|

市場調查報告書

商品編碼

2073330

北美飼料香精和甜味劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)North America Feed Flavors and Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

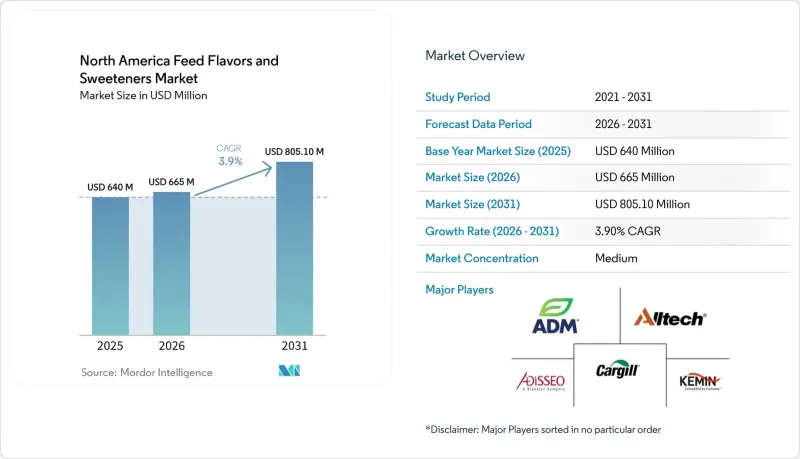

根據 Mordor Intelligence 預測,北美飼料香精和甜味劑市場規模預計在 2025 年將達到 6.4 億美元,在 2026 年將達到 6.65 億美元。

此外,預計到預測期結束時將達到 8.051 億美元,並預計從 2026 年到 2031 年將以 3.9% 的複合年成長率成長。

本報告按類型(香料和甜味劑)、牲畜(豬、反芻動物及其他)和國家(美國、加拿大和墨西哥)進行細分。市場預測以價值(美元)和數量(公噸)表示。

北美飼料香精和甜味劑市場趨勢及洞察

提高複合飼料產量並擴大飼料廠規模

工業飼料生產持續推動北美飼料風味劑和甜味劑市場朝向更廣泛、更穩定的需求基礎邁進。根據Alltech飼料調查,墨西哥的複合飼料產量預計在2024年至2025年間增加2%,自2020年以來增加7.7%,顯示豬飼料產量將大幅增加。此外,加拿大擁有429家商業飼料廠,年加工量達2,890萬噸,為市場提供了堅實的基礎。如此規模使得工廠層級能夠進行系統化的添加劑採購。隨著透過商業系統分銷的飼料比例相對於農場間混合飼料的比例不斷增加,採購決策也變得更加集中和技術化。這有利於那些能夠提供穩定供應鏈、應用支援以及跨多個畜種持續供應的供應商。此外,一旦產品被納入飼料廠的規格和性能記錄,就很難替換已建立的方案。這種營運結構持續支撐著北美飼料風味劑和甜味劑市場的成長,因為商業飼料廠大規模採購並尋求適用於標準化飼料生產的添加劑。

減少抗生素使用計劃正在推高對飼料促效劑添加劑的需求。

抗生素減量計畫正在提升商業飼料中風味劑和甜味劑的功能性作用。隨著抗生素生長促進劑使用量的減少,生產者越來越依賴提高早期飼料的偏好來維持採食量和日增重。這在仔豬和幼齡反芻動物的飼養中尤其重要,因為食慾下降會立即影響其生產性能和健康。香料和甜味劑如今已不再被視為可有可無的添加劑,而是被視為促進飼料量的重要工具。此外,大規模的豬飼料研究表明,植物來源添加劑系統可以在維持豬隻生產性能的同時減少對抗生素的依賴,這進一步凸顯了提高偏好的重要性。因此,合理使用抗生素是北美飼料香料和甜味劑市場的主要驅動力。

監管審查和原料核准流程變得越來越冗長。

在北美飼料香精和甜味劑市場,監管審查仍然是限制新產品市場擴張速度的一大阻礙因素。為動物開發的新型香精和高濃度甜味劑通常需要經過漫長的核准流程,這些流程依據的是《美國聯邦法規》第21篇第573部分及其相關的成分定義程序。中小企業受到的影響尤其嚴重,因為在產品上市之前,合規性需要投入大量可用資金。這種情況往往有利於擁有充足財力和專門的合規團隊的大型企業。此外,與人類食品領域的類似進展相比,飼料香精和甜味劑領域的新產品推廣速度也相對較慢。北美飼料香精和甜味劑市場依賴已通過核准的成分,而漫長的審查週期阻礙了產品系列的創新,從而構成了一項重大限制。

細分市場分析

預計到2025年,調味料將繼續主導北美飼料調味劑和甜味劑市場,佔82.2%的佔有率。如此高的市場佔有率反映了其在反芻動物和豬飼料中的常規使用,在這些飼料中,調味劑對於掩蓋不良氣味和確保穩定的飼料量至關重要。調味料是市售飼料配方中不可或缺的成分,其需求主要來自常規配方,而非偶爾的特殊用途。這種持續的使用使得調味劑成為北美飼料調味劑和甜味劑市場中標準和高階飼料飼料的核心成分。

預計2026年至2031年間,甜味劑的複合年成長率將達5.8%,超過香精。這種加速成長主要歸功於甜味劑在敏感飼料中的重要作用,尤其是在飼餵初期、過渡期飼料以及含有苦味活性物質的配方中,提高飼料量至關重要。此外,甜味劑在含有減甲烷成分的牛飼料以及仔豬飼料中也日益重要,因為飼料的偏好直接影響生產性能。因此,儘管香精仍然是北美飼料香精和甜味劑市場最大的細分市場,但甜味劑正在成為推動市場成長的主要動力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 美國、加拿大和墨西哥的複合飼料加工量增加,飼料廠規模擴大。

- 減少抗生素使用計劃增加了對飼料添加劑的需求。

- 消費者對優質肉類和乳製品的需求不斷成長,對偏好的要求也越來越高。

- 潔淨標示和在優質飼料。

- 精準飼餵和人工智慧驅動的採食量監測可提高偏好和投資回報率可見度。

- 透過取代蛋白質、產品特定配方和減少甲烷的飼料。

- 市場限制因素

- 監管審查和原料核准流程變得越來越冗長。

- 對飼料配製公司和綜合企業的成本成長和投資報酬率進行審查

- 由於 FDA 和 AAFCO 框架的變化,原料過渡存在不確定性。

- 柑橘和糖蜜用量的波動會影響調味料和甜味劑的經濟效益。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 味道

- 甜味劑

- 動物

- 豬

- 反芻動物

- 乳牛

- 肉牛

- 其他

- 其他

- 國家

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cargill, Incorporated

- ADM

- Kemin Industries Inc.

- Alltech

- Adisseo

- Prinova Group LLC

- AFB International

- DSM-Firmenich AG

- Kerry Group

- International Flavors & Fragrances Inc.

- Phytobiotics Futterzusatzstoffe GmbH

- Norel SA

- Novonesis

- Canadian Bio-Systems Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america feed flavors and sweeteners market was valued at USD 640 million in 2025, projected to be USD 665 million by 2026, and is estimated to reach USD 805.1 million by the end of the forecast period, growing at a CAGR of 3.9% from 2026 to 2031.

This report is Segmented by Type (Flavors and Sweeteners), by Livestock (Swine, Ruminants, and Others), and by Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Feed Flavors and Sweeteners Market Trends and Insights

Higher Compound Feed Throughput and Feed Mill Scale

Industrial feed output continues to drive the North American feed flavors and sweeteners market toward a wider, more stable demand base. According to the Alltech Feed Survey, Mexico's compound feed output increased by 2% from 2024 to 2025 and had expanded by 7.7% since 2020, indicating that the country is adding real volume to swine feed manufacturing. Additionally, Canada also provides a solid base through 429 commercial feed mills that process 28.9 million metric tons annually, and that scale supports organized additive procurement at the mill level. As more feed moves through commercial systems rather than on-farm mixing, purchasing decisions become more centralized and more technical. That favors suppliers that can offer stable delivery forms, application support, and consistent supply across multiple species. It also makes established programs harder to replace once a product is built into mill specifications and performance records. This operating structure continues to support growth in the North America feed flavors and sweeteners market because commercial mills buy at scale and seek additives that fit standardized feed production.

Antibiotic-Reduction Programs Increasing Demand for Intake-Support Additives

Antibiotic reduction programs are enhancing the functional role of flavors and sweeteners in commercial feed. With the reduction of antibiotic growth promoters, producers increasingly rely on improved feed acceptance in early-life diets to maintain intake and daily weight gain. This is particularly critical in nursery swine and young ruminant programs, where reduced appetite can quickly impact performance and health outcomes. Flavors and sweeteners are now viewed as essential tools for supporting feed intake rather than optional enhancements. Additionally, large-scale swine studies have demonstrated that plant-based additive systems can reduce antibiotic dependence while maintaining pig performance, further emphasizing the importance of palatability support. As a result, antibiotic stewardship has become a key driver for the North America feed flavors and sweeteners market.

Lengthy Regulatory Review and Ingredient Approval Pathways

Regulatory review continues to be a significant constraint on the pace at which new products can scale in the North America feed flavors and sweeteners market. Novel flavor actives and high-intensity sweeteners for animal use often face extended approval processes under 21 CFR Part 573 and related ingredient-definition procedures. Smaller companies are disproportionately affected, as regulatory compliance can consume a substantial portion of their available investment before commercial launch. This dynamic tends to favor larger companies with greater financial resources and dedicated regulatory teams. Additionally, it delays the introduction of newer masking and sweetening systems compared to similar advancements in human food. This remains a notable limitation, as the North America feed flavors and sweeteners market relies on approved ingredients, and prolonged review timelines hinder portfolio innovation.

Other drivers and restraints analyzed in the detailed report include:

- Premium Meat, and Dairy Requirements Lifting Palatability Standards

- Clean-Label and Natural Additive Adoption in Premium Feed

- Cost Inflation and ROI (Return on Investment) Scrutiny Among Feed Formulators and Integrators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flavors accounted for 82.2% of the North American feed flavors and sweeteners market in 2025, maintaining a dominant position. This significant share reflects their routine use across ruminant and swine feeds, where they are essential for masking undesirable odors and ensuring consistent feed intake. Flavors are an integral part of commercial feed formulations, with their demand driven by regular inclusion rather than occasional specialty use. This consistent utilization positions flavors as a core component of both standard compound feed and premium formulations in the North American feed flavors and sweeteners market.

Sweeteners are projected to grow at a CAGR of 5.8% from 2026 to 2031, outpacing flavors. This accelerated growth is attributed to their role in sensitive diets where stimulating feed intake is critical, particularly in early-life feeding, transition diets, and formulations containing bitter-tasting bioactives. Sweeteners are also gaining importance in dairy rations that incorporate methane-reduction ingredients and in nursery swine diets, where feed acceptance directly impacts performance. Consequently, while flavors remain the largest segment, sweeteners are emerging as the primary growth driver in the North American feed flavors and sweeteners market.

Complete Report Scope:

- By Type

- Flavors

- Sweeteners

- By Animal

- Swine

- Ruminants

- Dairy Cattle

- Beef Cattle

- Others

- Others

- By Country

- United States

- Canada

- Mexico

- Rest of North America

List of Companies Covered in this Report:

- Cargill, Incorporated

- ADM

- Kemin Industries Inc.

- Alltech

- Adisseo

- Prinova Group LLC

- AFB International

- DSM-Firmenich AG

- Kerry Group

- International Flavors & Fragrances Inc.

- Phytobiotics Futterzusatzstoffe GmbH

- Norel S.A.

- Novonesis

- Canadian Bio-Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Higher compound feed throughput and feed mill scale in the United States, Canada, and Mexico

- 4.2.2 Antibiotic-reduction programs increasing demand for intake-support additives

- 4.2.3 Premium meat, and dairy requirements lifting palatability standards

- 4.2.4 Clean-label and natural additive adoption in premium feed

- 4.2.5 Precision feeding and AI-based intake monitoring improving palatability ROI visibility

- 4.2.6 Taste-masking demand from alternative proteins, by-products, and methane-reduction rations

- 4.3 Market Restraints

- 4.3.1 Lengthy regulatory review and ingredient approval pathways

- 4.3.2 Cost inflation and ROI scrutiny among feed formulators and integrators

- 4.3.3 Ingredient transition uncertainty under evolving FDA and AAFCO frameworks

- 4.3.4 Citrus and molasses input volatility affecting flavor and sweetener economics

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 By Animal

- 5.2.1 Swine

- 5.2.2 Ruminants

- 5.2.2.1 Dairy Cattle

- 5.2.2.2 Beef Cattle

- 5.2.2.3 Others

- 5.2.3 Others

- 5.3 By Country

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

- 5.3.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cargill, Incorporated

- 6.4.2 ADM

- 6.4.3 Kemin Industries Inc.

- 6.4.4 Alltech

- 6.4.5 Adisseo

- 6.4.6 Prinova Group LLC

- 6.4.7 AFB International

- 6.4.8 DSM-Firmenich AG

- 6.4.9 Kerry Group

- 6.4.10 International Flavors & Fragrances Inc.

- 6.4.11 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.12 Norel S.A.

- 6.4.13 Novonesis

- 6.4.14 Canadian Bio-Systems Inc.