|

市場調查報告書

商品編碼

2072513

美國船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Bunker Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

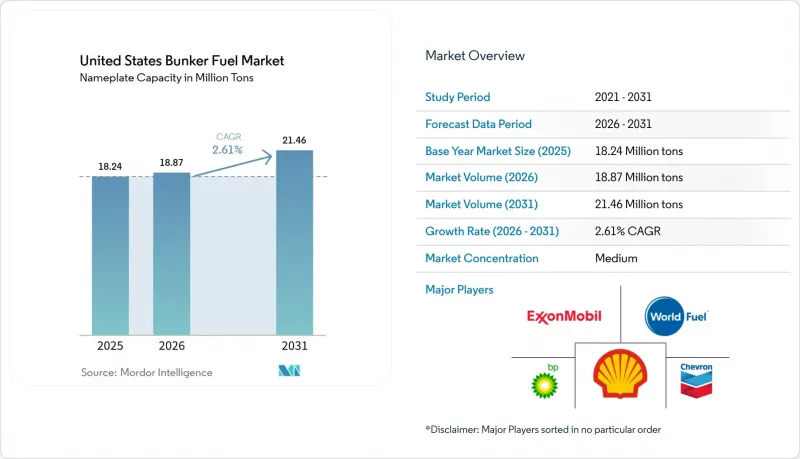

據 Mordor Intelligence 稱,2025 年美國船用燃料市場規模(按額定容量計算)為 1824 萬噸,預計到 2031 年將從 2026 年的 1887 萬噸成長至 2146 萬噸,在預測期(2026-2031 年)內61%。

本報告按燃料類型(高硫燃料油、超低硫燃料油、超低硫燃料油、船用輕柴油、液化天然氣、甲醇、生物/合成燃料、氨等)、燃料庫方式(船對船、港對船、液化天然氣駁船對船、可攜式儲罐/貨櫃)和船舶類型(貨櫃船、油輪、散裝船駁船、貨船、船舶/船/特種船)。市場規模和預測均以噸(MT)為單位。

美國船用燃料市場趨勢與洞察

為遵守國際海事組織2020年硫排放法規,需求激增。

東岸煉油廠設備配置不足,迫使墨西哥灣沿岸擁有殘油重整設施的煉油廠調整供應結構,導致現貨採購的前置作業時間延長。高硫燃料油 (HSFO) 和超低硫燃料油 (VLSFO) 之間的價格差異已縮小至每噸近 50 美元,降低了投資新建脫硫維修的合理性,並迫使更多業者使用合規燃料。雖然已投入使用的配備脫硫裝置的船舶仍在繼續消耗高硫燃料油,但加州和康乃狄克州對洗滌水的更嚴格規定限制了開放回路系統的使用,並降低了地理柔軟性。預計到 2025 年,美國海岸警衛隊防衛隊檢查員在主要貨櫃油輪停靠港口增加抽樣檢查,將使因違反硫排放規定而被滯留的船舶數量增加 18%。這些因素共同作用,穩定了支撐美國船用燃料市場超低硫燃料油需求的合規溢價。

美國液化天然氣加註基礎設施擴建

超過6500萬美元的聯邦和州政府津貼加速了洛杉磯和傑克遜維爾陸上液化天然氣(LNG)設施的建設,為2026年及以後投入運營的雙燃料貨櫃船和郵輪提供支援。休士頓航道供應商正在利用現有的液化終端進行海上船對船傳輸,與駁船運輸相比,LNG交付成本降低了15%。 2025年3月,傑克遜維爾迎來了首艘符合《瓊斯法案》的12000立方米LNG加註駁船的投入使用,該駁船將加註時間縮短了40%,為沿海運輸效率樹立了新標竿。由於擔心甲烷洩漏,美國環保署(EPA)提案在引擎上安裝監測系統,這可能會使新船的成本增加50萬美元。然而,原始設備製造商(OEM)正在轉向封閉回路型燃燒系統,他們聲稱該系統可以將洩漏減少70%。嘉年華集團和皇家加勒比海郵輪公司在 12 艘計劃投入運營的郵輪上率先採用液化天然氣,確保了需求基礎,並降低了與額外基礎設施投資相關的風險。

液化天然氣燃料庫設施的高資本成本

專門設計的液化天然氣駁船的建造費用在4000萬美元至6000萬美元之間,陸上設施的建造費用則超過8000萬美元。然而,對於中小港口而言,在運輸量無法確定的情況下,很難承擔如此龐大的資本支出。截至2026年初,僅有三艘符合《瓊斯法案》的液化天然氣駁船投入使用,導致沿海航線供不應求,迫使貨物從卡車轉運至船舶。這使得交付價格飆升了高達30%。由於貸款機構已將氨和氫氣可能造成的市場動盪風險納入考量,貸款條件變得更加嚴格,資本充足率已提高至40%以上,最低利率也已接近15%。在休士頓,原定於2025年底開工的價值9,000萬美元的LNG接收站因需求的不確定性而被推遲,港口當局也繼續保持謹慎態度。在長期採購協議最終敲定之前,主要樞紐以外地區的液化天然氣基礎設施擴張很可能會繼續落後於整體市場需求。

細分市場分析

2025年,超低硫燃料油(VLSFO)將占美國船用燃料市場的40.63%,滿足廣大船隊的合規需求。液化天然氣(LNG)預計將以每年9.1%的速度成長,這得益於新型雙燃料船舶的交付以及計劃於2028年投入使用的三艘新型燃料駁船,為營運商實現其2030年排放目標提供了切實可行的途徑。船用輕柴油(MGO)和超低硫燃料油(ULSFO)在海上支援船舶領域仍佔據著獨特的地位,因為其引擎的簡易性超過了成本溢價。高硫燃料油(HSFO)的需求保持穩定,主要來自配備脫硫裝置的油輪和散裝貨船,但由於沿海地區排放法規的日益嚴格,其市場範圍正在縮小。甲醇和氨仍處於商業化前期階段,但墨西哥灣沿岸地區已宣布超過30億美元的產能,顯示2028年後美國船用燃料市場格局可能會重組。

液化天然氣(LNG)能量密度低,但由於國內天然氣資源豐富,其交付成本較低,部分抵消了這一劣勢。隨著船東權衡長期碳排放責任與短期資金柔軟性,超低硫燃料油(VLSFO)的成長正在放緩。這種矛盾可能會在整個預測期內影響船隊的採購政策。馬士基簽訂了一份20萬噸的綠色甲醇採購契約,為未來的合約設定了價格基準,綠色甲醇的信譽也因此不斷提升。生物燃料混合燃料符合低碳燃料標準(LCFS)的積分要求,有助於抵消西海岸地區具有競爭力的交付成本,但由於原料短缺,目前供應有限。鑑於燃料多樣化的現狀,供應商面臨著在美國船用燃料市場維持燃料組合多元化的壓力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 國際海事組織對2020年硫排放法規的反應非常強烈。

- 美國液化天然氣燃料庫基礎設施的擴建

- 美國油輪和貨櫃運輸量增加

- 郵輪公司對低硫燃料的需求

- 加州低碳燃料標準(LCFS)引領可再生生物燃料的發展。

- IRA稅額扣抵正在促進綠色甲醇的供應。

- 市場限制因素

- 液化天然氣燃料庫設施的高資本成本

- 原油價格波動會影響燃油經濟性

- 加裝售後市場洗滌器以降低LS燃油消耗

- 計劃中的碳排放稅導致投資轉向其他領域。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- PESTLE分析

第5章 市場規模與成長預測

- 按燃料類型

- 高硫燃料油(HSFO)

- 超低硫燃料油(VLSFO)

- 超低硫燃料油(ULSFO)

- 船用柴油燃料(MGO)

- 液化天然氣(LNG)

- 甲醇

- 生物/合成燃料

- 氨

- 其他燃料類型

- 透過加油方法

- 船對船

- 從港口到船舶(卡車/管道)

- 從液化天然氣駁船到船舶

- 可攜式儲罐和容器

- 按船舶類型

- 容器

- 油船

- 散貨船

- 普通貨物

- 客運/滾裝客車

- 海上及特種船舶

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Exxon Mobil Corporation

- Shell Plc

- Chevron Corporation

- BP Plc

- TotalEnergies SE

- World Fuel Services Corp.

- NuStar Energy LP

- Phillips 66

- Marathon Petroleum Corp.

- Valero Energy Corp.

- Trafigura Group Pte. Ltd.

- Glencore Plc

- Peninsula Petroleum

- Crowley Maritime Corp.

- Seacor Holdings

- Kinder Morgan Inc.

- Global Gas & Oil Trading LLC

- Clipper Oil

- Sprague Operating Resources

- Pilot Thomas Logistics

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states bunker fuel market size in terms of nameplate capacity was valued at 18.24 million tons in 2025 and is estimated to grow from 18.87 million tons in 2026 to reach 21.46 million tons by 2031, at a CAGR of 2.61% during the forecast period (2026-2031).

This report is Segmented by Fuel Type (HSFO, VLSFO, ULSFO, MGO, LNG, Methanol, Bio-/Synthetic Fuels, Ammonia, and More), Bunkering Method (Ship-To-Ship, Port-To-Ship, LNG Barge-To-Ship, and Portable Tanks and Containers), and Vessel Type (Container, Tanker, Bulk Carrier, General Cargo, Passenger/Ro-Pax, and Offshore and Specialized). The Market Sizes and Forecasts are Provided in Terms of Volume (MT)

United States Bunker Fuel Market Trends and Insights

IMO 2020 sulfur-cap compliance surge

Refinery configuration gaps on the East Coast forced supply realignment toward Gulf plants that possess residue-upgrading hardware, creating longer lead times for spot purchases. The narrowing HSFO-VLSFO spread, now near USD 50 per metric ton, has erased the investment case for new scrubber retrofits, locking more operators into compliant fuels. Scrubber-equipped vessels already on the water continue to consume HSFO, but stricter wash-water restrictions in California and Connecticut are curbing open-loop systems and reducing geographic flexibility. Detentions for sulfur violations rose 18% in 2025 as U.S. Coast Guard inspectors intensified sampling at major container and tanker gateways. Collectively, these factors stabilize the compliance premium that underpins VLSFO demand inside the United States bunker fuel market.

Expansion of U.S. LNG Bunkering Infrastructure

Federal and state grants exceeding USD 65 million have catalyzed groundbreaking for shore-based LNG facilities at Los Angeles and Jacksonville, supporting dual-fuel container and cruise tonnage arriving from 2026 onward. Houston Ship Channel suppliers exploit existing liquefaction terminals for offshore ship-to-ship transfers, shaving 15% from delivered LNG costs relative to barge deliveries. The first 12,000-cubic-meter Jones Act-compliant LNG bunker barge entered service at Jacksonville in March 2025 and cut fueling time by 40%, setting a new benchmark for coastal efficiency. Methane-slip concerns prompted the Environmental Protection Agency to propose on-engine monitoring that could add USD 0.5 million to newbuilds, but OEMs are rolling out closed-loop combustion systems that claim 70% slip reduction. Early LNG adoption by Carnival Corporation and Royal Caribbean for twelve forthcoming cruise ships secures a demand anchor that de-risks additional infrastructure commitments.

High Capital Cost of LNG Bunkering Assets

Purpose-built LNG barges cost USD 40-60 million while shore installations exceed USD 80 million, capital levels that smaller ports struggle to underwrite without volume certainty. Only three Jones Act-compliant LNG barges were in service by early 2026, creating supply gaps on coastal trades and forcing truck-to-ship transfers that inflate delivered prices by up to 30%. Financing terms have tightened as lenders factor in ammonia and hydrogen disruption risk, pushing equity requirements above 40% and hurdle rates toward 15%. Houston deferred a USD 90 million LNG terminal in late 2025 over demand uncertainty, signaling continued caution among port authorities. Until more long-term offtake contracts materialize, LNG infrastructure growth outside core hubs will lag broader market needs.

Other drivers and restraints analyzed in the detailed report include:

- Growing U.S. Tanker and Container Traffic

- Renewable Bio-Blend Bunkers Driven by California LCFS

- Crude-Price Volatility Impacting Fuel Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

VLSFO accounted for 40.63% of the United States bunker fuel market size in 2025, anchoring compliance demand for the broader fleet. LNG is forecast to expand at 9.1% annually, supported by dual-fuel newbuild deliveries and three new bunker barges scheduled before 2028, giving operators a viable pathway to meet 2030 emissions targets. MGO and ULSFO retain niche roles among offshore support vessels where engine simplicity outweighs the cost premium. HSFO demand has stabilized around scrubber-equipped tankers and bulk carriers but faces geographic shrinkage as coastal discharge rules tighten. Methanol and ammonia remain pre-commercial yet have more than USD 3 billion in announced capacity along the Gulf Coast, signaling a potential reshuffling of the United States bunker fuel market landscape after 2028.

LNG's energy-density disadvantage is partially offset by lower delivered costs linked to abundant domestic gas. VLSFO growth is slowing as owners weigh long-term carbon liability against short-term capital flexibility, a tension likely to define fleet-wide procurement through the forecast horizon. Green methanol gains credibility following Maersk's 200,000-metric-ton offtake deal, which sets a pricing benchmark for additional contracts. Bio-blends qualify for LCFS credits that subsidize a competitive delivered cost on the West Coast, yet feedstock scarcity caps immediate volume. The multi-fuel reality underscores the need for suppliers to maintain diversified fuel portfolios within the United States bunker fuel market.

Complete Report Scope:

- By Fuel Type

- High-Sulfur Fuel Oil (HSFO)

- Very-Low-Sulfur Fuel Oil (VLSFO)

- Ultra-Low-Sulfur Fuel Oil (ULSFO)

- Marine Gas Oil (MGO)

- Liquefied Natural Gas (LNG)

- Methanol

- Bio-/Synthetic Fuels

- Ammonia

- Other Fuel Types

- By Bunkering Method

- Ship-to-Ship

- Port-to-Ship (Truck/Pipeline)

- LNG Barge-to-Ship

- Portable Tanks and Containers

- By Vessel Type

- Container

- Tanker

- Bulk Carrier

- General Cargo

- Passenger/Ro-Pax

- Offshore and Specialized

List of Companies Covered in this Report:

- Exxon Mobil Corporation

- Shell Plc

- Chevron Corporation

- BP Plc

- TotalEnergies SE

- World Fuel Services Corp.

- NUStar Energy L.P.

- Phillips 66

- Marathon Petroleum Corp.

- Valero Energy Corp.

- Trafigura Group Pte. Ltd.

- Glencore Plc

- Peninsula Petroleum

- Crowley Maritime Corp.

- Seacor Holdings

- Kinder Morgan Inc.

- Global Gas & Oil Trading LLC

- Clipper Oil

- Sprague Operating Resources

- Pilot Thomas Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IMO 2020 sulfur-cap compliance surge

- 4.2.2 Expansion of U.S. LNG bunkering infrastructure

- 4.2.3 Growing U.S. tanker & container traffic

- 4.2.4 Cruise-line demand for low-sulfur fuels

- 4.2.5 Renewable bio-blend bunkers driven by California LCFS

- 4.2.6 IRA tax credits catalyzing green-methanol supply

- 4.3 Market Restraints

- 4.3.1 High capital cost of LNG bunkering assets

- 4.3.2 Crude-price volatility impacting fuel economics

- 4.3.3 Retrofit scrubbers reducing LS-fuel consumption

- 4.3.4 Prospective carbon-levy shifting investment away

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 High-Sulfur Fuel Oil (HSFO)

- 5.1.2 Very-Low-Sulfur Fuel Oil (VLSFO)

- 5.1.3 Ultra-Low-Sulfur Fuel Oil (ULSFO)

- 5.1.4 Marine Gas Oil (MGO)

- 5.1.5 Liquefied Natural Gas (LNG)

- 5.1.6 Methanol

- 5.1.7 Bio-/Synthetic Fuels

- 5.1.8 Ammonia

- 5.1.9 Other Fuel Types

- 5.2 By Bunkering Method

- 5.2.1 Ship-to-Ship

- 5.2.2 Port-to-Ship (Truck/Pipeline)

- 5.2.3 LNG Barge-to-Ship

- 5.2.4 Portable Tanks and Containers

- 5.3 By Vessel Type

- 5.3.1 Container

- 5.3.2 Tanker

- 5.3.3 Bulk Carrier

- 5.3.4 General Cargo

- 5.3.5 Passenger/Ro-Pax

- 5.3.6 Offshore and Specialized

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Exxon Mobil Corporation

- 6.4.2 Shell Plc

- 6.4.3 Chevron Corporation

- 6.4.4 BP Plc

- 6.4.5 TotalEnergies SE

- 6.4.6 World Fuel Services Corp.

- 6.4.7 NuStar Energy L.P.

- 6.4.8 Phillips 66

- 6.4.9 Marathon Petroleum Corp.

- 6.4.10 Valero Energy Corp.

- 6.4.11 Trafigura Group Pte. Ltd.

- 6.4.12 Glencore Plc

- 6.4.13 Peninsula Petroleum

- 6.4.14 Crowley Maritime Corp.

- 6.4.15 Seacor Holdings

- 6.4.16 Kinder Morgan Inc.

- 6.4.17 Global Gas & Oil Trading LLC

- 6.4.18 Clipper Oil

- 6.4.19 Sprague Operating Resources

- 6.4.20 Pilot Thomas Logistics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

南美洲船用燃料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)新加坡船用燃料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

南美洲船用燃料:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)新加坡船用燃料:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)船用燃料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 船用燃料市場:依燃料類型、船舶類型、運作模式、船用引擎類型、最終用戶和通路分類-2026-2032年全球市場預測

船用燃料市場:依燃料類型、船舶類型、運作模式、船用引擎類型、最終用戶和通路分類-2026-2032年全球市場預測 船用燃料市場規模、佔有率和趨勢分析報告:按燃料類型、應用、地區和細分市場預測(2026-2033 年)

船用燃料市場規模、佔有率和趨勢分析報告:按燃料類型、應用、地區和細分市場預測(2026-2033 年) 全球船用燃料油市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球船用燃料油市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 船用燃料市場規模、佔有率、趨勢及預測(按燃料類型、船舶類型、銷售商及地區分類),2026-2034年

船用燃料市場規模、佔有率、趨勢及預測(按燃料類型、船舶類型、銷售商及地區分類),2026-2034年 2026年全球船用燃料市場報告

2026年全球船用燃料市場報告 2026-2030年全球船用燃料油市場

2026-2030年全球船用燃料油市場 全球船用燃料市場-產業規模、佔有率、趨勢、機會和預測,按類型、商業分銷商、應用、地區和競爭格局分類,2021-2031年預測

全球船用燃料市場-產業規模、佔有率、趨勢、機會和預測,按類型、商業分銷商、應用、地區和競爭格局分類,2021-2031年預測