|

市場調查報告書

商品編碼

2064522

員工脈搏調查與訪談平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Employee Pulse Survey And Listening Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

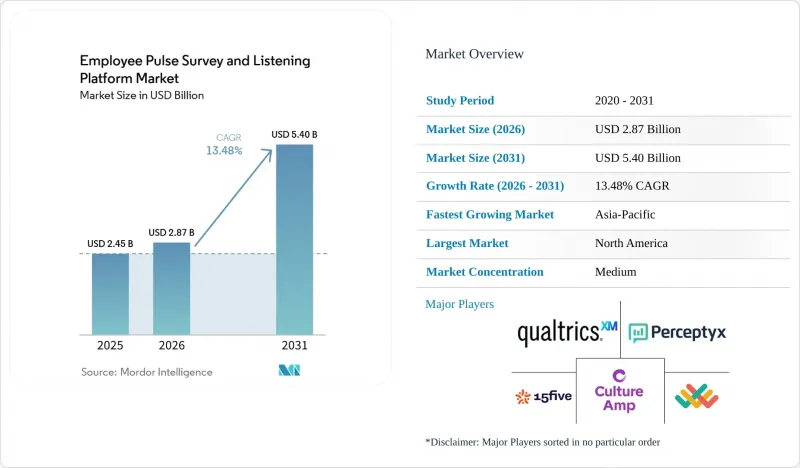

根據 Mordor Intelligence 預測,員工脈搏調查和訪談平台的市場規模預計將在 2025 年達到 24.5 億美元,在 2026 年達到 28.7 億美元,在 2031 年達到 54 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 13.48%。

本報告按組件(平台/軟體、服務)、部署方式(雲端等)、公司規模(大型企業、中小企業)、功能(用戶參與度調查、用戶脈搏調查等)、最終用戶行業(銀行、金融服務和保險、醫療保健/生命科學等)以及地區進行細分。市場預測以美元計價。

全球員工脈搏調查與審計平台市場趨勢與分析

人工智慧驅動的情感分析與預測洞察

大規模語言模型正在改變員工心聲調查和傾聽平台市場,使其從被動的資料收集層轉變為更主動的勞動力智慧系統。如今,透過分析自由說明文本,供應商無需在每個階段都依賴人工解讀,即可識別員工倦怠徵兆、離職風險,並為每位經理制定具體的後續步驟。這一轉變意義重大,因為它即使是從簡短的心聲調查中也能提取有用的主題,從而減少對冗長調查的依賴,並降低調查疲勞。人工智慧正成為員工心聲調查和傾聽平台市場的關鍵指標,因為員工對自動化的態度正在影響他們的信任度、準備度和採用率。蓋洛普在2026年4月發布的報告顯示,管理階層對人工智慧工具的支援是預測員工採用人工智慧的最強指標。這使得傾聽能力與更廣泛的生產力提升計畫更加緊密地連結在一起。

混合辦公和遠距辦公模式的擴展

混合辦公和遠距辦公不再是臨時性的營運模式,而是成為勞動力結構設計的重要組成部分。這種轉變使得透過科技傾聽員工心聲變得至關重要,因為分散的團隊會失去許多管理者過去透過面對面交流獲得的非正式訊息。年度員工敬業度調查並不適用於這種情況,因為單一的年度調查結果無法隨著團隊組成、工作量以及與管理者關係的頻繁變化而保持效用。員工脈搏調查和傾聽平台市場正受益於此趨勢,因為買家越來越需要行動優先、非同步交付且整合在協作工具中的產品,而不是要求員工登入其他系統。 2026年1月,ManpowerGroup德國公司報告稱,58%的德國員工出現職業倦怠症狀,65%的員工打算繼續留在現有公司,54%的員工仍在尋找新的工作。這凸顯了在職場中持續「傾聽」的重要性。

對資料隱私、匿名性和跨境合規性的擔憂

在員工脈搏調查和訪談平台市場,隱私法規仍然是最嚴格的營運限制之一。 GDPR規定,違反關鍵處理規則可能面臨高達2,000萬歐元(2,260萬美元)或全球整體年收入4%的罰款,因此供應商和雇主必須對員工回饋資料實施更嚴格的控制。一個實際挑戰是,即使是標榜匿名的調查,如果團隊規模較小,或者同時使用人口統計篩選條件和時間戳數據,仍然可能洩露個人識別資訊。 2026年3月,有報告指出,員工調查計畫必須根據GDPR謹慎處理同意、人口統計、資料處理和匿名閾值。這表明,管治不再只是法律審查,而是產品設計不可或缺的一部分。因此,我們看到採購週期延長,供應商審查更加嚴格,以及對區域託管、閾值管理和可配置資料保存規則的需求日益成長。

細分市場分析

截至2025年,平台/軟體在員工意見調查和傾聽平台市場規模中佔比71.20%,而服務板塊預計到2031年將以15.23%的複合年成長率成長。軟體仍然是支出核心,因為它負責管理調查執行、儀表板顯示、基準測試和大規模分析。許多初始購買決策仍然專注於平臺本身,因為它也作為員工和經理日常互動的系統。然而,服務板塊的成長速度更快,因為許多人力資源團隊缺乏時間和內部能力將傾聽資料轉化為可供大規模組織管理者執行的行動步驟。

服務需求主要來自實施工作、分析諮詢、行動計畫制定支援以及持續的專案管理。這些收入來源的客戶留存率高於純軟體訂閱模式,因為供應商關係延伸至管治、解讀和變革實施。這在員工脈搏調查和訪談平台市場尤其重要,因為買家越來越希望彌合衡量結果與管理者採取的具體行動之間的差距。 Leapsome 於 2026 年 5 月轉型為更廣泛的人力資源資訊系統 (HRIS) 模型,其邏輯與此類似,即將員工敬業度資料與薪資核算、缺勤和績效記錄整合到一個統一的營運環境中。因此,在員工脈搏調查和訪談平台行業,能夠將數據轉化為工作流程變更(而不僅僅是添加報告層)的服務正變得越來越有價值。

預計到2025年,基於雲端的部署將佔據68.45%的市場佔有率,而混合部署預計到2031年將以14.89%的複合年成長率成長。雲端之所以仍然是首選,是因為它支援快速配置、持續更新、降低維護負擔以及方便分散式團隊存取。此外,雲端與大多數基於SaaS的人力資源軟體的交付模式相契合,簡化了許多雇主的採購和部署流程。這些優勢鞏固了雲端作為跨國公司和中型企業新部署中心樞紐的地位。

混合部署的擴展是由大規模、受監管的雇主推動的,他們需要雲端分析功能和現代化介面,同時又不願犧牲對敏感員工資料的控制權。在員工脈搏調查和訪談平台市場,混合部署不僅僅是邁向全面雲端部署的過渡階段。對於銀行、金融和保險 (BFSI)、醫療保健、公共部門以及其他資料居住要求與內部安全法規重疊的組織而言,混合部署正成為穩定可靠的最終選擇。當現有政策和安全控制措施無法透過第三方雲端處理員工資料時,本地部署環境仍然至關重要。隨著員工脈搏調查和訪談平台市場的成熟,部署柔軟性本身正成為一項重要的購買標準,因為一旦管治和基礎設施建立起來,切換成本就會增加。

區域分析

截至2025年,北美將佔據員工心聲調查和傾聽平台市場規模的40.05%,而亞太地區預計到2031年將以16.89%的複合年成長率成長。北美仍然是最大的收入來源,這得益於其人力資源技術應用的成熟度以及許多大型企業已建立專門的人力分析能力。預計到2025年,美國和加拿大的員工敬業度將達到31%,在所有受調查地區中最高,而員工的日常壓力水平也高達50%,這表明市場對更完善的傾聽基礎設施的需求依然強勁。隨著主導更多由區域主導,而不再僅依賴美國總部主導的部署,加拿大和墨西哥的需求也不斷成長。北美員工心聲調查和傾聽平台市場不僅受益於其龐大的市場規模,還受益於其將人才數據與業務績效緊密結合的強大趨勢。

由於法令遵循與採購決策密切相關,歐洲在員工滿意度調查和訪談平台市場繼續佔據重要的戰略地位。隨著《企業永續性報告指令》(CSRD) 要求企業披露員工信息,管理良好的員工意見數據對於需要在多個營業單位間進行可復現報告的上市公司而言變得越來越有價值。預計到2025年,歐洲的員工敬業度將僅為12%,連續第五年成為全球最低水平,這意味著運作良好的平台仍有很大的提升空間。如果雇主優先考慮本地託管、與勞工委員會的親和性以及符合GDPR要求的設置,那麼總部位於歐盟的供應商將擁有競爭優勢。

亞太地區是員工滿意度調查和訪談平台成長最快的市場,這主要得益於印度、中國、日本、韓國和澳洲等國人力資源部門的數位轉型。跨國公司不斷擴張,員工隊伍語言多元化,也推動了對多語言支援和集中管理的需求。南美和中東及非洲市場雖然規模較小,但隨著當地企業和跨國公司子公司實現人力資源系統的標準化並採用以智慧型手機為中心的調查管道,這些市場的重要性日益凸顯。在這一廣泛擴張的背景下,行動傳輸端普及打破了傳統准入壁壘,且勞動力市場正常化進程仍在進行中的地區,員工滿意度調查和訪談平台市場正蓬勃發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴展混合遠距辦公模式

- 企業對員工敬業度和留任率的關注度日益提高

- 人工智慧驅動的情感分析、預測與洞察

- 雲端原生人力資源技術堆疊的成長

- 進行多語言調查,並考慮現場負責人。

- 人力資本資訊揭露與福祉管治要求

- 市場限制因素

- 對資料隱私、匿名性和跨境合規性的擔憂。

- 調查疲勞和回復品質下降

- 調查週期後的管理可行性差距

- HCM套件帶來的商品搭售壓力和價格下降

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 平台/軟體

- 服務

- 透過部署方法

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按功能

- 員工敬業度調查與員工滿意度調查

- 生命週期聆聽

- 情感分析和文本智慧

- 行動計劃制定和管理支持

- 其他功能

- 按最終用戶行業分類

- 銀行、金融服務和保險業 (BFSI)

- 醫學與生命科學

- IT/通訊

- 零售與電子商務

- 工業/製造業

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Qualtrics, LLC

- Culture Amp Pty Ltd

- 15Five, Inc.

- Degree, Inc. d/b/a Lattice

- Perceptyx, Inc.

- Quantum Workplace, Inc.

- Leapsome GmbH

- WorkTango, Inc.

- Energage, LLC

- Effectory BV

- Explorance Inc.

- EngageRocket Pte. Ltd.

- CultureMonkey Private Limited

- Workleap Software Inc.

- Achievers Solutions Inc.

- SurveySparrow Inc.

- Betterworks System Inc.

- Synergita Software Private Limited

- LutherOne as

- Bargain Technologies Private Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the employee pulse survey and listening platform market size is projected to be USD 2.45 billion in 2025, USD 2.87 billion in 2026, and reach USD 5.40 billion by 2031, growing at a CAGR of 13.48% from 2026 to 2031.

This report is Segmented by Component (Platform/Software and Services), Deployment Mode (Cloud-Based, and More), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Capability (Engagement and Pulse Surveys, and More), End-User Industry (BFSI, Healthcare and Life Sciences and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Employee Pulse Survey And Listening Platform Market Trends and Insights

Ai-Powered Sentiment Analytics And Predictive Insights

Large language models are changing the employee pulse survey and listening platform market from a passive collection layer into a more active workforce intelligence system. Open-text analysis now helps vendors flag burnout signals, attrition risk, and manager-specific next steps without relying on manual interpretation at every step. That change matters because shorter pulse formats can still produce useful themes, reducing dependence on long surveys and helping counter survey fatigue. In the employee pulse survey and listening platform market, AI is also becoming a key metric, as employee sentiment around automation now affects trust, readiness, and adoption. Gallup reported in April 2026 that manager support for AI tools was the strongest predictor of employee AI adoption, which tied listening capability more closely to broader productivity agendas.

Expansion Of Hybrid And Remote Work Models

Hybrid and remote work now function as a structural part of workforce design rather than a temporary operating model. That shift has made technology-mediated listening much more important because distributed teams lose many of the informal signals that managers once picked up in person. Annual engagement surveys don't fit well in this setting because team composition, workload levels, and manager relationships change too often for a single annual snapshot to remain useful. The employee pulse survey and listening platform market is benefiting from this pattern because buyers increasingly want mobile-first, asynchronous delivery that reaches people inside collaboration tools instead of asking them to log in to a separate system. ManpowerGroup Deutschland reported in January 2026 that 58% of German employees showed burnout symptoms, while 65% planned to stay with their employer and 54% were still searching for new roles, underscoring the need for continuous listening to become more operationally relevant.

Data Privacy, Anonymity, And Cross-Border Compliance Concerns

Privacy regulation remains one of the hardest operating constraints in the employee pulse survey and listening platform market. GDPR can impose fines of up to EUR 20 million (USD 22.6 million) or 4% of global annual turnover for violations of core processing rules, so vendors and employers need much tighter controls around employee feedback data. The practical challenge is that surveys marketed as anonymous can still become re-identifiable when teams are small or when demographic filters and timestamp data are combined. In March 2026, it was noted that employee survey programs have to address consent, demographics, processors, and anonymity thresholds carefully under GDPR, which shows how governance has become part of product design rather than just legal review. The result is longer buying cycles, tighter vendor scrutiny, and stronger demand for regional hosting, threshold controls, and configurable data retention rules.

Other drivers and restraints analyzed in the detailed report include:

- Rising Enterprise Focus On Employee Engagement And Retention

- Growth Of Cloud-Native Hr Technology Stacks

- Survey Fatigue And Declining Response Quality

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform/software held 71.20% of the employee pulse survey and listening platform market size in 2025, while services are forecast to expand at a 15.23% CAGR through 2031. Software remained the core layer of spending because it manages survey delivery, dashboarding, benchmarking, and analytics at scale. It also serves as the daily system through which employees and managers interact, so most initial buying decisions still center on the platform itself. Even so, services are growing faster because many HR teams lack the time or in-house capability to translate listening data into manager-ready actions across large organizations.

Services demand is being pulled by implementation work, analytics consulting, action-planning support, and ongoing program management. These revenue streams are also stickier than software-only subscriptions because the vendor relationship extends into governance, interpretation, and change execution. In the employee pulse survey and listening platform market, that matters because buyers increasingly want help closing the gap between measurement and visible manager response. Leapsome's May 2026 move to a broader HRIS model followed the same logic, tying engagement data to payroll, absence management, and performance records within a single operating environment. The employee pulse survey and listening platform industry is therefore placing greater value on services that convert data into workflow changes rather than just producing another reporting layer.

Cloud-based deployment commanded a 68.45% share in 2025, while hybrid deployment is expected to grow at a 14.89% CAGR through 2031. Cloud remained the default choice because it supports rapid provisioning, continuous updates, lower maintenance burden, and easier access for distributed teams. It also aligns with the delivery model of most SaaS-based HR software, which makes procurement and rollout simpler for many employers. These advantages kept the cloud at the center of new deployments across multinational and mid-market accounts.

Hybrid deployment is growing because large regulated employers need cloud analytics and modern interfaces without sacrificing control over sensitive employee data. In the employee pulse survey and listening platform market, hybrid is not just a bridge toward full cloud adoption. It is a stable destination for BFSI, healthcare, public sector, and other organizations dealing with overlapping data residency and internal security rules. On-premises still matters when workforce data cannot be processed by third-party clouds under existing policy or security controls. As the employee pulse survey and listening platform market matures, deployment flexibility is becoming a buying criterion in its own right because switching costs rise once governance and infrastructure are set.

Geography Analysis

North America held 40.05% of the employee pulse survey and listening platform market size in 2025, while Asia-Pacific is forecast to grow at a 16.89% CAGR through 2031. North America remained the largest revenue pool because HR technology adoption is mature and many large employers already operate dedicated people analytics functions. Employee engagement in the United States and Canada stood at 31% in 2025, the highest among measured regions, but daily stress also reached 50%, which keeps demand for better listening infrastructure elevated. Canada and Mexico are also adding demand as adoption becomes more locally driven and less dependent on U.S. headquarters-led rollouts. The employee pulse survey and listening platform market in North America benefits from both scale and a stronger tendency to connect people data with business performance.

Europe remains strategically important in the employee pulse survey and listening platform market because compliance rules and buying decisions are closely linked. Workforce disclosure pressure under CSRD is making well-governed listening data more valuable for public companies that need repeatable reporting across multiple entities. Employee engagement in Europe was 12% in 2025 for the fifth straight year, which left the region with the lowest engagement level globally and a large improvement opportunity for well-executed platforms. EU-based vendors can hold an advantage when employers prioritize regional hosting, works council familiarity, and GDPR-aligned configuration.

Asia-Pacific is the fastest-growing geography in the employee pulse survey and listening platform market, supported by HR digitization in India, China, Japan, South Korea, and Australia. Multinational expansion across linguistically diverse workforces is also raising demand for multilingual delivery and centralized oversight. South America, the Middle East, and Africa remain smaller but increasingly relevant as domestic groups and multinational subsidiaries standardize workforce systems and adopt smartphone-first survey channels. Within this broader expansion, the employee pulse survey and listening platform market is gaining traction in regions where mobile delivery solves earlier access barriers and where workforce formalization is still progressing.

- Qualtrics, LLC

- Culture Amp Pty Ltd

- 15Five, Inc.

- Degree, Inc. d/b/a Lattice

- Perceptyx, Inc.

- Quantum Workplace, Inc.

- Leapsome GmbH

- WorkTango, Inc.

- Energage, LLC

- Effectory B.V.

- Explorance Inc.

- EngageRocket Pte. Ltd.

- CultureMonkey Private Limited

- Workleap Software Inc.

- Achievers Solutions Inc.

- SurveySparrow Inc.

- Betterworks System Inc.

- Synergita Software Private Limited

- LutherOne a.s.

- Bargain Technologies Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Hybrid and Remote Work Models

- 4.2.2 Rising Enterprise Focus on Employee Engagement and Retention

- 4.2.3 AI-Powered Sentiment Analytics and Predictive Insights

- 4.2.4 Growth of Cloud-Native HR Technology Stacks

- 4.2.5 Multilingual and Frontline-Friendly Survey Delivery

- 4.2.6 Human Capital Disclosure and Well-Being Governance Requirements

- 4.3 Market Restraints

- 4.3.1 Data Privacy, Anonymity, and Cross-Border Compliance Concerns

- 4.3.2 Survey Fatigue and Declining Response Quality

- 4.3.3 Manager Actionability Gap After Survey Cycles

- 4.3.4 Bundling Pressure from HCM Suites and Price Compression

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform/Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Capability

- 5.4.1 Engagement and Pulse Surveys

- 5.4.2 Lifecycle Listening

- 5.4.3 Sentiment Analytics and Text Intelligence

- 5.4.4 Action Planning and Manager Enablement

- 5.4.5 Other Capabilities

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Qualtrics, LLC

- 6.4.2 Culture Amp Pty Ltd

- 6.4.3 15Five, Inc.

- 6.4.4 Degree, Inc. d/b/a Lattice

- 6.4.5 Perceptyx, Inc.

- 6.4.6 Quantum Workplace, Inc.

- 6.4.7 Leapsome GmbH

- 6.4.8 WorkTango, Inc.

- 6.4.9 Energage, LLC

- 6.4.10 Effectory B.V.

- 6.4.11 Explorance Inc.

- 6.4.12 EngageRocket Pte. Ltd.

- 6.4.13 CultureMonkey Private Limited

- 6.4.14 Workleap Software Inc.

- 6.4.15 Achievers Solutions Inc.

- 6.4.16 SurveySparrow Inc.

- 6.4.17 Betterworks System Inc.

- 6.4.18 Synergita Software Private Limited

- 6.4.19 LutherOne a.s.

- 6.4.20 Bargain Technologies Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

網路欺騙市場規模、佔有率和成長分析:按安全層部署、組件架構、部署基礎設施方法、最終用戶產業和地區分類-2026-2033年產業預測

網路欺騙市場規模、佔有率和成長分析:按安全層部署、組件架構、部署基礎設施方法、最終用戶產業和地區分類-2026-2033年產業預測 全球網路安全市場:機會與戰略展望(至2035年)

全球網路安全市場:機會與戰略展望(至2035年) IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年

IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年 網路安全代理型人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

網路安全代理型人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) IT與通訊網路安全市場:依解決方案、部署類型、企業規模、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測

IT與通訊網路安全市場:依解決方案、部署類型、企業規模、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測 通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析

通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析 網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 2026-2030年全球公共部門網路安全市場

2026-2030年全球公共部門網路安全市場 全球網路安全代理型人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球網路安全代理型人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034) 後量子安全市場分析及至2035年預測:產品、服務、技術、組件、應用、部署狀態及最終用戶

後量子安全市場分析及至2035年預測:產品、服務、技術、組件、應用、部署狀態及最終用戶