|

市場調查報告書

商品編碼

1939004

建築化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

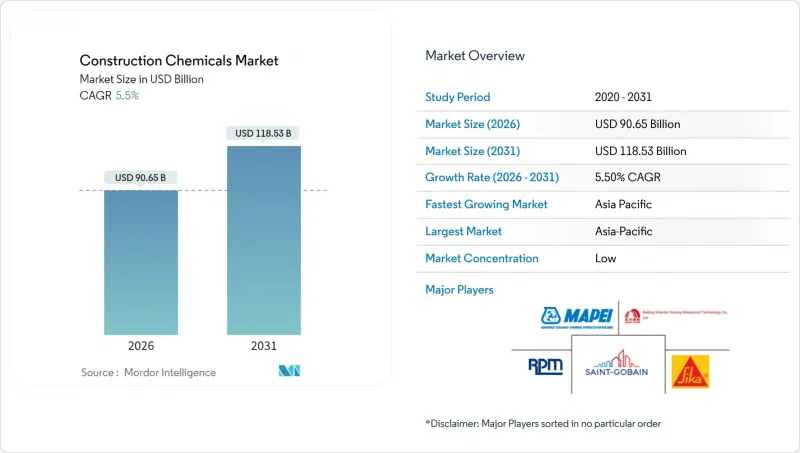

預計到 2026 年,建築化學品市場規模將達到 906.5 億美元,高於 2025 年的 859.2 億美元。

預計到 2031 年將達到 1,185.3 億美元,2026 年至 2031 年的複合年成長率為 5.5%。

穩健的城市基礎設施規劃、更嚴格的綠色建築法規以及穩定的住宅需求共同推動了建築化學品市場的成長前景。防水系統是產品收入的基石,因為保險公司和建築規範機構都將防潮作為首要任務,而先進的表面處理技術在自動化預製構件廠中也日益普及。亞太地區的成長勢頭最為強勁,大型企劃規劃正在加速特種化學品的應用。在成熟經濟體中,隨著新建設活動趨於平穩,資產翻新計畫將支撐市場需求。競爭環境有利於那些將配方技術與現場技術服務結合的供應商,他們可以幫助承包商滿足更嚴格的性能規格。

全球建築化學品市場趨勢與洞察

都市化主導的基礎建設熱潮推動了新興市場的需求。

亞太地區的永續城市建設計畫正推動大量使用外加劑、防水劑和養護劑,以提高擁擠工地上的耐久性。印度耗資1.4兆美元的國家基礎設施計畫也起到了類似的催化作用,其大規模高速公路和地鐵計劃指定使用低收縮混凝土外加劑,以確保樓板的連續性。聯合國人居住署預測,到2050年,城市居民將增加25億,這意味著與交通、公共產業和高層住宅相關的化學物質具有長期成長潛力。建築商也依賴快速凝固水泥漿來滿足大型企劃的工期要求。綜上所述,這些因素表明,建設化學品市場具有超越短期波動的內在結構性需求。

綠建築標準推動外加劑需求

能源性能指令迫使設計師設定碳排放限制,促使混凝土生產商採用高性能減水劑和水泥添加劑。歐盟根據《建築能源性能指令》規定,所有新建建築必須在2030年前淨零排放。美國LEED v4.1和BREEAM標準同樣評估低VOC密封劑和生物基塗料,從而推動了大豆多元醇基聚氨酯防水膜的高階細分市場發展。諸如EPA Safer Choice等產品註冊計畫進一步引導建築商選擇水性系統。在監管截止日期前改善產品的供應商能夠增強市場信心,並在建設化學品市場中提升定價權。

石化產品價格波動

原油及其衍生原料價格的波動擠壓了供應商的利潤空間,並使承包商的預算編制變得更加複雜。 2024年全年,布蘭特原油價格在每桶70至90美元之間波動,丙烯和環氧樹脂的價格也隨之波動。製造商採取的應對措施包括自行承擔成本上漲或加收附加費,這在某些情況下導致高價值產品無法按時交付現場。不斷上升的地緣政治風險進一步擾亂了供應鏈,促使配方商轉向生物基多元醇和再生聚合物。因此,在原料價格趨勢穩定之前,短期內的不確定性預計將限制建設化學品市場的預期成長率。

細分市場分析

到2025年,防水解決方案將佔據建設化學品市場35.10%的佔有率,凸顯了其在保護混凝土和磚石結構免受潮氣侵蝕方面的核心作用。這個細分市場受益於更嚴格的建築規範,這些規範強制要求對地下室進行全面防水,採用綠色屋頂膜,並在蓄水結構中使用負壓側塗層。易受洪水侵襲地區的基建機構需要能夠填充寬達2毫米裂縫的彈性體片材,儘管大宗聚合物價格波動,但其價格仍居高不下。製造商透過在聚合物鏈中加入奈米黏土阻隔層來打造差異化品牌,從而將透水性降低40%。

表面處理化學品領域成長最快,複合年成長率達6.65%,這主要得益於市場對採用機器人養護劑以提高批次均勻性的自動化預製構件廠的需求不斷成長。此外,用於減少物流倉庫粉塵產生的矽酸鋰硬化劑的需求也在增加。外加劑產品組合持續發展,其中聚羧酸醚類高效減水劑可在24小時內達到25 MPa的強度,從而實現模板的重複使用,這對於模組化建築至關重要。

建築化學品報告按產品類型(黏合劑、錨固劑和水泥漿、混凝土外加劑、混凝土保護塗料、地板樹脂、修補和修復化學品、密封劑等)、最終用途(商業、工業和公共、基礎設施、住宅)和地區(亞太地區、北美、歐洲、南美、中東和非洲)進行細分。

區域分析

至2025年,亞太地區將佔建築化學品市場41.10%的佔有率,並在2031年之前保持6.12%的最高複合年成長率。在中國,「一帶一路」計劃和沿海港口維修計畫正在推動市場需求,其中低氯化物外加劑在海洋環境中尤其重要。印度的智慧城市計畫正在推動100多個城市採購屋頂防水材料和路面密封劑。同時,東南亞工業園區的建設正在加速,帶動了對耐二氧化碳塗料的需求。注重價格的建築商傾向於選擇本地配方,但也會就複雜的橋面工程諮詢跨國供應商,從而達成合作生產協議,進一步擴大區域市場滲透率。

北美地區公共部門現代化進程持續推動穩定的收入成長。 5500億美元的聯邦基礎設施法案將用於15,000英里車道的道路翻新,這需要使用纖維增強型修補砂漿。諸如《國際住宅規範》之類的建築規範要求在地下室安裝防潮層,從而促進了零售防水卷材的銷售。因此,美國和加拿大的成長抵消了私人商業建築開工量的周期性放緩,使建設化學品市場保持了穩健的成長動能。

歐洲正經歷一場日趨成熟又充滿創新的變革。歐洲綠色交易的碳中和目標要求使用低水泥熟料水泥,這推動了對高性能減水劑和無碳矽烷密封劑的需求。德國和義大利老舊橋樑的出現促使陰極防蝕水泥漿的應用,而斯堪地那維亞則正在開發用於地下隔熱材料的生物基聚氨酯泡棉。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 都市化推動基礎建設蓬勃發展

- 綠建築標準推動外加劑需求

- 政府針對建設業的新冠疫情後經濟措施

- 老舊資產導致維修和維修支出增加

- 3D列印混凝土的廣泛應用需要一種特殊的配比。

- 市場限制

- 石化產品價格波動

- 加強溶劑型產品中揮發性有機化合物(VOCs)的監管

- 高級外加劑配比技能差距

- 價值鏈分析

- 法律規範

- 波特五力模型

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

- 價格趨勢分析(選定原料)

第5章 市場規模與成長預測

- 依產品

- 黏合劑

- 熱熔膠

- 反應性

- 溶劑型

- 水系統

- 錨栓和水泥漿

- 水泥基

- 樹脂

- 混凝土外加劑

- 加速器

- 空氣夾帶

- 高效減水劑(超塑劑)

- 萊特德

- 收縮率降低

- 黏度調節劑

- 減水劑(塑化劑)

- 其他類型

- 混凝土保護塗層

- 丙烯酸纖維

- 醇酸樹脂

- 環氧樹脂

- 聚氨酯

- 其他樹脂

- 地板樹脂

- 丙烯酸纖維

- 環氧樹脂

- 聚天門冬胺酸

- 聚氨酯

- 其他樹脂

- 修復和修復化學品

- 纖維纏繞系統

- 水泥漿

- 微型混凝土砂漿

- 改質砂漿

- 鋼筋保護罩

- 密封劑

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 表面處理化學品

- 硬化劑

- 釋放劑

- 其他類型

- 防水解決方案

- 化學品

- 電影

- 黏合劑

- 按最終用途

- 商業的

- 工業和公共設施

- 基礎設施

- 住宅

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 印尼

- 馬來西亞

- 泰國

- 越南

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲地區

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- 3M

- Akzo Nobel NV

- Ardex Group

- Arkema

- Asian Paints

- Beijing Oriental Yuhong Waterproof Technology Co., Ltd.

- CEMEX SAB de CV

- Dow

- HB Fuller Company

- Henkel AG and Co. KGaA

- Jiangsu Subote New Material Co., Ltd.

- KCC Corporation

- LATICRETE International, Inc.

- MAPEI SpA

- MC-Bauchemie

- Pidilite Industries Ltd.

- PPG Industries Inc.

- RPM International Inc.

- Saint-Gobain

- Sika AG

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

Construction Chemicals Market size in 2026 is estimated at USD 90.65 billion, growing from 2025 value of USD 85.92 billion with 2031 projections showing USD 118.53 billion, growing at 5.5% CAGR over 2026-2031.

Robust urban infrastructure pipelines, tighter green-building mandates, and steady residential demand together strengthen the construction chemicals market growth outlook. Waterproofing systems anchor product revenues because insurers and code officials prioritize moisture protection, while advanced surface treatments gain traction in automated precast yards. Regional momentum remains centered in Asia-Pacific, where megaproject pipelines accelerate specialty chemical adoption. Across mature economies, asset rehabilitation programs sustain volume when new-build activity plateaus. Competitive dynamics favor suppliers that marry formulation science with on-site technical service, helping contractors meet stricter performance specifications.

Global Construction Chemicals Market Trends and Insights

Urbanization-Led Infrastructure Boom Drives Emerging-Market Demand

Sustained city building programs in Asia-Pacific drive bulk consumption of admixtures, waterproofers, and curing compounds that improve durability in congested job sites. India's USD 1.4 trillion National Infrastructure Pipeline offers a similar catalyst, with large highway and metro packages specifying low-shrinkage concrete admixtures for slab continuity. UN-Habitat forecasts 2.5 billion additional urban residents by 2050, implying a long runway for chemical demand tied to transit, utilities, and high-rise housing. Contractors also lean on fast-setting grouts to keep megaproject schedules on track. Taken together, these factors embed a structural pull for the construction chemicals market that transcends short-cycle fluctuations.

Green-building Codes Boost Admixture Demand

Energy-performance directives now force designers to cap embodied carbon, pushing concrete producers to adopt high-range water reducers and supplementary cementitious materials. The European Union requires all new buildings to achieve net-zero emissions by 2030 under the Energy Performance of Buildings Directive. U.S. LEED v4.1 and BREEAM standards likewise reward low-VOC sealants and bio-based coatings, stimulating premium niches for soy-polyol polyurethane membranes. Product registries such as EPA Safer Choice further influence contractor specifications toward water-borne systems. Suppliers that reformulate ahead of code deadlines capture specification loyalty and reinforce pricing power within the construction chemicals market.

Petro-chemical Price Volatility

Fluctuating oil and derivative feedstock prices compress supplier margins and complicate contractor budgeting. Brent crude traded between USD 70 and USD 90 per barrel throughout 2024, pulling propylene and epoxy resin prices along the same path. Manufacturers absorb cost spikes or issue surcharges that sometimes delay jobsite adoption of premium products. Heightened geopolitical risks further disrupt supply chains, prompting formulators to diversify into bio-based polyols or recycled polymers. Short-term uncertainty therefore trims the forecast growth slope of the construction chemicals market until feedstock trends stabilize.

Other drivers and restraints analyzed in the detailed report include:

- Government Post-COVID Stimulus for Construction

- Aging Assets Spur Repair and Rehabilitation Spend

- Stricter VOC Limits on Solvent-borne Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Waterproofing solutions captured 35.10% of construction chemicals market share in 2025, illustrating their central role in safeguarding concrete and masonry against moisture intrusion. The sub-segment benefits from stricter building codes that specify full-basement tanking, green-roof membranes, and negative-side coatings on water-retaining structures. Infrastructure agencies in flood-prone regions demand elastomeric sheets that can bridge 2 mm-wide cracks, supporting premium pricing even when commodity polymers fluctuate. Manufacturers integrate nanoclay barriers into polymer chains to cut permeance by 40%, strengthening brand differentiation.

The fastest-growing surface-treatment chemicals segment posts a 6.65% CAGR, fueled by automated precast factories that apply curing compounds by robot to enhance batch consistency. Demand also rises for lithium-silicate hardeners that cut dusting in logistics warehouses. Admixture portfolios continue to evolve with polycarboxylate ether superplasticizers that deliver 25 MPa in 24 hours, enabling form-reuse cycles critical to modular construction.

The Construction Chemicals Report is Segmented by Product (Adhesives, Anchors and Grouts, Concrete Admixtures, Concrete Protective Coatings, Flooring Resins, Repair and Rehabilitation Chemicals, Sealants, and More), End-Use Sector (Commercial, Industrial and Institutional, Infrastructure, and Residential), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific held 41.10% construction chemicals market share in 2025 and maintains the highest 6.12% CAGR through 2031. China anchors demand with Belt and Road rail lines and coastal port upgrades that specify low-chloride admixtures for marine exposure. India's Smart Cities Mission triggers rooftop waterproofing and paving sealant purchases across 100 municipalities, while Southeast Asia accelerates industrial park builds that require anti-carbonation coatings. Price-sensitive contractors favor locally blended formulations yet consult multinational suppliers for complex bridge decks, enabling cooperative production agreements that deepen regional penetration.

North America contributes steady revenue on the back of public-sector modernization. The USD 550 billion federal infrastructure act channels funds into 15,000 highway-lane-mile resurfacing projects that need fiber-modified patching mortars. Building codes such as the International Residential Code mandate dampproof courses in basements, supporting retail membrane sales. Growth in the United States and Canada therefore offsets cyclic softness in private commercial starts, keeping the construction chemicals market on a positive slope.

Europe shows mature yet innovation-driven behavior. Carbon-neutrality goals in the European Green Deal demand clinker-reduced cements, advancing demand for high-range water reducers and silane sealers that restrict carbonation. Aging bridge stock in Germany and Italy spurs cathodic-protection grout usage, while Scandinavia pioneers bio-based polyurethane foams for below-grade insulation.

- 3M

- Akzo Nobel N.V.

- Ardex Group

- Arkema

- Asian Paints

- Beijing Oriental Yuhong Waterproof Technology Co., Ltd.

- CEMEX S.A.B. de C.V.

- Dow

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Jiangsu Subote New Material Co., Ltd.

- KCC Corporation

- LATICRETE International, Inc.

- MAPEI S.p.A.

- MC-Bauchemie

- Pidilite Industries Ltd.

- PPG Industries Inc.

- RPM International Inc.

- Saint-Gobain

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urbanization-led infrastructure boom

- 4.2.2 Green-building codes boost admixture demand

- 4.2.3 Government post-COVID stimulus for construction

- 4.2.4 Aging assets spur repair and rehabilitation spend

- 4.2.5 3D-printed concrete adoption needs specialty mixes

- 4.3 Market Restraints

- 4.3.1 Petro-chemical price volatility

- 4.3.2 Stricter VOC limits on solvent-borne products

- 4.3.3 Skill gap in dosing advanced admixtures

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Pricing Trend Analysis (Selected Raw Materials)

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Adhesives

- 5.1.1.1 Hot-melt

- 5.1.1.2 Reactive

- 5.1.1.3 Solvent-borne

- 5.1.1.4 Water-borne

- 5.1.2 Anchors and Grouts

- 5.1.2.1 Cementitious

- 5.1.2.2 Resin

- 5.1.3 Concrete Admixtures

- 5.1.3.1 Accelerator

- 5.1.3.2 Air-entraining

- 5.1.3.3 High Range Water Reducer (Super Plasticizer)

- 5.1.3.4 Retarder

- 5.1.3.5 Shrinkage-reducing

- 5.1.3.6 Viscosity Modifier

- 5.1.3.7 Water Reducer (Plasticizer)

- 5.1.3.8 Other Types

- 5.1.4 Concrete Protective Coatings

- 5.1.4.1 Acrylic

- 5.1.4.2 Alkyd

- 5.1.4.3 Epoxy

- 5.1.4.4 Polyurethane

- 5.1.4.5 Other Resins

- 5.1.5 Flooring Resins

- 5.1.5.1 Acrylic

- 5.1.5.2 Epoxy

- 5.1.5.3 Polyaspartic

- 5.1.5.4 Polyurethane

- 5.1.5.5 Other Resins

- 5.1.6 Repair and Rehabilitation Chemicals

- 5.1.6.1 Fiber-wrapping systems

- 5.1.6.2 Injection grouts

- 5.1.6.3 Micro-concrete mortars

- 5.1.6.4 Modified mortars

- 5.1.6.5 Rebar protectors

- 5.1.7 Sealants

- 5.1.7.1 Acrylic

- 5.1.7.2 Epoxy

- 5.1.7.3 Polyurethane

- 5.1.7.4 Silicone

- 5.1.7.5 Other Resins

- 5.1.8 Surface-treatment Chemicals

- 5.1.8.1 Curing compounds

- 5.1.8.2 Mold-release agents

- 5.1.8.3 Other Types

- 5.1.9 Waterproofing Solutions

- 5.1.9.1 Chemicals

- 5.1.9.2 Membranes

- 5.1.1 Adhesives

- 5.2 By End-Use Sector

- 5.2.1 Commercial

- 5.2.2 Industrial and Institutional

- 5.2.3 Infrastructure

- 5.2.4 Residential

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Indonesia

- 5.3.1.7 Malaysia

- 5.3.1.8 Thailand

- 5.3.1.9 Vietnam

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 Spain

- 5.3.3.5 United Kingdom

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Ardex Group

- 6.4.4 Arkema

- 6.4.5 Asian Paints

- 6.4.6 Beijing Oriental Yuhong Waterproof Technology Co., Ltd.

- 6.4.7 CEMEX S.A.B. de C.V.

- 6.4.8 Dow

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG and Co. KGaA

- 6.4.11 Jiangsu Subote New Material Co., Ltd.

- 6.4.12 KCC Corporation

- 6.4.13 LATICRETE International, Inc.

- 6.4.14 MAPEI S.p.A.

- 6.4.15 MC-Bauchemie

- 6.4.16 Pidilite Industries Ltd.

- 6.4.17 PPG Industries Inc.

- 6.4.18 RPM International Inc.

- 6.4.19 Saint-Gobain

- 6.4.20 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

印度建設化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)東南亞建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

印度建設化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)東南亞建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 建築化學品市場預測至2034年-按產品類型、化學品類型、應用、最終用途和地區分類的全球分析

建築化學品市場預測至2034年-按產品類型、化學品類型、應用、最終用途和地區分類的全球分析 建築化學品市場規模、佔有率和成長分析:黏合劑和密封劑、混凝土外加劑、砂漿和水泥漿、防水化學品、修補和保護劑以及地區分類-2026-2033年產業預測越南建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

建築化學品市場規模、佔有率和成長分析:黏合劑和密封劑、混凝土外加劑、砂漿和水泥漿、防水化學品、修補和保護劑以及地區分類-2026-2033年產業預測越南建築化學品市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 建築化學品市場:2026-2032年全球市場預測(依產品類型、技術、劑型、建築類型、應用、最終用戶和通路分類)固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年

建築化學品市場:2026-2032年全球市場預測(依產品類型、技術、劑型、建築類型、應用、最終用戶和通路分類)固定式機械錨栓市場:依產品類型、材料、應用、終端用戶產業及通路分類,全球預測,2026-2032年 建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

建築化學品市場分析及預測(至2035年):類型、產品、應用、形態、材質類型、技術、最終用戶、功能、安裝類型、解決方案歐洲建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國建設化學品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)