|

市場調查報告書

商品編碼

2061960

網路安全代理型人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cybersecurity Agentic AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

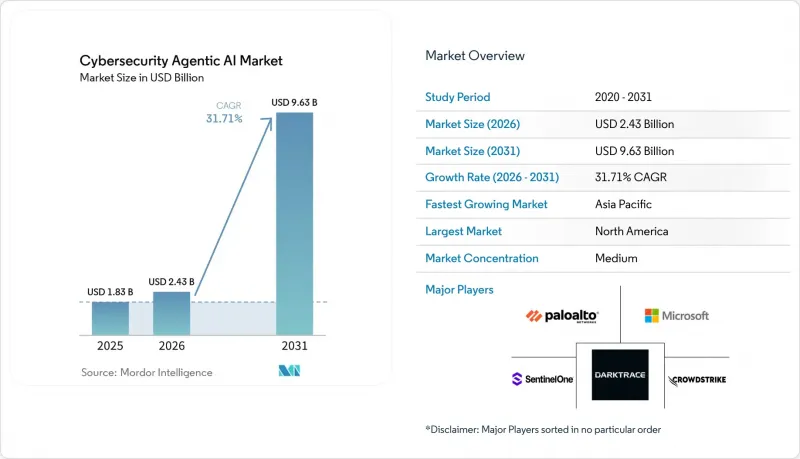

根據 Mordor Intelligence 預測,網路安全代理型人工智慧的市場規模預計將在 2025 年達到 18.3 億美元,在 2026 年達到 24.3 億美元,在 2031 年達到 96.3 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 31.71%。

本報告按組件(軟體平台等)、安全等級(網路安全、終端安全等)、部署方式(雲端原生、本地部署、混合部署)、組織規模(大型企業、中小企業)、產業(銀行、金融服務和保險、醫療保健和生命科學等)以及地區進行細分。市場預測以美元計價。

全球網路安全代理型人工智慧市場趨勢與洞察

透過自主響應迴路實現即時威脅緩解

隨著威脅活動不斷升級並超越人工分診模式的應對能力,基於代理的網路安全人工智慧市場正在蓬勃發展。 2026年3月,CrowdStrike報告稱,攻擊者已將突破時間縮短至29分鐘,分析師主導的遏制措施幾乎沒有餘地。自主回應循環至關重要,因為它們將調查、優先排序和遏制整合到一個流程中,避免了團隊交接造成的延誤。 IBM於2025年4月發布的自主威脅營運機器(Autonomous Threat Operations Machine)正是這種變革的體現,它利用多代理工作流程和特定領域模型,以最少的人工干預執行分診和補救工作。這些循環會產生反饋效應,從而產生數據以增強未來的檢測和反應能力。

多重雲端環境中機器生成攻擊面的爆炸性成長

隨著人工智慧工作負載的成長,網路安全領域基於代理的人工智慧市場也不斷擴張,這擴大了安全團隊面臨的攻擊面。思科在2026年2月指出,隨著代理工作負載在雲端的擴散,企業對人工智慧感知策略執行的需求日益成長,從而推動了對自主安全控制的需求。 Palo Alto Networks在2025年的一項調查發現,99%在生產環境中使用人工智慧的組織至少經歷過一次針對其人工智慧系統的攻擊,41%的組織報告指出API攻擊有所增加。 Orca Security的一項調查顯示,到2025年,55%的組織將使用兩個或多個雲端供應商,高於2024年的12%,凸顯了身分管理和策略環境的碎片化。這推動了對能夠解讀上下文並跨雲端、API和信任區域協調操作的安全系統的需求成長。

對抗性人工智慧與模型中毒的風險

網路安全領域的基於代理的人工智慧市場面臨著這樣的挑戰:雖然自主性增強了防禦能力,但如果模型或資料管道遭到破壞,則會加劇損害。 OWASP 將資料和模型投毒(包括後門植入、輸出篡改和拒絕服務攻擊)列為重大風險。 ICLR 2025 的研究表明,即使在預訓練階段只有 0.1% 的投毒率,也可能在已部署的模型中持續存在。谷歌威脅情報小組發布的報告顯示,在 2025 年,威脅行為者將利用人工智慧進行攻擊,並展示了其在網路攻擊中的實際應用。在監管嚴格的領域,這些風險可能導致人工智慧的普及應用延遲,因為買家會設定更嚴格的權限、縮小部署範圍,並在允許其在生產系統中自主運作之前要求進行廣泛的檢驗。

細分市場分析

到2025年,軟體平台將佔據39.71%的市場。這反映出企業越來越傾向於採用跨端點、雲端、身分和網路遙測的整合式基於代理的編配。該領域受益於共用策略、記憶體和統一的回應邏輯,從而簡化了大規模自主操作。分散式代理部署被視為一種風險,因為它可能導致決策不一致和重複操作。服務仍然是第二大組成部分,因為許多組織在部署、工作流程重構、策略映射和模型管治需要外部支援。

隨著買家從一次性部署轉向持續調優和監控,對服務的需求日益成長。 GitLab 於 2025 年發布的 Duo Agent 平台公開測試版,凸顯了編配如何擴展到開發和安全工作流程,從而推動了諮詢和整合需求。受延遲敏感環境中本地推理需求的驅動,預計到 2031 年,硬體加速器將以 32.31% 的複合年成長率成長。這種轉變將使硬體成為邊緣和高速環境中即時自主防禦的關鍵基礎,從而減少對高延遲雲端往返時間的依賴。

到2025年,網路安全將佔據網路安全代理型人工智慧市場28.23%的佔有率。這是因為網路遙測仍能提供最廣泛的即時可見性,涵蓋東西向流量、橫向權限提升和策略違規等情況。對於許多企業而言,網路層仍然是核心基礎,使基於代理的系統能夠關聯跨資產和環境的行為。端點安全也保持著強勁的地位,因為它是將自主調查和引導式修復引入現有安全架構的最便捷途徑。因此,端點平台已成為網路安全代理型人工智慧市場中採用基於代理技術的常見切入點。

SentinelOne在2026年3月發布的報告顯示,其自主調查功能Purple AI在2026會計年度第四季售出的許可證中佔比超過50%,凸顯了終端設備供應商如何利用其現有基本客群來推廣基於代理的功能。隨著企業處理越來越多的非人類身分和API驅動的存取路徑,雲端和SaaS安全性以及身分和存取管理(IAM)也在蓬勃發展。 OT和IoT安全是成長最快的領域,預計到2031年複合年成長率將達到33.31%,這主要得益於數位基礎設施和實體基礎設施的快速整合。網路安全領域基於代理的AI市場正在從簡單的異常檢測轉向能夠解讀網路意圖和運行環境的平台。

區域分析

2025年,北美將佔據網路安全代理型人工智慧市場34.86%的佔有率,這主要得益於強大的供應商基礎和企業的早期採用。監管產業中推行的持續監控和網路彈性政策也進一步推動了市場成長。 2025年12月,ISC2報告指出,該地區網路安全技能嚴重短缺,推動了對能夠減少人工操作的平台的需求。此外,企業合約的擴展也促進了市場成長,客戶透過更廣泛的平台合作關係部署代理功能,而非單獨購買。

預計到2031年,亞太地區將以32.71%的複合年成長率成長,成為成長最快的區域市場。這一成長主要得益於數位化快速發展、多重雲端的普及以及對人工智慧攻擊的擔憂。該地區各組織機構加強網路防禦的速度超過了其擴充專業安全團隊的速度。關鍵基礎設施的現代化和分散式環境的監控也在推動市場需求,而資料本地化法規和監管成熟度的提高可能會帶來更多機會。

到2025年,歐洲將名列第三,需求主要集中在金融服務、製造業和關鍵基礎設施領域。在這些領域,管治和文件記錄與檢測同等重要。 2026年發表在《人工智慧與倫理》期刊上的一項研究強調了歐洲對透明度和可解釋性的重視,這支撐了對可審計自主系統的需求。中東和非洲地區正透過數位轉型(DX)計畫從小規模的基數快速成長,而南美洲則在勒索軟體威脅日益成長和金融業數位化的推動下逐步擴張。這兩個地區都處於發展初期,但對擴充性的監控和回應模型的需求正在不斷成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 透過自主響應迴路實現即時威脅緩解

- 多重雲端環境中機器生成的攻擊面激增

- 利用人工智慧進行連續控制監測的監管要求

- 網路安全人員長期短缺,正在加速人工智慧安全技術的應用。

- 將LLM代理程式整合到DevSecOps管道中

- 增加對專注於人工智慧安全領域的新創公司的創業融資

- 市場限制因素

- 對抗性人工智慧與模型中毒的風險

- 基於代理的人工智慧決策中可解釋性的局限性

- 訓練以安全為中心的平台模型需要很高的運算成本

- 資料來源標準因司法管轄區而異。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體平台

- 服務(MDR、諮詢、整合)

- 硬體加速器(AI最佳化晶片、感測器)

- 按安全等級

- 網路安全

- 端點安全

- 應用程式安全

- 雲端和SaaS安全

- 身分和存取管理

- OT/IoT 安全

- 部署模式

- 雲端原生

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按行業分類

- BFSI

- 醫療保健和生命科學

- 政府/國防

- 資訊科技/通訊

- 製造業

- 零售與電子商務

- 能源公用事業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- CrowdStrike Holdings Inc.

- Palo Alto Networks Inc.

- Darktrace plc

- SentinelOne Inc.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- Rapid7 Inc.

- Arctic Wolf Networks Inc.

- Sophos Ltd.

- Elastic NV

- Google LLC

- Amazon Web Services Inc.

- Accenture plc

- Noma Security

- Vectra AI

- Okta Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the cybersecurity agentic AI market size is projected to be USD 1.83 billion in 2025, USD 2.43 billion in 2026, and reach USD 9.63 billion by 2031, growing at a CAGR of 31.71% from 2026 to 2031.

This report is Segmented by Component (Software Platforms, and More), Security Level (Network Security, Endpoint Security, and More), Deployment (Cloud-Native, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cybersecurity Agentic AI Market Trends and Insights

Real-Time Threat Mitigation Via Autonomous Response Loops

The cybersecurity agentic AI market is growing as threat activity outpaces manual triage models. CrowdStrike reported in March 2026 that adversaries reduced breakout time to 29 minutes, leaving little room for analyst-led containment. Autonomous response loops are crucial because they integrate investigation, prioritization, and containment into a single process, avoiding delays caused by team handoffs. IBM's Autonomous Threat Operations Machine, launched in April 2025, demonstrates this shift by using multi-agent workflows and domain-specific models for triage and remediation with minimal human input. These loops create a feedback effect, generating data to enhance future detection and response.

Explosion of Machine-Generated Attack Surfaces in Multi-Cloud Environments

The cybersecurity agentic AI market is expanding as AI-enabled workloads increase the attack surface for security teams. Cisco noted in February 2026 that enterprises seek AI-aware policy enforcement as agentic workloads spread across clouds, driving demand for autonomous security controls. Palo Alto Networks' 2025 research found that 99% of organizations using AI in production experienced at least one attack on their AI systems, with 41% reporting increased API attacks. Orca Security found 55% of organizations used two or more cloud providers in 2025, up from 12% in 2024, highlighting a fragmented identity and policy environment. This strengthens demand for security systems that interpret context and coordinate actions across clouds, APIs, and trust zones.

Adversarial AI and Model Poisoning Risks

The cybersecurity agentic AI market faces challenges as the same autonomy that enhances defense can amplify damage if models or data pipelines are compromised. OWASP identifies data and model poisoning as critical risks, including backdoor insertion, output manipulation, and denial-of-service attacks. Research at ICLR 2025 revealed that even a 0.1% poisoning rate during pre-training can persist into deployed models. Google's Threat Intelligence Group documented AI misuse by threat actors in 2025, showing its practical application in cyberattacks. These risks may slow adoption in regulated sectors, as buyers impose stricter permissions, narrower deployment scopes, or demand extensive validation before allowing autonomous actions in production systems.

Other drivers and restraints analyzed in the detailed report include:

- Chronic Cyber Workforce Shortage Accelerating AI Security Adoption

- Regulatory Mandates for AI-Driven Continuous Controls Monitoring

- Limited Explainability of Agentic AI Decisions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms held a 39.71% share in 2025, reflecting enterprise preference for integrated agentic orchestration across endpoint, cloud, identity, and network telemetry. This segment benefits from shared policy, memory, and unified response logic, simplifying autonomous actions at scale. Fragmented agent deployments are seen as a risk due to inconsistent decisions and duplicate actions. Services remained the second-largest component as many organizations require external support for deployment, workflow redesign, policy mapping, and model governance.

Service demand is increasingly recurring as buyers shift from one-time implementation to ongoing tuning and oversight. GitLab's 2025 public beta of the Duo Agent Platform highlighted how orchestration extends into development and security workflows, driving advisory and integration needs. Hardware accelerators are projected to grow at a 32.31% CAGR through 2031, driven by the need for local inference in latency-sensitive environments. This shift positions hardware as a key enabler of real-time autonomous defense in edge and high-speed settings, reducing reliance on slower cloud round-trip times.

Network security commanded a 28.23% share of the cybersecurity agentic AI market in 2025 because network telemetry still provides the broadest real-time view of east-west movement, lateral escalation, and policy violations. For many enterprises, the network layer remains the backbone that allows agentic systems to correlate behavior across assets and environments. Endpoint security also retained a strong position because it is often the easiest place to introduce autonomous investigation and guided remediation into an existing security stack. This has made endpoint platforms a common entry point for agentic adoption in the cybersecurity agentic AI market.

SentinelOne reported in March 2026 that its Purple AI autonomous investigation capability was included in over 50% of licenses sold in Q4 FY26, highlighting how endpoint vendors leverage their installed base to distribute agentic features. Cloud and SaaS security and IAM are also growing as organizations handle an increasing number of non-human identities and API-driven access paths. OT and IoT security, the fastest-growing segment at a 33.31% CAGR through 2031, is driven by the rapid convergence of digital and physical infrastructure. The cybersecurity agentic AI market is shifting toward platforms that interpret both network intent and operational context, rather than just detecting anomalies.

Geography Analysis

North America accounted for 34.86% of the cybersecurity agentic AI market in 2025, driven by its strong vendor base and early enterprise adoption. Policies promoting continuous monitoring and cyber resilience in regulated sectors further support growth. ISC2 reported in December 2025 that critical cybersecurity skill gaps in the region are boosting demand for platforms that reduce manual effort. Market growth is also tied to enterprise contract expansions, with customers adopting agentic functions through broader platform relationships rather than stand-alone purchases.

Asia-Pacific is projected to grow at a 32.71% CAGR through 2031, making it the fastest-growing regional market. This growth is fueled by rapid digital expansion, multi-cloud adoption, and concerns over AI-enabled attacks. Organizations in the region are scaling cyber defenses faster than they can expand skilled security teams. Critical infrastructure modernization and distributed environment monitoring also drive demand, though data localization rules and regulatory maturity may create uneven opportunities.

Europe ranked third in 2025, with demand focused on financial services, manufacturing, and critical infrastructure, where governance and documentation are as important as detection. Research published in AI and Ethics in 2026 highlighted Europe's emphasis on transparency and explainability, supporting demand for auditable autonomous systems. The Middle East and Africa are growing from a smaller base through digital transformation programs, while South America is gradually expanding amid rising ransomware threats and financial sector digitization. Both regions are in an early development stage,s but show increasing demand for scalable monitoring and response models.

- CrowdStrike Holdings Inc.

- Palo Alto Networks Inc.

- Darktrace plc

- SentinelOne Inc.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- Rapid7 Inc.

- Arctic Wolf Networks Inc.

- Sophos Ltd.

- Elastic N.V.

- Google LLC

- Amazon Web Services Inc.

- Accenture plc

- Noma Security

- Vectra AI

- Okta Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Real-Time Threat Mitigation via Autonomous Response Loops

- 4.2.2 Explosion of Machine-Generated Attack Surfaces in Multi-Cloud Environments

- 4.2.3 Regulatory Mandates for AI-Driven Continuous Controls Monitoring

- 4.2.4 Chronic Cyber Workforce Shortage Accelerating AI Security Adoption

- 4.2.5 Integration of LLM Agents in DevSecOps Pipelines

- 4.2.6 Growing Venture Funding for Specialized AI Security Startups

- 4.3 Market Restraints

- 4.3.1 Adversarial AI and Model Poisoning Risks

- 4.3.2 Limited Explainability of Agentic AI Decisions

- 4.3.3 High Computational Costs of Training Security-Specific Foundation Models

- 4.3.4 Fragmented Data Provenance Standards Across Jurisdictions

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services (MDR, Advisory, Integration)

- 5.1.3 Hardware Accelerators (AI-Optimized Silicon, Sensors)

- 5.2 By Security Level

- 5.2.1 Network Security

- 5.2.2 Endpoint Security

- 5.2.3 Application Security

- 5.2.4 Cloud and SaaS Security

- 5.2.5 Identity and Access Management

- 5.2.6 OT / IoT Security

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Native

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Mid-Sized Enterprises

- 5.5 By Industry Vertical

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Government and Defense

- 5.5.4 IT and Telecom

- 5.5.5 Manufacturing

- 5.5.6 Retail and E-Commerce

- 5.5.7 Energy and Utilities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CrowdStrike Holdings Inc.

- 6.4.2 Palo Alto Networks Inc.

- 6.4.3 Darktrace plc

- 6.4.4 SentinelOne Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Microsoft Corporation

- 6.4.7 Cisco Systems Inc.

- 6.4.8 Fortinet Inc.

- 6.4.9 Check Point Software Technologies Ltd.

- 6.4.10 Trend Micro Incorporated

- 6.4.11 Rapid7 Inc.

- 6.4.12 Arctic Wolf Networks Inc.

- 6.4.13 Sophos Ltd.

- 6.4.14 Elastic N.V.

- 6.4.15 Google LLC

- 6.4.16 Amazon Web Services Inc.

- 6.4.17 Accenture plc

- 6.4.18 Noma Security

- 6.4.19 Vectra AI

- 6.4.20 Okta Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球網路安全市場:機會與戰略展望(至2035年)

全球網路安全市場:機會與戰略展望(至2035年) IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年

IT與通訊網路安全市場-全球產業規模、佔有率、趨勢、機會與預測:按部署模式、安全解決方案、最終用戶產業、地區和競爭格局分類,2021-2031年 IT與通訊網路安全市場:依解決方案、部署類型、企業規模、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測

IT與通訊網路安全市場:依解決方案、部署類型、企業規模、最終用戶、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測 通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析

通訊網路安全市場預測至2034年-按組件、部署模式、安全類型、解決方案類型、應用、最終用戶和地區分類的全球分析 網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測

網路安全市場規模、佔有率和成長分析:按組件、部署模式、安全類型、組織規模、最終用戶產業和地區分類-2026-2033年產業預測 2026-2030年全球公共部門網路安全市場

2026-2030年全球公共部門網路安全市場 全球網路安全代理型人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球網路安全代理型人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034) 後量子安全市場分析及至2035年預測:產品、服務、技術、組件、應用、部署狀態及最終用戶人工智慧驅動的網路安全解決方案市場預測至2034年:按交付方式、技術類型、安全類型、部署方式、組織規模、最終用戶和地區分類的全球分析

後量子安全市場分析及至2035年預測:產品、服務、技術、組件、應用、部署狀態及最終用戶人工智慧驅動的網路安全解決方案市場預測至2034年:按交付方式、技術類型、安全類型、部署方式、組織規模、最終用戶和地區分類的全球分析 網路安全市場:按組件、安全類型、組織規模、部署模式和產業分類-2026-2032年全球市場預測

網路安全市場:按組件、安全類型、組織規模、部署模式和產業分類-2026-2032年全球市場預測