|

市場調查報告書

商品編碼

1938988

歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

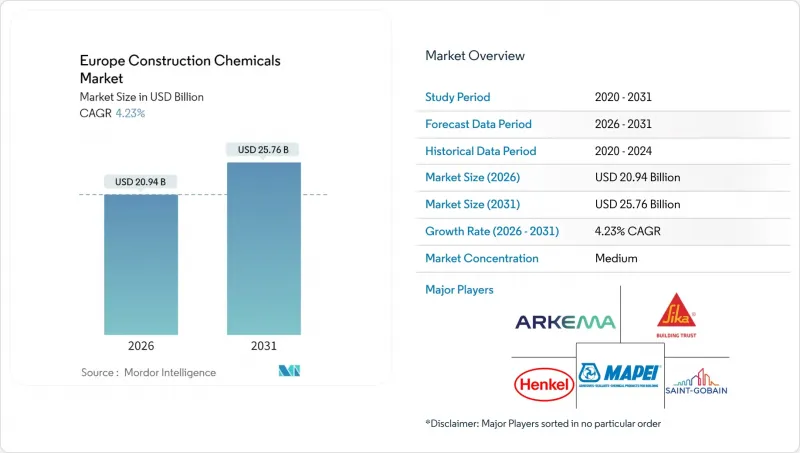

預計到 2026 年,歐洲建築化學品市場規模將達到 209.4 億美元。

這意味著從 2025 年的 200.9 億美元成長到 2031 年的 257.6 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.23%。

儘管週期性放緩,建設業仍在持續擴張,這得益於歐盟綠色交易、建築能源性能指令 (EPBD) 和歐洲互聯互通基金 (CEF) 等公共部門獎勵策略,這些措施推動了低碳材料和基礎設施更新方面的支出。隨著計劃業主採用強制性環境產品聲明 (EPD),那些將專業配方技術與檢驗的環境資格相結合的供應商越來越有可能贏得專案。產業整合正在加速,聖戈班以 10.25 億美元收購福斯羅克 (Fosroc) 就是一個例證。同時,西卡 (Sika) 等主要企業正利用地域多元化和特種產品系列來維持利潤率。雖然原料成本波動,尤其是環氧樹脂和聚氨酯原料的價格波動,給盈利帶來壓力,但生物基、不含全氟烷基物質 (PFAS) 和負碳化學技術的創新正在創造新的收入來源,並增強歐洲建設化學品市場的監管應對力。

歐洲建設化學品市場趨勢與洞察

歐盟綠色交易資金推動了對永續建築的需求。

1兆歐元的「綠色交易」投資框架要求到2030年對3500萬棟建築進行低碳維修,這將直接提振對生物基外加劑、再生防水材料和負碳添加劑的需求,從而支撐歐洲建設化學品市場。BASF於2024年底推出的生物基丙烯酸乙酯,在保持性能的同時,將產品碳足跡降低了30%,這標誌著供應商正在調整策略,為應對2024/3110號建築產品法規中強制性的環境產品聲明要求做好準備。財政獎勵和綠色債券合格促使消費者傾向於選擇具有透明生命週期數據的產品,從而在歐洲建設化學品市場中催生了一個高階細分市場。政府的維修補貼使得高性能密封劑、絕緣黏合劑和液態防水膜成為市政住宅營運商的核心採購重點。預計2026年社會氣候基金的資金增加將鞏固此促進因素的中期重要性,因為市場對節能化學品的需求將持續超過傳統替代方案。

歐盟「互聯歐洲基金」(CEF)將促進跨國基礎設施支出

總額達337億歐元的「氣候工程基金2021-2027」計畫將資金投入鐵路、隧道和港口計劃,從而推動對高性能外加劑、快凝砂漿和隧道防水材料等特種化學品的需求,尤其是在波羅的海鐵路和地中海連接線等沿線地區。滿足氣候適應資產標準有利於碳纖維增強系統和自修復混凝土的應用,這些材料能夠延長建築物的使用壽命。僅由「氣候工程基金」共同資助的「大巴黎快線」計畫就需要大量噴塗防水膜和低排放量混凝土速凝劑。能夠認證多用途系統符合多項國家標準的供應商將在競標獲得競爭優勢,這將在「氣候工程基金2021-2027」計畫結束及下一階段(計畫於2028年啟動)期間,進一步鞏固歐洲建設化學品市場的發展勢頭。

環氧樹脂、聚氨酯和丙烯酸原料的價格波動

受庫存緊張和對亞洲進口環氧樹脂徵收10.8%至40.8%反傾銷稅的影響,2025年1月環氧樹脂現貨價格上漲1.73%。聚氨酯前驅物價格受原油價格波動的影響,而高耗能的丙烯酸單體產業鏈則面臨歐洲電力成本上漲的挑戰。小規模混煉企業往往缺乏避險和後向整合,這擠壓了利潤空間並減緩了創新投資。部分客戶延後了非必要的維修工程,略微抑制了歐洲建設化學品市場的銷售。儘管主要生產商已簽署長期契約,但預計到2026年,採購的不確定性仍將對價格上漲構成不利影響。

細分市場分析

2025年,防水系統佔據了歐洲建設化學品市場31.62%的佔有率,這主要得益於隧道、地下室和橋面等建築對耐久性的嚴格要求。該領域的領先地位歸功於避免高昂的故障成本,終端用戶儘管價格較高,但仍傾向於選擇優質防水卷材和液態塗料。 2024年,隨著公共部門維修津貼優先用於提升防潮性能,歐洲建設化學品市場在防水領域的規模穩定成長。流域防洪措施的加強也提振了需求,推動了真空側漿砂漿和彈性體覆蓋層的應用。產品創新主要集中在不含PFAS的聚合物、生物基瀝青改質劑以及即使在熱循環條件下也能保持黏合力的奈米二氧化矽增強塗料。 SOPREMA的收購策略透過整合瀝青、聚甲基丙烯酸甲酯(PMMA)和聚氨酯技術並提供系統質保,增強了客戶留存率。同時,供應商正在加速開發與 BIM 工作流程整合的數位化細部設計工具,以提高規範合規性並減少施工錯誤。

混凝土外加劑是成長最快的產品線,預計到2031年將以5.05%的複合年成長率成長,這主要得益於基礎設施業主尋求符合低碳目標的高性能外加劑。高性能減水劑、自密實劑和收縮補償劑價格較高,推動了歐洲建設化學品市場外加劑市場規模的擴大,銷售量也隨之成長。監管壓力推動了對低鹼外加劑和六價鉻減量塑化劑的需求,而研發開發平臺放在能夠提高水泥強度比的奈米粘土分散技術上。黏合劑和密封劑在帷幕牆、地板材料和建築幕牆應用中保持著穩定的需求,而PFAS的逐步淘汰正在推動矽酮和矽烷封端聚合物替代品的湧現,重塑歐洲建築化學品行業的競爭格局。由於具有靜電耗散和耐化學腐蝕的特性,地板樹脂在關鍵任務型資料中心和物流樞紐中越來越受歡迎。同時,錨固件和水泥漿在風電場基礎和工業廠房維修中保持著適度的成長。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 歐盟綠色交易資金推動了對永續建築的需求。

- 透過歐盟互聯互通基金(CEF)促進跨境基礎設施投資

- 更嚴格的EPBD能源效率標準增加了對高性能外加劑的需求。

- 碳中和混凝土概念採用新型水泥基輔助材料

- 綠色氫氣巨型工廠的發展推動了低溫儲槽專用水泥漿的需求

- 市場限制

- 環氧樹脂、聚氨酯和丙烯酸原料的價格波動

- 嚴格的VOC和PFAS逐步淘汰法規限制了溶劑型化學品的使用。

- 高級地板材料和維修系統認證安裝人員短缺

- 監管環境

- 價值鏈分析

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 終端用戶產業趨勢

第5章 市場規模與成長預測

- 依產品

- 黏合劑

- 熱熔膠

- 反應性

- 溶劑型

- 水溶液

- 錨栓和水泥漿

- 水泥基固定材料

- 樹脂固定

- 混凝土外加劑

- 加速器

- 空氣引射器

- 高效減水劑

- 緩速器

- 收縮抑制劑

- 黏度調節劑

- 塑化劑

- 其他

- 混凝土保護塗層

- 丙烯酸纖維

- 醇酸樹脂

- 環氧樹脂

- 聚氨酯

- 其他樹脂

- 地板樹脂

- 丙烯酸纖維

- 環氧樹脂

- 聚天門冬胺酸

- 聚氨酯

- 其他樹脂

- 維修和維修化學品

- 纖維纏繞系統

- 水泥漿

- 微型混凝土砂漿

- 改質砂漿

- 鋼筋保護材料

- 密封劑

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 表面處理化學品

- 固化劑

- 釋放劑

- 其他

- 防水解決方案

- 化學品

- 防水膜

- 黏合劑

- 按最終用戶類別

- 商業的

- 工業和公共設施

- 基礎設施

- 住宅

- 按地區

- 法國

- 德國

- 義大利

- 俄羅斯

- 西班牙

- 英國

- 其他歐洲地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率**(%)/排名分析

- 公司簡介

- Ardex Group

- Arkema(Bostik)

- CEMEX SAB de CV

- HA-BE BETONCHEMIE

- Henkel AG and Co. KGaA

- Kao Chemicals Europe, SLU

- Kingspan Group

- MAPEI SpA

- MC-Bauchemie

- PCI Augsburg GmbH

- RPM International Inc.

- Saint-Gobain

- Schomburg

- Selena Group

- Sika AG

- SOPREMA Group

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

Europe Construction Chemicals market size in 2026 is estimated at USD 20.94 billion, growing from 2025 value of USD 20.09 billion with 2031 projections showing USD 25.76 billion, growing at 4.23% CAGR over 2026-2031.

Expansion continues despite cyclical construction slowdowns because public-sector stimulus under the EU Green Deal, the Energy Performance of Buildings Directive (EPBD), and the Connecting Europe Facility steers spending toward low-carbon materials and infrastructure upgrades. Suppliers that combine specialty formulations with verifiable environmental credentials are more likely to win specifications as project owners adopt mandatory Environmental Product Declarations (EPDs). Consolidation accelerates, illustrated by Saint-Gobain's USD 1.025 billion acquisition of FOSROC, while leaders such as Sika leverage geographic diversification and specialty product portfolios to protect margins. Raw-material cost volatility, chiefly in epoxy and polyurethane feedstocks, pressures profitability, yet innovation in bio-based, Per- and Polyfluoroalkyl Substances (PFAS)-free, and carbon-negative chemistries creates new revenue streams and improves regulatory resilience across the Europe Construction Chemicals market.

Europe Construction Chemicals Market Trends and Insights

EU Green Deal funding accelerates sustainable construction demand

The EUR 1 trillion Green Deal investment framework mandates low-carbon renovation across 35 million buildings by 2030, directly increasing volumes for bio-based admixtures, recycled-content waterproofing, and carbon-negative additives that underpin the Europe Construction Chemicals market. BASF's bio-based ethyl acrylate launch in late 2024 cut product carbon footprints by 30% while maintaining performance, signaling supplier realignment toward mandatory environmental product declarations under Construction Products Regulation 2024/3110. Financial incentives and green bond eligibility heighten customer preference for products with transparent life-cycle data, creating a premium segment within the Europe Construction Chemicals market. Government renovation subsidies make high-performance sealants, insulation adhesives, and liquid-applied membranes core purchasing priorities for municipal housing operators. As more funding flows from the Social Climate Fund in 2026, market demand for energy-efficient chemistries continues to outpace conventional alternatives, cementing the driver's medium-term importance.

EU Connecting Europe Facility boosts trans-border infrastructure spend

The EUR 33.7 billion CEF 2021-2027 program channels capital into rail, tunnel, and port projects, thereby increasing demand for specialty chemicals such as high-performance admixtures, rapid-setting mortars, and tunnel waterproofing along corridors like Rail Baltica and the Mediterranean link. Compliance with climate-resilient asset criteria favors carbon-fiber-reinforced systems and self-healing concrete, which extend the structure's lifespan. The Grand Paris Express, co-funded through CEF, alone consumes sizable volumes of spray-applied membranes and low-emission concrete accelerators. Suppliers able to certify multipurpose systems across several national standards secure bid advantages, reinforcing growth momentum for the Europe Construction Chemicals market until the program's close and anticipated sequel in 2028.

Volatile prices of epoxy, PU, and acrylic feedstocks

January 2025 spot epoxy resin prices increased by 1.73% as inventories tightened and anti-dumping duties of 10.8%-40.8% were imposed on Asian imports. Polyurethane precursors mirror crude volatility, while energy-intensive acrylic monomer chains face elevated European power costs. Smaller formulators often lack hedging or backward integration, which erodes margins and delays innovation spending. Some customers defer nonessential renovations, marginally dampening volumes in the Europe Construction Chemicals market. Although major producers negotiate long-term contracts, procurement uncertainty is expected to remain a pricing headwind through 2026.

Other drivers and restraints analyzed in the detailed report include:

- Stricter EPBD energy-efficiency codes increase demand for high-performance admixtures

- Carbon-neutral concrete initiatives adopt novel supplementary cementitious materials

- Stringent VOC and PFAS phase-out regulations restrict solvent-borne chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing systems secured a 31.62% Europe Construction Chemicals market share in 2025, underpinned by stringent durability requirements for tunnels, basements, and bridge decks. The segment's dominance stems from high failure-cost avoidance, which makes end-users favor premium membranes and liquid-applied coatings despite the price premiums. The Europe Construction Chemicals market size for waterproofing grew steadily in 2024 as public-sector renovation grants prioritized moisture-control upgrades. Demand also benefits from rising flood-risk mitigation in riverine regions, encouraging uptake of negative-side slurry mortars and elastomeric overlays. Product innovation focuses on PFAS-free polymers, bio-based asphalt modifiers, and nano-silica-enhanced coatings that maintain adhesion under thermal cycling. SOPREMA's acquisition strategy combines bitumen, Polymethyl methacrylate (PMMA), and polyurethane technologies, offering system warranties that tighten customer lock-in. Meanwhile, suppliers are accelerating the development of digital detailing tools that integrate with BIM workflows, thereby improving specification compliance and reducing installation errors.

Concrete admixtures represent the fastest-growing product line, with a 5.05% CAGR to 2031, as infrastructure owners demand high-performance mixes that are compatible with low-carbon objectives. High-range water reducers, self-consolidating agents, and shrinkage-compensating additives command premium pricing, lifting the Europe Construction Chemicals market size for admixtures alongside volume growth. Regulatory pressure boosts demand for low-alkali accelerators and chromium-VI-reduced plasticizers, while R&D pipelines focus on nano-clay dispersion technologies that enhance the strength-to-cement ratio. Adhesives and sealants maintain stable demand across curtain-wall, flooring, and facade applications, yet PFAS phase-outs catalyze a wave of silicone and silane-terminated polymer replacements, reshaping competitive positioning inside the Europe Construction Chemicals industry. Flooring resins are gaining traction in data centers and logistics hubs, where static-dissipative and chemical-resistant surfaces are mission-critical. In contrast, anchors and grouts are securing moderate growth in wind-farm foundations and industrial plant retrofits.

The Europe Construction Chemicals Market Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Sealants, and More), End-User Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (France, Germany, Italy, Russia, Spain, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Ardex Group

- Arkema (Bostik)

- CEMEX S.A.B de C.V

- HA-BE BETONCHEMIE

- Henkel AG and Co. KGaA

- Kao Chemicals Europe, S.L.U.

- Kingspan Group

- MAPEI S.p.A.

- MC-Bauchemie

- PCI Augsburg GmbH

- RPM International Inc.

- Saint-Gobain

- Schomburg

- Selena Group

- Sika AG

- SOPREMA Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Green Deal funding accelerates sustainable construction demand

- 4.2.2 EU Connecting Europe Facility boosts trans-border infrastructure spend

- 4.2.3 Stricter EPBD energy-efficiency codes increase demand for high-performance admixtures

- 4.2.4 Carbon-neutral concrete initiatives adopt novel supplementary cementitious materials

- 4.2.5 Growth of green-hydrogen mega-plants drives specialty grouts for cryogenic tanks

- 4.3 Market Restraints

- 4.3.1 Volatile prices of epoxy, PU, and acrylic feedstocks

- 4.3.2 Stringent VOC and PFAS phase-out regulations restrict solvent-borne chemistries

- 4.3.3 Shortage of certified applicators for advanced flooring and repair systems

- 4.4 Regulatory Landscape

- 4.5 Value Chain Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 End-use Sector Trends

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-Melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious Fixing

- 5.1.2.2 Resin Fixing

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-Entraining

- 5.1.3.3 Super-plasticizer

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-Reducer

- 5.1.3.6 Viscosity-Modifier

- 5.1.3.7 Plasticizer

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-Wrapping Systems

- 5.1.6.2 Injection Grouting

- 5.1.6.3 Micro-concrete Mortars

- 5.1.6.4 Modified Mortars

- 5.1.6.5 Rebar Protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-Treatment Chemicals

- 5.1.8.1 Curing Compounds

- 5.1.8.2 Mold-Release Agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-User Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

- 5.3 By Geography

- 5.3.1 France

- 5.3.2 Germany

- 5.3.3 Italy

- 5.3.4 Russia

- 5.3.5 Spain

- 5.3.6 United Kingdom

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ardex Group

- 6.4.2 Arkema (Bostik)

- 6.4.3 CEMEX S.A.B de C.V

- 6.4.4 HA-BE BETONCHEMIE

- 6.4.5 Henkel AG and Co. KGaA

- 6.4.6 Kao Chemicals Europe, S.L.U.

- 6.4.7 Kingspan Group

- 6.4.8 MAPEI S.p.A.

- 6.4.9 MC-Bauchemie

- 6.4.10 PCI Augsburg GmbH

- 6.4.11 RPM International Inc.

- 6.4.12 Saint-Gobain

- 6.4.13 Schomburg

- 6.4.14 Selena Group

- 6.4.15 Sika AG

- 6.4.16 SOPREMA Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

印度建設化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)東南亞建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

印度建設化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)東南亞建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 建築化學品市場預測至2034年-按產品類型、化學品類型、應用、最終用途和地區分類的全球分析

建築化學品市場預測至2034年-按產品類型、化學品類型、應用、最終用途和地區分類的全球分析 建築化學品市場規模、佔有率和成長分析:黏合劑和密封劑、混凝土外加劑、砂漿和水泥漿、防水化學品、修補和保護劑以及地區分類-2026-2033年產業預測越南建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

建築化學品市場規模、佔有率和成長分析:黏合劑和密封劑、混凝土外加劑、砂漿和水泥漿、防水化學品、修補和保護劑以及地區分類-2026-2033年產業預測越南建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 建築化學品市場:2026-2032年全球市場預測(依產品類型、技術、劑型、建築類型、應用、最終用戶和通路分類)固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年

建築化學品市場:2026-2032年全球市場預測(依產品類型、技術、劑型、建築類型、應用、最終用戶和通路分類)固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年 建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)