|

市場調查報告書

商品編碼

2072514

新加坡船用燃料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Singapore Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

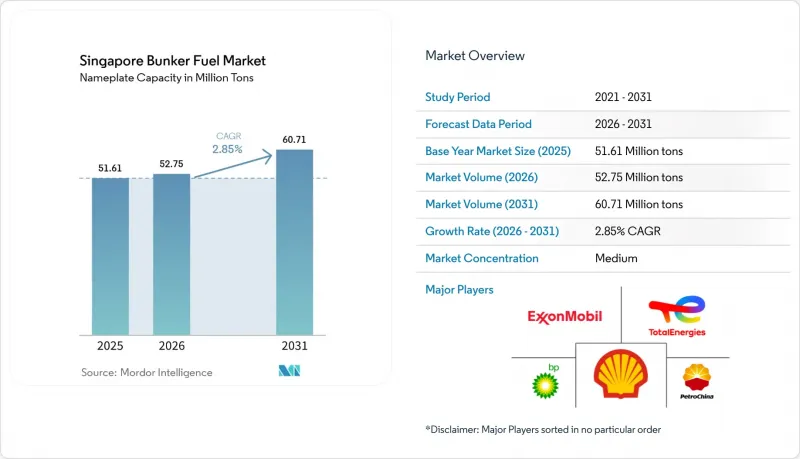

根據 Mordor Intelligence 預測,新加坡船用燃料市場規模(以額定容量計算)到 2025 年將達到 5,161 萬噸,到 2026 年將達到 5,275 萬噸,到 2031 年將達到 6,071 萬噸。

預計從 2026 年到 2031 年,其複合年成長率將達到 2.85%。

本報告按燃料類型(高硫燃料油、超低硫燃料油、超低硫燃料油、船用輕柴油、液化天然氣、甲醇、生物/合成燃料、氨等)、燃料庫方式(船對船、港對船、液化天然氣駁船對船、可攜式儲罐/貨櫃)和船舶類型(貨櫃船、油輪、散裝船駁船、貨船、船舶/船/特種船)。市場規模和預測以噸(MT)為單位。

新加坡船用燃料市場趨勢及洞察

遵守 IMO 2020 硫排放法規將提振對超低硫燃料油 (VLSFO) 的需求。

國際海事組織(IMO)於2020年1月實施的0.50%硫含量上限預計將使超低硫燃料油(VLSFO)的市佔率在2025年達到55.3%。同時,高硫燃料油(HSFO)與VLSFO之間的價格差在2024年下半年達到每噸150-180美元,提高了脫硫裝置的經濟效益,並帶動了HSFO需求的復甦。由於燃油密集型超大型油輪(VLCC)和好望角型散裝貨船安裝脫硫裝置的投資回收期已縮短至18個月以內,船東即使在運費持續波動的情況下也能進行改裝投資。供應商現在需要同時維持VLSFO和HSFO的庫存,導致其營運資金需求比2020年以前增加了約15-20%。國際海事組織(IMO)2023年溫室氣體策略要求在2030年將排放減少5%至10%,加速了人們對液化天然氣(LNG)和甲醇的興趣,並可能從2028年起削弱超低硫燃料油(VLSFO)的優勢。馬士基2023年在新加坡成功進行的船對船甲醇加註作業顯示了替代燃料的技術可行性,但甲醇的低能量密度意味著在負載容量方面需要做出妥協。

新加坡是世界最大的船舶加油中心。

該港口預計2024年將售出5,492萬噸燃料,約佔全球船用燃料需求的18%。全天候營運和50多家持證供應商支撐著該港口的競爭優勢。紅海航線的改道增加了經好望角的亞歐航線航程,航程延長了8,500海裡,導致燃料消耗量增加33%,進而使船用燃料供應量增加200萬至300萬噸。裕廊島土地資源稀缺,限制了其儲油能力的擴張,目前儲油量約2,050萬立方公尺。隨著空間限制的加劇,一些買家正轉向馬來西亞的巴生港和印尼的巴淡島。除非新加坡能夠保持在替代燃料領域的領先地位,否則到2030年,印度和越南區域煉油廠的擴張可能導致新加坡的市場佔有率下降5%至8%。綠色船舶計畫 2024 年的撥款(相當於 46 萬噸液化天然氣和 88 萬噸生質燃料)凸顯了向未來燃料的轉變,旨在鞏固其作為長期樞紐的重要性。

原油價格波動給交易商的利潤率帶來了壓力。

2024年,布蘭特原油價格在每桶70至90美元之間波動。由於供應商難以將成本波動轉嫁給船東,燃油貿易商的利潤率從2020-2022年通常的6-8%被壓縮至3-5%。馬士基2025年第一季的平均燃油成本為每噸569美元,年減9%,但價格傳導落後原油價格波動4-6週,凸顯了時間上的錯配。未與上游產業整合的獨立公司需要提前30-45天預付庫存資金,並面臨價格飆升的風險,可能導致季度利潤被吞噬。 2024年10月高硫燃油(HSFO)價格的飆升,使得HSFO與超低硫燃油(VLSFO)之間的價格差擴大至每噸150-180美元。這導致配備脫硫裝置的船舶靠港次數增加了15%,但供應商被迫將買賣價差擴大5-7%以控制風險。對於中小企業而言,由於追加保證金會佔用其有限的營運資金,避險交易仍受到限制。

細分市場分析

在新加坡船用燃料油市場,超低硫燃料油(VLSFO)的市場規模預計將在2025年達到2920萬噸,佔市場佔有率的55.3%,這主要得益於船舶遵守國際海事組織(IMO)2020年的硫排放規定。液化天然氣(LNG)的銷量雖然基數仍然較小,但預計到2031年將以28.9%的複合年成長率成長,這主要得益於2024年46萬噸的銷量以及更多LNG加註駁船的投入使用。重質燃料油(HSFO)的需求在2024年隨著與VLSFO價格差距的擴大而回升。配備脫硫裝置的船舶正在享受成本節約帶來的收益,投資回收期縮短至不到18個月。甲醇、生質燃料和氨的總合市佔率目前仍低於2%,但預計在2028年及以後將迎來轉機,這主要得益於監管政策的明確化以及試點計畫的基礎建設。

從長遠來看,隨著船東為應對即將到來的碳排放稅而著手保障船隊的未來,替代燃料預計將對超低硫燃料油(VLSFO)的優勢構成挑戰。因此,新加坡的船用燃料市場可能呈現兩極化的格局:傳統燃料的需求在2028年之前保持穩定,之後液化天然氣(LNG)、甲醇和先進生質燃料的採用速度將加快。儘管由於廢油衍生生質柴油燃料的原料限制以及氨燃料的安全隱患,供應仍將較為緊張,但那些及早進入這些細分市場的公司,在法規強制要求使用零碳燃料時,或許能夠獲得較高的利潤率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對超低硫燃料油的需求是由遵守國際海事組織 2020 年硫排放法規所驅動的。

- 新加坡是世界最大的燃料庫中心。

- 電子商務主導的貿易導致貨櫃處理量增加

- 政府對液化天然氣燃料庫基礎設施的支援措施

- 綠色船舶計畫下的新型生質燃料和電子燃料加註試點項目

- 一個降低交易成本的數位化燃料庫平台。

- 市場限制因素

- 原油價格波動給交易商的利潤率帶來了壓力。

- 利用氨和甲醇等替代能源實現脫碳轉型

- 土地短缺制約了倉儲設施的擴建

- 由於對質量流量計的監管更加嚴格,營運成本增加。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- PESTLE分析

第5章 市場規模與成長預測

- 按燃料類型

- 高硫燃料油(HSFO)

- 超低硫燃料油(VLSFO)

- 超低硫燃料油(ULSFO)

- 船用柴油燃料(MGO)

- 液化天然氣(LNG)

- 甲醇

- 生物/合成燃料

- 氨

- 其他

- 燃料庫方法

- 船對船

- 港口到船舶(卡車/管道)

- 液化天然氣駁船到船舶

- 可攜式儲罐和容器

- 按船舶類型

- 貨櫃船

- 油船

- 散貨船

- 普通貨船

- 客船/滾裝船

- 海上及特種船舶

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- PetroChina International(Singapore)

- Sentek Marine & Trading

- Ocean Bunkering Services

- Equatorial Marine Fuel

- Shell Eastern Trading

- TotalEnergies Marine Fuels

- ExxonMobil Asia Pacific

- BP Singapore

- Chevron Singapore

- Glencore Singapore

- Trafigura-TFG Marine

- Minerva Bunkering

- Vitol Bunkers

- Bunker One(Singapore)

- Pavilion Energy

- CMA CGM Fuel Singapore

- Maersk Oil Trading Singapore

- Hafnia Bunkers

- Mitsui & Co. Energy Trading

- Itochu Petroleum Singapore

- Sinanju-Consort Bunkers

第7章 市場機會與未來展望

According to Mordor Intelligence, the singapore bunker fuel market size in terms of nameplate capacity is projected to be 51.61 million tons in 2025, 52.75 million tonnes in 2026, and reach 60.71 million tonnes by 2031, growing at a CAGR of 2.85% from 2026 to 2031.

This report is Segmented by Fuel Type (HSFO, VLSFO, ULSFO, MGO, LNG, Methanol, Bio-/Synthetic Fuels, Ammonia, and More), Bunkering Method (Ship-To-Ship, Port-To-Ship, LNG Barge-To-Ship, and Portable Tanks and Containers), and Vessel Type (Container, Tanker, Bulk Carrier, General Cargo, Passenger/Ro-Pax, and Offshore and Specialized). The Market Sizes and Forecasts are Provided in Terms of Volume (MT).

Singapore Bunker Fuel Market Trends and Insights

IMO 2020 Sulfur-Cap Compliance Boosting VLSFO Demand

The IMO's 0.50% sulfur ceiling, active since January 2020, pushed VLSFO to a 55.3% share in 2025 and simultaneously triggered an HSFO rebound as scrubber economics improved when the HSFO-VLSFO spread touched USD 150-180 per ton in late 2024. Scrubber payback periods fell below 18 months for fuel-intensive VLCCs and capesize bulkers, motivating owners to fund retrofits even amid freight-rate volatility. Suppliers must now carry parallel VLSFO and HSFO inventories, inflating working-capital needs by roughly 15-20% compared with pre-2020 practice. The IMO's 2023 GHG strategy requiring 5-10% emission cuts by 2030 accelerates interest in LNG and methanol, likely tapering VLSFO's dominance beyond 2028. Maersk's successful 2023 ship-to-ship methanol bunkering in Singapore shows the technical feasibility of alternatives, yet methanol's lower energy density forces compromises on cargo capacity.

Singapore's Position as the World's Largest Bunkering Hub

The port sold 54.92 MT of fuel in 2024, equaling about 18% of global marine demand and benefitting from 24/7 operations and over 50 licensed suppliers. Red Sea diversions boosted Asia-Europe voyages via the Cape, adding 8,500 nautical miles and 33% more fuel burn, translating into an extra 2-3 MT of bunkering volume. Jurong Island's land scarcity restricts storage expansion to roughly 20.5 million cubic meters, nudging some buyers toward Malaysia's Port Klang and Indonesia's Batam when space constraints pinch. Regional refinery build-outs in India and Vietnam could erode as much as 5-8% of Singapore's share by 2030 unless the city-state sustains its alternative-fuel lead. The Green Ship Programme's 2024 payouts for 460,000 ton of LNG and 880,000 ton of biofuels underscore the pivot to future fuels that aims to cement hub relevance over the long run.

Oil-Price Volatility Compressing Trader Margins

Brent crude oscillated between USD 70 and USD 90 per barrel in 2024, squeezing bunker-trader margins to 3-5% from the 6-8% typical in 2020-2022 as suppliers struggled to pass cost swings to shipowners on quarterly contracts. Maersk's average bunker expense fell to USD 569 per ton in Q1 2025, down 9% year-on-year, yet price transmission lagged crude by four to six weeks, spotlighting timing mismatches. Independents lacking upstream integration must pre-fund inventories 30-45 days ahead, exposing them to spikes that can erase quarterly profit. An HSFO price rally in October 2024 widened the HSFO-VLSFO spread to USD 150-180 per ton, prompting a 15% uptick in scrubber-equipped calls but forcing suppliers to widen bid-ask spreads by 5-7% to manage risk. Hedging remains limited for smaller firms because margin calls tie up scarce working capital.

Other drivers and restraints analyzed in the detailed report include:

- Rising Container Throughput from E-Commerce-Driven Trade

- Government Incentives for LNG Bunkering Infrastructure

- Decarbonisation Shift Toward Ammonia & Methanol Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Singapore bunker fuel market size for very-low-sulfur fuel oil reached 29.2 MT in 2025, corresponding to a 55.3% share as vessels complied with the IMO 2020 sulfur cap. LNG volumes, though starting from a small base, are rising at a 28.9% CAGR through 2031 on the back of 460,000 tons sold in 2024 and the arrival of additional LNG bunker barges. HSFO rebounded in 2024 when the price gap to VLSFO widened, with scrubber-fitted ships capturing savings and cutting payback periods below 18 months. Methanol, biofuels, and ammonia collectively remain below 2% today, yet regulatory clarity and pilot infrastructure signal an inflection from 2028 onward.

Longer term, alternative fuels are expected to challenge VLSFO dominance as shipowners future-proof fleets against impending carbon levies. The Singapore bunker fuel market is therefore likely to exhibit a dual-track profile: stable demand for conventional fuels through 2028, overlapped by accelerating uptake of LNG, methanol, and advanced biofuels thereafter. Feedstock constraints on waste-oil-based biodiesel and safety questions around ammonia keep supply tight, but early movers in these niches could secure premium margins once regulation mandates zero-carbon fuels.

Complete Report Scope:

- By Fuel Type

- High-Sulfur Fuel Oil (HSFO)

- Very-Low-Sulfur Fuel Oil (VLSFO)

- Ultra-Low-Sulfur Fuel Oil (ULSFO)

- Marine Gas Oil (MGO)

- Liquefied Natural Gas (LNG)

- Methanol

- Bio-/Synthetic Fuels

- Ammonia

- Other Fuel Types

- By Bunkering Method

- Ship-to-Ship

- Port-to-Ship (Truck/Pipeline)

- LNG Barge-to-Ship

- Portable Tanks and Containers

- By Vessel Type

- Container

- Tanker

- Bulk Carrier

- General Cargo

- Passenger/Ro-Pax

- Offshore and Specialized

List of Companies Covered in this Report:

- PetroChina International (Singapore)

- Sentek Marine & Trading

- Ocean Bunkering Services

- Equatorial Marine Fuel

- Shell Eastern Trading

- TotalEnergies Marine Fuels

- ExxonMobil Asia Pacific

- BP Singapore

- Chevron Singapore

- Glencore Singapore

- Trafigura - TFG Marine

- Minerva Bunkering

- Vitol Bunkers

- Bunker One (Singapore)

- Pavilion Energy

- CMA CGM Fuel Singapore

- Maersk Oil Trading Singapore

- Hafnia Bunkers

- Mitsui & Co. Energy Trading

- Itochu Petroleum Singapore

- Sinanju-Consort Bunkers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IMO 2020 sulfur-cap compliance boosting VLSFO demand

- 4.2.2 Singapore's position as the world's largest bunkering hub

- 4.2.3 Rising container throughput from e-commerce-driven trade

- 4.2.4 Government incentives for LNG bunkering infrastructure

- 4.2.5 Emerging bio-/e-fuel bunkering pilots under Green Ship Programme

- 4.2.6 Digital bunkering platforms lowering transaction costs

- 4.3 Market Restraints

- 4.3.1 Oil-price volatility compressing trader margins

- 4.3.2 Decarbonisation shift toward ammonia & methanol alternatives

- 4.3.3 Land-scarce storage expansion limitations

- 4.3.4 Stricter mass-flow-meter enforcement raising OPEX

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 High-Sulfur Fuel Oil (HSFO)

- 5.1.2 Very-Low-Sulfur Fuel Oil (VLSFO)

- 5.1.3 Ultra-Low-Sulfur Fuel Oil (ULSFO)

- 5.1.4 Marine Gas Oil (MGO)

- 5.1.5 Liquefied Natural Gas (LNG)

- 5.1.6 Methanol

- 5.1.7 Bio-/Synthetic Fuels

- 5.1.8 Ammonia

- 5.1.9 Other Fuel Types

- 5.2 By Bunkering Method

- 5.2.1 Ship-to-Ship

- 5.2.2 Port-to-Ship (Truck/Pipeline)

- 5.2.3 LNG Barge-to-Ship

- 5.2.4 Portable Tanks and Containers

- 5.3 By Vessel Type

- 5.3.1 Container

- 5.3.2 Tanker

- 5.3.3 Bulk Carrier

- 5.3.4 General Cargo

- 5.3.5 Passenger/Ro-Pax

- 5.3.6 Offshore and Specialized

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 PetroChina International (Singapore)

- 6.4.2 Sentek Marine & Trading

- 6.4.3 Ocean Bunkering Services

- 6.4.4 Equatorial Marine Fuel

- 6.4.5 Shell Eastern Trading

- 6.4.6 TotalEnergies Marine Fuels

- 6.4.7 ExxonMobil Asia Pacific

- 6.4.8 BP Singapore

- 6.4.9 Chevron Singapore

- 6.4.10 Glencore Singapore

- 6.4.11 Trafigura - TFG Marine

- 6.4.12 Minerva Bunkering

- 6.4.13 Vitol Bunkers

- 6.4.14 Bunker One (Singapore)

- 6.4.15 Pavilion Energy

- 6.4.16 CMA CGM Fuel Singapore

- 6.4.17 Maersk Oil Trading Singapore

- 6.4.18 Hafnia Bunkers

- 6.4.19 Mitsui & Co. Energy Trading

- 6.4.20 Itochu Petroleum Singapore

- 6.4.21 Sinanju-Consort Bunkers

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

南美洲船用燃料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)美國船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

南美洲船用燃料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)美國船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 船用燃料市場:依燃料類型、船舶類型、運作模式、船用引擎類型、最終用戶和通路分類-2026-2032年全球市場預測

船用燃料市場:依燃料類型、船舶類型、運作模式、船用引擎類型、最終用戶和通路分類-2026-2032年全球市場預測 船用燃料市場規模、佔有率和趨勢分析報告:按燃料類型、應用、地區和細分市場預測(2026-2033 年)

船用燃料市場規模、佔有率和趨勢分析報告:按燃料類型、應用、地區和細分市場預測(2026-2033 年) 全球船用燃料油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球船用燃料油市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 船用燃料市場規模、佔有率、趨勢及預測(按燃料類型、船舶類型、銷售商及地區分類),2026-2034年

船用燃料市場規模、佔有率、趨勢及預測(按燃料類型、船舶類型、銷售商及地區分類),2026-2034年 2026年全球船用燃料市場報告

2026年全球船用燃料市場報告 2026-2030年全球船用燃料油市場

2026-2030年全球船用燃料油市場 全球船用燃料市場-產業規模、佔有率、趨勢、機會和預測,按類型、商業分銷商、應用、地區和競爭格局分類,2021-2031年預測

全球船用燃料市場-產業規模、佔有率、趨勢、機會和預測,按類型、商業分銷商、應用、地區和競爭格局分類,2021-2031年預測