|

市場調查報告書

商品編碼

2073174

無紙化企業和數位化流程永續性軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Paperless Enterprise and Digital Process Sustainability Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

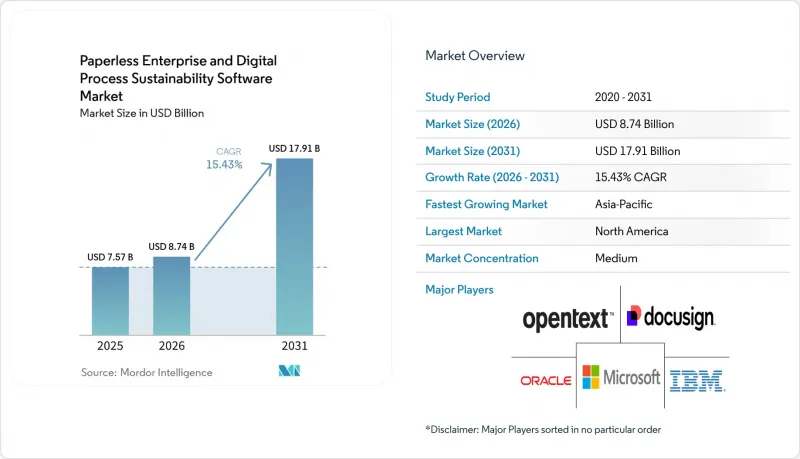

根據 Mordor Intelligence 預測,無紙化企業和數位化流程永續性軟體的市場規模預計將從 2025 年的 75.7 億美元和 2026 年的 87.4 億美元成長到 2031 年的 179.1 億美元,2026 年至 2031 年的複合年成長率為 15.43%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、應用程式(文件管理等)、最終用戶業(製造業、教育業等)和地區進行細分。市場預測以價值(美元)表示。

全球無紙化企業及數位化流程永續性軟體市場趨勢及洞察

對無紙化合規和審計回應的需求日益成長。

無紙化企業和數位化流程永續性軟體市場正在擴張,因為合規不再被視為可有可無的軟體升級。德國於2025年7月14日修訂了其GoBD指南,提高了對符合合規要求的電子記錄管理和商業交易中的數位歸檔的要求。日本也基於《電子記帳法》推動電子記錄管理的正式合規,將數位儲存和搜尋要求置於企業工作流程決策的核心。這意味著買家不僅僅是用數位資料夾替換紙本文件,而是在建立一個具有審計管治的成熟流程層。整體這項基礎,同一系統就能實現更快的搜尋、更強大的版本控制以及更清晰的證據追蹤,涵蓋財務、採購和營運等各個環節。隨著法律和營運要求的相互強化,這種組合正在增強無紙化企業和數位化流程永續性軟體市場的韌性。

人工智慧驅動的文件擷取和工作流程自動化

人工智慧驅動的數據採集技術正在改變企業負責人無紙化企業和數位化流程永續性軟體市場的評估方式。這種轉變不再局限於光學字元辨識 (OCR),因為負責人現在期望資料擷取、路由和檢驗能夠在管理管治的工作流程環境中完成。 LF AI 和資料基金會於 2026 年 6 月 9 日成立了“DocLang 規範工作小組”,旨在開發一個適用於 AI 原生文件的開放標準。此舉至關重要,因為它將使 AI 系統文件資料的準備和處理在所有企業用例中更加一致。此外,競爭的重點正從簡單的資料收集轉向編配、分析和管治。因此,在無紙化企業和數位化流程永續性軟體市場,能夠將智慧直接整合到生產工作流程中,而不是將 AI 作為獨立功能提供的供應商,更受青睞。

擁有根深蒂固的舊有系統的公司對變革管理有抵觸情緒。

在無紙化企業和數位化流程永續性軟體市場中,變革管理仍然是最明顯的限制之一,尤其是在那些根深蒂固的傳統流程公司中。許多公司仍然在員工熟悉的現有ERP整合流程中運行大量文件的工作流程,即使這些流程效率低。這造成了阻力,因為轉型不僅費力,而且常常引發團隊對短期內生產力和合規性中斷的擔憂。這個問題通常在部署後才會顯現出來,公司購買並實施平台後才發現,其工作流程功能實際上只使用了一小部分。在這種情況下,公司只看到了系統的成本,而沒有意識到其流程價值。因此,無紙化企業和數位化流程永續性軟體市場的供應商正透過將軟體與實施支援計畫、工作流程重新設計協助以及可衡量的使用目標相結合,穩步贏得市場佔有率。

細分市場分析

預計到2025年,軟體收入將佔總收入的63.47%,其中授權和平台收入仍將在無紙化企業和數位化流程永續性軟體市場中佔據核心地位。這反映出文件管理、工作流程邏輯、記錄處理和報告功能仍源自核心軟體層。然而,預計到2031年,服務領域的複合年成長率將達到16.01%,超過無紙化企業和數位化流程永續性軟體市場的整體成長率。服務領域的快速擴張表明,許多買家現在需要的不僅僅是實施支援。他們需要整合工作、管治設計、工作流程映射以及系統運作後的持續最佳化。在這一領域,軟體仍然是收入支柱,但隨著實施複雜性的增加,服務的重要性也不斷提升。

人工智慧平台需要比傳統文件庫更結構化的資料、更強大的控制和更嚴謹的流程設計,這改變了軟體和服務之間的平衡。為了使企業能夠大規模可靠地運作自動化,通常需要對ERP、CRM、中間件和傳統文件環境進行全面支援。這意味著供應商和合作夥伴在初始授權銷售之後需要持續投入工作。 Newgen於2026年5月發布的「企業編排層」表明,供應商正在從孤立的自動化轉向在整個企業流程中持續、受控的管治。 ABBYY也透過其產品定位和在管治文件處理領域的持續評估,強調了受控文件人工智慧的重要性,進一步強化了其在準確性、可審計性和營運一致性方面的價值。這表明,無紙化企業和數位化流程永續性軟體市場並沒有偏離軟體本身,而是更加重視將軟體轉化為功能性營運模式的服務層。

到2025年,基於雲端的採用將佔總收入的68.91%,在無紙化企業和數位化流程永續性軟體市場佔據最大佔有率。此外,預計到2031年,雲端的複合年成長率將達到17.42%,明顯高於無紙化企業和數位化流程永續性軟體市場的整體成長率。目前,採用雲端的理由已不再只是為了降低基礎設施成本。買家越來越傾向於將雲端採用與人工智慧賦能、快速更新和更具可擴展性的工作流程執行聯繫起來。這在文件密集型環境中尤其重要,因為在這些環境中,提取、路由、搜尋和分類不再依賴靜態計算假設。與本地部署模式相比,雲端平台也更容易支援通路拓展、市場主導的採購和捆綁銷售。這些因素確保了雲端在新的採用決策中始終處於領先地位,尤其是當企業尋求實現工作流程管理和使用者存取現代化時。

類似的趨勢也體現在供應商將其內容工具與更廣泛的雲端生態系整合。 Laserfiche 於 2026 年 6 月在 AWS Marketplace 上線,透過許多 IT 團隊已經熟悉的雲端管道,擴大了其面向受監管企業買家的直接採購管道。同時,本地部署和混合模式在無紙化企業和數位化流程永續性軟體市場中仍然至關重要。這是因為一些買家仍然無法將其所有內容和流程資料放在公共雲端環境中。 2026 年 5 月,UiPath 發布了面向本地部署的基於代理的 AI 功能,其目標用戶顯然是需要更強主權控制的公共部門和受監管用例。因此,在政策風險與技術性能同等重要的產業,混合部署被視為一種切實可行的營運模式,而非權宜之計。在此背景下,儘管雲端在無紙化企業和數位化流程永續性軟體市場中仍然佔據主導地位,但混合架構在實際買家行為中仍然發揮著重要作用。

區域分析

到2025年,北美將佔全球銷售額的35.43%,成為無紙化企業和數位化流程永續性軟體市場中最大的區域佔有率。這一主導地位源自於成熟企業軟體的廣泛應用、強大的雲端基礎設施以及大型企業長期以來對工作流程自動化的偏好。此外,該地區客戶群樂於將文件系統與更廣泛的生產力、自動化和分析平台相整合,也為其發展提供了助力。根據Automation Anywhere的數據顯示,第四季61%的軟體訂單為人工智慧驅動的部署。這表明該地區的企業需求已不再局限於簡單的任務自動化。事實上,北美仍然是無紙化企業和數位化流程永續性軟體市場的基石,因為該地區在規模、整合意願和雲端技術熟練度方面最為契合。

歐洲仍然是第二大市場,其在無紙化企業和數位化流程永續性軟體市場中的地位主要受相關法規的影響。歐盟指令 (EU) 2026/470 於 2026 年 3 月 18 日生效,強制要求採用統一的數位資料格式和 XBRL 標籤來揭露相關的永續性資訊。此外,德國於 2025 年 7 月修訂了其 GoBD 指南,進一步強調了妥善進行數位歸檔和電子記錄管理的合規性重要性。這些措施使歐洲成為需求主要由正式義務而非自願性現代化預算驅動的地區典範。這種環境正在推動無紙化企業和數位化流程永續性軟體市場中能夠提供強大的在地化、稽核管理和工作流程管治的供應商的發展。

預計到2031年,亞太地區將以16.81%的複合年成長率成長,成為無紙化企業和數位化流程永續性軟體市場規模預測中成長最快的區域市場。該地區受益於主要經濟體同步成長的數位化壓力,尤其是在那些簿記、稅收和記錄保存法規日益嚴格的國家。日本就是一個典型的例子,其《電子簿記法》持續強調企業遵守數位化儲存和搜尋規定。南美洲和中東及非洲地區仍處於發展初期,但隨著數據在地化、雲端存取和基於監管的數位化項目的改進,它們的重要性日益凸顯。這將為無紙化企業和數位化流程永續性軟體市場提供更廣泛的成長基礎,使其不再局限於北美和歐洲等成熟市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對無紙化合規和審計回應的需求日益成長。

- 規範遠距和混合辦公的業務流程

- 人工智慧驅動的文件擷取和工作流程自動化

- 永續發展報告給企業帶來了數位轉型的壓力。

- 與企業系統整合和 API主導的編配

- 已存檔流程資料和流程挖掘中蘊藏的未開發價值

- 市場限制因素

- 擁有眾多舊有系統的公司對變革管理有抵觸情緒

- 資料居住要求和主權限制

- 混合應用堆疊中的工作流程碎片化

- 受監管買家的長期企業銷售週期

- 產業價值鏈分析

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 按部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- 文件管理

- 工作流程自動化

- 電子簽章

- 試算表

- 記錄管理

- 追蹤和報告流程永續性

- 按最終用戶行業分類

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 資訊科技/通訊

- 政府/公共部門

- 製造業

- 零售與電子商務

- 教育

- 能源公用事業

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- OpenText Corporation

- Oracle Corporation

- IBM Corporation

- DocuSign, Inc.

- SAP SE

- Adobe Inc.

- Box, Inc.

- Hyland Software, Inc.

- Laserfiche

- M-Files Corporation

- DocuWare GmbH

- Nintex Global, Inc.

- Appian Corporation

- UiPath Inc.

- Automation Anywhere, Inc.

- ABBYY Development Inc.

- Newgen Software Technologies Limited

- Tungsten Automation Corporation

- Kofax, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the paperless enterprise and digital process sustainability software market size is projected to expand from USD 7.57 billion in 2025 and USD 8.74 billion in 2026 to USD 17.91 billion by 2031, registering a CAGR of 15.43% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Document Management, and More), End-User Industry (Manufacturing, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Paperless Enterprise and Digital Process Sustainability Software Market Trends and Insights

Rising Demand for Paperless Compliance and Audit Readiness

The paperless enterprise and digital process sustainability software market is moving forward because compliance is no longer treated as a discretionary software upgrade. Germany updated its GoBD guidance on July 14, 2025, and the rule tightened expectations around compliant electronic recordkeeping and digital archiving for business transactions. Japan has also been pushing formal electronic bookkeeping compliance under the Electronic Bookkeeping Act, which keeps digital storage and retrieval requirements at the center of enterprise workflow decisions. This means buyers are not just replacing paper files with digital folders, they are building governed process layers that can stand up in an audit. Once that foundation is in place, the same systems also support faster retrieval, stronger version control, and cleaner evidence trails across finance, procurement, and operations. That combination is making the paperless enterprise and digital process sustainability software market more resilient, because legal needs and operational needs are now reinforcing each other.

AI-Enabled Document Capture and Workflow Automation

AI-enabled capture is changing how the paperless enterprise and digital process sustainability software market is evaluated by enterprise buyers. The shift is no longer limited to optical character recognition, because buyers now expect extraction, routing, and validation to happen inside a governed workflow environment. The LF AI and Data Foundation launched the DocLang Specification Working Group on June 9, 2026, with the aim of creating an open standard for AI-native documents. That move matters because it supports more consistent preparation and handling of document data for AI systems across enterprise use cases. It also shifts competitive pressure away from simple capture and toward orchestration, analytics, and governance. As a result, the paperless enterprise and digital process sustainability software market is rewarding vendors that can embed intelligence directly in production workflows instead of offering AI as an isolated feature.

Change Management Resistance in Legacy-Heavy Enterprises

Change management remains one of the clearest limits on the paperless enterprise and digital process sustainability software market, especially where legacy processes are deeply embedded. Many enterprises still run document-heavy workflows inside established ERP-linked routines that employees know well, even if those routines are slow. That creates resistance not only because migration takes effort, but also because teams often fear short-term disruption to productivity and compliance. The problem often appears after deployment, when a platform is purchased and implemented, but only a small share of its workflow capability is actually used. In those cases, the business sees the cost of the system before it sees the process value of the system. This is why vendors in the paperless enterprise and digital process sustainability software market are gaining ground when they pair software with adoption programs, workflow redesign support, and measurable usage targets.

Other drivers and restraints analyzed in the detailed report include:

- Remote and Hybrid Work Process Standardization

- Sustainability Reporting Pressure on Enterprise Process Digitization

- Data Residency and Sovereignty Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 63.47% of revenue in 2025, which kept license and platform income at the center of the paperless enterprise and digital process sustainability software market. That position reflects the fact that document control, workflow logic, records handling, and reporting functions still begin with a core software layer. Even so, services are projected to grow at a 16.01% CAGR through 2031, which is faster than the overall paperless enterprise and digital process sustainability software market. The faster expansion in services shows that many buyers now need more than installation support. They need integration work, governance design, workflow mapping, and continued optimization after the system goes live. In this segment, software remained the commercial anchor, but services became more important as the complexity of deployment increased.

The balance between software and services is changing because AI-capable platforms require cleaner data structures, stronger controls, and tighter process design than older document repositories did. Enterprises often need support across ERP, CRM, middleware, and legacy document environments before automation can run reliably at scale. That creates recurring work for vendors and partners even after the initial license has been sold. Newgen introduced its Enterprise Orchestration Layer in May 2026, which showed how vendors are trying to move from isolated automation into continuous, governed execution across enterprise processes. ABBYY also emphasized governed document AI through its product positioning and continued recognition in intelligent document processing, which reinforced the value of accuracy, auditability, and operational consistency. This means the Paperless Enterprise and Digital Process Sustainability Software Market industry is not shifting away from software, but it is placing more value on the service layer that turns software into a working operating model.

Cloud-based deployment held 68.91% of revenue in 2025, giving it the largest share of the paperless enterprise and digital process sustainability software market. It is also projected to grow at a 17.42% CAGR through 2031, which places cloud clearly ahead of the overall paperless enterprise and digital process sustainability software market size growth rate. The current case for cloud is broader than lower infrastructure cost, because buyers increasingly connect cloud adoption with AI readiness, faster updates, and more scalable workflow execution. That matters in document-heavy environments where extraction, routing, search, and classification can no longer depend on static compute assumptions. Cloud platforms also support channel expansion, marketplace-led buying, and bundle-based distribution more easily than on-premises models do. These factors are keeping cloud at the forefront of new deployment decisions, especially where enterprises want to modernize both workflow control and user access.

The same pattern is visible in how vendors are linking content tools with broader cloud ecosystems. Laserfiche launched on AWS Marketplace in June 2026, which expanded direct procurement access for regulated enterprise buyers through a cloud channel already familiar to many IT teams. At the same time, on-premises and hybrid models remain important in the paperless enterprise and digital process sustainability software market because some buyers still cannot place all content and process data in a public cloud environment. UiPath released agentic AI capabilities for on-premises deployment in May 2026, with clear attention to public sector and regulated use cases that require stronger sovereignty control. Hybrid deployment therefore remains less of a temporary compromise and more of a practical operating model in sectors where policy risk matters as much as technical performance. In that context, the paperless enterprise and digital process sustainability software market share of cloud remains dominant, but mixed architectures are still important to actual buyer behavior.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Model

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Document Management

- Workflow Automation

- E-Signature

- Electronic Forms

- Records Management

- Process Sustainability Tracking and Reporting

- By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare and Life Sciences

- Information Technology and Telecom

- Government and Public Sector

- Manufacturing

- Retail and E-Commerce

- Education

- Energy and Utilities

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 35.43% of revenue in 2025, giving it the largest regional position in the paperless enterprise and digital process sustainability software market. That lead came from mature enterprise software adoption, strong cloud infrastructure, and a long-standing preference for workflow automation in large organizations. The region also benefits from a buyer base that is comfortable linking document systems with broader productivity, automation, and analytics platforms. Automation Anywhere reported that 61% of its Q4 software bookings came from AI-driven deployments, which shows how enterprise demand in the region is moving beyond narrow task automation. In practical terms, North America remains the part of the paperless enterprise and digital process sustainability software market where scale, integration appetite, and cloud familiarity are most aligned.

Europe remained the second-largest geography, and its role in the paperless enterprise and digital process sustainability software market is shaped heavily by regulation. Directive (EU) 2026/470 entered into force on March 18, 2026, and it requires harmonized digital data formats and XBRL tagging for covered sustainability disclosures. Germany also updated its GoBD guidance in July 2025, which reinforced the compliance importance of proper digital archiving and electronic records management. Those measures make Europe the clearest example of a region where demand is often driven by formal obligations rather than optional modernization budgets. That environment supports vendors that can present strong localization, audit control, and workflow governance in the paperless enterprise and digital process sustainability software market.

Asia-Pacific is projected to grow at a 16.81% CAGR through 2031, which makes it the fastest-growing regional segment in the paperless enterprise and digital process sustainability software market size outlook. The region is benefiting from simultaneous digitization pressure across large economies, especially where bookkeeping, tax, and recordkeeping rules are tightening. Japan remains a clear example because the Electronic Bookkeeping Act continues to keep digital storage and retrieval compliance in focus for businesses. South America, the Middle East, and Africa remain earlier-stage areas, but they are becoming more relevant as data localization, cloud access, and regulatory digitization programs improve. This gives the paperless enterprise and digital process sustainability software market a wider growth base beyond its mature centers in North America and Europe.

- Microsoft Corporation

- OpenText Corporation

- Oracle Corporation

- IBM Corporation

- DocUSign, Inc.

- SAP SE

- Adobe Inc.

- Box, Inc.

- Hyland Software, Inc.

- Laserfiche

- M-Files Corporation

- DocuWare GmbH

- Nintex Global, Inc.

- Appian Corporation

- UiPath Inc.

- Automation Anywhere, Inc.

- ABBYY Development Inc.

- Newgen Software Technologies Limited

- Tungsten Automation Corporation

- Kofax, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Paperless Compliance and Audit Readiness

- 4.2.2 Remote and Hybrid Work Process Standardization

- 4.2.3 AI-Enabled Document Capture and Workflow Automation

- 4.2.4 Sustainability Reporting Pressure on Enterprise Process Digitization

- 4.2.5 Integration With Enterprise Systems and API-Led Orchestration

- 4.2.6 Underused Value From Archived Process Data and Process Mining

- 4.3 Market Restraints

- 4.3.1 Change Management Resistance in Legacy-Heavy Enterprises

- 4.3.2 Data Residency and Sovereignty Constraints

- 4.3.3 Workflow Fragmentation Across Mixed Application Stacks

- 4.3.4 Long Enterprise Sales Cycles for Regulated Buyers

- 4.4 Industry Value-Chain Analysis

- 4.5 Supply Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Document Management

- 5.4.2 Workflow Automation

- 5.4.3 E-Signature

- 5.4.4 Electronic Forms

- 5.4.5 Records Management

- 5.4.6 Process Sustainability Tracking and Reporting

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services, and Insurance (BFSI)

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Government and Public Sector

- 5.5.5 Manufacturing

- 5.5.6 Retail and E-Commerce

- 5.5.7 Education

- 5.5.8 Energy and Utilities

- 5.5.9 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 OpenText Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 IBM Corporation

- 6.4.5 DocuSign, Inc.

- 6.4.6 SAP SE

- 6.4.7 Adobe Inc.

- 6.4.8 Box, Inc.

- 6.4.9 Hyland Software, Inc.

- 6.4.10 Laserfiche

- 6.4.11 M-Files Corporation

- 6.4.12 DocuWare GmbH

- 6.4.13 Nintex Global, Inc.

- 6.4.14 Appian Corporation

- 6.4.15 UiPath Inc.

- 6.4.16 Automation Anywhere, Inc.

- 6.4.17 ABBYY Development Inc.

- 6.4.18 Newgen Software Technologies Limited

- 6.4.19 Tungsten Automation Corporation

- 6.4.20 Kofax, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

南美洲綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Kubernetes:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

南美洲綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Kubernetes:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 雲端應用安全市場:按組件、部署模式、最終用戶產業和企業規模分類-2026-2032年全球市場預測

雲端應用安全市場:按組件、部署模式、最終用戶產業和企業規模分類-2026-2032年全球市場預測 容器和 Kubernetes 安全市場報告:按組件、產品、組織規模、行業垂直領域和地區分類(2026-2034 年)

容器和 Kubernetes 安全市場報告:按組件、產品、組織規模、行業垂直領域和地區分類(2026-2034 年) Kubernetes市場規模、佔有率和成長分析(按組件、產品、組織規模、垂直產業和地區分類)-2026-2033年產業預測

Kubernetes市場規模、佔有率和成長分析(按組件、產品、組織規模、垂直產業和地區分類)-2026-2033年產業預測 雲端應用安全市場規模、佔有率和成長分析(按類型、組件、組織規模、部署類型、垂直產業和地區分類)-2026-2033年產業預測

雲端應用安全市場規模、佔有率和成長分析(按類型、組件、組織規模、部署類型、垂直產業和地區分類)-2026-2033年產業預測 全球 Kubernetes 市場

全球 Kubernetes 市場 2026 年至 2032 年容器和 Kubernetes 安全市場(按產品、組織規模、垂直產業和地區分類)

2026 年至 2032 年容器和 Kubernetes 安全市場(按產品、組織規模、垂直產業和地區分類)