|

市場調查報告書

商品編碼

2073331

非洲飼料香精和甜味劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Africa Feed Flavors and Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

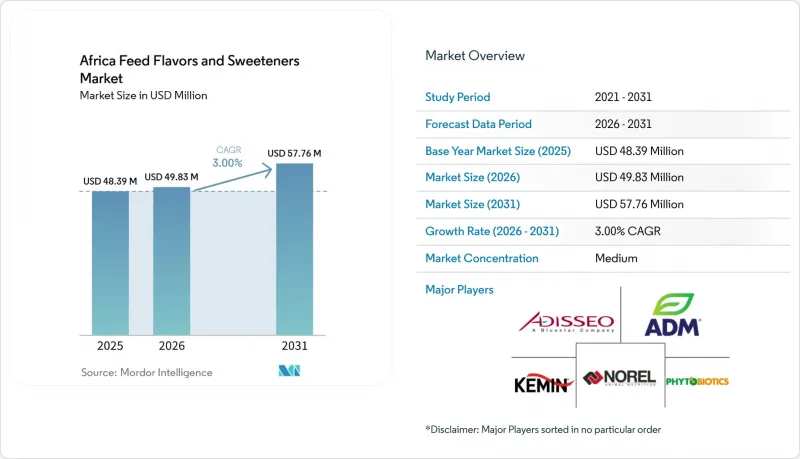

根據 Mordor Intelligence 預測,非洲飼料香精和甜味劑市場規模預計將在 2025 年達到 4,839 萬美元,從 2026 年的 4,983 萬美元成長到 2031 年的 5,776 萬美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按輔料(香料和甜味劑)、目標動物(水產養殖、家禽、反芻動物、豬和其他動物)以及地區(埃及、肯亞、南非和非洲其他地區)進行細分。市場預測以價值(美元)和數量(公噸)表示。

非洲飼料香精和甜味劑市場的趨勢和洞察。

家禽和乳牛飼料的工業化

隨著非洲畜牧飼料生產,特別是家禽和乳牛飼料的工業化,控制偏好和飼料量的重要性日益凸顯。根據美國農業部海外農業局(FAS)2025年的數據,家禽飼料將佔肯亞複合飼料總產量的約41%,乳牛飼料緊追在後,佔39%。這表明,市售複合飼料將主導肯亞的飼料產業。隨著飼料生產商擴大採用標準化複合飼料,對香料和甜味劑的需求也不斷成長。這些添加劑對於確保飼料偏好、促進穩定採食以及提高顆粒飼料和加工飼料的功效至關重要。商業飼料生產的趨勢正在擴大非洲飼料調味劑和甜味劑的市場。

重點在於最佳化飼料攝取量和飼料轉換率。

隨著非洲畜牧養殖戶將飼料攝取量和飼料轉換率作為控制生產成本的首要任務,飼料香精和甜味劑市場正經歷快速成長。美國農業部海外農業局指出,到2025年,飼料成本可能佔肯亞雞肉生產總成本的82%,凸顯了飼料性能在決定農場盈利方面所扮演的關鍵角色。有鑑於此,將飼料香精和甜味劑添加到市售複合飼料中已成為日益成長的趨勢。這些添加劑不僅能提高偏好,還能促進穩定的飼料量,尤其是在加工飼料和飼料中。隨著生產者尋求能夠提高營養利用率和改善生產經濟效益的解決方案,預計非洲商業畜牧業對飼料香精和甜味劑的需求將進一步擴大。

注重成本效益的配方

由於成本考量,非洲飼料香精和甜味劑市場面臨挑戰,畜牧養殖戶在飼料配方中優先考慮必需營養素而非特殊添加劑。根據美國農業部海外農業局(USDA FAS)預測,在2025/26銷售年度,埃及的玉米消費量預計將達到1,580萬噸,主要得益於家禽業的復甦。由於商業性畜牧養殖需要大量的飼料穀物,因此飼料預算的很大一部分都用於作為主要能源來源的原料。這一趨勢限制了對飼料必需添加劑的投入,導致飼料香精和甜味劑的使用率較低,尤其是在那些旨在控制飼料成本並保持生產競爭力的生產者中。

細分市場分析

預計到2025年,非洲飼料香精和甜味劑市場中,香料將佔據94.0%的最大市場佔有率,這反映出該地區畜牧業對提升偏好解決方案的強勁需求。市場動態主要受反芻動物生產系統普及的影響,在這些系統中,飼料香料在確保飼料適口性和採食量穩定方面發揮著至關重要的作用,不受飼料和配方變化的影響。商業飼料生產商擴大在複合飼料中添加調味劑,旨在提高產品一致性和畜牧生產力。這種需求在有組織的飼料分銷管道中尤其明顯,凸顯了配方精準性和採食量控制對畜牧生產力的重要性。

在非洲飼料風味劑和甜味劑市場,甜味劑市場預計在2026年至2031年間以3.0%的複合年成長率(CAGR)高速成長,超過較成熟的風味劑市場。飼料生產商正在探索更廣泛的偏好市場的成長。這一成長主要得益於畜牧業生產的商業化程度不斷提高,以及人們日益重視最佳化飼料攝取量,尤其是在生產面臨挑戰的階段。甜味劑正在幼畜營養管理和特種飼料開闢新的市場,透過提升飼料偏好來提高生產效率。儘管甜味劑的普及程度落後於風味劑(主要是因為許多非洲畜牧系統仍然優先考慮基本營養需求),但飼料生產的逐步現代化正在為甜味劑的進一步市場滲透鋪平道路。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

- 調查方法

第2章:本報告的內容

第3章:執行摘要和主要發現

第4章:主要產業趨勢

- 飼養的動物數量

- 家禽

- 反芻動物

- 豬

- 飼料生產

- 水產養殖

- 家禽

- 反芻動物

- 豬

- 法律規範

- 埃及

- 肯亞

- 南非

- 其他非洲國家

- 價值鍊和通路分析

- 市場促進因素

- 家禽和乳牛飼料的工業化

- 重點在於最佳化飼料量和飼料轉換率

- 替代依賴抗生素的生產力提高方法

- 天然和植物來源偏好的需求

- 穩定熱應激攝取的必要性

- 以非洲自由貿易區(AfCFTA)主導的飼料貿易正式整合。

- 市場限制因素

- 以成本為導向的包容性經濟學

- 替代添加劑和掩味措施

- 外匯波動導致進口成本上升

- 本地生產的甜味劑和糖蜜供應不穩定。

- 波特五力分析

第5章 市場規模與成長預測

- 透過輔助添加劑

- 味道

- 甜味劑

- 動物

- 水產養殖

- 魚

- 蝦

- 其他類型的水產養殖

- 家禽

- 肉雞

- 產蛋母雞

- 其他家禽

- 反芻動物

- 肉牛

- 乳牛

- 其他反芻動物

- 豬

- 其他動物

- 水產養殖

- 按地區

- 埃及

- 肯亞

- 南非

- 其他非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Adisseo France SAS(China National BlueStar(Group)Co., Ltd.)

- Archer Daniels Midland Company

- Kemin Industries, Inc.

- Norel, SA

- Phytobiotics Futterzusatzstoffe GmbH

- Lucta, SA

- Alltech, Inc.

- Innovad NV/SA(Innovad Group)

- Palital Feed Additives BV(Arvesta NV)

- Nutreco NV(SHV Holdings NV)

- dsm-firmenich AG

- Evonik Industries AG

- Cargill, Incorporated

- International Flavors and Fragrances Inc.

- Guilin Layn Natural Ingredients Corp.

第7章 執行長需要思考的關鍵策略問題

According to Mordor Intelligence, the africa feed flavors and sweeteners market was valued at USD 48.39 million in 2025 and is projected to grow from USD 49.83 million in 2026 to USD 57.76 million by 2031 at a CAGR of 3.0% from 2026 to 2031.

This report is Segmented by Sub-Additive (Flavors and Sweeteners), by Animal (Aquaculture, Poultry, Ruminants, Swine, and Other Animals), and by Geography (Egypt, Kenya, South Africa, and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Africa Feed Flavors and Sweeteners Market Trends and Insights

Industrialization of Poultry and Dairy Feed

As Africa's livestock feed production industrializes, particularly in poultry and dairy, the importance of palatability and feed intake management is rising. According to the United States Department of Agriculture (USDA) Foreign Agricultural Service (FAS) in 2025, poultry feed made up roughly 41% of Kenya's total compound feed output, with dairy feed close behind at 39%. This underscores the dominance of commercially formulated feed in Kenya's organized feed industry. With feed manufacturers increasingly adopting standardized compound feed for poultry and dairy, there's a growing demand for flavoring and sweetening additives. These additives are crucial for ensuring feed acceptance, promoting consistent intake, and enhancing the efficacy of pelleted and processed rations. This trend towards commercial feed manufacturing is expanding the market for feed flavors and sweeteners throughout Africa.

Feed Intake and Conversion Ratio Optimization Focus

As livestock producers in Africa prioritize feed intake and conversion efficiency to manage production costs, the market for feed flavors and sweeteners is witnessing a surge. The United States Department of Agriculture Foreign Agricultural Service highlights that by 2025, feed costs in Kenya could constitute a staggering 82% of the total expenses in chicken meat production, underscoring the pivotal role of feed performance in determining farm profitability. In light of this, there is a growing trend of integrating feed flavors and sweeteners into commercial formulations. These additives not only boost palatability but also promote steady feed consumption, especially in processed and pelleted diets. With producers on the lookout for solutions that enhance nutrient utilization and bolster production economics, the demand for feed flavors and sweeteners is poised for growth in Africa's commercial livestock sector.

Cost-Sensitive Inclusion Economics

The feed flavors and sweeteners market in Africa encounters challenges as livestock producers prioritize essential nutritional components over specialty additives in feed formulations due to cost considerations. According to the United States Department of Agriculture Foreign Agricultural Service (USDA FAS), Egypt's corn consumption reached 15.8 million metric tons in the 2025/26 marketing year, driven by a recovery in the poultry sector. With commercial livestock production requiring substantial feed grain inputs, a significant portion of feed budgets is allocated to core energy ingredients. This focus restricts the financial resources available for non-essential additives, limiting the adoption of feed flavors and sweeteners, particularly among producers aiming to control feed costs and sustain competitive production economics.

Other drivers and restraints analyzed in the detailed report include:

- Replacement of Antibiotic-Led Performance Tools

- Natural and Phytogenic Palatability Demand

- Substitute Additives and Flavor Masking Workarounds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Africa feed flavors and sweeteners market share for flavors accounted for the largest 94.0% in 2025, reflecting the strong preference for palatability enhancement solutions in the region's livestock sector. The market dynamics are shaped by the prevalence of ruminant production systems, where feed flavors play a pivotal role in ensuring feed acceptance and consistent intake, regardless of forage and ration variations. Commercial feed manufacturers are increasingly infusing flavoring solutions into their compound feeds, aiming to boost product consistency and enhance animal performance. Demand is particularly pronounced in organized feed channels, emphasizing the significance of formulation precision and intake management for livestock productivity.

The Africa feed flavors and sweeteners market size for sweeteners is projected to grow at the fastest CAGR of 3.0% from 2026 to 2031, outpacing the more mature flavor segment as feed producers explore broader palatability strategies. The surge is bolstered by the rising commercialization of livestock production and heightened awareness regarding feed intake optimization, especially during challenging production phases. Sweeteners are carving a niche in young animal nutrition and specialized feed applications, where their role in enhancing feed acceptance can drive production efficiency. While their uptake lags behind flavors-primarily because many African livestock systems still emphasize fundamental nutritional needs-the gradual modernization of feed manufacturing is paving the way for deeper market penetration.

Complete Report Scope:

- By Sub-Additive

- Flavors

- Sweeteners

- By Animal

- Aquaculture

- Fish

- Shrimp

- Other Aquaculture Species

- Poultry

- Broiler

- Layer

- Other Poultry Birds

- Ruminants

- Beef Cattle

- Dairy Cattle

- Other Ruminants

- Swine

- Other Animals

- Aquaculture

- By Geography

- Egypt

- Kenya

- South Africa

- Rest of Africa

List of Companies Covered in this Report:

- Adisseo France SAS (China National BlueStar (Group) Co., Ltd.)

- Archer Daniels Midland Company

- Kemin Industries, Inc.

- Norel, S.A.

- Phytobiotics Futterzusatzstoffe GmbH

- Lucta, S.A.

- Alltech, Inc.

- Innovad NV/SA (Innovad Group)

- Palital Feed Additives B.V. (Arvesta NV)

- Nutreco N.V. (SHV Holdings N.V.)

- dsm-firmenich AG

- Evonik Industries AG

- Cargill, Incorporated

- International Flavors and Fragrances Inc.

- Guilin Layn Natural Ingredients Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Animal Headcount

- 4.1.1 Poultry

- 4.1.2 Ruminants

- 4.1.3 Swine

- 4.2 Feed Production

- 4.2.1 Aquaculture

- 4.2.2 Poultry

- 4.2.3 Ruminants

- 4.2.4 Swine

- 4.3 Regulatory Framework

- 4.3.1 Egypt

- 4.3.2 Kenya

- 4.3.3 South Africa

- 4.3.4 Rest of Africa

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Industrialization of poultry and dairy feed

- 4.5.2 Feed intake and conversion ratio optimization focus

- 4.5.3 Replacement of antibiotic-led performance tools

- 4.5.4 Natural and phytogenic palatability demand

- 4.5.5 Heat-stress intake stabilization needs

- 4.5.6 African Continental Free Trade Area (AfCFTA)-led formal feed trade integration

- 4.6 Market Restraints

- 4.6.1 Cost-sensitive inclusion economics

- 4.6.2 Substitute additives and flavor masking workarounds

- 4.6.3 FX-driven import cost inflation

- 4.6.4 Local sweetener and molasses supply unreliability

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Sub-Additive

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 By Animal

- 5.2.1 Aquaculture

- 5.2.1.1 Fish

- 5.2.1.2 Shrimp

- 5.2.1.3 Other Aquaculture Species

- 5.2.2 Poultry

- 5.2.2.1 Broiler

- 5.2.2.2 Layer

- 5.2.2.3 Other Poultry Birds

- 5.2.3 Ruminants

- 5.2.3.1 Beef Cattle

- 5.2.3.2 Dairy Cattle

- 5.2.3.3 Other Ruminants

- 5.2.4 Swine

- 5.2.5 Other Animals

- 5.2.1 Aquaculture

- 5.3 By Geography

- 5.3.1 Egypt

- 5.3.2 Kenya

- 5.3.3 South Africa

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Adisseo France SAS (China National BlueStar (Group) Co., Ltd.)

- 6.4.2 Archer Daniels Midland Company

- 6.4.3 Kemin Industries, Inc.

- 6.4.4 Norel, S.A.

- 6.4.5 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.6 Lucta, S.A.

- 6.4.7 Alltech, Inc.

- 6.4.8 Innovad NV/SA (Innovad Group)

- 6.4.9 Palital Feed Additives B.V. (Arvesta NV)

- 6.4.10 Nutreco N.V. (SHV Holdings N.V.)

- 6.4.11 dsm-firmenich AG

- 6.4.12 Evonik Industries AG

- 6.4.13 Cargill, Incorporated

- 6.4.14 International Flavors and Fragrances Inc.

- 6.4.15 Guilin Layn Natural Ingredients Corp.