|

市場調查報告書

商品編碼

2073210

中東飼料香精和甜味劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East Feed Flavors and Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

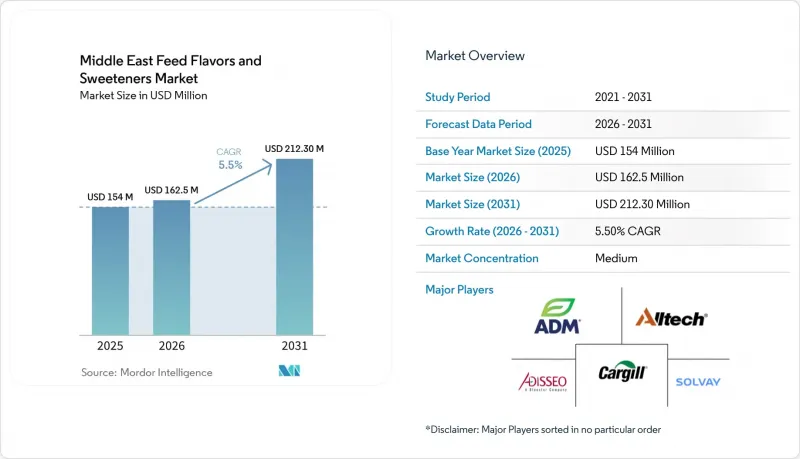

根據 Mordor Intelligence 預測,中東飼料香精和甜味劑市場規模預計將在 2025 年達到 1.54 億美元,從 2026 年的 1.625 億美元成長到 2031 年的 2.123 億美元,在 2026 年至 2031 年期間的複合年成長率為 5.5%。

本報告按類型(香料和甜味劑)、動物(反芻動物、豬和其他動物)和國家(伊朗、沙烏地阿拉伯和其他中東國家)進行細分。市場預測以價值(美元)和數量(公噸)表示。

中東飼料風味劑和甜味劑市場的趨勢和洞察。

商業動物飼料對提高偏好的需求日益成長。

該地區的商業飼料生產正從基礎商品混合飼料轉向營養豐富、性能導向的配方,導致飼料配方中感官添加劑的使用量增加。飼料廠正在添加香精和甜味劑以維持飼料量,因為飼料會影響飼料轉換率,並推高肉類和乳製品的生產成本。在沙烏地阿拉伯,偏好已成為大規模家禽和酪農系統中飼料配方的標準組成部分,不再僅被視為一種可選添加劑。根據Alltech Feed發布的2026年調查報告,全球複合飼料產量將在2025年達到14億噸。報告也指出,中東地區的飼料生產面臨疾病威脅和原料波動等挑戰,因此穩定的飼料量對生產者至關重要。在現代化的飼料廠中,連續混合和精確計量提高了低濃度特種成分的穩定性,進一步提升了這些添加劑的價值。因此,中東飼料香精和甜味劑市場受益於飼料需求的成長以及高品質添加劑使用技術條件的改善。這一趨勢促進了重複購買,因為隨著飼料輔助系統被納入標準飼料配方,飼料生產商越來越傾向於將其從市售配方中剔除。

擴大家禽和反芻動物飼料生產

沙烏地阿拉伯和伊朗畜牧業產量的成長推動了對添加香料和甜味劑的複合飼料的需求不斷成長。在反芻動物領域,沙烏地阿拉伯計畫在2026年11月前逐步淘汰多年生飼料,預計將增加對商品飼料和全混合日糧(TMR)的依賴,從而進一步刺激對添加劑的需求,以掩蓋青貯飼料和複合飼料特有的異味。伊朗也憑藉其龐大的牛和強大的家禽業(得益於國內飼料生產能力的支持)推動了這一趨勢。 2026年,沙烏地阿拉伯和俄羅斯簽署了13項畜牧業協議(總額達48億沙烏地里亞爾,約13億美元),進一步證明雙方持續致力於加強整個價值鏈的蛋白質生產能力。隨著家禽和反芻動物飼料消耗量的增加,中東飼料調味劑和甜味劑市場受益於基於穩定採食量的商業複合飼料規模的擴大。

對進口特種原料的依賴

在該地區,先進的飼料風味和甜味劑系統高度依賴進口特殊原料。天然風味基底、包埋偏好增強劑和活性甜味劑等關鍵成分主要來自歐洲、美國和亞洲,而非在國內生產。這種依賴性使飼料生產商面臨多重成本壓力,包括運費、外匯波動和採購週期延長。 2026年初,霍爾木茲海峽附近日益緊張的軍事局勢迫使主要航運公司暫停在波斯灣的運營,導致飼料添加劑的交付嚴重延誤,這一問題尤為突出。此外,法規核准流程也阻礙了緊急替代方案的引進。註冊和跨境核准程序通常耗時過長,難以應對迫在眉睫的供不應求。因此,中東飼料風味和甜味劑市場存在結構性脆弱性,需求保持穩定,但產品供應可能突然變得緊張。這種依賴也限制了小規模買家的定價柔軟性。這是因為與大規模、一體化的客戶相比,小規模的買家通常缺乏維持庫存和確保有利物流條件的能力。

細分市場分析

預計到2025年,中東飼料香精和甜味劑市場中,香精將持續保持主導地位,佔82.2%的市場。這一主導地位主要歸功於香精系統在肉雞幼畜飼料飼料、育成雞飼料以及牛全混合日糧(TMR)中的廣泛應用。這些香精有助於掩蓋原料特性的差異,並維持飼料偏好性的一致性。此外,在許多家禽和酪農養殖場,香精的使用通常已納入標準飼料配方。 Adiseo在中東和非洲的2025年牛營養夥伴關係計畫強調了牛精準營養和可靠採食量之間日益成長的平衡需求,這將進一步推動香精系統在控制飼餵方案中的應用。然而,由於飼料生產商越來越傾向於使用低劑量、高效力的香精系統,以在降低添加劑用量的同時達到類似的感官效果,供應商面臨挑戰。

預計到2031年,甜味劑市場將以4.3%的複合年成長率成長。儘管目前市場規模較小,但預計它將成為成長最快的細分市場。這一成長主要受歐洲進口飼料添加劑無糖精製趨勢的推動,而歐盟法規2024/1727的實施進一步促進了這一趨勢。該法規要求複合飼料必須在2026年7月前符合相關規定。歐洲食品安全局(EFSA)2025年對天然甜味劑(NHDC)的安全評估進一步明確了糖精替代品的發展方向。 Phytobiotics和ADM等公司正在將無糖精替代品推向市場,這些替代品採用天然來源或受體靶向的甜味劑系統。由於這一轉變是由進口飼料配方的變化而非當地法規所驅動,因此中東飼料風味劑和甜味劑市場的經銷商不得不先核實替代甜味劑系統的合格,才能在其供應商的配方中實施大規模變更。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 市場對提高飼料偏好的需求日益成長。

- 擴大家禽和反芻動物飼料生產

- 過渡到無抗生素飼料方案

- 擴大現代飼料生產能力

- 擴大天然飼料原料的使用

- 畜牧營養中的熱應激管理

- 市場限制因素

- 對進口特種原料的依賴

- 小規模飼料生產商的價格敏感性

- 缺乏本地配方和測試基礎設施

- 供應鏈中斷和貿易波動

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 味道

- 甜味劑

- 動物

- 豬

- 反芻動物

- 牛

- 牛

- 其他

- 其他

- 國家

- 伊朗

- 沙烏地阿拉伯

- 其他中東國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Solvay SA

- ADM

- Adisseo

- Alltech, Inc.

- Arvesta(Palital Feed Additives BV)

- Cargill, Inc.

- Innov Ad NV/SA

- Phytobiotics Futterzusatzstoffe GmbH

- Prinova Group LLC

- AFB International, Inc.

- CJ CheilJedang Corporation

- Orffa International Holding BV

- Amlan International

- Dr. Eckel Animal Nutrition GmbH and Co. KG

- Symrise AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east feed flavors and sweeteners market was USD 154.0 million in 2025 and projected to grow from USD 162.5 million in 2026 to USD 212.3 million by 2031, registering a CAGR of 5.5% during the period from 2026 to 2031.

This report is Segmented by Type (Flavors and Sweeteners), by Animal (Ruminants, Swine, and Other Animals), and by Country (Iran, Saudi Arabia, and the Rest of the Middle East). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Middle East Feed Flavors and Sweeteners Market Trends and Insights

Rising Demand for Palatability Enhancement in Commercial Feed

Commercial feed production in the region is transitioning from basic commodity-style blends to denser, performance-oriented rations, leading to increased use of sensory additives in formulations. Feed mills incorporate flavors and sweeteners to maintain feed intake, as feed refusal negatively impacts conversion efficiency and raises the cost of producing meat and milk. In Saudi Arabia, large poultry and dairy systems already consider palatability as a standard component of feed formulation rather than an optional addition. According to the Alltech Feed survey 2026, global compound feed production reached 1.4 billion metric tons in 2025. The report also highlighted that Middle East feed output faces challenges, including disease pressure and raw material variability, making stable feed intake critical for producers. The value of these additives is further enhanced in modern mills, where continuous mixing and precise dosing improve the consistency of low-inclusion specialty ingredients. Consequently, the Middle East feed flavors and sweeteners market is benefiting from both increased feed demand and improved technical conditions for the use of premium additives. This trend fosters repeat purchasing behavior, as once intake-support systems are integrated into standard feed specifications, mills are less inclined to remove them from commercial formulations.

Growth in Poultry and Ruminant Feed Production

Increasing livestock production in Saudi Arabia and Iran is driving higher demand for compound feed incorporating flavors and sweeteners. On the ruminant side, the planned cessation of perennial forage cultivation in Saudi Arabia by November 2026 is anticipated to increase reliance on commercial feed and total mixed rations, thereby intensifying the need for additives to mask silage and formulation off-notes. Iran also contributes to this trend, with its substantial cattle population and a robust poultry industry supported by domestic feed manufacturing capabilities. In 2026, Saudi Arabia's 13 livestock agreements with Russia, valued at SAR 4.8 billion (USD 1.3 billion), further indicate ongoing efforts to enhance protein production capacity across the value chain. As feed volumes expand in both poultry and ruminant systems, the Middle East feed flavors and sweeteners market benefits from a growing base of commercial formulas reliant on stable intake.

Dependence on Imported Specialty Ingredients

The region heavily relies on imported specialty ingredients for advanced feed flavor and sweetener systems. Key components such as natural flavor bases, encapsulated palatants, and active sweetener compounds are predominantly sourced from Europe, the United States, and Asia, rather than domestic production. This reliance subjects feed mills to multiple cost pressures, including freight charges, currency fluctuations, and extended procurement cycles. The issue became particularly evident in early 2026, when military escalation near the Strait of Hormuz prompted major shipping lines to halt Gulf operations, resulting in significant delays in feed additive deliveries. Additionally, regulatory approval processes hinder emergency substitutions, as registration and cross-border acceptance are often too slow to address immediate shortages. Consequently, the Middle East feed flavors and sweeteners market exhibits structural vulnerability, such as demand remaining steady, but product availability can unexpectedly become constrained. This dependency also limits pricing flexibility for smaller buyers, who typically lack the capacity to maintain inventory or secure favorable logistics terms compared to larger, integrated customers.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Antibiotic-Free Feed Programs

- Expansion of Modern Feed Milling Capacity

- Price Sensitivity Among Small Feed Producers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flavors account for 82.2% of the Middle East feed flavors and sweeteners market in 2025, maintaining their leading position. This dominance is attributed to the widespread use of flavor systems in broiler starter and grower feeds and in dairy total mixed rations, which help mask variations in raw material characteristics and ensure consistent feed acceptance. Additionally, flavor usage is often integrated into standard feed specifications at many poultry and dairy operations. Adisseo's 2025 dairy nutrition partnership program in the Middle East and Africa highlights the increasing need to balance precision nutrition with reliable intake in dairy cattle, further supporting the use of flavor systems in controlled feeding programs. However, suppliers face challenges as mills increasingly prefer lower-dose, higher-potency systems that achieve similar sensory outcomes at reduced inclusion rates.

Sweeteners are projected to grow at a compound annual growth rate (CAGR) of 4.3% through 2031, positioning them as the fastest-growing subcategory despite their currently smaller market value. This growth is primarily attributed to the saccharin-free reformulation trend in imported European feed additives, driven by Regulation EU 2024/1727, which mandates compliance for compound feed by July 2026. The European Food Safety Authority's (EFSA) 2025 assessment of NHDC safety has further clarified the pathway for saccharin replacements. Companies such as Phytobiotics and ADM have introduced saccharin-free alternatives utilizing natural or receptor-targeted sweetener systems. As this transition is influenced by imported feed reformulation rather than local bans, distributors in the Middle East feed flavors and sweeteners market face pressure to qualify alternative sweetener systems before broader changes are implemented in supplier formulations.

Complete Report Scope:

- By Type

- Flavors

- Sweeteners

- By Animal

- Swine

- Ruminants

- Dairy Cattle

- Beef Cattle

- Others

- Others

- By Country

- Iran

- Saudi Arabia

- Rest of Middle East

List of Companies Covered in this Report:

- Solvay S.A.

- ADM

- Adisseo

- Alltech, Inc.

- Arvesta (Palital Feed Additives B.V.)

- Cargill, Inc.

- Innov Ad NV/SA

- Phytobiotics Futterzusatzstoffe GmbH

- Prinova Group LLC

- AFB International, Inc.

- CJ CheilJedang Corporation

- Orffa International Holding BV

- Amlan International

- Dr. Eckel Animal Nutrition GmbH and Co. KG

- Symrise AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Palatability Enhancement in Commercial Feed

- 4.2.2 Growth in Poultry and Ruminant Feed Production

- 4.2.3 Shift Toward Antibiotic-Free Feed Programs

- 4.2.4 Expansion of Modern Feed Milling Capacity

- 4.2.5 Increasing Use of Natural Feed Inputs

- 4.2.6 Heat Stress Management in Livestock Nutrition

- 4.3 Market Restraints

- 4.3.1 Dependence on Imported Specialty Ingredients

- 4.3.2 Price Sensitivity Among Small Feed Producers

- 4.3.3 Limited Local Formulation and Testing Infrastructure

- 4.3.4 Supply Chain Disruptions and Trade Volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 By Animal

- 5.2.1 Swine

- 5.2.2 Ruminants

- 5.2.2.1 Dairy Cattle

- 5.2.2.2 Beef Cattle

- 5.2.2.3 Others

- 5.2.3 Others

- 5.3 By Country

- 5.3.1 Iran

- 5.3.2 Saudi Arabia

- 5.3.3 Rest of Middle East

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Solvay S.A.

- 6.4.2 ADM

- 6.4.3 Adisseo

- 6.4.4 Alltech, Inc.

- 6.4.5 Arvesta (Palital Feed Additives B.V.)

- 6.4.6 Cargill, Inc.

- 6.4.7 Innov Ad NV/SA

- 6.4.8 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.9 Prinova Group LLC

- 6.4.10 AFB International, Inc.

- 6.4.11 CJ CheilJedang Corporation

- 6.4.12 Orffa International Holding BV

- 6.4.13 Amlan International

- 6.4.14 Dr. Eckel Animal Nutrition GmbH and Co. KG

- 6.4.15 Symrise AG