|

市場調查報告書

商品編碼

2038697

航空燃油添加劑市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。Aviation Fuel Additives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

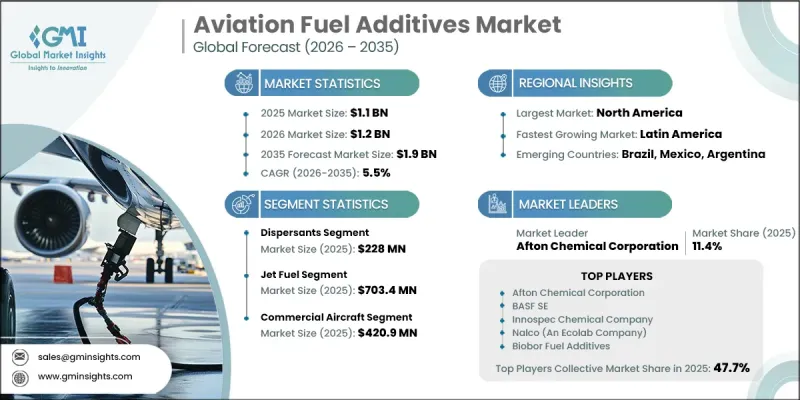

2025年全球航空燃油添加劑市場價值為11億美元,預計到2035年將以5.5%的複合年成長率成長至19億美元。

隨著航空業將運行安全、燃油效率和複雜燃油系統的長期可靠性置於優先地位,航空燃油添加劑產業持續蓬勃發展。這些特殊的化學配方以可控的比例混合到航空燃油中,旨在提升燃油性能、維持燃油穩定性,並確保燃油在其整個生命週期內的安全操作。其功能涵蓋了從最大限度減少氧化、控制污染到降低腐蝕風險以及在燃油運輸過程中控制靜電行為等多個方面。航空業嚴格的合規要求促使這些添加劑持續使用,從而確保其與飛機系統的兼容性,並在各種環境條件下維持燃油品質。從提煉和儲存到分銷和最終的飛機加油,添加劑即使在長期儲存以及暴露於溫度和壓力波動的情況下,也能支持燃油品質的維持。市場上還湧現出旨在適應不斷變化的燃油成分(例如混合燃油和替代航空燃油)的創新添加劑配方。計量和噴射系統的技術進步提高了精度和效率,從而能夠更好地控制添加劑的使用,同時增強燃油的整體性能和系統相容性。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 11億美元 |

| 預測金額 | 19億美元 |

| 複合年成長率 | 5.5% |

到2025年,分散劑市場規模將達到2.28億美元,凸顯了其在維持燃油清潔度和運作穩定性方面的重要作用。對分散劑和抗氧化劑配方的日益依賴,凸顯了它們在防止沉積物形成和在長期儲存和運輸過程中保持燃油品質方面的重要性。旨在控制低溫性能的添加劑對於維持穩定的燃油流量和最大限度地降低運行風險仍然至關重要,尤其是在溫度波動會影響燃油性能的嚴苛飛行條件下。

預計2025年,噴射機燃料市場規模將達到7.034億美元,凸顯其在航空生態系統中的主導地位。持續添加添加劑對於確保熱穩定性、控制污染以及在長時間飛行中保持可靠的燃油性能至關重要。燃油分銷網路的日益複雜化和燃油成分的不斷演變,進一步凸顯了對能夠適應不斷變化的營運和技術要求,同時又能在不同航空系統中保持一致性的先進添加劑解決方案的需求。

北美航空燃油添加劑市場預計將從2025年的3.847億美元成長到2035年的6.61億美元,主要得益於活躍的航空業和完善的加油基礎設施。該地區強勁的需求源於持續不斷的航班運營以及在大規模儲存和分銷系統中維持燃油品質的必要性。嚴格的品質標準和營運效率要求推動了性能增強型添加劑的持續應用。此外,龐大的航空網路以及保護燃油系統免受劣化、污染和性能波動影響的需求也進一步推動了市場的持續成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 民用和軍用飛機運作量增加

- 對燃油品質穩定性的需求

- 延長燃料儲存和運輸期限

- 產業潛在風險與挑戰

- 添加劑與燃料相容性的局限性

- 複雜的燃料物流和處理要求

- 市場機遇

- 擴大永續航空燃料的使用

- 添加劑配方技術的進步

- 加強對燃油系統的保護要求

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按添加劑類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依添加劑類型分類,2022-2035年

- 分散劑

- 抗氧化劑

- 除冰劑

- 腐蝕抑制劑

- 防爆劑

- 金屬惰性

- 其他(燃料穩定劑、燃燒促進劑)

第6章 市場估算與預測:依燃料類型分類,2022-2035年

- 航空汽油

- 噴射機燃料

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 民航機

- 客機

- 貨機

- 軍用機

- 其他(私人飛機、直升機)

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- Afton Chemical Corporation

- Chevron Corporation

- BASF SE

- Biobor Fuel Additives

- Dorf-Ketal Chemicals India Pvt., Ltd.

- Innospec Chemical Company

- Meridian Fuels

- Nalco an Ecolab Company

- LANXESS Deutschland GmbH

- AS Harrison &Co

The Global Aviation Fuel Additives Market was valued at USD 1.1 billion in 2025 and is estimated to grow at a CAGR of 5.5% to reach USD 1.9 billion by 2035.

The aviation fuel additives industry continues to gain momentum as the aviation sector prioritizes operational safety, fuel efficiency, and long-term reliability across complex fuel systems. These specialized chemical formulations are blended into aviation fuels in controlled quantities to enhance performance, maintain stability, and ensure safe handling throughout the fuel lifecycle. Their functional role extends to minimizing oxidation, limiting contamination, reducing corrosion risks, and managing electrostatic behavior during fuel movement. Strict compliance requirements across the aviation sector reinforce the consistent use of these additives, ensuring compatibility with aircraft systems and maintaining fuel integrity under varying environmental conditions. From refining and storage to distribution and final aircraft fueling, additives support quality preservation even during prolonged storage and exposure to fluctuating temperatures and pressure levels. The market is also witnessing innovation in additive formulations designed to align with evolving fuel compositions, including blended and alternative aviation fuels. Technological advancements in dosing and injection systems are improving accuracy and efficiency, allowing better control over additive application while enhancing overall fuel performance and system compatibility.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.1 Billion |

| Forecast Value | $1.9 Billion |

| CAGR | 5.5% |

The dispersants segment accounted for USD 228 million in 2025, reflecting their essential role in maintaining fuel cleanliness and operational stability. Increasing reliance on dispersants and antioxidant formulations highlights their importance in preventing deposit formation and preserving fuel quality during extended storage and transportation cycles. Additives designed to manage low-temperature performance remain critical for maintaining consistent fuel flow and minimizing operational risks, particularly in demanding flight conditions where temperature variations can affect fuel behavior.

The jet fuel segment captured USD 703.4 million in 2025, underscoring its dominant role within the aviation ecosystem. Continuous additive integration is required to ensure thermal stability, control contamination, and support reliable fuel performance across extended flight durations. The growing complexity of fuel distribution networks and the evolution of fuel compositions further emphasize the need for advanced additive solutions that can adapt to changing operational and technical requirements while maintaining consistency across diverse aviation systems.

North America Aviation Fuel Additives Market is anticipated to grow from USD 384.7 million in 2025 to USD 661 million by 2035, driven by high aviation activity levels and a well-established fueling infrastructure. The region demonstrates strong demand due to continuous flight operations and the need to maintain fuel integrity across large-scale storage and distribution systems. Strict quality standards and operational efficiency requirements encourage ongoing adoption of performance-enhancing additives. Sustained demand is further supported by extensive aviation networks and the need to protect fuel systems from degradation, contamination, and performance inconsistencies over time.

Key companies operating in the Global Aviation Fuel Additives Market include Afton Chemical Corporation, BASF SE, Chevron Corporation, Innospec Chemical Company, LANXESS Deutschland GmbH, Nalco an Ecolab Company, Dorf-Ketal Chemicals India Pvt., Ltd., Meridian Fuels, Biobor Fuel Additives, and A S Harrison & Co. Companies in the Aviation Fuel Additives Market are focusing on advancing formulation technologies to improve performance, compatibility, and environmental compliance. Strategic investments in research and development are enabling the creation of additives that align with next-generation fuel requirements and evolving aviation standards. Market participants are strengthening their supply chains and expanding global distribution networks to ensure consistent product availability. Collaboration with fuel producers and aviation stakeholders is enhancing product integration across the value chain. Firms are also prioritizing precision dosing technologies and digital monitoring solutions to improve application efficiency. Sustainability initiatives, product diversification, and long-term partnerships are further supporting competitive positioning and market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Additive Type

- 2.2.3 Fuel Type

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing commercial and military flight operations

- 3.2.1.2 Need for fuel quality consistency

- 3.2.1.3 Extended fuel storage and transport durations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited additive compatibility with fuels

- 3.2.2.2 Complex fuel logistics and handling requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of sustainable aviation fuels

- 3.2.3.2 Advancements in additive formulation technologies

- 3.2.3.3 Improved fuel system protection requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By additive type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Additive Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dispersants

- 5.3 Antioxidants

- 5.4 Anti-icing

- 5.5 Corrosion inhibitors

- 5.6 Antiknock

- 5.7 Metal deactivators

- 5.8 Others (fuel stabilizers, combustion improvers)

Chapter 6 Market Estimates and Forecast, By Fuel Type, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Aviation gasoline

- 6.3 Jet fuel

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Commercial aircraft

- 7.3 Passenger aircraft

- 7.4 Cargo aircraft

- 7.5 Military aircraft

- 7.6 Others (private jets, helicopters)

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Afton Chemical Corporation

- 9.2 Chevron Corporation

- 9.3 BASF SE

- 9.4 Biobor Fuel Additives

- 9.5 Dorf-Ketal Chemicals India Pvt., Ltd.

- 9.6 Innospec Chemical Company

- 9.7 Meridian Fuels

- 9.8 Nalco an Ecolab Company

- 9.9 LANXESS Deutschland GmbH

- 9.10 A S Harrison & Co

運輸燃料市場:依燃料類型、來源、混合比例、最終用戶和分銷管道分類-2026-2032年全球市場預測航空燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、飛機類型、原料、添加劑、最終用戶和分銷管道分類)

運輸燃料市場:依燃料類型、來源、混合比例、最終用戶和分銷管道分類-2026-2032年全球市場預測航空燃料市場:2026-2032年全球市場預測(按燃料類型、混合比例、飛機類型、原料、添加劑、最終用戶和分銷管道分類) 航空燃料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球航空燃油終端市場規模、佔有率、趨勢及成長分析報告(2026-2034)

航空燃料市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年全球航空燃油終端市場規模、佔有率、趨勢及成長分析報告(2026-2034) 航空燃料市場報告:按燃料類型、飛機類型、最終用途和地區分類,2026-2034年

航空燃料市場報告:按燃料類型、飛機類型、最終用途和地區分類,2026-2034年 2026年全球航空燃料市場報告航空汽油(Avgas)市場規模、佔有率、成長及全球產業分析:依終端用戶和地區劃分的洞察與預測(2026-2034)

2026年全球航空燃料市場報告航空汽油(Avgas)市場規模、佔有率、成長及全球產業分析:依終端用戶和地區劃分的洞察與預測(2026-2034) 航空燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按燃料類型、應用、類型、地區和競爭格局分類,2021-2031年運輸燃料市場-全球產業規模、佔有率、趨勢、機會和預測:按燃料類型、最終用戶、地區和競爭對手分類,2021-2031年

航空燃料市場-全球產業規模、佔有率、趨勢、機會、預測:按燃料類型、應用、類型、地區和競爭格局分類,2021-2031年運輸燃料市場-全球產業規模、佔有率、趨勢、機會和預測:按燃料類型、最終用戶、地區和競爭對手分類,2021-2031年 2026-2030年全球國防飛機航空燃料市場

2026-2030年全球國防飛機航空燃料市場