|

市場調查報告書

商品編碼

2073350

印尼資料中心建置:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Indonesia Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

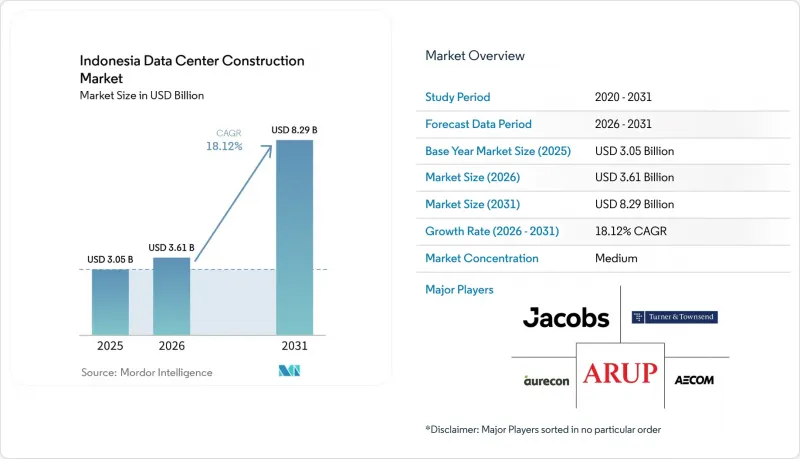

據 Mordor Intelligence 稱,印尼資料中心建設市場預計到 2026 年價值 36.1 億美元,高於 2025 年的 30.5 億美元,預計到 2031 年將達到 82.9 億美元。

預計 2026 年至 2031 年的複合年成長率為 18.12%。

本報告按資料中心層級(一級和二級、三級和四級)、資料中心類型(託管、超大規模雲端超大規模資料中心業者(CSP) 自建、企業級、邊緣運算)和基礎設施(電力基礎設施、機械基礎設施)進行分類。市場預測以美元計價。

印尼資料中心建置市場趨勢與洞察

雲端運算和人工智慧主導的超大規模投資正在加速對設施的需求。

超大規模雲端公司正在重塑印尼的資料中心建設市場,它們採用的人工智慧工作負載需要液冷、40-60千瓦的機架以及每個園區超過50兆瓦的連續供電模組。騰訊5億美元的投資、英偉達和印尼電信(Indosat Ooredoo Hutchison)2億美元的GPU中心,以及BDx公司500兆瓦可再生能源供電的人工智慧園區,都清楚地展現了印尼資本流入的規模。人工智慧最佳化的資料中心正在推動超大規模設施對高密度基礎設施和先進冷卻技術的需求。對浸沒式冷卻和高密度電動公車的需求不斷成長,正將當地承包商的技能推向極限,促使全球工程公司與本土專家組建聯合團隊。隨著土地所有者提供預先已通過核准的許可證和已建成的變電站,建設工期已從2022年的平均22個月縮短至2025年的16-18個月。

《2030年印尼國家數位藍圖》將加速公共部門的IT發展步伐。

此藍圖要求將各部會的IT工作負載整合到四個國家資料中心(PDN)。旗艦專案芝卡朗PDN耗資1.6468億歐元(1.8959億美元),將提供25,000個處理器核心,計畫於2024年8月投入運作。另外三個PDN站點計劃在巴淡島和努沙登加拉群島建設,預計未來五年對Tier 4標準設施的需求將持續成長。 2023年第82號總統令要求各機構從傳統設施遷移,導致安全雲端區域、零信任網路和網路彈性機房的設計和建設合約激增。此外,推出的「INA DIGITAL」也推動了這項擴張。 「INA DIGITAL」是一個全新的公共服務一站式窗口,於2024年5月啟動,數據顯示各部會之間的頻寬需求遠高於先前的預期。

電力消耗增加和碳排放稅負擔加重

印尼的碳排放稅制度於2022年生效,對超過各行業排放上限的部分課稅。由於煤炭發電仍佔印尼國家電力公司(PLN)發電結構的67%,因此大規模園區若不簽訂可再生能源購電協議(PPA)並安裝現場太陽能發電設施,將面臨成本大幅超支的風險。 PLN提出的2060年淨零排放的藍圖加劇了未來價格的不確定性,要求營運商實施即時電力監控、餘熱再利用和需量反應計畫。像EDGE2這樣的先行業者已經將碳中和的成本轉嫁給了租戶,開創了溢價定價的先例。

細分市場分析

三級資料中心佔印尼資料中心建置市場的50.62%,體現了成本與可用性之間的平衡。像NeutraDC這樣的託管服務供應商正利用三級認證來吸引那些既要求99.982%運轉率,也受限於資本支出的企業租戶。一級和二級資料中心則繼續服務於對延遲敏感的邊緣節點,在這些節點上,適度的冗餘是可以接受的。

隨著人工智慧工作負載和強制性主權雲的出現,零停機時間成為接受度,印尼資料中心建設市場正以18.6%的複合年成長率快速成長,Tier 4級資料中心正在重塑印尼資料中心建設市場。 DCI Indonesia位於雅加達市中心的Tier IV級邊緣資料中心便是向零故障架構轉型的一個典範,其採用的浸沒式冷卻和分區電源路徑技術使其專案成本比Tier 3級資料中心高出25-30%。 STT GDC發布的AI叢集將進一步鞏固Tier 4級資料中心在未來設計中的地位。

鑑於印尼企業基礎分散,預計到2025年,託管服務將佔印尼企業總收入的56.72%。像Digital Edge位於雅加達的23兆瓦資料中心這樣的設施,透過模組化機房提供擴充性,並與主要租戶簽訂多年期契約,從而比傳統的運營商機房更快地提高入住率。

自建超大規模資料中心業者資料中心正以19.5%的複合年成長率成長,透過在20公頃的土地上建造超過120兆瓦的園區,不斷擴大印尼資料中心建設市場。 EdgeConneX獲得的4.038億美元永續發展掛鉤融資,便是營運商如何利用綠色債券結構為可再生能源建設項目提供資金的典範。超大規模資料中心業者的湧入正迫使現有託管業者轉向批發套房或客製化建設模式,模糊了曾經涇渭分明的多租戶和單一租戶策略之間的界限。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 雲端運算和人工智慧主導的超大規模投資正在加速對設施的需求。

- 《2030年印尼國家數位藍圖》正在推動公共部門對IT的需求。

- 在雅加達和巴淡島登陸的新型國際海底電纜提高了延遲標準。

- 雅加達-萬隆資料中心走廊的公私合營獎勵措施

- 購電協議 (PPA) 和綠色電價方案為校園運作可再生能源供電鋪平了道路。

- 在泗水、棉蘭和望加錫發展邊緣樞紐,以支持新興的二線城市。

- 市場限制因素

- 電力消耗增加和碳排放稅的影響

- 雅加達市中心及芝卡朗工業園區周邊地價飆升

- 機電工程認證專業建築工人短缺

- 由於PLN變電站電網維修週期延長,電力恢復工作被推遲。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 資料中心的關鍵統計數據

- 印尼資料中心營運商列表(每兆瓦)

- 印尼即將開展的主要資料中心項目清單(2025-2030 年)

- 印尼資料中心建置中的資本支出與營運支出

- 2023 年及 2024 年印尼主要城市資料中心電力容量吸收量(兆瓦)。

- 將人工智慧(AI)引入印尼的資料中心建設

- 監理與合規框架

第5章 市場規模與成長預測

- 層級類型

- 一級和二級

- 三級

- 第四級

- 依資料中心類型

- 搭配

- 自主研發的超大規模資料中心業者(CSP)

- 企業和邊緣運算

- 透過基礎設施

- 按類型分類的電氣基礎設施

- 配電解決方案

- 配電解決方案

- 備用電源解決方案

- 備用電源解決方案

- 配電解決方案

- 透過機械基礎設施

- 冷卻系統

- 冷卻系統

- 機架和機櫃

- 機架和機櫃

- 伺服器和儲存

- 伺服器和儲存

- 其他機械基礎設施

- 其他機械基礎設施

- 冷卻系統

- 一般建築

- 服務 - 設計與諮詢、整合、支援與維護

- 按類型分類的電氣基礎設施

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- Data Center Infrastructure Investment Based on Megawatt(MW)Capacity, 2024 vs 2030

- Data Center Construction Landscape(Key Vendors Listings)

- 公司簡介

- Aurecon Group Pty Ltd

- PT AECOM Indonesia

- Arup Group

- Jacobs Engineering Group Inc.

- Turner and Townsend

- AWP Architects

- Aesler Group International

- PT Arkonin

- DSCO Group Pte Ltd

- Larsen and Toubro Ltd

- NTT Global Data Centers Indonesia

- Huawei Technologies

- Vertiv Group Corp.

- Schneider Electric SE

- ABB Ltd

- Legrand SA

- PT DCI Indonesia Tbk

- Princeton Digital Group

- Telkom Data Ekosistem(NeutraDC)

- BDx Indonesia

- List of Data Center Construction Companies

第7章 市場機會與未來展望

According to Mordor Intelligence, the indonesian data center construction market size in 2026 is estimated at USD 3.61 billion, growing from 2025 value of USD 3.05 billion with 2031 projections showing USD 8.29 billion, growing at 18.12% CAGR over 2026-2031.

This report is Segmented by Tier Type (Tier 1 and 2, Tier 3 and Tier 4), Data Center Type(Colocation, Self-Built Hyperscalers (CSPs), Enterprise, and Edge), Infrastructure (Electrical Infrastructure, Mechanical Infrastructure). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Data Center Construction Market Trends and Insights

Cloud and AI-Led Hyperscale Investments Accelerate Facility Demand

Hyperscale cloud firms are redefining the Indonesian data center construction market by introducing AI workloads that require liquid-cooling, 40-60 kW racks, and contiguous power blocks exceeding 50 MW per campus. Tencent's USD 500 million commitment, Nvidia's USD 200 million GPU center with Indosat Ooredoo Hutchison, and BDx's 500 MW renewable-powered AI campus exemplify the scale of capital flowing into. Indonesia (AI) optimised data center is increasing demand for high-density infrastructure and advanced cooling technologies across hyperscale facilities. The need for immersion cooling and high-density electrical buses is stretching local contractors' skill sets, prompting global engineering firms to form joint teams with domestic specialists. Construction schedules have tightened from an average 22 months in 2022 to 16-18 months in 2025 as land owners provide pre-approved permits and ready-built substations.

National Digital Indonesia Roadmap 2030 Spurs Public-Sector IT Loads

The Roadmap mandates the consolidation of ministerial IT workloads into four National Data Centers (PDN). The flagship Cikarang PDN, financed at EUR 164.68 million (USD 189.59 million), delivers 25,000 processor cores and is scheduled to begin in August 2024. Three additional PDN sites in Batam and Nusantara are in the pipeline, ensuring steady demand for Tier 4 builds over the next five years. Presidential Regulation 82/2023 requires agencies to migrate from legacy facilities, stimulating a surge of design-build contracts for secure cloud zones, zero-trust networks, and cyber-resilient plant rooms. The ramp-up has also catalysed INA DIGITAL, the new single window for public services that launched in May 2024, which now drives inter-ministerial bandwidth requirements well beyond earlier forecasts

Rising Power-Use and Carbon-Tax Exposure

Indonesia's carbon-tax regime took effect in 2022, applying levies on emissions that exceed sector caps. Because coal still supplies 67% of PLN's generation mix, large campuses risk material cost over-runs unless they secure renewable PPAs or on-site solar. PLN's roadmap to net-zero by 2060 adds future price uncertainty, driving operators toward real-time power monitoring, waste-heat reuse, and demand-response programmes. Early movers such as EDGE2 now pass carbon-neutral costs through to tenants, setting a precedent for premium pricing.

Other drivers and restraints analyzed in the detailed report include:

- New International Subsea Cables Landing in Jakarta and Batam Raise Latency Standards

- Edge Build-Outs in Surabaya, Medan and Makassar to Serve Tier-2 Cities

- Escalating Land Prices Around Jakarta CBD and Cikarang Industrial Parks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tier 3 facilities account for 50.62% of the Indonesia data center construction market size, reflecting their balanced cost-to-availability ratio. Colocation providers such as NeutraDC rely on Tier 3 certifications to court enterprise tenants that demand 99.982% uptime while staying mindful of capex constraints. Tier 1 and Tier 2 sites continue to serve latency-sensitive edge nodes where modest redundancy is acceptable.

Tier 4 builds, advancing at 18.6% CAGR, are reshaping the Indonesia data center construction market as AI workloads and sovereign-cloud mandates eliminate tolerance for downtime. DCI Indonesia's Tier IV edge facility in central Jakarta signals the march toward zero-fault architecture, with immersion cooling and compartmentalised power paths driving project costs 25-30% above Tier 3. STT GDC's announced AI clusters will further entrench Tier 4's position in future-ready designs.

Colocation maintains 56.72% of 2025 revenue thanks to Indonesia's fragmented enterprise base. Facilities such as Digital Edge's 23 MW Jakarta site offer scalability through modular halls, securing multi-year anchor tenants that raise the utilisation curve faster than legacy carrier-hotels.

Self-build hyperscalers are registering a 19.5% CAGR, swelling the Indonesia data center construction market through 120-MW-plus campuses on 20-hectare plots. EdgeConneX's USD 403.8 million sustainability-linked loan typifies how operators deploy green-bond structures to finance renewable-powered builds. The hyperscaler push is forcing colocation incumbents to pivot toward wholesale suites and build-to-suit models, blurring once-clear lines between multi-tenant and single-tenant strategies.

Complete Report Scope:

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Distribution Solution

- Power Backup Solutions

- Power Backup Solutions

- Power Distribution Solution

- By Mechanical Infrastructure

- Cooling Systems

- Cooling Systems

- Racks and Cabinets

- Racks and Cabinets

- Servers and Storage

- Servers and Storage

- Other Mechanical Infrastructure

- Other Mechanical Infrastructure

- Cooling Systems

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

List of Companies Covered in this Report:

- Aurecon Group Pty Ltd

- PT AECOM Indonesia

- Arup Group

- Jacobs Engineering Group Inc.

- Turner and Townsend

- AWP Architects

- Aesler Group International

- PT Arkonin

- DSCO Group Pte Ltd

- Larsen and Toubro Ltd

- NTT Global Data Centers Indonesia

- Huawei Technologies

- Vertiv Group Corp.

- Schneider Electric SE

- ABB Ltd

- Legrand SA

- PT DCI Indonesia Tbk

- Princeton Digital Group

- Telkom Data Ekosistem (NeutraDC)

- BDx Indonesia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-and-AI led hyperscale investments accelerate facility demand

- 4.2.2 National Digital Indonesia Roadmap 2030 spurs public-sector IT loads

- 4.2.3 New international subsea cables landing in Jakarta and Batam raise latency standards

- 4.2.4 Jakarta Bandung data-center corridor public-private zoning incentives

- 4.2.5 Corporate PPAs and green-tariff schemes open the door for renewable-powered campuses

- 4.2.6 Edge build-outs in Surabaya, Medan and Makassar to serve emerging Tier-2 cities

- 4.3 Market Restraints

- 4.3.1 Rising power-use and carbon-tax exposure

- 4.3.2 Escalating land prices around Jakarta CBD and Cikarang industrial parks

- 4.3.3 Shortage of specialised MEP-certified construction labour

- 4.3.4 Slow grid-upgrade cycle times at PLN substations delay energisation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Data Center Statistics

- 4.8.1 Exhaustive Data Center Operators in Indonesia(in MW)

- 4.8.2 List of Major Upcoming Data Center Projects in Indonesia (2025-2030)

- 4.8.3 CAPEX and OPEX For Indonesia Data Center Construction

- 4.8.4 Data Center Power Capacity Absorption In MW, Selected Cities, Indonesia, 2023 and 2024

- 4.9 Artificial Intelligence (AI) Inclusion in Data Center Construction in Indonesia

- 4.10 Regulatory and Compliance Framework

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Tier Type

- 5.1.1 Tier 1 and 2

- 5.1.2 Tier 3

- 5.1.3 Tier 4

- 5.2 By Data Center Type

- 5.2.1 Colocation

- 5.2.2 Self-build Hyperscalers (CSPs)

- 5.2.3 Enterprise and Edge

- 5.3 By Infrastructure

- 5.3.1 By Electrical Infrastructure

- 5.3.1.1 Power Distribution Solution

- 5.3.1.1.1 Power Distribution Solution

- 5.3.1.2 Power Backup Solutions

- 5.3.1.2.1 Power Backup Solutions

- 5.3.1.1 Power Distribution Solution

- 5.3.2 By Mechanical Infrastructure

- 5.3.2.1 Cooling Systems

- 5.3.2.1.1 Cooling Systems

- 5.3.2.2 Racks and Cabinets

- 5.3.2.2.1 Racks and Cabinets

- 5.3.2.3 Servers and Storage

- 5.3.2.3.1 Servers and Storage

- 5.3.2.4 Other Mechanical Infrastructure

- 5.3.2.4.1 Other Mechanical Infrastructure

- 5.3.2.1 Cooling Systems

- 5.3.3 General Construction

- 5.3.4 Service - Design and Consulting, Integration, Support and Maintenance

- 5.3.1 By Electrical Infrastructure

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Data Center Infrastructure Investment Based on Megawatt (MW) Capacity, 2024 vs 2030

- 6.5 Data Center Construction Landscape (Key Vendors Listings)

- 6.6 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.6.1 Aurecon Group Pty Ltd

- 6.6.2 PT AECOM Indonesia

- 6.6.3 Arup Group

- 6.6.4 Jacobs Engineering Group Inc.

- 6.6.5 Turner and Townsend

- 6.6.6 AWP Architects

- 6.6.7 Aesler Group International

- 6.6.8 PT Arkonin

- 6.6.9 DSCO Group Pte Ltd

- 6.6.10 Larsen and Toubro Ltd

- 6.6.11 NTT Global Data Centers Indonesia

- 6.6.12 Huawei Technologies

- 6.6.13 Vertiv Group Corp.

- 6.6.14 Schneider Electric SE

- 6.6.15 ABB Ltd

- 6.6.16 Legrand SA

- 6.6.17 PT DCI Indonesia Tbk

- 6.6.18 Princeton Digital Group

- 6.6.19 Telkom Data Ekosistem (NeutraDC)

- 6.6.20 BDx Indonesia

- 6.7 List of Data Center Construction Companies

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 資料中心建置市場:依資料中心類型、建設形式、等級、組件、建設服務類型及最終用戶產業分類-2026-2032年全球市場預測

資料中心建置市場:依資料中心類型、建設形式、等級、組件、建設服務類型及最終用戶產業分類-2026-2032年全球市場預測 2026年全球資料中心建置市場報告

2026年全球資料中心建置市場報告 全球資料中心建設市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球資料中心建設市場規模、佔有率、趨勢和成長分析報告(2026-2034) 資料中心建置市場:依層級、建設類型、企業規模、應用與地區分類

資料中心建置市場:依層級、建設類型、企業規模、應用與地區分類 資料中心建置市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、設備北美資料中心建置:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

資料中心建置市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、材料類型、部署模式、最終用戶、設備北美資料中心建置:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 資料中心建置市場規模、佔有率和趨勢分析報告:按基礎設施、層級、最終用途、地區和細分市場預測(2026-2033 年)

資料中心建置市場規模、佔有率和趨勢分析報告:按基礎設施、層級、最終用途、地區和細分市場預測(2026-2033 年) 2026-2030年全球資料中心建置市場新加坡資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

2026-2030年全球資料中心建置市場新加坡資料中心建置:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)