|

市場調查報告書

商品編碼

2073171

南美洲綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)South America Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

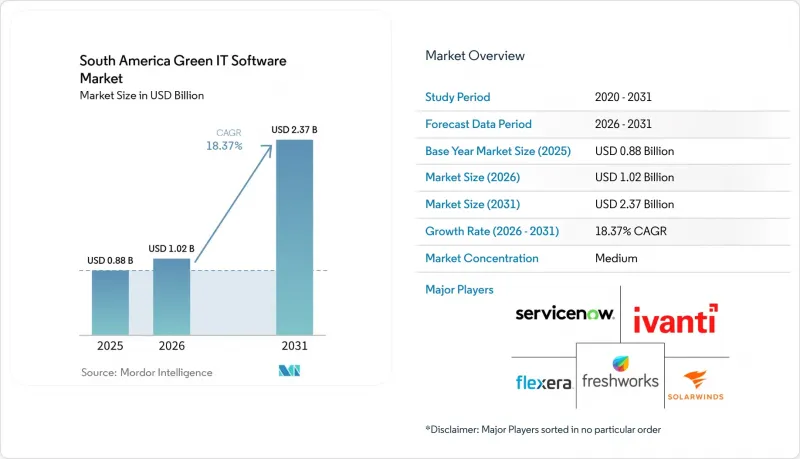

據 Mordor Intelligence 稱,2025 年南美綠色 IT 軟體市場價值 8.8 億美元,預計到 2031 年將從 2026 年的 10.2 億美元成長至 23.7 億美元,預測期(2026-2031 年)複合年成長率為 18.37%。

本報告按交付方式(軟體和服務)、部署方式(雲端、本地部署、混合部署)、企業規模(大型企業和中小企業)、解決方案類型(碳管理和計算軟體等)、最終用戶(IT和電信、銀行、金融服務和保險、能源和公共產業等)以及地區進行細分。市場預測以美元計價。

南美洲綠色IT軟體市場趨勢與洞察

日益嚴格的碳排放報告和ESG合規要求

在南美洲綠色IT軟體市場,合規性仍然是最明顯的短期採購促進因素。企業不再只是需要儀錶板;他們需要的是能夠支援可追溯資料收集、可重複計算和結構化報告工作流程的平台。這種轉變對於大型企業尤其重要,因為在這些企業中,永續發展、財務、法律和IT團隊需要一個共用系統,而不是分散的電子表格或一次性的諮詢服務。這種轉變也解釋了為什麼碳管理和會計軟體仍然是許多實施過程中的首選採購。一旦企業實施了核心報告系統,下一步通常是新增相關的模組,用於資料管理、目標追蹤和工作流程管理。與短期專案週期相比,這種模式在南美洲綠色IT軟體市場創造了更永續的收入基礎。

企業對節能型IT營運的興趣日益濃厚

在南美洲綠色IT軟體市場,能源效率正從一項次要優勢逐漸成為營運的首要任務。隨著數位化工作負載的不斷成長,IT團隊不得不監控資源利用率、識別閒置容量並在不增加電力消耗量的情況下提升效能。這正在改變採購方的組成,軟體選擇範圍正從永續發展團隊擴展到基礎設施、維運和平台工程團隊。此外,當能源最佳化能夠被證實對營運成本、運作規劃和資產壽命產生可衡量的影響時,其價值提案將更具吸引力。這使得綠色IT軟體即使對於目前無需直接報告這些因素的公司也至關重要。從長遠來看,這種廣泛的效用預計將進一步推動南美綠色IT軟體市場的普及,吸引那些既主導合規又主導效率的客戶。

傳統IT環境中高階整合的複雜性

在南美洲綠色IT軟體市場,整合挑戰仍是加速普及應用的主要障礙。許多公司仍在使用過時的ERP、採購、物流、設施管理和服務管理系統,這些系統並非為將資料導入標準化的碳排放和能源報告工具而設計。這延長了採用週期,因為負責人必須先將不同格式、所有者和品質等級的資料進行映射,軟體才能產生可靠的輸出。此外,在選擇供應商時,實施支援、預置連接器以及本地合作夥伴的能力顯得尤為重要。如果全球平台低估了大規模區域組織引進週期數據的碎片化程度,則可能失去發展動力。因此,整合準備情況以及產品覆蓋範圍通常是南美洲綠色IT軟體市場的關鍵因素。

細分市場分析

到2025年,軟體將佔據南美綠色IT軟體市場76.14%的佔有率。這表明買家仍然傾向於可配置且可擴展的平台。這反映了企業的實際需求,他們需要能夠在單一、可重複的環境中管理排放資料、工作流程規則、報告範本和稽核追蹤的工具。軟體層也符合市場趨勢,因為資訊揭露預期和內部管治需求變化如此之快,以至於靜態的報告流程無法跟上步伐。買家重視能夠更新類別、調整運算邏輯和新增模組,而無需每次需求變更時重建營運模型。這使得軟體在南美綠色IT軟體市場中具有結構性優勢,因為它支援可擴展性、連續性和內部所有權。

預計到2031年,服務業將以18.43%的複合年成長率成長,這表明即使在軟體主導的市場中,實施工作仍然至關重要。企業仍需要支援來整合舊有系統、整理歷史記錄、明確職責以及建立定期報告週期的管治規則。此外,隨著內部成熟度的提高,許多組織在調整模板和管理方法方面需要幫助,因此,實施後的諮詢和管理服務變得越來越重要。隨著綠色IT軟體產業從初始實施轉向在更廣泛的業務職能範圍內進行持續最佳化,服務層的重要性預計將會成長。然而,最有前景的服務機會可能不會取代平台實施,而是作為其補充,從而確保軟體在南美綠色IT軟體市場的經營模式中仍然佔據核心地位。

到2025年,雲端解決方案將佔據南美綠色IT軟體市場64.17%的佔有率。這反映了可擴展交付和持續產品更新的吸引力。這種模式適用於那些希望發布新的報表範本、工作流程功能和分析功能,而無需進行耗時的內部升級專案的公司。它也滿足了那些偏好可跨地區和跨職能部署的訂閱式軟體的公司的需求,從而促進了其技術環境的標準化。南美洲綠色IT軟體市場的許多買家最初都從報表和資料管理等用例入手,然後將平台擴展到營運領域,這一現像也推動了雲端技術的普及。這種順序減輕了初始負擔,縮短了價值實現時間。

混合部署預計到2031年將以18.52%的複合年成長率成長,凸顯了控制和柔軟性共存的必要性。處理高度敏感營運資料的公司仍然需要基於雲端的分析和報告的速度,但可能更傾向於在受管理的本地環境中保留某些記錄和連接器。這種架構也對分階段進行現代化改造而非一次性替換所有系統的公司具有吸引力。 HPE發布的GreenLake Intelligence反映了向混合IT管理的更廣泛趨勢,它將營運視覺性與以永續性為中心的最佳化相結合。雖然本地部署預計仍將繼續存在,但其客戶群有限,南美綠色IT軟體市場顯然正在轉向平衡更新速度、可審計性和資料管理的架構。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業對節能型IT營運的興趣日益濃厚

- 日益嚴格的碳排放報告和ESG合規要求

- 擴展雲端和虛擬化基礎架構管理

- 加大力度最佳化資料中心的能耗

- 公共部門數位永續發展計劃

- 廣泛採用人工智慧技術最佳化IT資產和工作負載。

- 市場限制因素

- 跨越傳統IT環境進行高階整合的複雜性。

- 中小企業的預算限制

- 永續性衡量缺乏標準化

- 對資料安全和資料儲存位置的擔憂

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 按解決方案類型

- 碳管理和運算軟體

- ESG報告和合規軟體

- 永續性資料管理平台

- 脫碳規劃軟體

- 能源和資源最佳化軟體

- 最終用戶

- 資訊科技/通訊

- BFSI

- 製造業

- 能源公用事業

- 零售與電子商務

- 政府

- 衛生保健

- 建築和基礎設施

- 其他終端用戶產業

- 按地區

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ServiceNow, Inc.

- SolarWinds Corporation

- Freshworks Inc.

- Ivanti Software, Inc.

- Flexera Software LLC

- Dynatrace, Inc.

- Progress Software Corporation

- Open Text Corporation

- New Relic, Inc.

- Workiva Inc.

- ScienceLogic, Inc.

- Schneider Electric SE

- N-able, Inc.

- IBM Corporation

- IFS AB

- BMC Software, Inc.

- NinjaOne, LLC

- Dakota Software Corporation

- EcoVadis SAS

- Salesforce Inc

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america green IT software market size was valued at USD 0.88 billion in 2025 and estimated to grow from USD 1.02 billion in 2026 to reach USD 2.37 billion by 2031, at a CAGR of 18.37% during the forecast period (2026-2031).

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and More), End User (IT and Telecom, BFSI, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Green IT Software Market Trends and Insights

Growing Carbon Reporting and ESG Compliance Requirements

Compliance remains the clearest near-term buying trigger for the South America green IT software market. Enterprises are no longer looking only for dashboards; they now need platforms that support traceable data capture, repeatable calculations, and structured reporting workflows. This change matters most for larger companies, where sustainability, finance, legal, and IT teams now need shared systems rather than disconnected spreadsheets and one-off consulting exercises. It also helps explain why carbon management and accounting software continues to act as the first purchase in many deployment journeys. Once an enterprise implements a reporting core, it often adds adjacent modules for data management, target tracking, and workflow controls in the next stage. This pattern is giving the South America green IT software market a more durable revenue base than a short project cycle would provide.

Rising Enterprise Focus on Energy-Efficient IT Operations

Energy efficiency is becoming an operating priority rather than a side benefit in the South America green IT software market. As digital workloads grow, IT teams are under pressure to monitor utilization, identify idle capacity, and improve performance without increasing power consumption. That is changing the buyer profile, because software selection is moving beyond sustainability teams and into infrastructure, operations, and platform engineering groups. The value case is also easier to defend when energy optimization can show measurable effects on operating costs, uptime planning, and asset life. This makes green IT software relevant even for firms that are not yet under direct reporting pressure. Over time, that broader utility should help the South America green IT software market deepen adoption across both compliance-led and efficiency-led accounts.

High Integration Complexity Across Legacy IT Environments

Integration difficulty is still one of the main barriers to faster adoption in the South America green IT software market. Many enterprises run old ERP, procurement, logistics, facilities, and service management systems that were never designed to feed standardized carbon or energy reporting tools. That creates long deployment cycles because buyers must map data across different formats, owners, and quality levels before the software can produce trusted outputs. It also raises the importance of implementation support, prebuilt connectors, and local partner capability during vendor selection. Global platforms can lose momentum when they underestimate the extent of operational data fragmentation across large regional organizations. For this reason, integration readiness often matters as much as product breadth in the South America green IT software market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cloud and Virtualized Infrastructure Management

- Wider Adoption of AI-Based IT Asset and Workload Optimization

- Budget Constraints Among Small and Mid-Sized Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 76.14% of South America's green IT software market share in 2025, which shows that buyers still prefer platforms they can configure and expand over time. That position reflects a practical need, as enterprises want tools that can manage emissions data, workflow rules, reporting templates, and audit trails within a single, repeatable environment. The software layer also aligns with the market's direction, as disclosure expectations and internal governance needs are changing faster than static reporting processes can keep pace. Buyers value the ability to update categories, adjust calculation logic, and add new modules without rebuilding the operating model each time requirements change. This gives software a structural advantage in the South America green IT software market because it supports scale, continuity, and internal ownership.

Services are projected to grow at a 18.43% CAGR through 2031, indicating that implementation work remains essential even in a software-led market. Enterprises still need support to connect legacy systems, clean historical records, define ownership, and set governance rules for recurring reporting cycles. Advisory and managed services also become more relevant after deployment, because many organizations need help adapting templates and controls as internal maturity improves. The service layer is likely to rise in importance as the green IT software industry moves from first purchase to ongoing optimization across broader business functions. Even so, the strongest service opportunities are likely to sit beside platform rollouts rather than replace them, which keeps software at the center of the commercial model for the South America green IT software market.

Cloud-based solutions accounted for 64.17% share of the South America green IT software market size in 2025, reflecting the appeal of scalable delivery and continuous product updates. This model works well for enterprises that want new reporting templates, workflow features, and analytics releases without lengthy internal upgrade projects. It also meets the needs of companies standardizing their technology estates and preferring subscription-based software that can be deployed across regions and functions. In the South America green IT software market, cloud deployment is also helped by the fact that many buyers begin with reporting and data management use cases before extending the platform into operations. That sequence reduces the initial burden and accelerates time-to-value.

Hybrid deployment is expected to expand at a 18.52% CAGR through 2031, underscoring that control and flexibility must often coexist. Companies handling sensitive operating data still want cloud-based analytics and reporting speed, but they may prefer to retain selected records or connectors within controlled internal environments. This structure also appeals to enterprises that are modernizing in stages rather than replacing all systems at once. HPE's GreenLake Intelligence launch reflects the wider push toward hybrid IT management that combines operational visibility with sustainability-focused optimization. On-premise deployments are likely to persist in a narrower set of accounts, yet the South America green IT software market is clearly moving toward architectures that balance update speed, auditability, and data control.

Complete Report Scope:

- By offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End User

- IT and Telecom

- BFSI

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare

- Construction and Infrastructure

- Other End-User Industries

- By Geography

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

List of Companies Covered in this Report:

- ServiceNow, Inc.

- SolarWinds Corporation

- Freshworks Inc.

- Ivanti Software, Inc.

- Flexera Software LLC

- Dynatrace, Inc.

- Progress Software Corporation

- Open Text Corporation

- New Relic, Inc.

- Workiva Inc.

- ScienceLogic, Inc.

- Schneider Electric SE

- N-able, Inc.

- IBM Corporation

- IFS AB

- BMC Software, Inc.

- NinjaOne, LLC

- Dakota Software Corporation

- EcoVadis SAS

- Salesforce Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Enterprise Focus on Energy-Efficient IT Operations

- 4.2.2 Growing Carbon Reporting and ESG Compliance Requirements

- 4.2.3 Expansion of Cloud and Virtualized Infrastructure Management

- 4.2.4 Increasing Data Center Power Optimization Initiatives

- 4.2.5 Public Sector Digital Sustainability Programs

- 4.2.6 Wider Adoption of AI-Based IT Asset and Workload Optimization

- 4.3 Market Restraints

- 4.3.1 High Integration Complexity Across Legacy IT Environments

- 4.3.2 Budget Constraints Among Small and Mid-Sized Enterprises

- 4.3.3 Limited Standardization in Sustainability Measurement

- 4.3.4 Data Security and Data Residency Concerns

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of New Entrants

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End User

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

- 5.6 By Geography

- 5.6.1 Brazil

- 5.6.2 Argentina

- 5.6.3 Chile

- 5.6.4 Colombia

- 5.6.5 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ServiceNow, Inc.

- 6.4.2 SolarWinds Corporation

- 6.4.3 Freshworks Inc.

- 6.4.4 Ivanti Software, Inc.

- 6.4.5 Flexera Software LLC

- 6.4.6 Dynatrace, Inc.

- 6.4.7 Progress Software Corporation

- 6.4.8 Open Text Corporation

- 6.4.9 New Relic, Inc.

- 6.4.10 Workiva Inc.

- 6.4.11 ScienceLogic, Inc.

- 6.4.12 Schneider Electric SE

- 6.4.13 N-able, Inc.

- 6.4.14 IBM Corporation

- 6.4.15 IFS AB

- 6.4.16 BMC Software, Inc.

- 6.4.17 NinjaOne, LLC

- 6.4.18 Dakota Software Corporation

- 6.4.19 EcoVadis SAS

- 6.4.20 Salesforce Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

德國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)無紙化企業和數位化流程永續性軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Kubernetes:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

德國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)無紙化企業和數位化流程永續性軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Kubernetes:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 雲端應用安全市場:按組件、部署模式、最終用戶產業和企業規模分類-2026-2032年全球市場預測

雲端應用安全市場:按組件、部署模式、最終用戶產業和企業規模分類-2026-2032年全球市場預測 容器和 Kubernetes 安全市場報告:按組件、產品、組織規模、行業垂直領域和地區分類(2026-2034 年)

容器和 Kubernetes 安全市場報告:按組件、產品、組織規模、行業垂直領域和地區分類(2026-2034 年) Kubernetes市場規模、佔有率和成長分析(按組件、產品、組織規模、垂直產業和地區分類)-2026-2033年產業預測

Kubernetes市場規模、佔有率和成長分析(按組件、產品、組織規模、垂直產業和地區分類)-2026-2033年產業預測 雲端應用安全市場規模、佔有率和成長分析(按類型、組件、組織規模、部署類型、垂直產業和地區分類)-2026-2033年產業預測

雲端應用安全市場規模、佔有率和成長分析(按類型、組件、組織規模、部署類型、垂直產業和地區分類)-2026-2033年產業預測 全球 Kubernetes 市場

全球 Kubernetes 市場 2026 年至 2032 年容器和 Kubernetes 安全市場(按產品、組織規模、垂直產業和地區分類)

2026 年至 2032 年容器和 Kubernetes 安全市場(按產品、組織規模、垂直產業和地區分類)