|

市場調查報告書

商品編碼

2073514

印度建設化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

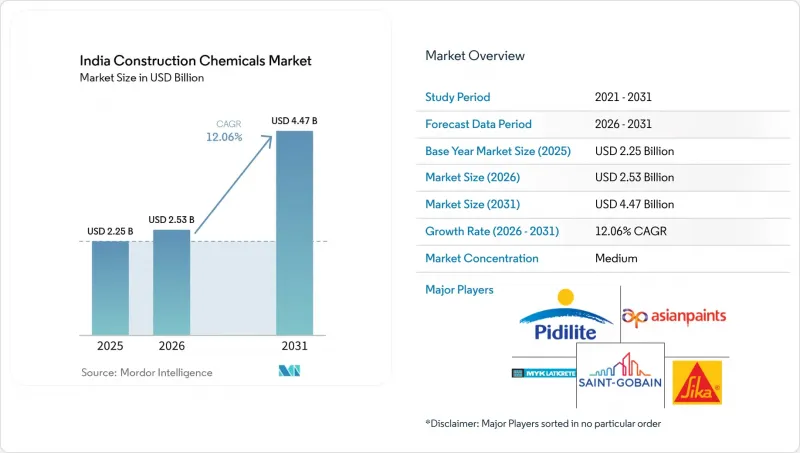

根據 Mordor Intelligence 預測,印度建設化學品市場規模將從 2025 年的 22.5 億美元成長到 2026 年的 25.3 億美元,到 2031 年將達到 44.7 億美元,2026 年至 2031 年的複合年成長率為 12.06%。

本報告按產品類別(黏合劑、錨固件和水泥漿、混凝土外加劑、混凝土保護塗料、地板樹脂、修補和再生化學品、密封劑、表面處理化學品、防水解決方案)和最終用途類別(商業、工業和公共設施、基礎設施、住宅)進行細分。市場預測以價值(美元)表示。

印度建設化學品市場趨勢與洞察

大型基礎設施項目正在推動對特種外加劑的需求。

國家基礎設施規劃預算撥款為地鐵隧道、沿海橋樑和地震多發地區的架空橋樑等項目帶來了穩定且大量的高性能減水劑、腐蝕抑制劑和抗收縮外加劑訂單。孟買地鐵3號線和德里梅拉特快速交通系統(RRTS)所需的高規格混凝土具有高初始強度和低滲透性,從而推動了對高品質聚羧酸醚類化學品的需求。根據「印度公路網計畫」(Bharatmala-Pariyojana)進行的公路建設計畫日益強調基於性能的混凝土配合比設計,競標文件中明確規定了高性能減水劑和空氣混合劑的用量。因此,供應商正在調整其研發方向,使其符合抗災基礎設施建設指南,並推出用於易受地下水滲漏影響的明挖回填段的纖維增強聚合物體系和結晶質建設化學品產品系列。這些趨勢與公共部門的發展規劃密切相關,促使在專案集中區域附近建立區域庫存中心,以最大限度地縮短前置作業時間。因此,在全球特種樹脂原料日益短缺的情況下,擁有關鍵單體後端連接的一體化製造商正在確保成本競爭優勢。

從現場攪拌混凝土過渡到預拌混凝土

隨著預拌混凝土(RMC)的日益普及,添加劑的訂購模式正轉向與攪拌站營運商簽訂批量供應合約。由於RMC即使經過長途運輸也能保持穩定的坍落度,因此對緩凝劑、黏度調節劑和泵送輔助劑的需求不斷成長——這些添加劑在小型現場攪拌機中很少使用。如今,自動化配料系統已直接與ERP平台整合,使供應商能夠即時監控用量並遠端最佳化配方調整。在土地資源有限的都市區地區,建築商更傾向於使用RMC以最大限度地減少交通干擾,這進一步增加了對多年框架合約下捆綁式添加劑包的需求。隨著區域營運商投資於線上水分感測器和流變控制設備,印度建設化學品市場正從通用散裝粉末轉向包含服務的化學解決方案,其中技術諮詢費用已包含在產品發票中。這種轉變提高了缺乏應用工程能力的非正規配料商的進入門檻。

石油化學樹脂價格波動

2024年環氧樹脂和聚氨酯樹脂價格的波動阻礙了專案預算的製定,並侵蝕了小規模製造商的營運資金儲備。外匯波動增加了MDI和TDI進口的成本轉嫁風險,而紅海運輸中斷則使前置作業時間週期延長了一個月。大型企業透過使用原油期貨合約和其他避險工具來應對這些衝擊,而區域性混合商則難以適應原料成本和售價的波動,導致交貨延遲。承包商擔心專案進行中價格重置,有時會重新使用基本的砂漿混合物,這減緩了高等級材料的採用。政府針對特種化學品的生產連結獎勵計畫(PLI)計劃可能在中期內緩解這些風險。然而,短期內,利潤率的壓縮嚴重影響了新增產能的決策,減緩了印度建設化學品市場的成長勢頭,而該市場原本應該表現良好。

細分市場分析

至2025年,防水解決方案將佔印度建設化學品市場的35.15%。這主要歸因於季風氣候城市對強效靜水壓防護的需求不斷成長,以及地下室建設的興起。在孟買、清奈和科欽等鹽霧腐蝕風險較高的城市,強制性的屋頂處理保固政策也推動了這一領域的發展。瀝青卷材正逐漸被結晶質外加劑和改質聚氨酯膜所取代,這些新型材料厚度更薄,使用壽命更長。供應商正利用價值工程,將現場診斷和紅外線熱成像服務整合到產品包裝中,從而提升銷售無溶劑底漆和濕固化面漆的銷售。在印度西部,由於地鐵擴建工程相關的隧道防水工作,PVC膜的銷售量保持穩定,這為國內擠出生產線帶來了規模經濟效益。此外,由於中等收入住宅熱潮,應用範圍擴大到陽台、平台和水箱,這也使得 SKU 週轉範圍從高價基礎設施項目擴展到其他領域。

混凝土外加劑市場的發展主要受預拌混凝土(RMC)廠的普及和基於性能的競標標準的推動。高強度、高減水率的外加劑使地鐵施工人員能夠在夜間進行混凝土澆築,而具有保坍和延緩凝固效果的混合料則滿足了交通堵塞的大都會圈60分鐘運輸距離的要求。隨著對高價值等級外加劑需求的成長,預計印度建設化學品市場中外加劑的市場佔有率將超過通用灰粉。黏合劑和外牆板對黏合劑、錨固件和水泥漿的需求不斷成長,快速固化的聚酯樹脂滿足了垂直建築的施工速度要求。防護塗層被應用於污水泵站、海水淡化廠和化學品儲存場等對耐酸性要求極高的場所。以環氧水磨石和聚氨酯水泥為代表的地板樹脂,因其能夠滿足HACCP和無塵室標準,在製藥、食品和飲料工廠中越來越受歡迎。修補化學品透過用於橋樑梁體和煙囪修補的專用碳纖維包裹物,打入了高價市場,即使在新建工程停滯時期,也能增強收入結構的韌性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大型基礎設施項目正在推動對特種外加劑的需求。

- 從現澆混凝土過渡到預拌混凝土

- 綠色標籤認證產品的快速普及

- 擴大維修和重組項目

- 對經濟適用住宅專案的需求不斷成長

- 市場限制因素

- 石化樹脂價格波動

- 施用器生態系的分散性阻礙了規範的遵守。

- 地緣政治風險下的特種原料進口依賴

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依產品

- 黏合劑

- 熱熔膠

- 反應性

- 溶劑型

- 水溶液

- 錨栓和水泥漿

- 水泥基固定材料

- 樹脂固定

- 混凝土外加劑

- 過早狹窄

- 空氣注入劑

- 高效減水劑

- 延誤代理人

- 收縮抑制劑

- 黏度調節劑

- 塑化劑

- 其他類型

- 混凝土保護塗層

- 丙烯酸纖維

- 阿爾基多

- 環氧樹脂

- 聚氨酯

- 其他樹脂

- 地板樹脂

- 丙烯酸纖維

- 環氧樹脂

- 聚天門冬胺酸

- 聚氨酯

- 其他樹脂

- 用於維修和修復的化學品

- 纖維纏繞系統

- 水泥漿

- 微混凝土砂漿

- 改質砂漿

- 鋼筋保護劑

- 密封劑

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 表面處理化學品

- 硬化劑

- 釋放劑

- 其他類型

- 防水解決方案

- 化學品

- 膜

- 黏合劑

- 按最終用途類別

- 商業

- 工業和公共機構

- 基礎設施

- 住宅

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- ADT Industries Private Limited

- Ardex Endura(India)Pvt Ltd

- Arkema(Bostik)

- Asian Paints

- Berger Paints India Ltd.

- Chembond Chemicals Limited

- CICO Group

- ECMAS Group

- HB Fuller Company

- Henkel AG & Co. KGaA

- Jotun

- Kansai Nerolac Paints Ltd.

- MAPEI SpA

- MC-Bauchemie

- MYK LATICRETE India, Inc.

- PENETRON

- Pidilite Industries Ltd.

- RPM International

- Saint-Gobain

- Sika AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the india construction chemicals market size is expected to grow from USD 2.25 billion in 2025 to USD 2.53 billion in 2026 and is forecast to reach USD 4.47 billion by 2031 at 12.06% CAGR over 2026-2031.

This report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, Surface-Treatment Chemicals, and Waterproofing Solutions), and End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential). The Market Forecasts are Provided in Terms of Value (USD).

India Construction Chemicals Market Trends and Insights

Mega-infrastructure pipeline boosts specialty admixture demand

National Infrastructure Pipeline allocations channel steady large-volume orders toward high-range water reducers, corrosion inhibitors, and shrinkage-reducing admixtures needed for metro tunneling, coastal bridges, and seismic-zone viaducts. High-specification concrete for the Mumbai Metro Line 3 and Delhi-Meerut RRTS requires elevated early strength and low permeability, thereby heightening demand for premium polycarboxylate-ether chemistries. Highway packages under the Bharatmala Pariyojana are increasingly mandating performance-based mixes, which embed superplasticizer and air-entrainment dosages in tender documents. Suppliers therefore align research and development pipelines to resilient-infrastructure guidelines, releasing fiber-reinforced polymer systems and crystalline waterproofing lines for cut-and-cover segments exposed to groundwater ingress. These dynamics keep the India construction chemicals market closely tethered to public-sector rollout timetables, with regional stocking hubs springing up near project clusters to minimize lead times. Consequently, integrated producers with backward linkages to key monomers secure a competitive cost advantage as specialty-grade resin inputs become increasingly scarce globally.

Transition from on-site mixed concrete to ready-mixed concrete

RMC penetration is increasing, reshaping reagent ordering cycles toward bulk-supply contracts with batching plant operators. Consistent slump retention across long haul times pushes demand for retarding admixtures, viscosity-modifying agents, and pumping aids that small on-site mixers seldom use. Automated dosing systems now integrate directly with ERP platforms, enabling suppliers to monitor real-time consumption and remotely optimize formulation tweaks. Metro contractors in land-scarce downtown cores favor RMC to curtail traffic disruptions, strengthening the captive pull for additive packages bundled under multi-year framework agreements. As regional players invest in inline moisture sensors and rheology controllers, the India construction chemicals market deepens its shift from commodity bulk powders toward service-wrapped chemistry solutions that embed technical advisory fees within product invoices. This transformation raises entry barriers for unorganized formulators lacking application engineering bandwidth.

Volatility in petro-chemical-based resin prices

Price swings in epoxy and polyurethane resins during 2024 hindered project budgeting and eroded the working capital buffers of small manufacturers. Currency fluctuation layered extra cost-pass-through risk onto imports of MDI and TDI, while Red Sea freight disruptions extended lead times by a month. Larger players absorbed shocks by tapping term crude contracts and using hedging instruments, but regional blenders struggled to synchronize selling prices with volatile input costs, resulting in delivery delays. Contractors, wary of mid-project price resets, sometimes reverted to basic cement-sand blends, which dampened the uptake of premium-grade materials. Government Production-Linked Incentive (PLI) frameworks for specialty chemicals may alleviate exposure over the medium term; however, in the interim, margin compression weighs on new capacity decisions, tempering the otherwise upbeat trajectory of the India construction chemicals market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid penetration of green-label certified products

- Growth of renovation and reconstruction projects

- Fragmented applicator ecosystem limits specification compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions captured 35.15% of India's construction chemicals market share in 2025 as monsoon-exposed cities and rising basement construction heightened the need for robust hydrostatic protection. The segment benefits from mandated roof-treatment warranties in Mumbai, Chennai, and Kochi, where saline spray accelerates corrosion. Bitumen-based sheets are gradually being replaced by crystalline admixtures and modified polyurethane membranes, which offer longer life-cycle value with thinner profiles. Suppliers bundle site diagnostics and IR-thermography services into product packages, leveraging value engineering to upsell solvent-free primers and moisture-curing topcoats. Across Western India, tunnel waterproofing for metro extensions sustains a steady volume of PVC membrane sales, injecting scale efficiencies into domestic extrusion lines. Complementary growth arises from balcony, podium, and water tank applications within the mid-income housing boom, broadening SKU rotation beyond big-ticket infrastructure projects.

Concrete admixtures are driven by the uptake of RMC plants and performance-based tender norms. Early-strength superplasticizers secure night concreting windows for metro contractors, while slump-retention retarding blends support 60-minute haul distances in congested metros. As value-added grades grow, the India construction chemicals market size for admixtures is projected to outpace that of commodity grey powders. Adhesives, anchors, and grouts gain traction from precast modules and facade panels, with rapid-curing polyester resins supporting vertical construction speed targets. Protective coatings line sewage lift stations, desalination plants, and chemical storage yards where high acid resistance is critical. Flooring resins, led by epoxy terrazzo and polyurethane cement, are gaining traction in pharmaceutical and food and beverage plants to meet HACCP and cleanroom standards. Repair chemicals unlock premium price points through specialty carbon-fiber wraps for bridge girders and chimney stack rehabilitation, adding resilience to revenue mixes during new-build pauses.

Complete Report Scope:

- By Product

- Adhesives

- Hot-Melt

- Reactive

- Solvent-borne

- Water-borne

- Anchors and Grouts

- Cementitious Fixing

- Resin Fixing

- Concrete Admixtures

- Accelerator

- Air-Entraining

- Super-plasticizer

- Retarder

- Shrinkage-Reducer

- Viscosity-Modifier

- Plasticizer

- Other Types

- Concrete Protective Coatings

- Acrylic

- Alkyd

- Epoxy

- Polyurethane

- Other Resins

- Flooring Resins

- Acrylic

- Epoxy

- Polyaspartic

- Polyurethane

- Other Resins

- Repair and Rehabilitation Chemicals

- Fiber-Wrapping Systems

- Injection Grouting

- Micro-concrete Mortars

- Modified Mortars

- Rebar Protectors

- Sealants

- Acrylic

- Epoxy

- Polyurethane

- Silicone

- Other Resins

- Surface-Treatment Chemicals

- Curing Compounds

- Mold-Release Agents

- Other Types

- Waterproofing Solutions

- Chemicals

- Membranes

- Adhesives

- By End-Use Sector

- Commercial

- Industrial and Institutional

- Infrastructure

- Residential

List of Companies Covered in this Report:

- 3M

- ADT Industries Private Limited

- Ardex Endura (India) Pvt Ltd

- Arkema (Bostik)

- Asian Paints

- Berger Paints India Ltd.

- Chembond Chemicals Limited

- CICO Group

- ECMAS Group

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jotun

- Kansai Nerolac Paints Ltd.

- MAPEI S.p.A.

- MC-Bauchemie

- MYK LATICRETE India, Inc.

- PENETRON

- Pidilite Industries Ltd.

- RPM International

- Saint-Gobain

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mega-infrastructure pipeline boosts specialty admixture demand

- 4.2.2 Transition from on-site mixed concrete to ready-mixed concrete

- 4.2.3 Rapid penetration of green-label certified products

- 4.2.4 Growth of renovation and reconstruction projects

- 4.2.5 Rising need for affordable housing projects

- 4.3 Market Restraints

- 4.3.1 Volatility in petro-chemical-based resin prices

- 4.3.2 Fragmented applicator ecosystem limits specification compliance

- 4.3.3 Import dependency on specialty raw materials amid geopolitical risks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ADT Industries Private Limited

- 6.4.3 Ardex Endura (India) Pvt Ltd

- 6.4.4 Arkema (Bostik)

- 6.4.5 Asian Paints

- 6.4.6 Berger Paints India Ltd.

- 6.4.7 Chembond Chemicals Limited

- 6.4.8 CICO Group

- 6.4.9 ECMAS Group

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Jotun

- 6.4.13 Kansai Nerolac Paints Ltd.

- 6.4.14 MAPEI S.p.A.

- 6.4.15 MC-Bauchemie

- 6.4.16 MYK LATICRETE India, Inc.

- 6.4.17 PENETRON

- 6.4.18 Pidilite Industries Ltd.

- 6.4.19 RPM International

- 6.4.20 Saint-Gobain

- 6.4.21 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

東南亞建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

東南亞建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 建築化學品市場預測至2034年-按產品類型、化學品類型、應用、最終用途和地區分類的全球分析

建築化學品市場預測至2034年-按產品類型、化學品類型、應用、最終用途和地區分類的全球分析 建築化學品市場規模、佔有率和成長分析:黏合劑和密封劑、混凝土外加劑、砂漿和水泥漿、防水化學品、修補和保護劑以及地區分類-2026-2033年產業預測越南建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

建築化學品市場規模、佔有率和成長分析:黏合劑和密封劑、混凝土外加劑、砂漿和水泥漿、防水化學品、修補和保護劑以及地區分類-2026-2033年產業預測越南建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 建築化學品市場:2026-2032年全球市場預測(依產品類型、技術、劑型、建築類型、應用、最終用戶和通路分類)固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年

建築化學品市場:2026-2032年全球市場預測(依產品類型、技術、劑型、建築類型、應用、最終用戶和通路分類)固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年 建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)