|

市場調查報告書

商品編碼

2073172

德國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Germany Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

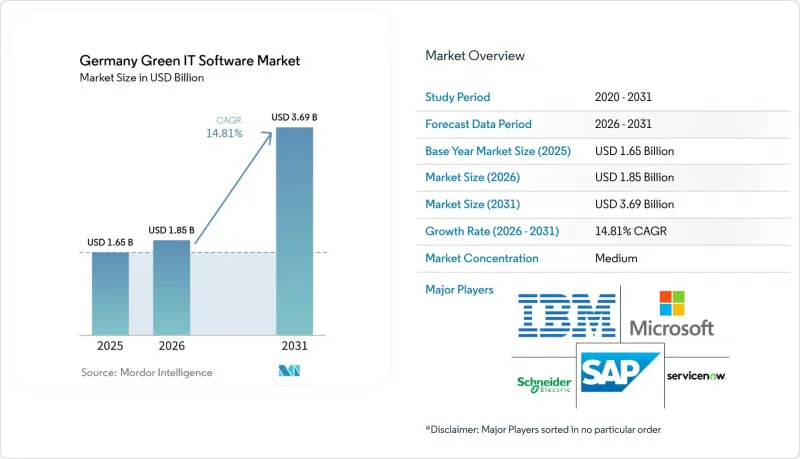

據 Mordor Intelligence 稱,德國綠色 IT 軟體市場預計將從 2025 年的 16.5 億美元成長到 2026 年的 18.5 億美元,到 2031 年達到 36.9 億美元,預計 2026 年至 2031 年的複合年成長率為 14.81%。

本報告按交付方式(軟體和服務)、部署方式(雲端、本地部署、混合部署)、公司規模(大型企業和中小企業)、解決方案類型(碳管理和計算軟體、ESG報告和合規軟體等)以及最終用戶(IT和通訊業等)進行分類。市場預測以美元計價。

德國綠色IT軟體市場趨勢與洞察

來自企業永續發展報告的監管壓力

德國企業永續發展報告指令(CSRD)的國有化進程正引領德國綠色IT軟體市場走向更規範化的採購週期,首批針對大型企業的大規模報告將於2026年到來。最初的目標群體包括約240家擁有1,000名以上員工的德國公司,預計到2028年,報告義務將逐步擴大至約15,000家公司。最初的ESRS框架要求在82個揭露項目中提供多達1100個資料點,而歐盟於2025年12月批准的綜合方案I通過對授權法規的修訂,預計將把這一要求減少到約400-500個資料點。這項調整不會降低軟體需求,因為企業仍然需要可審計的資料流和能夠隨著最終架構的逐步清晰而調整的工具。此外,從供應商收集資料的工作擴大涉及那些在其採購活動中不直接進行報告的中型企業。這是因為首批客戶仍需從相關公司取得檢驗的範圍 3 數據。 SAP 的《永續發展控制塔 2026》更新顯示,現有供應商正試圖透過擴展其 ESRS 指標覆蓋範圍並引入人工智慧驅動的審計就緒功能來滿足這種合規性主導的需求。

德國公司日益沉重的ESG報告負擔

德國綠色IT軟體市場的發展也得益於德國企業同時應對多個報告框架。大型金融機構需要根據銀行監理規定揭露ESG風險,而製造商也必須遵守歐盟分類標準和供應鏈實質審查要求。這種重疊性降低了單一用途工具的效用,因此買家正在轉向能夠從單一操作層管理報告、資料管治和稽核準備的平台。 Plan A憑藉其在德語工作流程、本地監管趨勢追蹤以及CSRD和ESRS變更的即時更新方面的優勢而確立了自身地位。該公司表示,自2024年以來,在為超過1500家DACH地區企業提供服務的同時,一直保持盈利。 2026年5月,SAP宣布,包括足跡最佳化代理在內的新型永續發展人工智慧代理商將於2026年底前全面推出,屆時情境模擬所需時間將從一天縮短至20分鐘。隨著報告工作量的增加,買家對分散的工具越來越不接受度,並且對能夠以統一的方式支援 CSRD、歐盟分類法、GRI 和銀行相關揭露要求的整合平台表現出越來越濃厚的興趣。

與傳統ERP和ITSM系統整合的複雜性。

傳統架構仍是德國綠色IT軟體市場整體普及的一大障礙。許多德國企業仍在使用SAP ECC、SAP IS-U或高度客製化的特定產業環境,這意味著綠色IT平台在產生可靠輸出之前,往往需要完成資料提取、映射和核對等艱鉅任務。雪上加霜的是,符合審計要求的永續性報告需要資產、採購、營運和財務數據的一致性遠高於現有系統環境所能支援的範圍。對於中型企業而言,持續遷移關鍵核心系統也增加了額外的負擔,因為它們內部資源有限,難以並行部署軟體。 FairEnergie GmbH 於 2026 年 6 月決定以基於 SAP S/4HANA Utilities 的雲端平台取代 SAP IS-U,這表明公共產業公司已在投入內部資源進行基礎轉型項目,這些項目將持續到 2027 年。因此,能夠提供 SAP 和 ServiceNow 現成連接器的供應商具有優勢,因為他們可以縮短實施時間,並減少買方需要承擔的客製化整合工作量。

細分市場分析

2025年,德國綠色IT軟體市場中,軟體佔據了76.14%的市場佔有率,成為該領域收入最高的類別。這一地位與企業級碳管理、ESG報告和脫碳規劃工具的許可密切相關,這些工具已在以SAP和微軟為中心的IT環境中得到應用。德國企業傾向於擴展現有平台契約,而不是部署獨立工具,因為這可以減少供應商數量、縮短安全審查週期,並將採購流程控制在已知的商業框架內。這一趨勢有助於現有供應商透過將永續性功能作為擴展功能納入更廣泛的ERP和雲端合約中來留住基本客群。這也意味著,在德國綠色IT軟體市場,軟體收入的成長主要來自對現有系統的利用,而不是透過完全取代新平台來實現的。

預計2026年至2031年,服務業的複合年成長率將達到14.93%。儘管其基數仍然相對較小,但預計它將成為服務產品中成長最快的細分市場。這一成長反映了一個簡單的營運現實:僅靠軟體本身無法產生符合審計要求的ESRS(環境和社會報告準則)輸出,除非圍繞軟體設計相應的管治結構、重要性評估、相關人員工作流程和資料修復措施。大規模組織還需要協助將永續性指標與金融機構、業務地點和供應商之間的關係連結起來,以確保其報告的可靠性。預計到2026年底將普遍推出的新型永續性人工智慧代理將減少日常服務工作,但可能需要合作夥伴公司投入額外的實施工作來配置和管理這些工具。此外,當製造企業採購負責人根據現有的環境管理實務選擇軟體供應商時,那些資料結構與ISO 14001式管理流程一致的供應商更有可能保持更有利的地位。

到2025年,基於雲端的部署將佔德國綠色IT軟體市場的64.17%,而混合部署預計到2031年將以15.02%的複合年成長率成長。雲端交付憑藉其快速部署、便捷的功能更新以及對CSRD和ESRS要求變化的快速響應,仍然是一個極具吸引力的選擇。然而,市場並非簡單地轉向公共雲端模式,因為許多買家仍需要對敏感供應商資訊、排放資料和營運資料的儲存進行更嚴格的控制。調查顯示,73%的德國公司已採用混合IT架構,這印證了混合環境並非過渡階段,而是已成為標準的觀點。與資料主權、NIS-2和BSI C5相關的要求,使得混合部署成為那些既希望獲得軟體速度又不想完全放棄本地控制的組織的理想折衷方案。

混合解決方案的需求也受到中階市場買家行為的驅動。德國中小企業正擴大將永續工作負載遷移到德國或歐盟境內的託管環境中,同時繼續使用公共雲端進行報告、儀表板或外部協作。這種模式對於收集範圍 3 資料非常有效,因為供應商資訊通常具有商業敏感性,企業不願意將其置於完全開放的架構中。在關鍵基礎設施 (KRITIS)相關企業、國防供應鏈和受監管的金融環境中,本地部署仍然發揮著重要作用,因為在這些領域,完全遷移到雲端仍然受到限制。因此,德國綠色 IT 軟體市場更重視那些能夠在清晰管治下跨多個環境遷移資料的供應商,而不是那些只推廣單一託管模式的供應商。未來,互通性、身份驗證支援、無縫整合以及託管規模等因素在採用決策中將變得更加重要。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 德國公司日益沉重的ESG報告負擔

- 能源成本的壓力正在加速軟體主導的最佳化。

- 主要IT用戶的資料中心脫碳計劃

- 追蹤 IT 資產的生命週期以減少範圍 3

- 與企業永續發展報告相關的監管壓力

- 混合工作負載中的人工智慧驅動能源編配

- 市場限制因素

- 與傳統ERP和ITSM系統整合的複雜性。

- 與核心安全和雲端計畫的競爭

- 各業務部門的永續發展數據各不相同。

- 中型企業內部碳計量成熟度較低

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 按解決方案類型

- 碳管理和會計軟體

- ESG報告合規軟體

- 永續性資料管理平台

- 脫碳規劃軟體

- 能源資源最佳化軟體

- 最終用戶

- 資訊科技/通訊

- BFSI

- 製造業

- 能源與公共產業

- 零售博彩

- 政府

- 衛生保健

- 建築和基礎設施

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- IBM Corporation

- Microsoft Corporation

- ServiceNow, Inc.

- Schneider Electric SE

- Siemens AG

- SAP SE

- Salesforce, Inc.

- Oracle Corporation

- ENGIE SA

- Enablon SA

- Wolters Kluwer NV

- Persefoni AI, Inc.

- Plan A

- Sweep SAS

- Envizi(IBM)

- Greenly SAS

- Quentic GmbH

- Sphera Solutions, Inc.

- Diligent Corporation

- Benchmark Gensuite, Inc.

- Dakota Software Corporation

- Microsoft Cloud for Sustainability

- EcoVadis SAS

- Salesforce Net Zero Cloud

- Sustainability Strategy and Roadmap Services

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany green IT software market is expected to grow from USD 1.65 billion in 2025 to USD 1.85 billion in 2026, and reach USD 3.69 billion by 2031, growing at a CAGR of 14.81% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, and More), and End User (IT and Telecom, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Green IT Software Market Trends and Insights

Regulatory Pressure from Corporate Sustainability Reporting

Germany's CSRD transposition path is moving the Germany green IT software market toward a more structured buying cycle, as the first major reporting wave reaches large companies in 2026. The initial group covers around 240 German enterprises with more than 1,000 employees, and the obligation then extends, in later waves, to a much broader base, reaching around 15,000 companies by 2028. The original ESRS framework carried up to 1,100 data points across 82 disclosures, and the EU Omnibus I package approved in December 2025 is reducing that requirement to an estimated 400-500 data points through a delegated revision. That adjustment is not lowering software demand, because companies still need auditable data flows and now want tools that can adapt as the final reporting architecture becomes clearer. Supplier data collection is also drawing many mid-market firms into procurement even when they do not file directly, because first-wave customers still need verified Scope 3 inputs from them. SAP's 2026 Sustainability Control Tower updates show how incumbent vendors are trying to capture this compliance-led demand by expanding ESRS metric coverage and introducing AI-based audit-readiness features.

Rising ESG Reporting Burden across German Enterprises

The German green IT software market is also supported by the fact that Germany enterprises are dealing with multiple reporting frameworks simultaneously, not just one. Large financial institutions face ESG risk disclosures under banking rules, while manufacturers must also handle EU Taxonomy alignment and supply chain due diligence requirements. That overlap is diminishing the usefulness of single-purpose tools and pushing buyers toward platforms that can manage reporting, data governance, and audit preparation from a single operating layer. Plan A built its position on German-language workflows, local regulatory tracking, and live updates for CSRD and ESRS changes, and the company said it has served more than 1,500 DACH enterprises while remaining profitable since 2024. SAP said in May 2026 that new sustainability AI agents, including a Footprint Optimization Agent, would be generally available by the end of 2026 and could reduce scenario simulation time from 1 day to 20 minutes. As reporting fatigue rises, buyers are showing less tolerance for fragmented tools and more interest in integrated platforms that can support CSRD, EU Taxonomy, GRI, and banking-related disclosure needs together.

Integration Complexity with Legacy ERP And ITSM Stacks

Legacy architecture remains a meaningful drag on deployment speed across the Germany green IT software market. Many German enterprises still run SAP ECC, SAP IS-U, or heavily customized sector-specific environments, so green IT platforms often face difficult extraction, mapping, and reconciliation work before they can produce reliable outputs. This problem is becoming sharper because audit-ready sustainability reporting requires asset, procurement, operational, and finance data to align at a much deeper level than many existing system landscapes were built to support. Mittelstand companies are facing an added burden because major core-system migrations are already underway, which reduces internal capacity for parallel software onboarding. FairEnergie GmbH's June 2026 decision to replace SAP IS-U with a cloud-based platform built on SAP S/4HANA Utilities shows how utility companies are already using internal resources on foundational change programs that run well into 2027. Vendors that can offer prebuilt connectors to SAP and ServiceNow therefore have an advantage, as they can shorten implementation timelines and reduce the amount of custom integration work buyers must fund.

Other drivers and restraints analyzed in the detailed report include:

- Energy Cost Pressure Accelerating Software-Led Optimization

- Data Center Decarbonization Programs Across Large IT Users

- Fragmented Sustainability Data Across Business Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 76.14% of the Germany green IT software market share in 2025, making it the leading revenue category in this segment. That position was tied to enterprise licensing for carbon management, ESG reporting, and decarbonization planning tools that were already being added inside SAP- and Microsoft-centered IT estates. German enterprises have often preferred to extend existing platform agreements rather than introduce standalone tools, because that reduces vendor count, shortens security reviews, and keeps procurement inside known commercial structures. This pattern has helped incumbent vendors defend their base, since sustainability functionality can be sold as a feature expansion within broader ERP or cloud contracts. It also means the German green IT software market has seen software revenue build first around installed-system leverage rather than around entirely new platform replacement cycles.

Services are projected to grow at a 14.93% CAGR from 2026 to 2031, making them the faster-moving part of the offering mix even though they remain on a smaller base. That growth reflects a simple operational reality: software alone does not create audit-ready ESRS output when governance structures, materiality assessments, stakeholder workflows, and data remediation still need to be designed around it. Large organizations also need support to map sustainability metrics to financial entities, operational sites, and supplier relationships before reporting can be trusted. New sustainability AI agents, which are expected to become generally available by the end of 2026, may reduce routine service work while creating additional implementation work for partners who configure and govern those tools. Vendors that align their data structures with ISO 14001-style management processes are also likely to stay better positioned when manufacturing buyers screen software providers against existing environmental management practices.

Cloud-based deployment held 64.17% of the Germany green IT software market in 2025, while hybrid deployment is projected to grow at a 15.02% CAGR through 2031. Cloud delivery has remained attractive because it allows faster rollout, easier feature updates, and quicker adjustment when CSRD and ESRS requirements change. At the same time, the market is not moving toward a simple public cloud model, since many buyers still need stronger control over where sensitive supplier, emissions, and operational data is stored. Surveys show that 73% of German enterprises operate hybrid IT architectures, which supports the view that mixed environments are already standard rather than transitional. Requirements tied to data sovereignty, NIS-2, and BSI C5 preferences have therefore made hybrid deployment a practical middle path for organizations that want software speed without fully giving up local control.

Hybrid demand is also being reinforced by buyer behavior in the mid-market. German SMEs are increasingly reshoring sustainability-sensitive workloads to German or EU-hosted environments while still using public cloud layers for reporting, dashboards, or external collaboration. That pattern works well for Scope 3 data collection, because supplier information often carries commercial sensitivity that companies do not want to place into a fully open architecture. On-premise deployment still keeps a role in KRITIS-related enterprises, defense-linked supply chains, and regulated financial settings where full cloud migration remains constrained. For this reason, the Germany green IT software market is rewarding vendors that can move data across several environments with clear governance rather than vendors that push one hosting model only. Over time, interoperability, certification readiness, and smooth integration are likely to matter more in deployment decisions than hosting scale alone

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management Accounting Software

- ESG Reporting Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy Resource Optimization Software

- By End User

- IT Telecom

- BFSI

- Manufacturing

- Energy Utilities

- Retail E-Commerce

- Government

- Healthcare

- Construction Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- SAP SE

- IBM Corporation

- Microsoft Corporation

- ServiceNow, Inc.

- Schneider Electric SE

- Siemens AG

- SAP SE

- Salesforce, Inc.

- Oracle Corporation

- ENGIE SA

- Enablon SA

- Wolters Kluwer N.V.

- Persefoni AI, Inc.

- Plan A

- Sweep SAS

- Envizi (IBM)

- Greenly SAS

- Quentic GmbH

- Sphera Solutions, Inc.

- Diligent Corporation

- Benchmark Gensuite, Inc.

- Dakota Software Corporation

- Microsoft Cloud for Sustainability

- EcoVadis SAS

- Salesforce Net Zero Cloud

- Sustainability Strategy and Roadmap Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ESG Reporting Burden Across German Enterprises

- 4.2.2 Energy Cost Pressure Accelerating Software-Led Optimization

- 4.2.3 Data Center Decarbonization Programs Across Large IT Users

- 4.2.4 IT Asset Lifecycle Tracking for Scope 3 Reduction

- 4.2.5 Regulatory Pressure From Corporate Sustainability Reporting

- 4.2.6 AI-Based Energy Orchestration In Hybrid Workloads

- 4.3 Market Restraints

- 4.3.1 Integration Complexity With Legacy ERP and ITSM Stacks

- 4.3.2 Budget Competition With Core Security and Cloud Programs

- 4.3.3 Fragmented Sustainability Data Across Business Units

- 4.3.4 Limited Internal Carbon Accounting Maturity In Mid-Market Firms

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of New Entrants

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management Accounting Software

- 5.4.2 ESG Reporting Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy Resource Optimization Software

- 5.5 By End User

- 5.5.1 IT Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy Utilities

- 5.5.5 Retail E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare

- 5.5.8 Construction Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 ServiceNow, Inc.

- 6.4.5 Schneider Electric SE

- 6.4.6 Siemens AG

- 6.4.7 SAP SE

- 6.4.8 Salesforce, Inc.

- 6.4.9 Oracle Corporation

- 6.4.10 ENGIE SA

- 6.4.11 Enablon SA

- 6.4.12 Wolters Kluwer N.V.

- 6.4.13 Persefoni AI, Inc.

- 6.4.14 Plan A

- 6.4.15 Sweep SAS

- 6.4.16 Envizi (IBM)

- 6.4.17 Greenly SAS

- 6.4.18 Quentic GmbH

- 6.4.19 Sphera Solutions, Inc.

- 6.4.20 Diligent Corporation

- 6.4.21 Benchmark Gensuite, Inc.

- 6.4.22 Dakota Software Corporation

- 6.4.23 Microsoft Cloud for Sustainability

- 6.4.24 EcoVadis SAS

- 6.4.25 Salesforce Net Zero Cloud

- 6.4.26 Sustainability Strategy and Roadmap Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

南美洲綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)無紙化企業和數位化流程永續性軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Kubernetes:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

南美洲綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)無紙化企業和數位化流程永續性軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Kubernetes:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 雲端應用安全市場:按組件、部署模式、最終用戶產業和企業規模分類-2026-2032年全球市場預測

雲端應用安全市場:按組件、部署模式、最終用戶產業和企業規模分類-2026-2032年全球市場預測 容器和 Kubernetes 安全市場報告:按組件、產品、組織規模、行業垂直領域和地區分類(2026-2034 年)

容器和 Kubernetes 安全市場報告:按組件、產品、組織規模、行業垂直領域和地區分類(2026-2034 年) Kubernetes市場規模、佔有率和成長分析(按組件、產品、組織規模、垂直產業和地區分類)-2026-2033年產業預測

Kubernetes市場規模、佔有率和成長分析(按組件、產品、組織規模、垂直產業和地區分類)-2026-2033年產業預測 雲端應用安全市場規模、佔有率和成長分析(按類型、組件、組織規模、部署類型、垂直產業和地區分類)-2026-2033年產業預測

雲端應用安全市場規模、佔有率和成長分析(按類型、組件、組織規模、部署類型、垂直產業和地區分類)-2026-2033年產業預測 全球 Kubernetes 市場

全球 Kubernetes 市場 2026 年至 2032 年容器和 Kubernetes 安全市場(按產品、組織規模、垂直產業和地區分類)

2026 年至 2032 年容器和 Kubernetes 安全市場(按產品、組織規模、垂直產業和地區分類)