|

市場調查報告書

商品編碼

2066762

電動汽車用鋰離子電池:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Lithium-ion Battery For Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

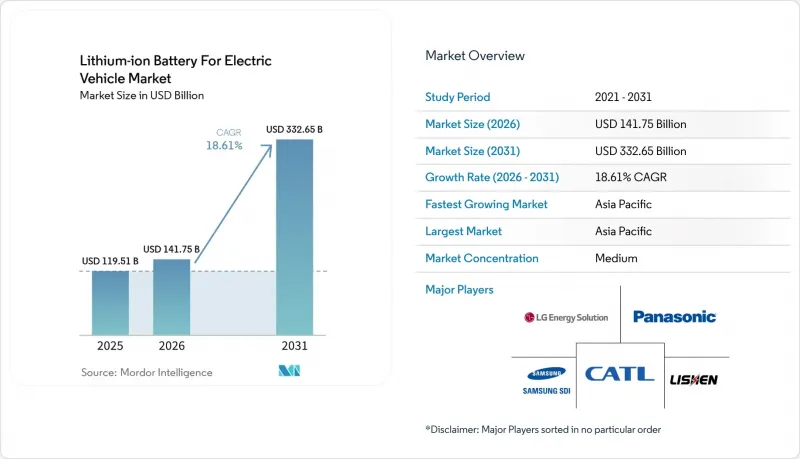

據 Mordor Intelligence 稱,電動車鋰離子電池的市場規模預計在 2026 年達到 1,417.5 億美元,高於 2025 年的 1,195.1 億美元,預計到 2031 年將達到 3,326.5 億美元。

預計 2026 年至 2031 年的複合年成長率為 18.61%。

本報告按電池化學成分(鋰離子電池、新興技術電池、鉛酸電池、鎳氫電池)、電池形狀(圓柱形、棱柱形、軟包型)、驅動系統(電池式電動車、插電式混合動力汽車、混合動力汽車)、車輛類型(乘用車、輕型商用車等)和地區(北美、歐洲、亞太地區等)進行分類。

全球電動車鋰離子電池發展趨勢及洞察

預計到 2029 年,鋰離子電池組的價格將降至 80 美元/kWh以下。

受碳酸鋰價格下跌和超級工廠規模擴大的推動,2024年電池組平均成本降至115美元/度數時,年減14%。中國產磷酸鋰鐵鋰(LFP)電池的競標價格降至95美元/千瓦時,使得入門車型無需補貼即可在亞洲市場銷售。特斯拉的「4680計畫」預計到2026年電池價格將降至70美元/千瓦時,凸顯了垂直整合的原始設備製造商(OEM)透過自有供應獲得套利利潤的重要性。

旨在加速重型卡車電氣化的法規

中國、歐盟和美國正在協調各自的計劃,以推動純電動卡車銷售成為主流。中國規定,到2030年,第一線城市新註冊的重型卡車中,50%必須是零排放車輛;歐盟的目標是到2040年將排放減少90%;美國環保署(EPA)則呼籲,到2032年,8級純電動卡車的銷量應佔總銷量的40%。每輛牽引車需要高達400千瓦時的電池電量,這將使電池需求遠遠超過乘用車的平均需求。

原物料價格波動

2024年1月至12月期間,碳酸鋰價格暴跌85%,迫使像Albemarle這樣的礦業公司削減在澳洲的產量。同期,硫酸鎳價格波動了46%,擠壓了鎳基複合材料(NMC)製造商的利潤空間,而磷酸鐵鋰(LFP)供應商則享有相對穩定的原料成本。歐洲電池製造商依賴進口90%的電池用氫氧化鋰,因此特別容易受到外匯風險的影響。

細分市場分析

到2025年,鋰離子電池市場中,NMC、LFP和NCA將佔據電動車鋰離子電池市場90.87%的需求。儘管成本高出20-30%,NMC仍主導著續航里程約400英里的高階車型市場。同時,LFP憑藉其無鈷的穩定性,目前在中國乘用車市場佔據44.65%的佔有率。鈉離子電池正在入門級應用領域嶄露頭角,而全固態電池預計將以30.90%的複合年成長率成長,並在2028年實現商業化。隨著LFP在亞洲的踏板車和公車上的應用,預計到2031年,光是LFP一項的鋰離子電池市場規模就將超過1247億美元。然而,如果固態電池的生產成本降至120美元/kWh以下,現有的液態電解質超級工廠將面臨加速折舊免稅額。

因此,電動車市場的鋰離子電池必須應對來自兩方面的威脅。固態固態電池預計能量密度將提高60%,對長續航里程領域中富鎳的NMC電池構成挑戰;而鈉離子電池在對成本高度敏感的車隊市場中價格低於磷酸鐵鋰電池。製造商正在拓展其正極材料產品組合,例如SVOLT公司已將無鈷NMX材料商業化,以規避ESG(環境、社會和管治)的審查。監管機構對碳足跡揭露的要求進一步收緊了化學成分的選擇,並且從2025年起,歐洲將在採購中優先考慮低排放正極材料。

預計到2025年,棱柱形電芯將佔電動車鋰離子電池市場出貨量的47.55%。比亞迪的「刀鋒」電池透過將長棱柱形單元整合底盤,省去了模組外殼,從而減輕了15%的重量。寧德時代的「麒麟」電池透過在側壁嵌入冷卻水通道,實現了255Wh/kg的電池密度。相比之下,特斯拉「4680」等圓柱形電池設計佔了35.25%的市場佔有率,並且在自動化生產方面更具優勢。無片電極設計可將內阻降低50%,進而達到5分鐘快速充電。

目前市佔率為17.20%的軟包電池預計到2031年將達到22.80%的年複合成長率(CAGR),這主要得益於寶馬「新等級」(Neue Klasse)強調靈活佈局以最大化車內空間。隨著歐洲超級工廠擴大產能,到本世紀末,軟包鋰離子電池市場規模可望達到600億美元。區域趨勢顯而易見:棱柱形電池在亞洲佔據主導地位,圓柱形電池在北美更受歡迎,而軟包電池在歐洲也逐漸受到關注。如果供應商不維護支援多種電池規格的生產線,則面臨客戶流失的風險。

區域分析

到2025年,亞太地區將佔電動車鋰離子電池市場50.35%的佔有率,其中中國550GWh的裝置容量遠超過歐洲和北美總和。在印度生產連結獎勵計畫計劃(PLI)支持的工廠以及東南亞摩托車市場蓬勃發展的推動下,電池需求預計將持續成長,全部區域預計到2031年將保持20.92%的複合年成長率。中國垂直整合的供應鏈佔全球鋰精煉量的70%,使其比依賴進口的競爭對手擁有15-20%的成本優勢。

在北美,《通貨膨脹控制法案》(IRA)的獎勵推動了22.05%的複合年成長率。預計到2024年,美國產能將達到80吉瓦時,這主要得益於特斯拉、通用-LG、福特-SK和Panasonic等公司計劃於2025年至2027年間運作的項目。國內採購需求正在重組供應契約,而亞洲巨頭則透過促進本地技術許可來獲取信貸。

歐洲緊隨其後,年複合成長率達19.35%,這主要得益於歐盟電池法規以及透過一家32億歐元的合資企業提供的聯合資金。到2024年,歐洲的電池產能將達到700吉瓦時。 Northvolt、ACC和寧德時代在匈牙利的基地都是歐洲本土成本優勢顯著的採購案例,對中國的出口利潤率構成了壓力。

儘管南美洲和中東/非洲地區合計僅佔8.25%的市場佔有率,但成長速度正在加快。位於巴西的Stellantis公司以及與沙烏地阿拉伯Ceer公司合資的生產線計畫於2026年投產,為在地採購奠定初步基礎。區域部署主要集中在公車和共享汽車領域,因為這些領域能夠立即實現燃油成本的降低。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 預計到 2029 年,鋰離子電池組的價格將降至每度電 80 美元以下。

- 中國、歐盟和美國重型卡車快速電氣化

- 原始設備製造商(比亞迪、特斯拉、吉利)的垂直整合正在推動對自產電池的需求。

- 為吸引超級工廠落腳該國而展開的地緣政治競爭(愛爾蘭共和協議、歐盟的BJT計畫、印度的PLI計畫)

- 800V快速充電架構提高了電池的平均容量。

- 由於不含鈷的設計,磷酸鐵鋰電池具有成本優勢,正在擴大其在對價格敏感的 2W/3W 市場的佔有率。

- 市場限制因素

- 原料(碳酸鋰、硫酸鎳)現貨價格波動

- 從 2028 年開始,全固態電池和鈉離子電池的商業化可能會蠶食鋰離子電池市場。

- ESG對中國供應鏈可追溯性的審查

- 電池起火引發的召回事件正在損害新興市場消費者的信心。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按電池的化學成分

- 鋰離子電池(NMC、LFP、NCA)

- 新興技術(全固體、鋰硫、鈉離子)

- 鉛酸

- 鎳氫電池

- 按細胞形狀

- 圓柱形

- 棱柱型

- 小袋

- 透過驅動系統

- 電池式電動車(BEV)

- 插電式混合動力車(PHEV)

- 混合動力電動車(HEV)

- 車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型卡車

- 巴士和長途汽車

- 二輪車和三輪車

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 澳洲和紐西蘭

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Contemporary Amperex Technology(CATL)

- BYD Company Ltd(FinDreams)

- LG Energy Solution Ltd

- Panasonic Energy Co Ltd

- Samsung SDI Co Ltd

- SK On Co Ltd

- CALB Group Co Ltd

- Gotion High-tech Co Ltd

- Eve Energy Co Ltd

- Sunwoda Electronic Co Ltd

- AESC(Envision)

- Northvolt AB

- SVOLT Energy Technology

- Farasis Energy

- ProLogium Technology Co Ltd

- StoreDot Ltd

- Tata Agratas Energy Storage

- ACC Automotive Cells Company

- QuantumScape Corp.

- Redwood Materials Inc.

- International Battery Co.(IBC)

- Italvolt SpA

- Britishvolt Ltd(in administration)

第7章 市場機會與未來展望

According to Mordor Intelligence, lithium-ion battery for electric vehicle market size in 2026 is estimated at USD 141.75 billion, growing from 2025 value of USD 119.51 billion with 2031 projections showing USD 332.65 billion, growing at 18.61% CAGR over 2026-2031.

This report is Segmented by Battery Chemistry (Lithium-Ion, Emerging, Lead-Acid, and Nickel-Metal-Hydride), Cell Format (Cylindrical, Prismatic, and Pouch), Propulsion (Battery Electric Vehicle, Plug-In Hybrid Electric Vehicle, and Hybrid Electric Vehicle), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), and Geography (North America, Europe, Asia-Pacific, and More).

Global Lithium-ion Battery For Electric Vehicle Market Trends and Insights

Declining Lithium-Ion Battery Pack Prices Below USD 80/kWh by 2029

Average pack costs fell to USD 115/kWh in 2024, down 14% year-on-year, driven by lithium carbonate deflation and gigafactory scale. Chinese LFP bids dipped to USD 95/kWh, enabling unsubsidized entry-level cars across Asia. Tesla projects USD 70/kWh by 2026 on its 4680 program, underscoring the captive-supply arbitrage available to vertically integrated OEMs.

Rapid Electrification Mandates for Heavy-Duty Trucks

China, the EU, and the United States have aligned timelines that push battery-electric trucks toward mainstream sales. China requires 50% zero-emission heavy-truck registrations in tier-1 cities by 2030, the EU is targeting a 90% emissions cut by 2040, and the U.S. EPA calls for 40% Class 8 battery-electric sales by 2032. Each tractor needs up to 400 kWh, amplifying cell demand far beyond passenger-car averages.

Raw-Material Price Volatility

Lithium carbonate collapsed 85% between January and December 2024, forcing miners such as Albemarle to throttle Australian output. Nickel sulfate swung 46% during the same period, squeezing NMC producers' margins, whereas LFP suppliers faced relatively stable input costs. European cell makers, importing 90% of battery-grade lithium hydroxide, are especially exposed to currency risk.

Other drivers and restraints analyzed in the detailed report include:

- OEM Vertical Integration Driving Captive Cell Demand

- Geopolitical Race to On-Shore Gigafactories

- Solid-State and Sodium-Ion Commercialization Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, lithium NMC, LFP, and NCA held 90.87% of demand inside the Lithium-ion battery for electric vehicle market. NMC rules premium 400-mile models despite a 20-30% cost premium, while LFP now owns 44.65% of China's passenger segment due to cobalt-free stability. Sodium-ion debuted for entry-level applications, and solid-state cells are projected at a 30.90% CAGR toward 2028 commercialization. The Lithium-ion battery market size for LFP alone is on track to surpass USD 124.7 billion by 2031 as Asian scooters and buses adopt the chemistry. Yet, if solid-state production costs fall under USD 120/kWh, incumbent liquid-electrolyte gigafactories face accelerated depreciation.

The Lithium-ion battery for the electric vehicle market must therefore manage a dual-front threat. Solid-state promises 60% higher energy density that challenges nickel-rich NMC in long-range segments, while sodium-ion undercuts LFP in cost-sensitive fleets. Producers are diversifying cathode portfolios, with SVOLT commercializing cobalt-free NMX to hedge against ESG scrutiny. Regulators' carbon-footprint disclosure rules intensify chemistry selection; low-emission cathodes earn procurement preference in Europe beginning 2025.

Prismatic cells delivered 47.55% of 2025 shipments within the Lithium-ion battery for electric vehicle market. BYD's Blade integrates long prismatic units into the chassis, removing module housings and cutting weight by 15%. CATL's Qilin achieves 255 Wh/kg pack density by embedding coolant channels within sidewalls. In contrast, cylindrical designs like Tesla's 4680 held a 35.25% share and excel at automated production; tabless electrodes lower internal resistance by 50% to support 5-minute fast charging.

Pouch cells, at 17.20% share, are forecast for 22.80% CAGR through 2031 as BMW's Neue Klasse favors flexible footprints that maximize cabin space. The Lithium-ion battery market size tied to pouch formats could reach USD 60 billion by decade-end as European gigafactories ramp up. Regional bias is evident: Asia champions prismatic, North America leans cylindrical, and Europe eyes pouch, forcing suppliers to maintain multi-format lines or risk customer attrition.

Geography Analysis

Asia-Pacific accounted for 50.35% of the Lithium-ion battery for electric vehicle market in 2025, with China's 550 GWh installed capacity dwarfing Europe and North America combined. Regional CAGR of 20.92% persists through 2031 as India's PLI-backed plants and Southeast Asia's two-wheeler boom raise cell offtake. China's vertically integrated chain, covering 70% of global lithium refining, provides a 15-20% cost advantage versus import-dependent rivals.

North America's IRA incentives underpin a 22.05% CAGR. Announced U.S. capacity reached 80 GWh in 2024, led by Tesla, GM-LG, Ford-SK, and Panasonic projects scheduled for 2025-2027 commissioning. Domestic sourcing requirements reshape supply deals, encouraging Asian giants to license technology locally to capture credits.

Europe follows at 19.35% CAGR on the back of the EU Battery Regulation and EUR 3.2 billion of joint-undertaking co-funding, which lifted the pipeline to 700 GWh in 2024. Northvolt, ACC, and CATL's Hungarian site illustrate cost-competitive continental sourcing that erodes Chinese export margins.

South America and the Middle East-Africa collectively stood at 8.25% share but are accelerating. Brazil's Stellantis line and Saudi Arabia's Ceer venture target 2026 starts, creating early footholds for localized supply. Regional adoption focuses on buses and ride-hailing fleets where fuel savings are immediate.

- Contemporary Amperex Technology (CATL)

- BYD Company Ltd (FinDreams)

- LG Energy Solution Ltd

- Panasonic Energy Co Ltd

- Samsung SDI Co Ltd

- SK On Co Ltd

- CALB Group Co Ltd

- Gotion High-tech Co Ltd

- Eve Energy Co Ltd

- Sunwoda Electronic Co Ltd

- AESC (Envision)

- Northvolt AB

- SVOLT Energy Technology

- Farasis Energy

- ProLogium Technology Co Ltd

- StoreDot Ltd

- Tata Agratas Energy Storage

- ACC Automotive Cells Company

- QuantumScape Corp.

- Redwood Materials Inc.

- International Battery Co. (IBC)

- Italvolt SpA

- Britishvolt Ltd (in administration)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining lithium-ion battery pack prices less than USD 80 /kWh by 2029

- 4.2.2 Rapid electrification mandates for heavy-duty trucks in China, EU & U.S.

- 4.2.3 OEM vertical-integration (BYD, Tesla, Geely) driving captive cell demand

- 4.2.4 Geopolitical race to on-shore Gigafactories (IRA, EU BJT, India PLI)

- 4.2.5 Fast-charging 800-V architectures lifting average battery size

- 4.2.6 LFP's cobalt-free cost edge expanding addressable price-sensitive 2-W/3-W markets

- 4.3 Market Restraints

- 4.3.1 Raw-material spot price volatility (lithium carbonate, nickel sulfate)

- 4.3.2 Solid-state & sodium-ion commercialisation risk cannibalising Li-ion post-2028

- 4.3.3 ESG scrutiny on Chinese supply chain traceability

- 4.3.4 Battery-fire recalls eroding consumer confidence in emerging markets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Chemistry

- 5.1.1 Lithium-ion (NMC, LFP, NCA)

- 5.1.2 Emerging (Solid-state, Li-S, Na-ion)

- 5.1.3 Lead-acid

- 5.1.4 Nickel-metal-hydride

- 5.2 By Cell Format

- 5.2.1 Cylindrical

- 5.2.2 Prismatic

- 5.2.3 Pouch

- 5.3 By Propulsion

- 5.3.1 Battery Electric Vehicle (BEV)

- 5.3.2 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.3.3 Hybrid Electric Vehicle (HEV)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Trucks

- 5.4.4 Buses and Coaches

- 5.4.5 Two and Three-wheelers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 NORDIC Countries

- 5.5.2.7 Russia

- 5.5.2.8 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Australia and New Zealand

- 5.5.3.7 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Nigeria

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Contemporary Amperex Technology (CATL)

- 6.4.2 BYD Company Ltd (FinDreams)

- 6.4.3 LG Energy Solution Ltd

- 6.4.4 Panasonic Energy Co Ltd

- 6.4.5 Samsung SDI Co Ltd

- 6.4.6 SK On Co Ltd

- 6.4.7 CALB Group Co Ltd

- 6.4.8 Gotion High-tech Co Ltd

- 6.4.9 Eve Energy Co Ltd

- 6.4.10 Sunwoda Electronic Co Ltd

- 6.4.11 AESC (Envision)

- 6.4.12 Northvolt AB

- 6.4.13 SVOLT Energy Technology

- 6.4.14 Farasis Energy

- 6.4.15 ProLogium Technology Co Ltd

- 6.4.16 StoreDot Ltd

- 6.4.17 Tata Agratas Energy Storage

- 6.4.18 ACC Automotive Cells Company

- 6.4.19 QuantumScape Corp.

- 6.4.20 Redwood Materials Inc.

- 6.4.21 International Battery Co. (IBC)

- 6.4.22 Italvolt SpA

- 6.4.23 Britishvolt Ltd (in administration)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

汽車鋰離子電池市場預測至2034年-全球產品、車輛類型、類別類型、電芯類型、通路和區域分析

汽車鋰離子電池市場預測至2034年-全球產品、車輛類型、類別類型、電芯類型、通路和區域分析 汽車鋰離子電池市場:電池類型、驅動系統、電芯形狀、容量範圍、電壓與容量、車輛類型、銷售管道、最終用途 - 全球市場預測 2026-2032

汽車鋰離子電池市場:電池類型、驅動系統、電芯形狀、容量範圍、電壓與容量、車輛類型、銷售管道、最終用途 - 全球市場預測 2026-2032 汽車鋰離子電池市場規模、佔有率和成長分析(按類型、車輛類型、應用、容量和地區分類)—2026-2033年產業預測

汽車鋰離子電池市場規模、佔有率和成長分析(按類型、車輛類型、應用、容量和地區分類)—2026-2033年產業預測 北美電動車鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)中東和非洲電動車用鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動車鋰離子電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲電動車鋰離子電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)法國電動車用鋰離子電池市場佔有率分析、產業趨勢、成長預測(2025-2030)英國電動車鋰離子電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)

北美電動車鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030 年)中東和非洲電動車用鋰離子電池:市場佔有率分析、產業趨勢和成長預測(2025-2030)亞太地區電動車鋰離子電池:市場佔有率分析、產業趨勢與成長預測(2025-2030)歐洲電動車鋰離子電池:市場佔有率分析、產業趨勢、成長預測(2025-2030)法國電動車用鋰離子電池市場佔有率分析、產業趨勢、成長預測(2025-2030)英國電動車鋰離子電池:市場佔有率分析、產業趨勢、成長預測(2025-2030) 汽車用鋰離子電池組的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)

汽車用鋰離子電池組的全球市場:產業分析,規模,佔有率,成長,趨勢,預測(2024年~2031年)