|

市場調查報告書

商品編碼

2073586

東協網路安全:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)ASEAN Cyber Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

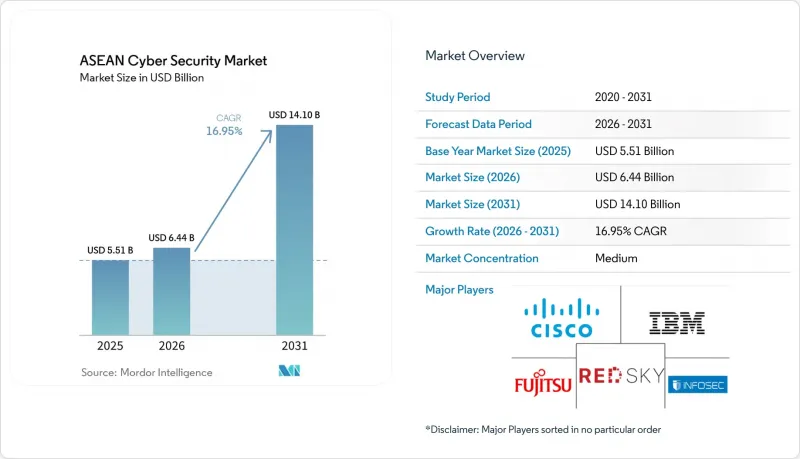

據 Mordor Intelligence 稱,2025 年東協網路安全市場價值 55.1 億美元,預計到 2031 年將從 2026 年的 64.4 億美元成長至 141 億美元,預測期(2026-2031 年)複合年成長率為 16.95%。

本報告以「交付方式(解決方案和服務)」、「部署方式(本地部署和雲端部署)」、「最終用戶產業(銀行、金融服務和保險、醫療保健、IT 和電信、工業和國防、製造業、零售和電子商務、能源和公共產業等)」、「最終用戶公司規模(中小企業和大型企業)」和「國家/地區」對產業進行分類。

東協網路安全市場趨勢與洞察

新加坡在銀行、金融服務和保險 (BFSI) 行業加速採用零信任機制方面處於主導。

新加坡金融管理局於2024年修訂了技術風險指南,此後新加坡各銀行加快了零信任架構的部署。如今,馬來西亞和泰國的金融機構也開始採用類似方法來保護開放銀行API、行動錢包和雲端核心。 Globe旗下的GCash已將其內部網路安全團隊規模擴大了五倍,以保護每年1兆菲律賓披索的交易安全,這顯示人員擴充與架構變革同步進行。供應商受益於身分管治、微隔離和持續認證等授權產品銷售量的成長,而服務供應商則從強制性設計和託管檢測中獲益。隨著監管機構強調彈性測試,零信任架構正從最佳實踐轉變為行業標準,從而推動了東協網路安全市場持續成長的勢頭。

物聯網在印尼製造業和智慧城市造成的攻擊性爆炸性擴張。

爪哇島和蘇門答臘島的先導計畫正在部署感測器、AGV(自動導引運輸車)和邊緣閘道器,但這些部署完全忽略了抵禦敵對網路攻擊的能力。 Alliance Laundry Systems在巴淡島的5G生產線反映了東協各地類似專案的趨勢,每個工廠都安裝了數萬個未託管的終端,需要進行網路分段、網路存取控制(NAC)和異常分析。本地系統整合商正與全球OEM廠商合作維修OT安全,而保險公司也越來越要求在核保前進行資產發現審計。曼谷和胡志明市類似的智慧城市電網正在推動全部區域對以物聯網為中心的威脅建模的需求,從而支撐東協網路安全市場兩位數的成長。

中小企業多重雲端安全營運的總擁有成本較高

儘管預計2024年將面臨65.9萬次網路攻擊,但僅有11%的越南企業表示已做好應對準備。由於需要使用AWS、Azure和Google Cloud等雲端平台上的專用工具,導致重複授權、複雜的整合以及分析師工作量的激增。培訓、威脅情報推送和全天候監控進一步增加了營運成本,迫使許多中小企業只能採取最低限度的措施,加劇了東協網路安全市場的漏洞。

細分市場分析

到2025年,解決方案將佔據東協網路安全市場佔有率的54.12%,這主要得益於對統一端點、網路和雲端控制平台的需求。身分和存取管理套件、新一代防火牆以及XDR堆疊將在初始採購週期中佔據主導地位,從而形成鎖定效應並鞏固與供應商的合約續約。隨著企業面臨技能短缺和監管審計,需要持續監控和客製化的合規性映射,專業服務服務和託管服務正以18.95%的複合年成長率快速成長。馬來西亞計劃在2025年培養25,000名網路安全防禦人員,凸顯了這些服務的重要性。

隨著各組織將一級警報響應、紫隊模擬和合規性文件外包,預計到 2031 年,由服務驅動的東協網路安全市場規模將達到 10 億美元左右。區域性 MSSP(資安管理服務提供者)提供諮詢、整合和營運服務,並將這些服務整合到基於結果的合約中,從而加速了製造業和公共產業等數位化進程滯後的行業的採用。

2025年,受中小企業和新業務對SaaS採用率不斷提高的推動,雲端運算將佔東協網路安全市場規模的57.34%。 Prisma Cloud、GuardDuty和Defender for Cloud等產品在價格敏感型經濟體中極具吸引力,因為它們無需前期資本支出(CAPEX)即可快速威脅搜尋、安全態勢評估和自動化修復。儘管銀行和醫療機構受資料居住要求的限制,目前仍採用混合參考架構,但即使是這些機構也在將其視覺化工具擴展到多重雲端工作負載。

隨著左移DevSecOps、容器安全和CNAPP平台成為標準採購項目,東協網路安全市場的雲端安全支出持續維持19.88%的複合年成長率。本地設備更新周期延長至五年以上,鞏固了向雲端原生控制方法的結構性轉變。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新加坡在銀行、金融服務和保險 (BFSI) 行業加速採用零信任機制方面處於主導。

- 物聯網在印尼製造業和智慧城市造成的攻擊性爆炸性擴張。

- 東南亞國協對安全營運中心(SOC)和電腦緊急應變小組(CERT)的政府資助投資

- 泰國通訊業者快速部署SASE以實現5G企業邊緣運算的商業化

- 擴大在新加坡交易所 (SGX) 和馬來西亞證券交易所 (Bursa Malaysia) 上市的公司的網路保險要求。

- 根據《個人資料保護法》,電子商務資料外洩罰款大幅增加(泰國和菲律賓)

- 市場限制因素

- 中小企業多重雲端營運總體擁有成本 (TCO) 高

- 10個成員國的資料保護條例存在差異

- 新興CLMV叢集缺乏GIAC認證的專業人員

- 家族企業集團網路安全韌性文化薄弱

- 重要法規結構的評估

- 價值鏈分析

- 技術展望

- 波特五力模型

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場區隔

- 報價

- 解決方案

- 應用程式安全

- 雲端安全

- 資料安全

- 身分和存取管理

- 基礎設施保護

- 綜合風險管理

- 網路安全設備

- 端點安全

- 其他服務

- 服務

- 專業服務

- 託管服務

- 解決方案

- 部署模式

- 現場

- 雲

- 按最終用戶行業分類

- BFSI

- 衛生保健

- 資訊科技/通訊

- 工業與國防

- 製造業

- 零售與電子商務

- 能源公用事業

- 製造業

- 其他

- 按最終用戶公司規模分類

- 中小企業

- 大公司

- 國家

- 新加坡

- 馬來西亞

- 泰國

- 印尼

- 菲律賓

- 越南

- 其他東南亞國協(汶萊、柬埔寨、寮國、緬甸)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems Inc.

- Fortinet Inc.

- Palo Alto Networks Inc.

- Trend Micro Incorporated

- IBM Corporation

- Check Point Software Technologies Ltd.

- Huawei Technologies Co. Ltd.

- Microsoft Corp.

- Kaspersky Lab

- Dell Technologies Inc.

- Broadcom Inc.(Symantec Enterprise)

- Splunk Inc.

- Sophos Ltd.

- Darktrace plc

- Zscaler Inc.

- F5 Inc.

- CrowdStrike Holdings Inc.

- Imperva Inc.

- Cybereason Inc.

- SEC Consult(Atos Group)

第7章 市場機會與未來展望

According to Mordor Intelligence, the ASEAN cybersecurity market size was valued at USD 5.51 billion in 2025 and estimated to grow from USD 6.44 billion in 2026 to reach USD 14.1 billion by 2031, at a CAGR of 16.95% during the forecast period (2026-2031).

This report Segments the Industry Into by Offering (Solutions, and Services), Deployment Mode (On-Premise, and Cloud), End-User Vertical (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Manufacturing, Retail and E-Commerce, Energy and Utilities, Manufacturing, and Others), End-User Enterprise Size (Small and Medium Enterprises (SMEs), and Large Enterprises), and Country.

ASEAN Cyber Security Market Trends and Insights

Intensifying Zero-Trust Adoption in Singapore-led BFSI Sector

Banks in Singapore accelerated zero-trust rollouts after the Monetary Authority updated its technology risk guidelines in 2024. Financial institutions across Malaysia and Thailand now mirror the approach to secure open-banking APIs, mobile wallets and cloud cores. Globe's GCash grew its internal cyber team five-fold to protect PHP 1 trillion in annual transactions, illustrating how headcount expansion parallels architectural change. Vendors gain from higher licence volumes for identity governance, micro-segmentation and continuous authentication, while service providers benefit from design and managed detection mandates. As regulators emphasise resilience tests, zero-trust has moved from best practice to baseline, underpinning sustained spending momentum in the ASEAN cybersecurity market.

Explosive IoT-Inflicted Attack Surface in Indonesian Manufacturing and Smart-Cities

Industry 4.0 pilots across Java and Sumatra add sensors, AGVs and edge gateways that were never hardened for hostile networks. Alliance Laundry Systems' 5G-enabled line in Batam mirrors projects across ASEAN, with each plant hosting tens of thousands of unmanaged endpoints that demand network segmentation, NAC and anomaly analytics. Local system integrators partner global OEMs to retrofit OT-security, while insurers increasingly insist on asset-discovery audits before underwriting. Similar smart-city grids in Bangkok and Ho Chi Minh City amplify the region-wide call for IoT-centric threat modelling, sustaining double-digit growth in the ASEAN cybersecurity market.

High Total-Cost-of-Ownership for Multi-Cloud SecOps in SMEs

Only 11% of Vietnamese firms report incident preparedness despite facing 659,000 attacks in 2024. The need for dedicated tooling across AWS, Azure and Google Cloud drives licence duplication, complex integration and spiraling analyst workloads. Training, threat-intel feeds and 24/7 monitoring further elevate opex, forcing many SMEs to opt for baseline controls, widening the exposure gap inside the ASEAN cybersecurity market.

Other drivers and restraints analyzed in the detailed report include:

- ASEAN Government-Funded SOC and CERT Investments

- Surging E-Commerce Data-Leak Fines Under PDPA

- Fragmented Data-Protection Regulations Across 10 Member States

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 54.12% of ASEAN cybersecurity market share in 2025, anchored by demand for integrated platforms that unify endpoint, network and cloud controls. Identity-and-access suites, next-generation firewalls and XDR stacks dominate initial purchase cycles, creating lock-in effects that fortify vendor renewals. Professional and managed services rise at 18.95% CAGR as enterprises confront skills shortages and regulatory audits that require continuous monitoring and bespoke compliance mapping. Malaysia's plan to train 25,000 cyber defenders by 2025 underscores the services imperative.

The ASEAN cybersecurity market size attributable to services will likely reach mid-single-billion-dollar levels by 2031 as organizations outsource tier-one alert handling, purple-team simulations and compliance documentation. Regional MSSPs bundle advisory, integration and operations in outcome-based contracts, accelerating adoption among late-digitizing sectors such as manufacturing and utilities.

Cloud deployments held 57.34% of the ASEAN cybersecurity market size in 2025, rising on the back of SaaS adoption among SMEs and greenfield ventures. Prisma Cloud, GuardDuty and Defender for Cloud enable rapid threat-hunting, posture scoring and automated remediation without upfront capex, making them attractive in price-sensitive economies. Hybrid reference architecture remains for banks and healthcare groups bound by data-residency mandates, yet even these institutions extend visibility tooling to multi-cloud workloads.

The ASEAN cybersecurity market continues to record 19.88% CAGR in cloud-security spend as shift-left DevSecOps, container security and CNAPP platforms become default procurement. On-premise appliance refresh cycles stretch to five years or more, solidifying the structural tilt toward cloud-native controls.

Complete Report Scope:

- By Offering

- Solutions

- Application Security

- Cloud Security

- Data Security

- Identity and Access Management

- Infrastructure Protection

- Integrated Risk Management

- Network Security Equipment

- Endpoint Security

- Other Services

- Services

- Professional Services

- Managed Services

- Solutions

- By Deployment Mode

- On-Premise

- Cloud

- By End-User Vertical

- BFSI

- Healthcare

- IT and Telecom

- Industrial and Defense

- Manufacturing

- Retail and E-commerce

- Energy and Utilities

- Manufacturing

- Others

- By End-User Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Country

- Singapore

- Malaysia

- Thailand

- Indonesia

- Philippines

- Vietnam

- Rest of ASEAN (Brunei, Cambodia, Laos, Myanmar)

List of Companies Covered in this Report:

- Cisco Systems Inc.

- Fortinet Inc.

- Palo Alto Networks Inc.

- Trend Micro Incorporated

- IBM Corporation

- Check Point Software Technologies Ltd.

- Huawei Technologies Co. Ltd.

- Microsoft Corp.

- Kaspersky Lab

- Dell Technologies Inc.

- Broadcom Inc. (Symantec Enterprise)

- Splunk Inc.

- Sophos Ltd.

- Darktrace plc

- Zscaler Inc.

- F5 Inc.

- CrowdStrike Holdings Inc.

- Imperva Inc.

- Cybereason Inc.

- SEC Consult (Atos Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying Zero-Trust Adoption in Singapore-led BFSI Sector

- 4.2.2 Explosive IoT-inflicted Attack Surface in Indonesian Manufacturing & Smart-Cities

- 4.2.3 ASEAN Government-Funded SOC & CERT Investments

- 4.2.4 Rapid SASE Roll-outs Among Thai Telcos to Monetise 5G Enterprise Edge

- 4.2.5 Growing Cyber-Insurance Mandates for Listed Firms on SGX & Bursa Malaysia

- 4.2.6 Surging e-Commerce Data-Leak Fines under PDPA (Thailand & Philippines)

- 4.3 Market Restraints

- 4.3.1 High Total-Cost-of-Ownership for Multi-Cloud SecOps in SMEs

- 4.3.2 Fragmented Data-Protection Regulations Across 10 Member States

- 4.3.3 Shortage of GIAC-Certified Professionals in Emerging CLMV Cluster

- 4.3.4 Low Cyber-Resilience Culture within Family-Owned Conglomerates

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.1.1 Application Security

- 5.1.1.2 Cloud Security

- 5.1.1.3 Data Security

- 5.1.1.4 Identity and Access Management

- 5.1.1.5 Infrastructure Protection

- 5.1.1.6 Integrated Risk Management

- 5.1.1.7 Network Security Equipment

- 5.1.1.8 Endpoint Security

- 5.1.1.9 Other Services

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Managed Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By End-User Vertical

- 5.3.1 BFSI

- 5.3.2 Healthcare

- 5.3.3 IT and Telecom

- 5.3.4 Industrial and Defense

- 5.3.5 Manufacturing

- 5.3.6 Retail and E-commerce

- 5.3.7 Energy and Utilities

- 5.3.8 Manufacturing

- 5.3.9 Others

- 5.4 By End-User Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Country

- 5.5.1 Singapore

- 5.5.2 Malaysia

- 5.5.3 Thailand

- 5.5.4 Indonesia

- 5.5.5 Philippines

- 5.5.6 Vietnam

- 5.5.7 Rest of ASEAN (Brunei, Cambodia, Laos, Myanmar)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Fortinet Inc.

- 6.4.3 Palo Alto Networks Inc.

- 6.4.4 Trend Micro Incorporated

- 6.4.5 IBM Corporation

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 Huawei Technologies Co. Ltd.

- 6.4.8 Microsoft Corp.

- 6.4.9 Kaspersky Lab

- 6.4.10 Dell Technologies Inc.

- 6.4.11 Broadcom Inc. (Symantec Enterprise)

- 6.4.12 Splunk Inc.

- 6.4.13 Sophos Ltd.

- 6.4.14 Darktrace plc

- 6.4.15 Zscaler Inc.

- 6.4.16 F5 Inc.

- 6.4.17 CrowdStrike Holdings Inc.

- 6.4.18 Imperva Inc.

- 6.4.19 Cybereason Inc.

- 6.4.20 SEC Consult (Atos Group)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026-2030年全球電網網路安全市場

2026-2030年全球電網網路安全市場 網路欺騙市場規模、佔有率和成長分析:按安全層部署、組件架構、部署基礎設施方法、最終用戶產業和地區分類-2026-2033年產業預測

網路欺騙市場規模、佔有率和成長分析:按安全層部署、組件架構、部署基礎設施方法、最終用戶產業和地區分類-2026-2033年產業預測 全球網路安全市場:機會與戰略展望(至2035年)

全球網路安全市場:機會與戰略展望(至2035年) 員工脈搏調查與訪談平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

員工脈搏調查與訪談平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年網路安全代理型人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年網路安全代理型人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) IT與通訊網路安全市場:依解決方案、部署類型、企業規模、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測

IT與通訊網路安全市場:依解決方案、部署類型、企業規模、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測 通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析

通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析 網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 2026-2030年全球公共部門網路安全市場

2026-2030年全球公共部門網路安全市場