|

市場調查報告書

商品編碼

2071369

航空燃料市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。Aviation Fuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

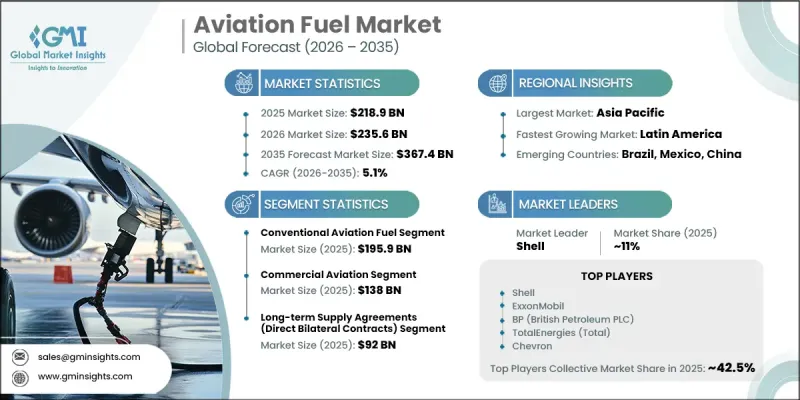

預計到 2025 年,全球航空燃料市場價值將達到 2,189 億美元,並預計以 5.1% 的複合年成長率成長,到 2035 年達到 3,674 億美元。

由於全球航空客運量(包括國內和國際客運量)持續成長,航空燃油市場正經歷穩定成長。旅遊業的活性化、商務旅行的增加以及區域間航空網路的不斷完善,都促進了全球飛機運轉率的提升。新興經濟體可支配收入的增加和中產階級的壯大,進一步推動了客運量的成長,並增強了對航空運輸服務的需求。此外,長途旅行的復甦和航班頻次的增加,也推動了商業航空公司營運中航空燃油消耗量的成長。長途旅行對航空運輸的日益青睞,持續推動市場成長。航空公司對機隊現代化和機場基礎建設的持續投資,也為航空燃油市場帶來了益處。航空公司正在擴建和升級機隊,以滿足不斷成長的客運需求,同時提高營運效率。同時,政府和私營部門的相關人員也在投資機場擴建項目、燃油供應基礎設施以及區域間互聯互通計劃,以提升航空運輸能力。這些趨勢持續為全球航空業的永續發展創造有利條件。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 2189億美元 |

| 預測金額 | 3674億美元 |

| 複合年成長率 | 5.1% |

預計2025年,傳統航空燃料市場規模將達到1,959億美元。由於其在民用、軍用和貨運航空領域的廣泛應用,該市場持續推動整個產業的發展。客運量的穩定成長、航線網路的不斷擴展以及飛機起降次數的增加,都支撐著對傳統航空燃料的強勁需求。此外,成熟的煉油能力、完善的供應鏈以及與現有飛機技術的兼容性,也持續推動傳統航空燃料在全球主要航空市場的廣泛應用。

預計2025年,民用航空市場規模將達到1,380億美元。國內外航線客運量的成長、航空公司網路的持續擴張以及全球飛機數量的增加,都支撐了該領域的強勁市場地位。旅遊業、商務旅行和廉價航空公司的營運擴張持續推動著民用航空領域的燃油需求。此外,航空貨運量的活性化和機場基礎設施的不斷改進也促進了燃油消耗量的成長,進一步鞏固了該領域的市場地位。

預計到2025年,北美航空燃油市場規模將達到633億美元。該地區受益於客運量的成長、成熟的民航產業以及機隊的持續擴張。美國仍然是該地區最大的航空燃油市場貢獻者,這得益於其龐大的國內航空網路、大規模的國防航空行動以及支撐航空燃油生產的高度發達的煉油基礎設施。貨運航空活動的成長以及對機場現代化和航空基礎設施建設的持續投資也是推動該地區成長的因素。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 全球航空旅客數量增加

- 擴大航空公司機隊規模並改善機場基礎設施

- 航空貨運和物流運輸的成長

- 產業潛在風險與挑戰

- 原油價格波動

- 嚴格的環境法規

- 市場機遇

- 擴大永續航空燃料(SAF)的使用

- 開發中國家的新興航空市場

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 專利趨勢

- 貿易統計資料(註:貿易統計僅涵蓋主要國家)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- LATAM

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依燃料類型分類,2022-2035年

- 傳統航空燃料

- 噴射機燃料(渦輪燃料)

- 航空汽油(Avgas)

- 其他

- 永續航空燃料(SAF)

- HEFA-SPK(氫化酯和脂肪酸)

- FT-SPK(FISCHER-TROPSCH法合成的石蠟煤油)

- ATJ-SPK(醇制噴射合成石蠟基煤油)

- 其他(聯合處理、SIP、HC-HEFA)

- 其他

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 商業航空

- 窄體飛機

- 寬體飛機

- 支線噴射機和渦輪螺旋槳飛機

- 航空貨運和貨運飛機

- 軍事航空

- 戰鬥機和作戰飛機

- 運輸和物流飛機

- 軍用直升機

- 軍用無人機和無人作戰飛行器(UCAV)

- 私人及商務航空

- 公務機

- 配備渦輪螺旋槳和活塞引擎的私人飛機

- 商用和民用無人機/無人飛行器

- 無人機在物流和最後一公里配送的應用

- 用於監測、測量和檢查的無人機

- 農業無人機

- 其他

第7章 市場估價與預測:依採購管道分類,2022-2035年

- 長期供應合約(直接雙邊合約)

- 在現貨市場購買

- 機上服務合約(透過FBO和地面服務代理)

- 政府和競標採購

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- UAE

- 其他中東和非洲國家

第9章:公司簡介

- ExxonMobil

- Shell

- BP(British Petroleum PLC)

- TotalEnergies(Total)

- Chevron

- Vitol

- World Kinect Corporation

- China Aviation Oil

- Indian Oil Corporation Limited

- Bharat Petroleum Corporation Limited(BPCL)

- Hindustan Petroleum Corporation Limited(HPCL)

- Gazprom

- Mercury Air Group

- Virent, Inc.

The Global Aviation Fuel Market was valued at USD 218.9 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 367.4 billion by 2035.

The market is experiencing steady expansion owing to the continuous rise in global air passenger traffic across both domestic and international routes. Increasing tourism activity, growing business travel, and improved regional air connectivity are contributing to higher aircraft utilization worldwide. Rising disposable incomes and the expansion of the middle-class population in developing economies are further supporting passenger growth and strengthening demand for air transportation services. In addition, the recovery of long-distance travel and the increase in flight frequency are driving higher aviation fuel consumption across commercial airline operations. Growing preference for air transportation for long-distance travel continues to reinforce market growth. The Aviation Fuel Market is also benefiting from ongoing investments in airline fleet modernization and airport infrastructure development. Airlines are expanding and upgrading their aircraft fleets to accommodate rising passenger demand while improving operational efficiency. Simultaneously, governments and private-sector stakeholders are investing in airport expansion projects, fueling infrastructure, and regional connectivity initiatives to enhance aviation capacity. These developments continue to create favorable conditions for sustained growth across the global aviation sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $218.9 Billion |

| Forecast Value | $367.4 Billion |

| CAGR | 5.1% |

The conventional aviation fuel segment generated USD 195.9 billion in 2025. The segment continues to dominate the industry due to its extensive use across commercial, military, and cargo aviation operations. Consistent growth in passenger traffic, expanding airline networks, and increasing aircraft movements are supporting strong demand for traditional aviation fuels. Furthermore, established refining capabilities, mature supply chains, and compatibility with existing aircraft technologies continue to reinforce the widespread adoption of conventional aviation fuel across major aviation markets worldwide.

The commercial aviation segment captured USD 138 billion in 2025. The segment's strong position is driven by rising passenger volumes across domestic and international routes, continued expansion of airline networks, and increasing aircraft deployment globally. Growth in tourism, business travel, and budget airline operations continues to support fuel demand within the commercial aviation sector. Additionally, increasing air freight activity and ongoing airport infrastructure enhancements are contributing to higher fuel consumption levels, further strengthening the segment's market position.

North America Aviation Fuel Market generated USD 63.3 billion in 2025. The region benefits from increasing passenger traffic, a well-established commercial aviation industry, and continuous fleet expansion activities. The United States remains the largest contributor to regional revenue, supported by an extensive domestic aviation network, substantial defense aviation operations, and a highly developed refining infrastructure that supports aviation fuel production. Regional growth is also being supported by increasing cargo aviation activity and continued investments in airport modernization and aviation infrastructure development.

Major companies operating in the Global Aviation Fuel Market include Chevron, Shell, ExxonMobil, TotalEnergies, BP (British Petroleum PLC), World Kinect Corporation, Vitol, China Aviation Oil, Indian Oil Corporation Limited, Bharat Petroleum Corporation Limited (BPCL), Hindustan Petroleum Corporation Limited (HPCL), Gazprom, Mercury Air Group, and Virent, Inc. a Companies operating in the Aviation Fuel Market are adopting a variety of strategic initiatives to strengthen their market presence and enhance long-term competitiveness. Key strategies include expanding refining capacity, optimizing fuel supply networks, and strengthening distribution infrastructure to improve operational efficiency and meet growing demand. Market participants are also investing in sustainable aviation fuel development, advanced production technologies, and research initiatives aimed at reducing carbon emissions and supporting industry sustainability goals. Strategic partnerships, long-term supply agreements, and collaborations with airlines, airports, and fuel distributors are helping companies secure stable revenue streams and expand customer reach. Additionally, businesses are focusing on geographic expansion, digital supply chain management, and infrastructure modernization to improve service reliability, increase market penetration, and maintain a strong competitive position within the evolving aviation fuel industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fuel Type

- 2.2.3 Application

- 2.2.4 Procurement Channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global air passenger traffic

- 3.2.1.2 Expansion of airline fleets and airport infrastructure

- 3.2.1.3 Growth in air cargo and logistics transportation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in crude oil prices

- 3.2.2.2 Stringent environmental regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of sustainable aviation fuel (SAF)

- 3.2.3.2 Emerging aviation markets in developing economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Fuel Type, 2022 - 2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Conventional Aviation Fuel

- 5.2.1 Jet Fuel (Turbine Fuel)

- 5.2.2 Aviation Gasoline (Avgas)

- 5.2.3 Others

- 5.3 Sustainable Aviation Fuel (SAF)

- 5.3.1 HEFA-SPK (Hydroprocessed Esters & Fatty Acids)

- 5.3.2 FT-SPK (Fischer-Tropsch Synthetic Paraffinic Kerosene)

- 5.3.3 ATJ-SPK (Alcohol-to-Jet Synthetic Paraffinic Kerosene)

- 5.3.4 Others (Co-processing, SIP, HC-HEFA)

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Commercial aviation

- 6.2.1 Narrow-body aircraft

- 6.2.2 Wide-body aircraft

- 6.2.3 Regional jets & turboprops

- 6.2.4 Air cargo & freighters

- 6.3 Military aviation

- 6.3.1 Fighter & combat aircraft

- 6.3.2 Transport & logistics aircraft

- 6.3.3 Military helicopters

- 6.3.4 Military UAVs & unmanned combat aerial vehicles (UCAVs)

- 6.4 Private & business aviation

- 6.4.1 Business jets

- 6.4.2 Turboprop & piston-engine private aircraft

- 6.5 Commercial & civil UAVs/drones

- 6.5.1 Logistics & last-mile delivery drones

- 6.5.2 Surveillance, mapping & inspection UAVs

- 6.5.3 Agricultural UAVs

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Procurement Channel, 2022 - 2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Long-Term Supply Agreements (Direct Bilateral Contracts)

- 7.3 Spot Market Purchases

- 7.4 Into-Plane Service Contracts (via FBOs & Handling Agents)

- 7.5 Government & Tender-Based Procurement

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ExxonMobil

- 9.2 Shell

- 9.3 BP (British Petroleum PLC)

- 9.4 TotalEnergies (Total)

- 9.5 Chevron

- 9.6 Vitol

- 9.7 World Kinect Corporation

- 9.8 China Aviation Oil

- 9.9 Indian Oil Corporation Limited

- 9.10 Bharat Petroleum Corporation Limited (BPCL)

- 9.11 Hindustan Petroleum Corporation Limited (HPCL)

- 9.12 Gazprom

- 9.13 Mercury Air Group

- 9.14 Virent, Inc.

南美航空燃料:市場佔有率分析、產業趨勢與統計及成長預測(2025-2031 年)

南美航空燃料:市場佔有率分析、產業趨勢與統計及成長預測(2025-2031 年) 可再生/生物噴射機燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按轉換路徑、來源、地區和競爭格局分類,2021-2031年

可再生/生物噴射機燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按轉換路徑、來源、地區和競爭格局分類,2021-2031年 航空燃料市場預測至2034年—按燃料類型、飛機類型、最終用戶和地區分類的全球分析

航空燃料市場預測至2034年—按燃料類型、飛機類型、最終用戶和地區分類的全球分析 航空燃油添加劑市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。

航空燃油添加劑市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。 運輸燃料市場:依燃料類型、來源、混合比例、最終用戶和分銷管道分類-2026-2032年全球市場預測航空燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、飛機類型、原料、添加劑、最終用戶和分銷管道分類)

運輸燃料市場:依燃料類型、來源、混合比例、最終用戶和分銷管道分類-2026-2032年全球市場預測航空燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、飛機類型、原料、添加劑、最終用戶和分銷管道分類) 航空燃料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球航空燃油終端市場規模、佔有率、趨勢及成長分析報告(2026-2034)

航空燃料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球航空燃油終端市場規模、佔有率、趨勢及成長分析報告(2026-2034) 航空燃料市場報告:按燃料類型、飛機類型、最終用途和地區分類,2026-2034年

航空燃料市場報告:按燃料類型、飛機類型、最終用途和地區分類,2026-2034年 2026年全球航空燃料市場報告

2026年全球航空燃料市場報告