|

市場調查報告書

商品編碼

2073110

南美洲飼料香精和甜味劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)South America Feed Flavors and Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

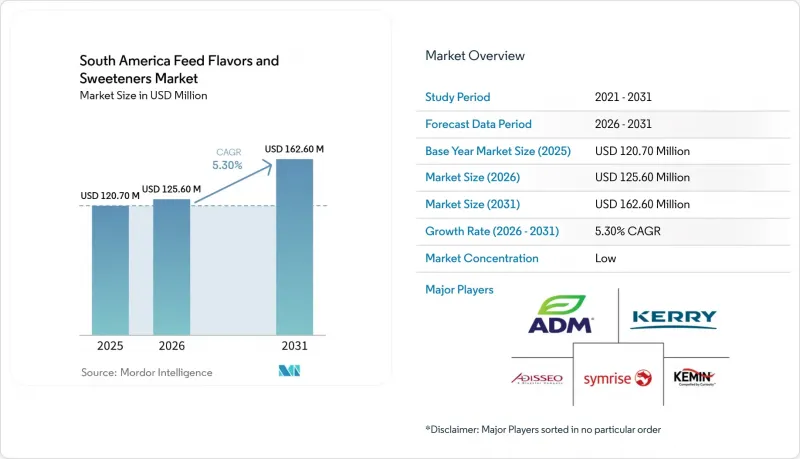

據 Mordor Intelligence 稱,2025 年南美飼料香精和甜味劑市場價值為 1.207 億美元,預計到 2031 年將達到 1.626 億美元,而 2026 年為 1.256 億美元,在預測期(2026-2031 年)內複合年成長率為 5. 5.30%。

本報告按子類型(香料和甜味劑)、動物種類(反芻動物、豬和其他動物種類)以及地區(巴西、智利、阿根廷和其他南美國家)進行細分。市場預測以價值(美元)和數量(公噸)表示。

南美飼料風味劑和甜味劑市場的趨勢和洞察。

出口主導的豬肉產量成長

作為全球最大的肉類出口國之一,同時也是主要的豬肉出口國,巴西為南美飼料風味劑和甜味劑市場提供了堅實的銷售量基礎。根據巴西動物蛋白協會(ABPA)預測,2025年,巴西豬肉出口量預計將達到150萬噸,較2024年增加11.6%,出口收入將增加至36.19億美元。在如此龐大的規模下,風味劑和甜味劑仍然是綜合生產商和合約農民日常配方中不可或缺的一部分,因為穩定的飼料攝取量對商業性至關重要。此外,隨著巴西進軍競爭日益激烈的出口市場,人們越來越關注符合已批准的添加劑和殘留標準的產品配方,這推動了感官添加劑而非傳統飼料增味劑的應用。

巴西及周邊地區商業飼料生產的擴張

根據Alltech Agri Food Statistics的數據,預計到2025年,南美洲的複合飼料產量將達到2.04446億噸,年增2.8%,其中巴西的產量將達到8,990.4萬噸。由於大部分複合飼料的加工都是在飼料廠進行,因此生產基地的擴張將拓寬南美洲飼料香精和甜味劑的潛在市場。大規模飼料廠加工能力的提升也提高了複雜偏好管理系統的經濟效益,因為固定添加劑和服務成本可以分攤到更大的產量上。雖然局部小規模的次區域市場出現了局部波動,但巴西和南錐體地區提供了大部分的穩定性。因此,區域分銷網路覆蓋範圍和本地技術支援將是南美洲飼料香精和甜味劑市場的關鍵競爭優勢。

飼料廠的分散化將減緩優質添加劑的普及。

南美飼料香精和甜味劑市場仍然由分散的飼料製造地運營,這些基地與大型一體化蛋白質公司各自獨立運作。中小規模飼料廠往往對價格較為敏感,且通常缺乏能力對高階感官評估系統進行系統性的檢驗測試。因此,即使飼料總產量龐大,高規格產品的實際目標市場也會縮小。此外,由於客戶分散在眾多小規模客戶中,供應商每噸產品的技術服務成本也會更高。因此,高級產品在南美飼料香精和甜味劑市場的部分地區,尤其是在巴西生產群集以外的地區,滲透速度較為緩慢。

細分市場分析

香精是最大的細分市場,預計到2025年將佔據南美飼料香精和甜味劑市場82.1%的佔有率,並廣泛應用於該地區豬和反芻動物的飼料中。其主導地位反映了香精能夠應對的諸多挑戰,包括掩蓋苦味成分、提高初期飼餵時的適口性以及在高產生產系統中提高採食量。此外,香精既適用於大規模一體化飼料方案,也適用於更標準化的預混合料配方,這支撐了南美飼料香精和甜味劑市場的持續需求。這種廣泛的適用性使得香精類別在結構上難以被取代,即使其他類型的解決方案有所改進也無濟於事。

甜味劑仍然是成長最快的細分市場,預計從2026年到2031年將以4.3%的複合年成長率成長。最大的驅動力是仔豬斷奶飼料,其採食量的增加直接影響仔豬的早期生長和飼料轉換率。 ADM的「SUCRAM」和安迪甦的「Optisweet」表明,供應商正在開發針對特定應用場景的技術解決方案,而不是簡單地將甜味劑定位為通用的增味劑。儘管整個風味劑行業的市場價值更高,但這種策略使甜味劑在南美飼料風味劑和甜味劑市場中呈現出更清晰的成長軌跡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章:主要產業趨勢

- 動物族群分析

- 反芻動物

- 豬

- 飼料生產分析

- 反芻動物

- 豬

- 法律規範

- 價值鍊和通路分析

- 市場促進因素

- 出口主導的豬肉生產擴張

- 巴西及周邊地區商業飼料供應的擴張

- 增加仔豬和幼畜飼料中甜味劑的使用量

- 人們越來越關注飼料轉換率和牲畜的營養狀況。

- 植物性蛋白質和替代成分的普及增加了對掩味劑的需求。

- 逐步淘汰抗菌劑導致人們對配方改良的需求增加,這些改良配方既能改善感官特性,又能維持攝取量。

- 市場限制因素

- 飼料廠的分散化正在減緩優質添加劑的廣泛應用。

- 關於感官添加劑,向農業、畜牧業和供應部 (MAPA) 註冊和遵守規定的複雜性。

- 由於外匯波動,進口微型元件的成本正在增加。

- 感染疾病和出口限制正在擾亂添加劑的採購模式。

第5章 市場規模與成長預測

- 按類型

- 味道

- 甜味劑

- 依動物類型

- 反芻動物

- 牛

- 牛

- 其他反芻動物

- 豬

- 其他動物類型

- 反芻動物

- 按地區

- 巴西

- 阿根廷

- 智利

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ADM

- Kerry Group plc

- Symrise AG

- BlueStar Adisseo Company

- Kemin Industries, Inc.

- dsm-firmenich AG

- Alltech

- Lucta, SA

- Prinova Group LLC

- Novonesis

- Cargill, Incorporated

- Phytobiotics Futterzusatzstoffe GmbH

- Norel, SA

- Orffa(Marubeni Corporation)

- BioAromas do Brasil

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america feed flavors and sweeteners market size was valued at USD 120.70 million in 2025 and estimated to grow from USD 125.60 million in 2026 to reach USD 162.60 million by 2031, at a CAGR of 5.30% during the forecast period (2026-2031).

This report is Segmented by Sub Type (Flavors and Sweeteners), by Animal Type (Ruminants, Swine, and Other Animal Type), and by Geography (Brazil, Chile, Argentina, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

South America Feed Flavors and Sweeteners Market Trends and Insights

Export-Led Pork Production Growth

Brazil's role as one of the world's largest meat exporter and a leading pork exporter creates a strong volume base for the South America feed flavors and sweeteners market. According to the Brazilian Association of Animal Protein (ABPA), Brazil's pork exports reached 1.5 million metric tons in 2025, up 11.6% from 2024, and export revenue rose to USD 3.619 billion. At that scale, stable feed intake is commercially important, so flavors and sweeteners remain part of the routine formulation toolkit for integrated producers and contract growers. Brazil's push into demanding export markets also raises attention to approved additives and residue-compliant formulations, which support sensory additive adoption over older intake-support tools.

Commercial Feed Volume Expansion Across Brazil and the Broader Region

South America produced 204.446 million metric tons of compound feed in 2025, up 2.8% year over year, and Brazil alone accounted for 89.904 million metric tons according to Alltech Agri Food Statistics. This wider production base expands the addressable market for South America feed flavors and sweeteners, as most inclusions occur at the feed mill level. Higher throughput at larger mills also improves the economics of precision palatability systems, since fixed application and service costs are spread across more tonnage. Brazil and the Southern Cone carried much of that stability, even as smaller subregional markets saw localized disruption. That makes regional distribution coverage and local technical support important competitive tools in the South America feed flavors and sweeteners market.

Fragmented Feed-Mill Base Slows Premium Additive Penetration

The South America feed flavors and sweeteners market still operates through a widely dispersed feed manufacturing base outside the largest integrated protein companies. Smaller and mid-sized mills are often more price-sensitive and less able to run structured validation trials for premium sensory systems. That reduces the practical addressable market for high-specification products even when headline feed volume is large. Suppliers also face higher technical service costs per ton when accounts are scattered across many smaller customers. The result is slower premium penetration across parts of the South America feed flavors and sweeteners market, especially outside Brazil's production clusters.

Other drivers and restraints analyzed in the detailed report include:

- Higher Use of Sweeteners in Piglet and Young-Animal Diets

- Reformulation Toward Alternative Protein Sources Increases Demand for Palatability Solutions

- Ministry of Agriculture, Livestock and Supply (MAPA) Registration and Compliance Complexity for Sensory Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flavors hold the largest segment, captured 82.1% of the South America feed flavors and sweeteners market share in 2025, confirming their widespread use across swine, and ruminant diets in the region. Their leading position reflects the broad set of problems they address, including masking bitter raw materials, improving first-feed acceptance, and supporting intake in high-performance production systems. Flavors also fit well into both large integrated feed programs and more standardized premix-based formulations, which supports repeat demand in the South America feed flavors and sweeteners market. This breadth makes the flavor category structurally harder to displace, even as adjacent solution types improve.

Sweeteners remain the fastest-growing segment, projected to expand at a 4.3% CAGR through 2026 to 2031. The strongest pull comes from piglet weaning diets, where intake support directly affects early growth and feed conversion. ADM's SUCRAM and Adisseo's Optisweet demonstrate the way suppliers have developed technical solutions tailored to specific use cases, rather than positioning sweeteners solely as general flavor enhancers. This approach provides sweeteners with a more defined growth trajectory within the South America feed flavors and sweeteners market, despite flavors maintaining a higher overall market value.

Complete Report Scope:

- By Type

- Flavors

- Sweeteners

- By Animal Type

- Ruminants

- Beef Cattle

- Dairy Cattle

- Other Ruminants

- Swine

- Other Animal Type

- Ruminants

- By Geography

- Brazil

- Argentina

- Chile

- Rest of South America

List of Companies Covered in this Report:

- ADM

- Kerry Group plc

- Symrise AG

- BlueStar Adisseo Company

- Kemin Industries, Inc.

- dsm-firmenich AG

- Alltech

- Lucta, S.A.

- Prinova Group LLC

- Novonesis

- Cargill, Incorporated

- Phytobiotics Futterzusatzstoffe GmbH

- Norel, S.A.

- Orffa (Marubeni Corporation)

- BioAromas do Brasil

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trends

- 4.1 Animal Headcount Analysis

- 4.1.1 Ruminants

- 4.1.2 Swine

- 4.2 Feed Production Analysis

- 4.2.1 Ruminants

- 4.2.2 Swine

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Export-led pork production growth

- 4.5.2 Commercial feed volume expansion across Brazil and the broader region

- 4.5.3 Higher use of sweeteners in piglet and young-animal diets

- 4.5.4 Increasing focus on feed efficiency and animal nutrition outcomes

- 4.5.5 Reformulation toward plant-protein and alternative raw materials increases masking needs

- 4.5.6 Antimicrobial phaseout raises demand for intake-preserving sensory reformulation

- 4.6 Market Restraints

- 4.6.1 Fragmented feed-mill base slows premium additive penetration

- 4.6.2 Ministry of Agriculture, Livestock and Supply (MAPA) registration and compliance complexity for sensory additives

- 4.6.3 Currency volatility raises the cost of imported micro-ingredients

- 4.6.4 Disease outbreaks and export restrictions disrupt additive purchasing patterns

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 By Animal Type

- 5.2.1 Ruminants

- 5.2.1.1 Beef Cattle

- 5.2.1.2 Dairy Cattle

- 5.2.1.3 Other Ruminants

- 5.2.2 Swine

- 5.2.3 Other Animal Type

- 5.2.1 Ruminants

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ADM

- 6.4.2 Kerry Group plc

- 6.4.3 Symrise AG

- 6.4.4 BlueStar Adisseo Company

- 6.4.5 Kemin Industries, Inc.

- 6.4.6 dsm-firmenich AG

- 6.4.7 Alltech

- 6.4.8 Lucta, S.A.

- 6.4.9 Prinova Group LLC

- 6.4.10 Novonesis

- 6.4.11 Cargill, Incorporated

- 6.4.12 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.13 Norel, S.A.

- 6.4.14 Orffa (Marubeni Corporation)

- 6.4.15 BioAromas do Brasil