|

市場調查報告書

商品編碼

2073485

船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

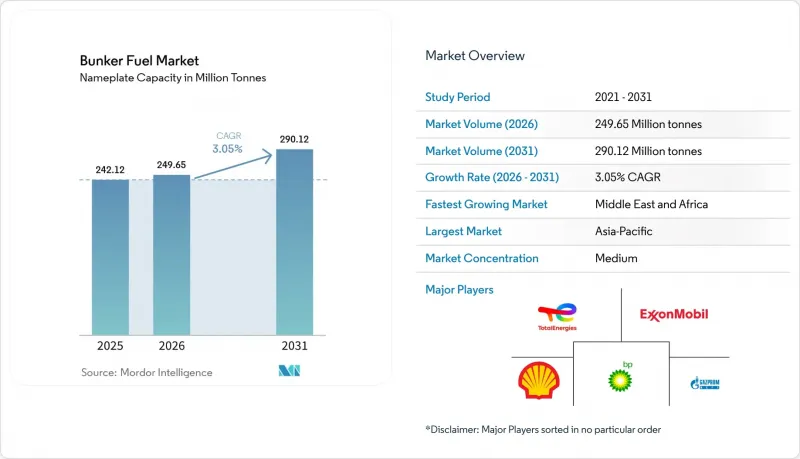

根據 Mordor Intelligence 的數據,2025 年額定產能的船用燃料市場規模估計為 2.4212 億噸,預計到 2031 年將從 2026 年的 2.4965 億噸成長至 2.9012 億噸,在預測期(2026-2031 年)成長 2.95% 的複合年成長率。

本報告依燃料種類(高硫燃料油、超低硫燃料油、超低硫燃料油、船用輕柴油、液化天然氣、甲醇、生物/合成燃料、氨、其他)、燃料庫方式(船對船、港對船、液化天然氣駁船對船、可攜式油罐和貨櫃)、船舶類型(貨櫃船、油輪、散裝貨船、雜貨船、客船/滾裝船、海上特種船舶)和地區(北美、歐洲、亞太、南美、其他)進行分類。

全球船用燃料市場趨勢及洞察

實施 IMO 2020 和擴大排放控制區 (ECA)。

自2020年實施以來,嚴格的硫含量法規持續迫使船東轉向使用合規燃料。預計到2025年,因硫含量不達標而被鹿特丹和新加坡扣留的船舶數量將會增加,這將迫使供應商在裝貨點實施即時檢測系統。歐盟海事燃料標準(FuelEU Maritime)除了硫含量法規外,還設定了碳排放強度目標,因此,營運商目前採用多種燃料組合:短程航線使用超低硫燃料油(VLSFO),新船使用液化天然氣(LNG),而現有船舶則二手生質燃料燃料混合燃料。根據船級社統計,截至2024年,共有638艘LNG動力船舶投入運營,累積訂單到2028年,這一數字將達到1200艘。這表明,合規措施已從簡單的燃料轉換轉向船隊的現代化改造。隨著地中海和東南亞部分地區排放控制區(ECA)的擴大,除配備脫硫裝置的船隊外,高硫燃料的合理性正在下降。雖然更嚴格的法規透過對低硫燃料的可預測需求支撐了船用燃料市場,但更嚴格的碳排放法規正在加速向甲醇和氨的多元化發展。

液化天然氣動力運輸船的訂單激增。

2024年,約70%的替代燃料船舶合約為液化天然氣(LNG)動力。這反映了LNG引擎久經考驗的可靠性,以及與超低硫燃油(VLSFO)相比,LNG動力船舶從船體到船尾的二氧化碳排放可減少高達25%的事實。現代重工和中國船舶重工集團已共同訂單超過100艘LNG相容型貨櫃船和散裝貨船,預計於2026年至2029年間交付。歐洲渡輪營運商正在推進滾裝客船向LNG動力船舶的維修,理由是低排放船舶可享有優惠待遇,例如挪威和德國的錨碇折扣。郵輪也呈現類似的趨勢,嘉年華郵輪公司訂購的LNG動力船舶正是為了滿足乘客對更環保航線的需求。目前,LNG引擎的交付週期已延長至18個月,船東們甚至在最終船體合約簽訂前就已鎖定生產檔期。儘管甲烷洩漏問題引發了爭議,但這些跡象表明,人們對LNG仍抱持著很高的信心。

加強生命週期溫室氣體排放法規,超越二氧化碳排放範疇

全球法規正從關注廢氣碳排放轉向關注生命週期指標,這些指標也涵蓋甲烷洩漏和上游排放。國際海事組織(IMO)計劃於2026年發布的指導方針草案將要求船東揭露甲烷洩漏係數。如果引擎並非高壓系統,該係數可能會抵消液化天然氣(LNG)在表面排放方面的優勢。加州計畫修訂的低碳燃料標準(LCFS)中也包含類似的處罰措施,這將給老舊的雙燃料引擎帶來成本壓力。研究估計,甲烷洩漏率在0.2%至3.5%之間,取決於引擎負荷。鑑於甲烷的全球暖化潛勢高達28,這可能會對燃料經濟性產生重大影響。新加坡和富查伊拉的脫硫裝置排放禁令也為重質燃油(HSFO)用戶帶來了相應的合規負擔。這些因素綜合起來將限制LNG價格進一步上漲的潛力,除非硬體和法規方面取得快速發展,否則船用燃料市場的複合年成長率(CAGR)將會放緩。

細分市場分析

即使到了2025年,超低硫燃料油(VLSFO)仍將佔全球總量的52.4%,這將支撐船用燃料市場達到一個規模相當的水平,即單一等級的燃料無需進行重大硬體改造即可滿足多種監管要求。預計這種燃料的主導地位只會逐步下降,因為許多船東透過長期合約對沖價格風險,且其受短期價差的影響有限。液化天然氣(LNG)預計31.6%的複合年成長率代表了第二個成長軸,其成長動力來自對低溫儲存、雙燃料引擎及相關供應鏈的投資。高硫燃料油(HSFO)仍然是配備脫硫裝置的船舶的可行選擇,但煉油廠設備的升級正在減少殘油產量,縮小了原本足以支撐脫硫裝置安裝成本的價格差異。

甲醇和氨正從試點階段邁向商業化初期,領先的船隊紛紛鎖定綠色通道航線和補貼加註位。生質燃料和電子燃料以5%至20%的比例混合,使船東能夠在不更換引擎的情況下降低船舶全生命週期的碳排放強度,從而在進行大規模技術轉型的同時滿足短期需求。因此,船用燃料市場呈現兩極化。現有船隊正在最大限度地利用超低硫燃料油(VLSFO)的經濟效益,而具有戰略意義的新船則著眼於未來,選擇液化天然氣(LNG)和甲醇作為燃料,以應對碳排放稅的實施。

區域分析

到2025年,亞太地區將佔全球總吞吐量的44.7%,這主要得益於新加坡5,060萬噸的吞吐量以及中國港口停靠量的激增。韓國和日本擴大了液化天然氣(LNG)供應,用於沿海渡輪和跨太平洋貨櫃航線;印尼和越南則投資於卡車運輸的超低硫燃料油(VLSFO)配送,以支持沿海製造業。印度國內航運限制的部分放寬促使孟買和清奈的船用燃料裝載量增加,但低硫燃料儲存能力有限,阻礙了成長。

預計中東和非洲地區將以3.5%的複合年成長率超越其他所有地區,這主要得益於富查伊拉630萬噸的銷量以及沙烏地阿美在紅海門戶的液化天然氣投資。阿布達比國家石油公司(ADNOC)和道達爾能源公司將於2026年初新增1.8萬立方公尺的浮體式液化天然氣倉儲設施,將使沿岸地區能夠掌控亞歐之間的物流運輸。儘管繞行造成了一些干擾,但埃及預計到2024年仍有2.06萬艘船舶使用蘇伊士運河,埃及正尋求透過在塞得港和蘇伊士建設液化天然氣供應基地來複製這一模式。

在歐洲,波羅的海、北海和英吉利海峽仍實施嚴格的排放控制區 (ECA) 法規。鹿特丹港擁有 920 萬噸的吞吐能力和擴建後的碼頭,使其成為超低硫重燃料油 (VLSFO) 和液化天然氣 (LNG) 的區域樞紐。根據「歐盟海事燃料計畫」(FuelEU Maritime),從 2025 年起將徵收碳強度課稅,強制船東混合生質燃料或確保甲醇裝載,以避免每噸二氧化碳當量 2400 歐元的罰款。在北美,「瓊斯法案」的法規阻礙了船對船 (S/S) 液化天然氣供應,而南美港口缺乏低溫倉儲設施意味著該地區的船用燃料市場仍然依賴傳統燃料。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 實施IMO 2020及擴大出口管制區

- 液化天然氣動力運輸船的訂單激增。

- 亞太地區海上貿易量激增。

- 脫硫裝置的改造正在支撐對重質燃油(HSFO)的需求。

- 綠色走廊計畫將加速船舶使用氨和甲醇進行燃料補給。

- 利用人工智慧技術最佳化燃料路線,減少浪費。

- 市場限制因素

- 加強對二氧化碳以外的生命週期溫室氣體的監管

- 原油價差的波動正在擾亂超低硫燃料油(VLSFO)的價格形成。

- 全球液化天然氣燃料庫基礎設施不足

- 由於煉油廠收率變化,殘餘燃料供應減少。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 投資分析

第5章 市場規模與成長預測

- 按燃料類型

- 高硫燃料油(HSFO)

- 超低硫燃料油(VLSFO)

- 超低硫燃料油(ULSFO)

- 船用柴油燃料(MGO)

- 液化天然氣(LNG)

- 甲醇

- 生物/合成燃料

- 氨

- 其他

- 燃料庫方法

- 船對船

- 港口到船舶(卡車/管道)

- 液化天然氣駁船到船舶

- 可攜式儲罐和容器

- 按船舶類型

- 貨櫃船

- 油船

- 散貨船

- 普通貨船

- 客運/滾裝船

- 海上特種船舶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 西班牙

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 新加坡

- 印尼

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 南非

- 奈及利亞

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Exxon Mobil

- Shell plc

- BP plc

- TotalEnergies SE

- Chevron Corp.

- Gazpromneft Marine Bunker

- Lukoil

- Minerva Bunkering

- Peninsula Petroleum

- World Fuel Services

- Bomin Bunker Holding

- GAC Bunker Fuels

- AP Moller-Maersk

- Mediterranean Shipping Co.

- CMA CGM

- COSCO Shipping

- Hapag-Lloyd

- Evergreen Marine

- ONE(Ocean Network Express)

- Yang Ming

- HMM Co.

- Pacific International Lines

第7章 市場機會與未來展望

According to Mordor Intelligence, the bunker fuel market size in terms of nameplate capacity was valued at 242.12 million tonnes in 2025 and is estimated to grow from 249.65 million tonnes in 2026 to reach 290.12 million tonnes by 2031, at a CAGR of 3.05% during the forecast period (2026-2031).

This report is Segmented by Fuel Type (HSFO, VLSFO, ULSFO, MGO, LNG, Methanol, Bio-/Synthetic Fuels, Ammonia, and More), Bunkering Method (Ship-To-Ship, Port-To-Ship, LNG Barge-To-Ship, and Portable Tanks and Containers), Vessel Type (Container, Tanker, Bulk Carrier, General Cargo, Passenger/Ro-Pax, and Offshore and Specialized), and Geography (North America, Europe, Asia-Pacific, South America, and More).

Global Bunker Fuel Market Trends and Insights

IMO 2020 Enforcement & ECA Expansion

Strict sulfur caps that began in 2020 continue to steer fleet owners toward compliant fuels. Detentions for non-compliant sulfur levels rose in Rotterdam and Singapore during 2025, pushing suppliers to install real-time testing at loading points. FuelEU Maritime layers carbon-intensity targets on top of sulfur limits, so operators now juggle VLSFO for short runs, LNG for new-builds, and bio-fuel blends for mid-life tonnage. Classification societies recorded 638 LNG-powered vessels on the water in 2024, with the orderbook pointing to 1,200 units by 2028, confirming that compliance has shifted from simple fuel switching to fleet renewal. ECAs in the Mediterranean and parts of Southeast Asia are widening, which narrows the economic case for high-sulfur grades outside scrubber-equipped fleets. As enforcement tightens, predictable demand for low-sulfur options anchors the bunker fuel market, yet the added carbon layer accelerates diversification toward methanol and ammonia.

Rapid Growth in LNG-Fuelled Fleet Orders

LNG secured around 70% of alternative-fuel vessel contracts placed during 2024, reflecting proven engine reliability and up to 25% lower well-to-wake CO2 emissions versus VLSFO. Hyundai Heavy Industries and China State Shipbuilding Corporation together hold more than 100 LNG-ready container and bulk carrier orders that will deliver between 2026 and 2029. European ferry operators are retrofitting Ro-Pax units to LNG, supported by discounted berthing fees in Norway and Germany that reward lower-emission vessels. Cruise lines mirror the trend; Carnival Corporation's LNG ship orders align with passenger demand for greener itineraries. Engine lead times now stretch to 18 months, prompting owners to secure manufacturing slots ahead of final hull contracts, signaling confidence in LNG despite emerging debate over methane slip.

Tightening Lifecycle-GHG Regulations Beyond CO2

Global rules are shifting from tailpipe carbon to full lifecycle metrics that capture methane slip and upstream emissions. IMO draft guidelines due in 2026 will force owners to disclose methane leakage factors that can neutralize LNG's headline emissions advantage if engines are not high-pressure systems. California's planned Low Carbon Fuel Standard revisions outline similar penalties, putting older dual-fuel engines under cost pressure. Studies peg methane slip between 0.2% and 3.5% depending on engine load, and given methane's 28X global-warming potential, this can materially shift fuel economics. Scrubber discharge bans in Singapore and Fujairah add parallel compliance burdens for HSFO users. The combined effect restrains LNG upside and crimps the bunker fuel market CAGR absent rapid hardware and regulatory evolution.

Other drivers and restraints analyzed in the detailed report include:

- Surging APAC Seaborne Trade Volumes

- Green-Corridor Initiatives Accelerating Ammonia & Methanol Bunkering

- Limited Global LNG Bunkering Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

VLSFO retained 52.4% of global volume in 2025, anchoring the bunker fuel market size at a point where one grade still meets broad compliance without major hardware changes. The fuel's dominance is expected to erode only gradually because many owners hedge price risk through term contracts, limiting exposure to short-term spreads. LNG's 31.6% forecast CAGR signals a second axis of growth that pulls investment into cryogenic storage, dual-fuel engines, and related supply chains. High-Sulfur Fuel Oil (HSFO) remains viable for scrubber-equipped tonnage, but refinery upgrades are shrinking residual output, squeezing discounts that justified scrubber spend.

Methanol and ammonia are moving from pilot to early commercialization as first-mover fleets secure green-corridor routes and subsidized bunkering slots. Bio-fuels and e-fuels are being blended at 5-20% levels, enabling owners to cut lifecycle intensity without engine changes, which shores up short-run demand while larger technology transitions play out. The result is a bifurcated bunker fuel market: legacy fleets maximize VLSFO economics, while strategic new builds lock in LNG or methanol to future-proof against carbon levies.

Complete Report Scope:

- By Fuel Type

- High-Sulfur Fuel Oil (HSFO)

- Very-Low-Sulfur Fuel Oil (VLSFO)

- Ultra-Low-Sulfur Fuel Oil (ULSFO)

- Marine Gas Oil (MGO)

- Liquefied Natural Gas (LNG)

- Methanol

- Bio-/Synthetic Fuels

- Ammonia

- Other Fuel Types

- By Bunkering Method

- Ship-to-Ship

- Port-to-Ship (Truck/Pipeline)

- LNG Barge-to-Ship

- Portable Tanks and Containers

- By Vessel Type

- Container

- Tanker

- Bulk Carrier

- General Cargo

- Passenger/Ro-Pax

- Offshore and Specialized

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Spain

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Indonesia

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific held 44.7% of volume in 2025, reflecting Singapore's 50.6 million-tonne throughput and China's surging port calls. South Korea and Japan expanded LNG offerings for short-sea ferries and trans-Pacific container loops, while Indonesia and Vietnam invested in truck-based VLSFO delivery to back near-shore manufacturing. India's partial cabotage liberalization boosted bunker uplift at Mumbai and Chennai, yet limited low-sulfur storage caps growth.

The Middle East and Africa region is projected to outpace all others at a 3.5% CAGR, anchored by Fujairah's 6.3 million-tonne sales and Saudi Aramco's LNG investments at Red Sea gateways. ADNOC and TotalEnergies added 18,000 m3 of floating LNG storage in early 2026, positioning the Gulf to intercept Asia-Europe flows. Egypt seeks to replicate the model by studying LNG supply points at Port Said and Suez, as 20,600 vessels still used the canal in 2024 despite diversion shocks.

Europe remains defined by strict ECA rules in the Baltic, North Sea, and English Channel. Rotterdam's 9.2 million-tonne throughput and expanded Gate terminal make it the regional hub for both VLSFO and LNG. FuelEU Maritime adds a carbon-intensity levy from 2025 onward, prompting owners to blend bio-fuels or book methanol slots to avoid EUR 2,400 penalties per tonne of CO2 equivalent. North America's Jones Act hurdles inhibit ship-to-ship LNG supply, while South American ports lack cryogenic storage, keeping the bunker fuel market there dependent on conventional grades.

- Exxon Mobil

- Shell plc

- BP plc

- TotalEnergies SE

- Chevron Corp.

- Gazpromneft Marine Bunker

- Lukoil

- Minerva Bunkering

- Peninsula Petroleum

- World Fuel Services

- Bomin Bunker Holding

- GAC Bunker Fuels

- AP Moller-Maersk

- Mediterranean Shipping Co.

- CMA CGM

- COSCO Shipping

- Hapag-Lloyd

- Evergreen Marine

- ONE (Ocean Network Express)

- Yang Ming

- HMM Co.

- Pacific International Lines

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IMO 2020 enforcement & ECA expansion

- 4.2.2 Rapid growth in LNG-fuelled fleet orders

- 4.2.3 Surging APAC seaborne trade volumes

- 4.2.4 Scrubber retrofits sustaining HSFO demand

- 4.2.5 Green-corridor initiatives accelerating ammonia & methanol bunkering

- 4.2.6 AI-driven fuel-route optimisation cutting wastage

- 4.3 Market Restraints

- 4.3.1 Tightening lifecycle-GHG regulations beyond CO2

- 4.3.2 Volatile crude spreads disrupting VLSFO pricing

- 4.3.3 Limited global LNG bunkering infrastructure

- 4.3.4 Refinery yield shift reducing residual fuel supply

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 High-Sulfur Fuel Oil (HSFO)

- 5.1.2 Very-Low-Sulfur Fuel Oil (VLSFO)

- 5.1.3 Ultra-Low-Sulfur Fuel Oil (ULSFO)

- 5.1.4 Marine Gas Oil (MGO)

- 5.1.5 Liquefied Natural Gas (LNG)

- 5.1.6 Methanol

- 5.1.7 Bio-/Synthetic Fuels

- 5.1.8 Ammonia

- 5.1.9 Other Fuel Types

- 5.2 By Bunkering Method

- 5.2.1 Ship-to-Ship

- 5.2.2 Port-to-Ship (Truck/Pipeline)

- 5.2.3 LNG Barge-to-Ship

- 5.2.4 Portable Tanks and Containers

- 5.3 By Vessel Type

- 5.3.1 Container

- 5.3.2 Tanker

- 5.3.3 Bulk Carrier

- 5.3.4 General Cargo

- 5.3.5 Passenger/Ro-Pax

- 5.3.6 Offshore and Specialized

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Spain

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Singapore

- 5.4.3.6 Indonesia

- 5.4.3.7 Australia

- 5.4.3.8 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Chile

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Exxon Mobil

- 6.4.2 Shell plc

- 6.4.3 BP plc

- 6.4.4 TotalEnergies SE

- 6.4.5 Chevron Corp.

- 6.4.6 Gazpromneft Marine Bunker

- 6.4.7 Lukoil

- 6.4.8 Minerva Bunkering

- 6.4.9 Peninsula Petroleum

- 6.4.10 World Fuel Services

- 6.4.11 Bomin Bunker Holding

- 6.4.12 GAC Bunker Fuels

- 6.4.13 AP Moller-Maersk

- 6.4.14 Mediterranean Shipping Co.

- 6.4.15 CMA CGM

- 6.4.16 COSCO Shipping

- 6.4.17 Hapag-Lloyd

- 6.4.18 Evergreen Marine

- 6.4.19 ONE (Ocean Network Express)

- 6.4.20 Yang Ming

- 6.4.21 HMM Co.

- 6.4.22 Pacific International Lines

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

南美洲船用燃料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)新加坡船用燃料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

南美洲船用燃料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)新加坡船用燃料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 船用燃料市場:依燃料類型、船舶類型、運作模式、船用引擎類型、最終用戶和通路分類-2026-2032年全球市場預測

船用燃料市場:依燃料類型、船舶類型、運作模式、船用引擎類型、最終用戶和通路分類-2026-2032年全球市場預測 船用燃料市場規模、佔有率和趨勢分析報告:按燃料類型、應用、地區和細分市場預測(2026-2033 年)

船用燃料市場規模、佔有率和趨勢分析報告:按燃料類型、應用、地區和細分市場預測(2026-2033 年) 全球船用燃料油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球船用燃料油市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 船用燃料市場規模、佔有率、趨勢及預測(按燃料類型、船舶類型、銷售商及地區分類),2026-2034年

船用燃料市場規模、佔有率、趨勢及預測(按燃料類型、船舶類型、銷售商及地區分類),2026-2034年 2026年全球船用燃料市場報告

2026年全球船用燃料市場報告 2026-2030年全球船用燃料油市場

2026-2030年全球船用燃料油市場 全球船用燃料市場-產業規模、佔有率、趨勢、機會和預測,按類型、商業分銷商、應用、地區和競爭格局分類,2021-2031年預測

全球船用燃料市場-產業規模、佔有率、趨勢、機會和預測,按類型、商業分銷商、應用、地區和競爭格局分類,2021-2031年預測