. This keeps software platforms at the center of the commercial model even when service delivery still happens through physical collection, repair, and remarketing operations.

Services are the fastest-growing offering type, and the circular economy platform for the IT market size for this segment is projected to expand at a 12.85% CAGR from 2026 to 2031. Enterprises are turning to managed service models when they lack internal ITAD expertise or when decommissioning cycles are becoming harder to manage due to AI server refresh activity. The installed base of AI servers has been identified as a major future ITAD challenge, underscoring the need for providers that can manage secure removal, grading, and recovery as an ongoing service. Service providers with recognized security and recycling credentials are also winning more enterprise tenders because buyers want a single accountable party for chain of custody, documentation, and jurisdiction-specific reporting.

Cloud held a 65.12% share in 2025, reflecting the appeal of lower upfront infrastructure costs and faster rollouts across distributed locations. The circular economy platform for the IT market adopted a cloud-first approach because many organizations wanted real-time asset tracking, automated reporting, and multi-site visibility without expanding their internal IT stacks. These benefits were especially relevant for mid-sized companies and newer technology businesses that needed structure but did not want to run an on-premises platform. At the same time, a full public cloud deployment does not suit every workflow because asset records, sanitization proofs, and customer data often reside in regulated environments. This is why deployment choice is increasingly shaped by compliance and data-handling needs rather than by pure architectural preference.

Hybrid is the fastest-growing deployment model, and the circular-economy platform for the IT market in this segment is projected to expand at a 12.92% CAGR from 2026 to 2031. Updated standards reinforced the need for program-level documentation and stronger operational controls, making hybrid deployment more suitable for organizations that need local control over sensitive records while still using cloud layers for reporting and partner coordination. Europe adds another pull factor because cross-border compliance and data management rules remain stricter, and China has also moved toward tighter controls through its national standard on electronic product information clearance. As a result, hybrid design is becoming the practical default for enterprise buyers that operate across regulated sectors or multiple jurisdictions.

Complete Report Scope:

- By Offering

- Software Platform

- Services

- By Deployment Model

- Cloud

- On Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small And Medium Enterprises

- By Circular Economy Application

- Asset Reuse and Redeployment

- Refurbishment

- ITAD

- Recycling and Recovery

- ESG and Compliance Reporting

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

Europe accounted for 34.56% of the circular economy platform for the IT market share in 2025, maintaining its position as the largest regional market. The circular economy platform for the IT market is strongest in Europe because the region combines WEEE, broader sustainability disclosure pressures, and tighter producer accountability within a single operating environment. A July 2025 evaluation found that collection and treatment results still fall short of policy goals, and that gap reinforces the case for tighter controls and better reporting systems. Italy's January 2026 transposition of Directive (EU) 2024/884 and Germany's reporting framework add country-level administrative pressure on top of the wider EU framework. This combination keeps Europe ahead because enterprises in the region have fewer practical ways to manage end-of-life IT assets without formal platform support.

North America remained the second-largest region, supported by federal procurement requirements, enterprise decommissioning demand, and stronger media sanitization expectations. The circular economy platform for the IT market in the United States is also being lifted by the updated NIST sanitization framework and by faster hardware turnover in hyperscale data centers. Asset lifecycle management revenue reached USD 232 million in Q1 2026, up 92% year on year, with organic data center decommissioning growth exceeding 100%, demonstrating how quickly enterprise and hyperscaler activity is scaling in the region. South America remains smaller and less standardized, but demand is growing as enterprises lean more heavily on refurbishment, redeployment, and controlled disposal to extend hardware value under tighter budgets.

Asia-Pacific is the fastest-growing region, and the circular economy platform for the IT market size there is projected to grow at a 13.12% CAGR through 2031. The market is expanding quickly across Asia-Pacific, but the drivers differ by country: Japan is building stronger commercial partnerships, China is tightening clearance and information-handling standards, and India is attracting new processing capacity. A mandatory national standard published in December 2025 for electronic product information clearance adds a clear compliance trigger for enterprise sanitization and disposal workflows in China. In Japan, a capital and business alliance signed in April 2026 is building a circular tech value chain spanning procurement, third-party maintenance, remarketing, and ITAD. India, Australia, and South Korea remain earlier in their adoption curves, while the Middle East and Africa are still nascent, with demand centered on smart-city, digital infrastructure, and data-center modernization programs in markets such as Saudi Arabia and the UAE.

- Sims Lifecycle Services, Inc.

- Electronic Recyclers International, Inc.

- Iron Mountain Incorporated

- TES-Amm (Singapore) Pte Ltd.

- Apto Solutions, Inc.

- SK Tes Pte. Ltd.

- ERS International AG

- Ingram Micro Inc.

- Jabil Inc.

- Flex Ltd.

- Hewlett Packard Enterprise Company

- HP Inc.

- Dell Technologies Inc.

- Lenovo Group Limited

- Canon Inc.

- Kyocera Corporation

- Sharp Corporation

- Cisco Systems, Inc.

- Oracle Corporation

- SAP SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Enterprise Demand for IT Asset Traceability

- 4.2.2 Regulatory Pressure on E-Waste Reporting And Audits

- 4.2.3 Expansion of Secure Data Sanitization Requirements

- 4.2.4 Corporate ESG Targets Driving Circular Procurement

- 4.2.5 AI Enabled Asset Grading and Refurbishment Workflows

- 4.2.6 Multi-Vendor Fleet Complexity Increasing Platform Adoption

- 4.3 Market Restraints

- 4.3.1 Fragmented Asset Data across Legacy IT Environments

- 4.3.2 Limited Standardization across Global Take-Back Programs

- 4.3.3 Trust Gaps Around Data Destruction and Chain of Custody

- 4.3.4 Channel Conflict with Incumbent ITAD and Resale Partners

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software Platform

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On Premises

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small And Medium Enterprises

- 5.4 By Circular Economy Application

- 5.4.1 Asset Reuse and Redeployment

- 5.4.2 Refurbishment

- 5.4.3 ITAD

- 5.4.4 Recycling and Recovery

- 5.4.5 ESG and Compliance Reporting

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sims Lifecycle Services, Inc.

- 6.4.2 Electronic Recyclers International, Inc.

- 6.4.3 Iron Mountain Incorporated

- 6.4.4 TES-Amm (Singapore) Pte Ltd.

- 6.4.5 Apto Solutions, Inc.

- 6.4.6 SK Tes Pte. Ltd.

- 6.4.7 ERS International AG

- 6.4.8 Ingram Micro Inc.

- 6.4.9 Jabil Inc.

- 6.4.10 Flex Ltd.

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 HP Inc.

- 6.4.13 Dell Technologies Inc.

- 6.4.14 Lenovo Group Limited

- 6.4.15 Canon Inc.

- 6.4.16 Kyocera Corporation

- 6.4.17 Sharp Corporation

- 6.4.18 Cisco Systems, Inc.

- 6.4.19 Oracle Corporation

- 6.4.20 SAP SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White Space and Unmet Need Assessment

美國數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印尼數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

美國數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)印尼數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度數位轉型:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2030年全球石油天然氣產業數位轉型市場

2026-2030年全球石油天然氣產業數位轉型市場 技術創新正在改變機場:市場展望(2025-2035 年)

技術創新正在改變機場:市場展望(2025-2035 年) 數位轉型市場規模、佔有率和趨勢分析報告:按類型、部署模式、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

數位轉型市場規模、佔有率和趨勢分析報告:按類型、部署模式、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 鐵路貨運數位轉型市場分析與預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、實施、最終用戶和解決方案分類

鐵路貨運數位轉型市場分析與預測(至2035年):按類型、產品類型、服務、技術、組件、應用、流程、實施、最終用戶和解決方案分類 數位轉型市場:依產品類型、部署模式、組織規模、業務職能與產業分類-2026-2032年全球市場預測

數位轉型市場:依產品類型、部署模式、組織規模、業務職能與產業分類-2026-2032年全球市場預測 2026年全球數位轉型諮詢服務市場報告

2026年全球數位轉型諮詢服務市場報告 數位轉型市場規模、佔有率、趨勢和預測:按類型、部署模式、企業規模、最終用戶產業和地區分類,2026-2034 年

數位轉型市場規模、佔有率、趨勢和預測:按類型、部署模式、企業規模、最終用戶產業和地區分類,2026-2034 年