|

市場調查報告書

商品編碼

2073657

北美電動車鋰離子電池:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)North America Lithium-ion Battery For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

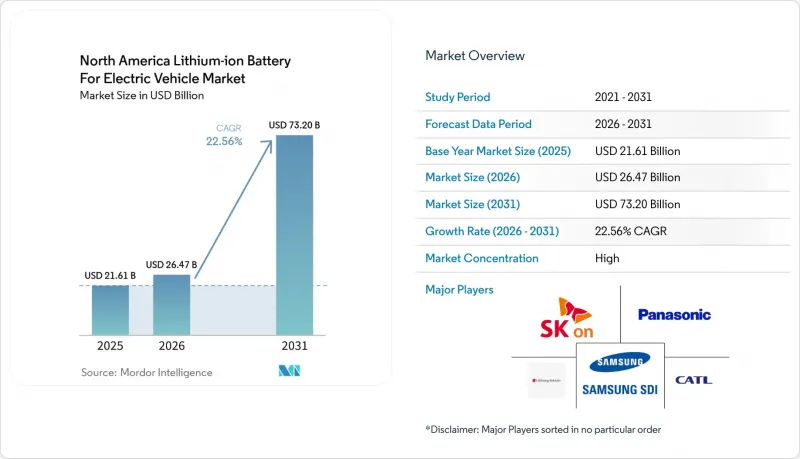

根據 Mordor Intelligence 預測,北美電動車鋰離子電池市場規模預計在 2025 年達到 216.1 億美元,在 2026 年達到 264.7 億美元,在 2031 年達到 732 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 22.56%。

本報告按電池化學成分(鋰離子電池、新興化學成分電池、鉛酸電池、鎳氫電池)、電池形狀(圓柱形、棱柱形、軟包型)、驅動系統(純電動車、插電式混合動力車、混合動力車)、車輛類型(乘用車、輕型商用車、中重型卡車、巴士、摩托車和三輪車)以及地區進行細分(美國、加拿大、中重型卡車、巴士、摩托車和三輪車)以及市場預測以美元計價。

北美電動車鋰離子電池市場趨勢與洞察。

鋰離子電池價格的下降正在降低成本障礙。

在北美電動車鋰離子電池市場,電池組價格的持續下降是最大的成本降低因素。電池組成本已從2018年的每千瓦時約300美元降至2026年的每千瓦時95至115美元,提高了車輛的價格競爭力,並緩解了汽車製造商的利潤壓力。然而,這種利好並不均衡,因為儘管生產補貼縮小了部分本地生產帶來的價格差異,但美國製造的磷酸鋰電池仍然比中國製造的同類產品更貴。這種成本差距促使北美電動車鋰離子電池市場更採用價格敏感的中檔車和商用,而非豪華乘用車。通用汽車表示,在其部分產品線中從鎳基複合材料電池(NMC)轉向磷酸鐵鋰電池,每輛車至少可節省6000美元的電池成本,這表明如今電池化學成分的選擇對零售價格的影響與車輛設計同樣重要。此外,新電池價格的下降降低了其在二手電池回收中對某些成本敏感的車隊應用的吸引力,使得直接回收利用(一種替代廢棄電池組漫長再利用鏈的方法)更具吸引力。

擴大電動車車型範圍並提供購車獎勵將增加潛在需求。

北美電動車鋰離子電池市場正受惠於乘用車和商用車領域電動車車型的持續豐富。預計中型和大型電動車車型數量將從2019年的24款增至2025年的161款,大幅擴大了車隊營運商和公共部門買家的選擇。產品線的擴張推動了電池需求,因為專用電動車平台能夠適應更多運作週期,而無需依賴有限的試點車型。加州的「先進清潔車II」法規以及其他州類似法規的實施預計將在未來十年推動監管需求,從而降低北美電動車市場鋰離子電池需求激增為暫時性的風險。儘管隨著2025年9月第30D條消費者稅額扣抵的結束,需求結構發生了變化,但由於商業業者仍可利用租賃相關的支援措施,車隊電氣化進程仍比預期更為強勁。這項變化意義重大。這是因為車隊需求通常需要比消費者零售需求更大容量的電池,而且往往是週期性的,並有明確的更換週期,因此為北美電動車鋰離子電池提供了更穩定的銷售量基礎。

一級鎳的原料供應瓶頸限制了鎳基合金的經濟效益。

北美電動車鋰離子電池市場仍嚴重依賴進口一級鎳,這對高鎳含量正極材料的原料供應構成重大風險。美國鎳加工能力不足全球整體3%,其位於密西根州的唯一一座運作中的鎳礦預計將於2025年底停產,這將進一步加劇美國對外部鎳源的依賴。印尼已在全球鎳生產中佔據主導地位,其鎳產量很大程度上依賴中國企業的加工,這導致其在聯邦能源監管委員會(FEOC)相關法規下面臨《通貨膨脹控制法案》(IRA)合格問題。因此,在北美電動車鋰離子電池市場,儘管天然金屬電池(NMC)在高階車型中仍具有更高的能量密度,但磷酸鐵鋰(LFP)在中階車型中正逐漸獲得成本優勢。雖然加拿大和美國正在加強其本地供應鏈,但專案進度和規模仍存在不確定性,這意味著鎳在中期內仍將是供應阻礙因素。

細分市場分析

2025年,鋰離子電池的化學成分將佔總銷售量的90.9%,使其成為北美電動車鋰離子電池市場(基準年)的核心。北美電動車鋰離子電池市場仍然高度依賴高階搭乘用電動車的NMC(自然微波控制)技術,因為高能量密度仍然是長續航里程平台的首要考慮因素。 NCA(自然微波控制)技術也仍然重要,尤其是在某些採用圓柱形電池結構且已有成熟生產線的高效能應用中。由於其成本低、安全性高,LFP(低頻電位)電池在中檔乘用車和商用車平台上的應用正在迅速擴展,這符合大規模生產專案的需求。通用汽車和LG能源解決方案公司正在將其美國產能轉向LFP電池的生產,這表明已公佈的工廠計劃不僅基於技術續航里程目標,也基於實際成本目標進行審查。

鉛酸電池和鎳氫電池在輕度混合動力汽車和輔助系統中仍然發揮著有限的作用,但隨著低壓架構加速向鋰離子電池過渡,它們的地位正在下降。新興電池化學公司在2025年的市佔率微乎其微,但預計到2031年將成長34.1%,成為北美電動車鋰離子電池市場成長最快的電池化學公司。 2026年4月,日產宣布其23層級構造固態電池原型包達到充放電基準,並計畫於2028年上市,同時維持每度75美元的價格目標。這清楚地表明,固態電池技術在量產前取得了顯著進展。同時,通用汽車和福特汽車正在開發的鋰錳電池可能會在全固態電池實現量產之前,拓寬未來的電池化學選擇範圍。簡而言之,市場可能會保持多元化,而不是只剩下兩種簡單的化學結構。

預計到2025年,圓柱形電芯將繼續在北美電動車鋰離子電池市場佔據領先地位,市佔率高達51.9%。圓柱形電芯之所以在北美電動車鋰離子電池市場備受青睞,部分原因在於松下在內華達州建立了大型2170型電芯生產基地,隨後將生產擴展到堪薩斯州的Panasonic。特斯拉的4680型電芯策略也推動了這一趨勢,因為這種規格的電芯與該公司的重型車輛和皮卡項目密切相關,這些項目需要高功率和成熟的本土化生產流程。軟包電芯在需要客製化封裝和平台特定佈局的領域中仍然發揮作用,並在一些合資項目的搭乘用電動車架構中繼續使用。然而,圓柱形電芯目前的領先地位並不能否認棱柱形電芯在北美電動車鋰離子電池市場的結構吸引力正在不斷增強。

預計到2031年,棱柱形電芯市場將以25.3%的年成長率成長,成為成長最快的電芯規格細分市場。這一成長反映了三個相互關聯的變化:磷酸鋰鐵(LFP)的廣泛應用、電芯到電池包一體化設計(Cell-to-pack design)的普及,以及商用車市場對棱柱形電芯模組化電池包製造的需求不斷成長。大眾汽車位於聖托馬斯的PowerCo工廠正圍繞棱柱形「統一電芯」進行建設,目標年產能為90吉瓦時(GWh),這將使該地區未來成為大眾汽車(VW.CA)重要的本地生產中心。即將修訂的《美墨加協定》(USMCA)可能會進一步有利於已在協定區內生產棱柱形電芯的製造商,因為在北美電動汽車鋰離子電池市場,遵守原產地規則的重要性正變得與單純的產量同等重要。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 鋰離子電池價格正在下降。

- 擴大電動車車型範圍及購車獎勵

- 北美電池製造產能擴張

- OEM廠商與電池製造商之間的長期採購協議

- 高矽陽極技術突破(2028 年後)

- 面向車隊的二次電池租賃模式

- 市場限制因素

- 一級鎳原料供應瓶頸

- 北美新鋰礦工程許可核准流程延誤

- 加州以外地區的回收法規存在不確定性

- 火災後的熱失控造成了聲譽風險,引起了廣泛關注。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按電池化學成分

- 鋰離子電池(NMC、LFP、NCA)

- 新興技術(全固體、鋰硫、鈉離子)

- 鉛酸

- 鎳氫電池

- 按細胞形狀

- 圓柱形

- 棱柱型

- 袋式

- 透過驅動系統

- 電池式電動車(BEV)

- 插電式混合動力車(PHEV)

- 混合動力電動車(HEV)

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型卡車

- 巴士和長途汽車

- 二輪車和三輪車

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- LG Energy Solution Ltd

- Panasonic Holdings Corporation

- SK On Co. Ltd

- Contemporary Amperex Technology Co. Ltd(CATL)

- Samsung SDI Co. Ltd

- BYD Company Ltd

- A123 Systems LLC

- EnerSys

- E-One Moli Energy Corp.

- VARTA AG

- Microvast Holdings Inc.

- Farasis Energy Inc.

- Romeo Power Inc.

- Northvolt AB

- Gotion High-Tech Co. Ltd

- Clarios LLC

- Envision AESC Group Ltd

- Tesla Inc.(Cell Manufacturing)

- FREYR Battery

- Solid Power Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america lithium-ion battery for electric vehicle market size is projected to be USD 21.61 billion in 2025, USD 26.47 billion in 2026, and reach USD 73.20 billion by 2031, growing at a CAGR of 22.56% from 2026 to 2031.

This report is Segmented by Battery Chemistry (Lithium-Ion, Emerging Chemistries, Lead-Acid, Nickel-Metal-Hydride), Cell Format (Cylindrical, Prismatic, Pouch), Propulsion (BEV, PHEV, HEV), Vehicle Type (Passenger Cars, Lcvs, Medium and Heavy Trucks, Buses, Two and Three-Wheelers), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Lithium-ion Battery For Electric Vehicle Market Trends and Insights

Declining Lithium-Ion Battery Prices Compressing Cost Barriers

The North America EV lithium-ion battery market is seeing its strongest cost support from the continued fall in battery pack prices. Pack-level costs fell from near USD 300 per kWh in 2018 to USD 95 to USD 115 per kWh in 2026, which improves vehicle affordability and eases pressure on automaker margins. The benefit is still uneven because US-made LFP cells remain more expensive than the Chinese supply, even after production credits narrow part of the gap for local manufacturing economics. That cost spread is pushing the North America EV lithium-ion battery market toward wider LFP adoption in mid-range vehicles and work fleets, where price sensitivity is stronger than in premium passenger programs. GM has stated that shifting from NMC to LFP in part of its portfolio could lower battery cost by at least USD 6,000 per vehicle, which shows how chemistry choice now affects retail pricing as much as vehicle engineering. Lower new-cell prices are also making second-life reuse less attractive in some cost-sensitive fleet applications, which increases the appeal of direct recycling instead of long reuse chains for retired packs.

Growing EV Model Availability and Purchase Incentives Broadening Addressable Demand

The North America EV lithium-ion battery market is benefiting from a wider range of EV models across passenger and commercial categories. Electric medium and heavy-duty vehicle model availability rose from 24 models in 2019 to 161 models by 2025, which materially broadened purchasing options for fleet operators and public buyers. This wider product base is reinforcing battery demand because more duty cycles can now be matched with dedicated electric platforms rather than limited pilot models. California's Advanced Clean Cars II rule and its adoption by additional states are keeping regulatory demand visible into the next decade, which reduces the risk of a short-lived demand spike in the North America EV lithium-ion battery market. The end of the Section 30D consumer credit in September 2025 changed the demand mix, yet commercial operators still retain access to leasing-related support, which has helped fleet electrification hold up better than expected. That shift matters because fleet demand usually involves larger batteries, repeat ordering behavior, and clearer replacement cycles than private retail demand, which gives the North America EV lithium-ion battery market a steadier volume base.

Raw-Material Supply Bottlenecks for Class-1 Nickel Constraining NMC Economics

The North America EV lithium-ion battery market remains exposed to imported Class-1 nickel, which keeps a key input risk in place for high-nickel cathode chemistries. The United States holds less than 3% of global nickel processing capacity, and its only operating nickel mine in Michigan was expected to cease production by the end of 2025, which raises dependence on external supply. Indonesia already dominates global nickel production, and much of that material is tied to Chinese-affiliated processing, which creates IRA eligibility problems under FEOC-related restrictions. As a result, the North America EV lithium-ion battery market is seeing a stronger cost case for LFP in mid-range applications, even when NMC still offers better energy density for premium models. Canada and the United States are trying to improve local supply links, but project timing and scaling remain uncertain enough that nickel will stay a constraint over the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Scale-Up of North American Cell Manufacturing Capacity Creating Supply-Side Density

- OEM-Battery Maker Long-Term Offtake Agreements Locking in Supply Visibility

- Thermal-Runaway Reputation Risk Elevating Safety Engineering Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion chemistries held 90.9% of revenue in 2025, which placed this segment at the center of the North America EV lithium-ion battery market size in the base year. The North America EV lithium-ion battery market still relies on NMC for premium passenger EVs because long-range platforms continue to prioritize high energy density. NCA also remains relevant in selected high-performance applications, especially where cylindrical formats and proven production lines already exist. LFP is expanding quickly in mid-range passenger vehicles and commercial platforms because its lower cost and stronger perceived safety profile match the needs of higher-volume programs. GM and LG Energy Solution are moving US capacity toward LFP production, which shows that announced plant plans are now being revised around practical cost targets rather than only technical range goals.

Lead-acid and nickel-metal-hydride chemistries still have small roles in mild-hybrid and auxiliary systems, but their position is weakening as low-voltage architectures increasingly shift toward lithium-ion support. Emerging chemistries held only a minimal revenue share in 2025, yet they are projected to expand at 34.1% through 2031, which makes them the fastest-growing chemistry group in the North America EV lithium-ion battery market. Nissan stated in April 2026 that its 23-layer solid-state prototype pack met charge and discharge benchmarks and remains aimed at a 2028 launch at a USD 75 per kWh pack cost, which keeps solid-state progress visible even before mass commercialization. At the same time, lithium-manganese-rich development at GM and Ford could broaden the future chemistry set before solid-state reaches large-scale production, which means the market is likely to remain mixed rather than settle around a simple two-chemistry structure

Cylindrical cells claimed 51.9% of the North America EV lithium-ion battery market share in 2025, which kept them in the lead across cell formats. The North America EV lithium-ion battery market has favored cylindrical formats because Panasonic built large-scale 2170 production in Nevada and then extended that base through De Soto, Kansas. Tesla's 4680 cell strategy also supports this position because the format is tied to its heavy vehicle and pickup programs, which require high output and a proven domestic manufacturing path. Pouch cells still retain a role where custom packaging and platform-specific layouts matter, and several joint-venture programs continue to use them in passenger EV architectures. That said, the present lead for cylindrical cells does not remove the growing structural appeal of prismatic designs in the North America EV lithium-ion battery market.

Prismatic cells are forecast to expand at 25.3% through 2031, which makes them the fastest-growing format segment. This growth reflects three linked shifts, namely broader LFP adoption, increasing use of cell-to-pack designs, and rising commercial vehicle demand, where modular pack logic is easier to implement with prismatic cells. Volkswagen's PowerCo plant in St. Thomas is being built around the Unified Cell in prismatic format with a targeted 90 GWh annual capacity, which gives the region a major future source of local prismatic output VW.CA. The upcoming USMCA review could further favor producers that already manufacture prismatic cells inside the trade bloc, because rules-of-origin compliance is becoming as important as pure manufacturing scale in the North America EV lithium-ion battery market.

Complete Report Scope:

- By Battery Chemistry

- Lithium-ion (NMC, LFP, NCA)

- Emerging (Solid-state, Li-S, Na-ion)

- Lead-acid

- Nickel-metal-hydride

- By Cell Format

- Cylindrical

- Prismatic

- Pouch

- By Propulsion

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Trucks

- Buses and Coaches

- Two and Three-wheelers

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- LG Energy Solution Ltd

- Panasonic Holdings Corporation

- SK On Co. Ltd

- Contemporary Amperex Technology Co. Ltd (CATL)

- Samsung SDI Co. Ltd

- BYD Company Ltd

- A123 Systems LLC

- EnerSys

- E-One Moli Energy Corp.

- VARTA AG

- Microvast Holdings Inc.

- Farasis Energy Inc.

- Romeo Power Inc.

- Northvolt AB

- Gotion High-Tech Co. Ltd

- Clarios LLC

- Envision AESC Group Ltd

- Tesla Inc. (Cell Manufacturing)

- FREYR Battery

- Solid Power Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining lithium-ion battery prices

- 4.2.2 Growing EV model availability & purchase incentives

- 4.2.3 Scale-up of North-American cell manufacturing capacity

- 4.2.4 OEM-battery maker long-term offtake agreements

- 4.2.5 Break-throughs in high-silicon anodes (>=2028)

- 4.2.6 Second-life battery leasing models for fleets

- 4.3 Market Restraints

- 4.3.1 Raw-material supply bottlenecks for Class-1 nickel

- 4.3.2 Slow permitting of new North-American lithium projects

- 4.3.3 Recycling regulatory uncertainty beyond California

- 4.3.4 Thermal-runaway reputation risk after high-profile fires

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, LFP, NCA)

- 5.1.2 Emerging (Solid-state, Li-S, Na-ion)

- 5.1.3 Lead-acid

- 5.1.4 Nickel-metal-hydride

- 5.2 By Cell Format

- 5.2.1 Cylindrical

- 5.2.2 Prismatic

- 5.2.3 Pouch

- 5.3 By Propulsion

- 5.3.1 Battery Electric Vehicle (BEV)

- 5.3.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.3.3 Hybrid Electric Vehicle (HEV)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Trucks

- 5.4.4 Buses and Coaches

- 5.4.5 Two and Three-wheelers

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 LG Energy Solution Ltd

- 6.4.2 Panasonic Holdings Corporation

- 6.4.3 SK On Co. Ltd

- 6.4.4 Contemporary Amperex Technology Co. Ltd (CATL)

- 6.4.5 Samsung SDI Co. Ltd

- 6.4.6 BYD Company Ltd

- 6.4.7 A123 Systems LLC

- 6.4.8 EnerSys

- 6.4.9 E-One Moli Energy Corp.

- 6.4.10 VARTA AG

- 6.4.11 Microvast Holdings Inc.

- 6.4.12 Farasis Energy Inc.

- 6.4.13 Romeo Power Inc.

- 6.4.14 Northvolt AB

- 6.4.15 Gotion High-Tech Co. Ltd

- 6.4.16 Clarios LLC

- 6.4.17 Envision AESC Group Ltd

- 6.4.18 Tesla Inc. (Cell Manufacturing)

- 6.4.19 FREYR Battery

- 6.4.20 Solid Power Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

電動汽車用鋰離子電池:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

電動汽車用鋰離子電池:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 汽車鋰離子電池市場預測至2034年-全球產品、車輛類型、類別類型、電芯類型、通路和區域分析

汽車鋰離子電池市場預測至2034年-全球產品、車輛類型、類別類型、電芯類型、通路和區域分析 汽車鋰離子電池市場:電池類型、驅動系統、電芯形狀、容量範圍、電壓與容量、車輛類型、銷售管道、最終用途 - 全球市場預測 2026-2032

汽車鋰離子電池市場:電池類型、驅動系統、電芯形狀、容量範圍、電壓與容量、車輛類型、銷售管道、最終用途 - 全球市場預測 2026-2032 汽車鋰離子電池市場規模、佔有率和成長分析(按類型、車輛類型、應用、容量和地區分類)—2026-2033年產業預測中東和非洲電動車用鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動車鋰離子電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲電動車鋰離子電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)法國電動車用鋰離子電池市場佔有率分析、產業趨勢、成長預測(2025-2030)英國電動車鋰離子電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)

汽車鋰離子電池市場規模、佔有率和成長分析(按類型、車輛類型、應用、容量和地區分類)—2026-2033年產業預測中東和非洲電動車用鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動車鋰離子電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲電動車鋰離子電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)法國電動車用鋰離子電池市場佔有率分析、產業趨勢、成長預測(2025-2030)英國電動車鋰離子電池:市場佔有率分析、產業趨勢、成長預測(2025-2030) 汽車用鋰離子電池組的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

汽車用鋰離子電池組的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)