|

市場調查報告書

商品編碼

2073559

南美航空燃料:市場佔有率分析、產業趨勢與統計及成長預測(2025-2031 年)South America Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

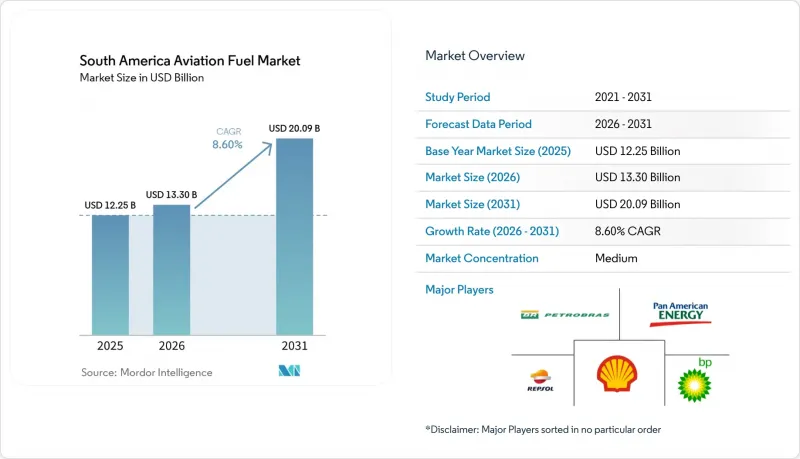

據 Mordor Intelligence 稱,2025 年南美航空燃料市場價值 122.5 億美元,預計到 2031 年將達到 200.9 億美元,而 2026 年為 133 億美元,預測期內(2026-2031 年)的複合年預計成長率為 8.60%。

本報告按燃料類型(傳統噴射機燃料、永續航空燃料、航空汽油)、飛機類型(窄體飛機、寬體飛機、支線噴氣式飛機和渦輪螺旋槳飛機、貨機)、應用領域(民用航空、國防和軍事、通用航空、城市空中運輸/電動垂直起降飛機)以及地區(巴西、阿根廷、哥倫比亞、智利、秘魯和其他南美國家)進行細分。市場預測以美元計價。

南美航空燃油市場趨勢與洞察

航空旅客數量的復甦正在推動對Jet-A1航空煤油的需求。

南美航空業已超越復甦階段,進入更廣泛的擴張階段,這為南美航空燃油市場建立了更強勁的需求基礎。 2026年第一季,拉丁美洲和加勒比海地區的航空公司旅客周轉量(RPK)較去年同期成長8.6%,而同期巴西國內市場也成長了11.4%。這表明客運量的成長仍然超出許多人的預期。客座率維持高位,2025年11月區域市場客座率達85.9%。這顯示供給能力緊張,飛機運轉率提高,而非預訂量出現暫時性激增。隨著航空公司延長飛機運營時間並提高上座率,幹線航線、中轉航線以及機場週轉的燃油需求將直接且可預測地成長。因此,南美航空燃油市場不僅受益於客運量的成長,也受益於可用飛機和機場時刻的更有效率利用。

低成本航空公司(LCC)的擴張和航線自由化將擴大燃油市場。

廉價航空公司的發展正在擴大南美航空燃油市場,將服務範圍從主要城際航線擴展到需要定期加油的區域機場。阿根廷推動的航空燃油市場放鬆管制,使得2026年第一季的座位供給能力增加了8.5%,顯示政策變化能夠迅速轉化為飛機運營量和航班頻次的增加。這意義重大,因為新航線不僅增加了客運量,還形成了持續的燃油需求樞紐,需要相應的儲存、配送協調和供應商可靠性。這種影響在國內和短程航線上尤其顯著,因為這些航線的單通道飛機日運轉率很高,燃油是影響營運最直接的因素之一。隨著自由化的推進,預計南美航空燃油市場的需求將不再局限於最大的樞紐機場,而是會呈現地理擴張。

該地區永續航空燃料(SAF)產能不足,造成短期供應風險。

南美航空燃料市場在尚未建立足夠的生產基礎以確保穩定供應的情況下,就正朝著強制使用永續航空燃料(SAF)的方向發展。儘管巴西石油公司(Petrobras)已在巴西建立了首個供應基準,但區域供應鏈仍處於起步階段,目前主要集中在少數項目和計劃中的產能擴張上。這縮小了供應窗口,早期合規將取決於有限的生產商數量、有限的聯合加工量以及煉油廠的逐步改造,而非高市場流動性。麻省理工學院(MIT)、拉丁美洲航空運輸協會(LATAM)和空中巴士公司(Airbus)對拉丁美洲脫碳的研究也指出了「預訂與索賠」模式的價值,因為如果小規模國內市場在本地實際供應完全建立之前無法參與SAF採購,它們將面臨困難。在產量擴展到少數幾個關鍵項目之外之前,南美航空燃料市場將面臨供應限制,即使法規已經明確,這也可能會延遲SAF的採用。

細分市場分析

預計到2025年,傳統噴射機燃料將佔南美航空燃料市場92.3%的佔有率,顯示該地區仍深深依賴石化燃料。這種主導地位與目前的市場狀況密切相關,因為機場燃料供應系統、分銷管道以及大部分煉油廠的生產都已符合Jet A-1及相關航空煤油的規格。因此,即使相關法規開始改變低碳替代燃料的採購行為,在可預見的未來,這一領域仍可能繼續保持其主要供應來源的地位。同時,航空燃料仍然是一個規模雖小但穩健的細分市場,因為通用航空、農業飛行和內陸運輸網路仍然依賴與大型航空公司燃料特性不同的飛機類型。

永續航空燃料(SAF)是成長最快的燃料類型,預計2026年至2031年間,南美航空燃料市場中該細分市場的規模將以28.6%的複合年成長率成長。高成長率源於其較小的初始規模,但隨著巴西政策框架的完善以及遵守CORSIA(國際航空碳抵消和減排計劃)的壓力,SAF正從象徵性的採購轉變為一項計劃性需求,其根本性轉變正在成為現實。巴西石油公司(Petrobras)引領了這一趨勢,於2025年12月交付了首批國內SAF,顯示經認證的本地供應可以從煉油廠生產轉向機場分銷。博阿文圖拉計畫和Reisen的認證流程也表明,南美航空燃料產業的建構正圍繞著原料取得、協同加工和乙醇基路線展開,而非等待單一的技術突破。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 疫情後航空客運量恢復狀況

- 廉價航空公司擴張和航線自由化

- 可支配所得增加和中產階級擴大

- 機場基礎設施現代化計劃

- eVTOL 和區域空中計程車計畫正在推動對 Jet-A1 的需求。

- 綠色走廊計畫正在加速地表防火(SAF)的推廣。

- 市場限制因素

- 該地區SAF生產能力的局限性

- 外匯波動加劇,燃油價格風險上升。

- 主要的能源結構是石化燃料,政策停滯不前。

- 偏遠機場的燃料管道出現瓶頸

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按燃料類型

- 傳統噴射機燃料

- 永續航空燃料(SAF)

- 航空汽油

- 按飛機類型

- 窄體飛機

- 寬體飛機

- 支線噴射機和渦輪螺旋槳飛機

- 貨機/專用貨機

- 透過使用

- 私人航空公司

- 國防/軍用航空

- 通用航空和公務航空

- 城市空中交通/電動垂直起降飛行器

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Petroleo Brasileiro SA(Petrobras)

- Repsol SA

- BP PLC

- Shell PLC

- TotalEnergies SE

- Pan American Energy SL

- Exxon Mobil Corporation

- Allied Aviation Services Inc.

- Ipiranga Produtos de Petroleo SA

- Raizen Energia SA

- YPF SA

- ENAP Refinerias SA

- Petroperu SA

- Chevron Corporation

- Vitol Aviation BV

- Gevo Inc.

- World Energy LLC

- Amyris Inc.

- SkyNRG BV

- Neste Oyj

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america aviation fuel market size was valued at USD 12.25 billion in 2025 and is estimated to grow from USD 13.30 billion in 2026 to reach USD 20.09 billion by 2031, at a CAGR of 8.60% during the forecast period (2026-2031).

This report is Segmented by Fuel Type (Conventional Jet Fuel, SAF, Avgas), Aircraft Type (Narrow-Body, Wide-Body, Regional Jets and Turboprops, Cargo/Freighters), Application (Commercial Airlines, Defense/Military, General Aviation, Urban Air Mobility/EVTOL), and Geography (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America). Market Forecasts are Provided in Value (USD).

South America Aviation Fuel Market Trends and Insights

Recovering Air Passenger Traffic Fuels Jet-A1 Demand

South America's airline sector has moved beyond a simple rebound and into a broader expansion phase that is now giving the South America aviation fuel market a firmer demand base. Latin America and Caribbean airlines recorded 8.6% year-on-year RPK growth in Q1 2026, and Brazil's domestic market grew 11.4% in the same period, which shows that traffic growth is still running ahead of many earlier expectations. Load factors have also stayed high, with the regional market reaching 85.9% in November 2025, which points to tight capacity and stronger aircraft utilization rather than a short-lived spike in bookings. When airlines keep aircraft in the air longer and fill more seats, fuel demand rises in a direct and predictable way across trunk routes, connecting routes, and airport turnarounds. This is why the South America aviation fuel market is benefiting not only from more passengers, but also from a more intensive use of available fleets and airport slots.

Expanding Low-Cost Carriers and Route Liberalization Widen the Fuel Market

Low-cost carrier growth is widening the South America aviation fuel market by pushing service beyond the main capital-city corridors and into secondary airports that need regular fuel supply. Argentina's liberalization push helped lift seat capacity by 8.5% in Q1 2026, which shows how policy change can quickly translate into more aircraft activity and more frequent departures. This matters because each new route does more than add passengers; it creates a repeat fuel-demand point that needs storage, delivery coordination, and supplier reliability. The effect is especially visible in domestic and short-haul flying, where single-aisle fleets run high daily utilization and turn fuel into one of the most immediate operating variables. As liberalization spreads, the South America aviation fuel market should see demand broaden geographically rather than remain tied only to the largest hubs.

Limited Regional SAF Production Capacity Creates Near-Term Supply Risk

The South America aviation fuel market is moving into mandated SAF consumption before the region has built a wide enough production base to supply it comfortably. Petrobras has established the first domestic delivery benchmark in Brazil, but the regional supply chain is still early and remains concentrated in a small number of projects and planned capacity additions. This creates a narrow supply window in which early compliance can depend on a small producer set, limited co-processing volumes, and gradual refinery adaptation rather than deep market liquidity. The MIT, LATAM, and Airbus work on Latin American decarbonization also points to the value of book-and-claim structures, because smaller national markets will struggle if they must wait for full local physical supply before participating in SAF procurement. Until production spreads beyond a few anchor projects, the South America aviation fuel market will face a supply-side constraint that can slow adoption even where regulation is already clear.

Other drivers and restraints analyzed in the detailed report include:

- Green-Corridor Commitments Accelerating SAF Uptake

- Airport Infrastructure Modernization Programs Drive Long-Term Fuel Infrastructure Demand

- Currency Volatility Increasing Fuel-Price Risk for Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional jet fuel accounted for 92.3% of South America aviation fuel market size in 2025, which shows that the region still runs on a deeply established fossil-fuel base. This dominance is tied to the installed reality of the market, because airport fuel systems, distribution assets, and most refinery output are already aligned with Jet A-1 and related aviation kerosene specifications. The segment should therefore remain the main source of supply over the near term, even as regulation starts to reshape procurement behavior around lower-carbon alternatives. Avgas remains a small but durable niche because general aviation, agricultural flying, and interior connectivity still depend on aircraft types that do not move with the same fuel profile as the main airline fleet.

SAF is the fastest-growing fuel type, with South America aviation fuel market size for this segment projected to expand at a 28.6% CAGR from 2026 to 2031. The growth rate looks high because the starting base is still small, but the underlying shift is real as Brazil's policy framework and CORSIA compliance pressures begin to turn SAF into a planning requirement rather than a symbolic purchase. Petrobras strengthened that path with its first domestic SAF delivery in December 2025, proving that certified local supply can move from refinery output into airport distribution. The Boaventura project and Raizen's certification pathway also show that the South America aviation fuel industry is building around feedstock access, co-processing, and ethanol-based routes rather than waiting for a single technology outcome.

Complete Report Scope:

- By Fuel Type

- Conventional Jet Fuel

- Sustainable Aviation Fuel (SAF)

- Avgas

- By Aircraft Type

- Narrow-body

- Wide-body

- Regional Jets and Turboprops

- Cargo/Freighters

- By Application

- Commercial Airlines

- Defense/Military Aviation

- General and Business Aviation

- Urban Air Mobility / eVTOL

- By Geography

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

List of Companies Covered in this Report:

- Petroleo Brasileiro SA (Petrobras)

- Repsol SA

- BP PLC

- Shell PLC

- TotalEnergies SE

- Pan American Energy SL

- Exxon Mobil Corporation

- Allied Aviation Services Inc.

- Ipiranga Produtos de Petroleo SA

- Raizen Energia SA

- YPF SA

- ENAP Refinerias SA

- Petroperu SA

- Chevron Corporation

- Vitol Aviation BV

- Gevo Inc.

- World Energy LLC

- Amyris Inc.

- SkyNRG BV

- Neste Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Recovering air passenger traffic post-pandemic

- 4.2.2 Expanding low-cost carriers and route liberalization

- 4.2.3 Rising disposable income & middle-class growth

- 4.2.4 Airport infrastructure modernization programs

- 4.2.5 eVTOL & regional air-taxi projects boost Jet-A1 demand

- 4.2.6 Green-corridor commitments accelerating SAF uptake

- 4.3 Market Restraints

- 4.3.1 Limited regional SAF production capacity

- 4.3.2 Currency volatility increasing fuel-price risk

- 4.3.3 Fossil-fuel dominated energy mix & policy inertia

- 4.3.4 Fuel-pipeline bottlenecks to remote airports

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 Conventional Jet Fuel

- 5.1.2 Sustainable Aviation Fuel (SAF)

- 5.1.3 Avgas

- 5.2 By Aircraft Type

- 5.2.1 Narrow-body

- 5.2.2 Wide-body

- 5.2.3 Regional Jets and Turboprops

- 5.2.4 Cargo/Freighters

- 5.3 By Application

- 5.3.1 Commercial Airlines

- 5.3.2 Defense/Military Aviation

- 5.3.3 General and Business Aviation

- 5.3.4 Urban Air Mobility / eVTOL

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Chile

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Petroleo Brasileiro SA (Petrobras)

- 6.4.2 Repsol SA

- 6.4.3 BP PLC

- 6.4.4 Shell PLC

- 6.4.5 TotalEnergies SE

- 6.4.6 Pan American Energy SL

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 Allied Aviation Services Inc.

- 6.4.9 Ipiranga Produtos de Petroleo SA

- 6.4.10 Raizen Energia SA

- 6.4.11 YPF SA

- 6.4.12 ENAP Refinerias SA

- 6.4.13 Petroperu SA

- 6.4.14 Chevron Corporation

- 6.4.15 Vitol Aviation BV

- 6.4.16 Gevo Inc.

- 6.4.17 World Energy LLC

- 6.4.18 Amyris Inc.

- 6.4.19 SkyNRG BV

- 6.4.20 Neste Oyj

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

航空燃料市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。

航空燃料市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。 可再生/生物噴射機燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按轉換路徑、來源、地區和競爭格局分類,2021-2031年

可再生/生物噴射機燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按轉換路徑、來源、地區和競爭格局分類,2021-2031年 航空燃料市場預測至2034年—按燃料類型、飛機類型、最終用戶和地區分類的全球分析航空燃油添加劑市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。

航空燃料市場預測至2034年—按燃料類型、飛機類型、最終用戶和地區分類的全球分析航空燃油添加劑市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。 運輸燃料市場:依燃料類型、來源、混合比例、最終用戶和分銷管道分類-2026-2032年全球市場預測航空燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、飛機類型、原料、添加劑、最終用戶和分銷管道分類)

運輸燃料市場:依燃料類型、來源、混合比例、最終用戶和分銷管道分類-2026-2032年全球市場預測航空燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、飛機類型、原料、添加劑、最終用戶和分銷管道分類) 航空燃料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球航空燃油終端市場規模、佔有率、趨勢及成長分析報告(2026-2034)

航空燃料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球航空燃油終端市場規模、佔有率、趨勢及成長分析報告(2026-2034) 航空燃料市場報告:按燃料類型、飛機類型、最終用途和地區分類,2026-2034年

航空燃料市場報告:按燃料類型、飛機類型、最終用途和地區分類,2026-2034年 2026年全球航空燃料市場報告

2026年全球航空燃料市場報告