|

市場調查報告書

商品編碼

2073113

開式齒輪潤滑劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Open Gear Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

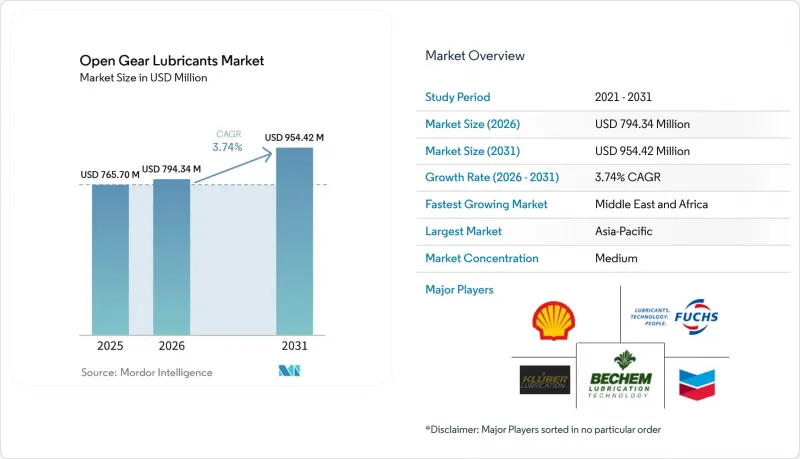

據 Mordor Intelligence 稱,預計開式齒輪潤滑油市場將從 2025 年的 7.657 億美元成長到 2026 年的 7.9434 億美元,到 2031 年達到 9.5442 億美元,2026 年至 2031 年的複合年成長率為 3.74%。

本報告按基礎油(礦物油、合成油、生物基油)、終端用戶產業(採礦、水泥、建築、發電、石油天然氣、船舶及其他)和地區(亞太、北美、歐洲、南美以及中東和非洲)進行細分。市場規模和預測均以美元計價。

全球開式齒輪潤滑油市場趨勢及洞察

採礦業和水泥業擴張導致需求增加

智利、秘魯和印尼銅礦和鐵礦的擴張,以及沙烏地阿拉伯新窯爐的投產,正在推高潤滑油的年消耗量。這些潤滑油對於連續運作的破碎機和迴轉窯至關重要。由於窯爐齒輪故障會導致停產並造成重大損失,因此採購部門目前優先考慮的是鐵姆肯認證的高運作能力,而非潤滑油的初始成本。克魯勃的合成開式齒輪產品透過降低潤滑油消耗量和動作溫度,顯著提高了設備的正常運作時間。此外,集中式噴灑系統可在每次齒輪旋轉時精確噴灑潤滑油,從而最大限度地減少浪費。因此,採購重點已從每公升價格轉向整個生命週期成本。

生物基潤滑劑的廣泛應用

美國環保署 (EPA) 的《船舶意外排放法案》強制要求大型船舶在油與海水接觸點使用環保潤滑劑。預計這項要求將增加對可在指定時間內分解的生物分解產品的需求。嘉實多碳中和的 BioTac OG 潤滑脂已獲得 PAS 2060 認證,代表了生物基潤滑脂的發展方向,它具有高生物分解性,並在四球極壓試驗中展現出卓越的焊接強度。離岸風力發電電場和沿海水泥碼頭正在加速向生物酯類潤滑脂過渡,以應對溢油事故後的法律責任並實現企業永續性。獲得目的地設備製造商 (OEM) 生物基配方認證的供應商正在成為競標評估的首選供應商。隨著經營團隊認知到生命週期碳計量的重要性,即使生物基開式齒輪潤滑油的價格高於傳統的礦物油,它們也有望獲得長期合約。

地緣政治因素導致供應鏈不穩定

霍爾木茲海峽的航運中斷(該海峽是歐洲II類基礎油的重要運輸通道)可能導致短期內調配成本大幅上升。改道至紅海已顯著延長前置作業時間,迫使採用即時生產的水泥廠依賴成本高昂的緊急礦物油儲備。北美調配商正轉向使用國產聚α烯烴作為對沖手段,但向合成基料的過渡需要經過一系列繁瑣的流程,包括實驗室測試和原始設備製造商(OEM)的重新認證。 Ⅱ類基礎油的現貨價格已大幅上漲,給獨立調配商的利潤率帶來了壓力。

細分市場分析

2025年,礦物油佔據了開式齒輪潤滑油市場43.56%的佔有率。這主要得益於亞洲水泥窯對成本的重視,這些地區的買家仍然按桶購買潤滑油,而不是根據設備的使用壽命來購買。預計2026年至2031年,該細分市場將以3.68%的複合年成長率成長。隨著印度和印尼現有設備的投入運作,合成潤滑油正在挑戰礦物油的主導地位。在國際電工委員會(IEC)關於風力發電機機齒輪箱法規的背景下,聚α烯烴和III類混合潤滑油目前在北美市場佔了很大的佔有率。在水泥產業,克魯勃的現場數據顯示,合成潤滑油可以降低油耗和運作溫度,這促使跨國公司將優質潤滑油作為標準配置。生物基酯類潤滑油目前市佔率較小,但成長勢頭強勁,尤其是在需要符合VIDA標準的甲板機械領域。製造商透過混合生物酯和聚α烯烴來拓寬溫度範圍,並有望在亞洲船舶領域開闢新的收入來源。鑑於其技術優勢和監管獎勵,儘管消費成長放緩,但合成潤滑油的以金額為準預計將在本世紀末之前超越礦物油。

用於開式齒輪潤滑油的合成油市場預計將顯著擴張,成為整體市場中成長最快的細分市場。隨著原始設備製造商 (OEM) 推薦的奈米添加劑在窯爐和磨機齒輪箱中日益普及,礦物油面臨著被限制在小眾、價格主導應用領域的威脅。為了應對這項挑戰,供應商正致力於透過將高利潤的合成油與數位化監控服務相結合,來保護其市場佔有率並建立長期服務合約。同時,歐洲 I 類礦物油產能的下降導致供應趨緊,並縮小了與 III 類礦物油的價格差距。這種轉變凸顯了採購部門為何優先考慮總擁有成本 (TCO) 而非單純的發票價格,從而加速了產業向合成油的轉型。

區域分析

到2025年,亞太地區將佔全球銷售額的35.40%。中國強大的重工業基礎和印度不斷擴張的水泥產業正在推動該地區的產業發展趨勢。中石化在天津的擴建預計將提升耐濕開式齒輪產品的供應,這與中石化在印尼的鎳銅冶煉廠運作的時間相吻合。該地區的高水準技術專長體現在日韓兩國的技術如何塑造了國際電工委員會(IEC)齒輪箱標準,以及原始設備製造商(OEM)如何引領低溫聚α烯烴混合物的應用。澳洲鐵礦石開採公司正在轉向自動化噴塗系統,以解決皮爾巴拉偏遠地區的人手不足,這進一步凸顯了該產業向合成解決方案的轉變。

中東和非洲地區是成長最快的地區,預計2026年至2031年複合年成長率將達到3.82%。沙烏地阿拉伯「2030願景」下的基礎設施項目正在推動水泥產量的持續成長。在利雅得,窯爐暴露在極端環境溫度和高磨蝕性砂粒中,因此對不易流失的高黏度合成潤滑油的需求日益成長。南非鉑金產業的復興在粉塵含量高的環境中也面臨類似的挑戰,但集中潤滑系統已被證明能有效顯著減少地下隧道意外運作。在以埃及新建地中海港口為首的北非航運樞紐,碼頭起重機正在採用生物基潤滑脂,以符合國際海事組織(IMO)的污染防治法規。然而,地區政治不穩定有時會推高進口基油的運費,導致買家轉向本地灌裝的合成潤滑油。

儘管北美和歐洲的整體成長率落後於其他地區,但由於嚴格的環境法規,它們對化學產品趨勢有顯著的影響。歐洲開式齒輪潤滑油市場預計將保持溫和成長,但全氟烷基和多氟烷基物質的禁用正迫使產品線進行重大調整。在美國,海上作業者正在逐步淘汰尾軸管中的礦物油,此舉是為了確保根據《船舶意外排放法》獲得鑽井許可證,從而導致對聚α烯烴和酯類等環保型潤滑油的需求增加。英國齒輪協會對國際電工委員會 (IEC) 標準的認可進一步推動了英國和北歐風電產業的需求。同時,南美洲,特別是智利和秘魯,在銅產量擴張的推動下,銷售量正強勁成長。然而,安第斯山脈礦山的物流挑戰推高了集中潤滑系統的價格,這些系統通常從美國和歐洲空運而來。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 採礦業和水泥業擴張導致需求增加

- 生物基潤滑劑的廣泛應用

- 合成基礎油的廣泛應用

- 利用人工智慧驅動的預測性維護減少潤滑油浪費。

- 採用經OEM認證的奈米添加劑配方,延長齒輪壽命。

- 高地礦區向集中式噴淋系統過渡

- 市場限制因素

- 地緣政治因素導致供應鏈不穩定

- 大直徑開式齒輪應用面臨的挑戰

- 影響傳統化學品的 PFAS 新法規

- 發展中地區缺乏高技能潤滑審計人員

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 基礎油

- 礦物油

- 合成油

- 生物基油

- 按最終用戶行業分類

- 礦業

- 水泥

- 建造

- 發電

- 石油和天然氣

- 海上

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Bel-Ray Company LLC

- BP plc

- Carl Bechem GmbH

- Castrol Limited

- Chevron Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil Lubricants

- Idemitsu Kosan Co. Ltd.

- Kluber Lubrication

- Lubrication Engineers Inc.

- Lubriplate Lubricants Company

- Petro-Canada Lubricants

- Petron Corporation

- Phillips 66 Lubricants

- Shell plc

- Sinopec Lubricants

- Specialty Lubricants Corporation

- TotalEnergies

- Valvoline Inc.

- Whitmore Manufacturing LLC.

第7章 市場機會與未來展望

According to Mordor Intelligence, the open gear lubricants market size is expected to increase from USD 765.70 million in 2025 to USD 794.34 million in 2026 and reach USD 954.42 million by 2031, growing at a CAGR of 3.74% over 2026-2031.

This report is Segmented by Base Oil (Mineral Oil, Synthetic Oil, and Bio-Based Oil), End-User Industry (Mining, Cement, Construction, Power Generation, Oil And Gas, Marine, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East, and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Open Gear Lubricants Market Trends and Insights

Rising Demand from Mining and Cement Expansion

Expansions of copper and iron-ore mines in Chile, Peru, and Indonesia, coupled with the introduction of new kilns in Saudi Arabia, are driving up annual lubricant consumption. These lubricants are essential for grinding mills and rotary kilns that operate continuously. Given that failures in kiln gears can halt production and incur substantial costs, procurement teams are now prioritizing high-load Timken ratings over the initial price of lubricants. Synthetic open-gear products from Kluber have reduced lubricant consumption and lowered operating temperatures, leading to noticeable improvements in operational uptime. Additionally, centralized spray systems are minimizing waste by precisely dosing lubricant with each gear rotation. As a result, the focus has shifted from the price per liter to the overall life-cycle cost.

Growth in Bio-Based Lubricants Adoption

The Environmental Protection Agency Vessel Incidental Discharge Act rule mandates that large vessels use environmentally acceptable lubricants at oil-to-sea interfaces. This requirement is expected to drive the demand for biodegradable products that break down within a specified timeframe. Castrol's carbon-neutral BioTac OG, certified to PAS 2060, showcases the evolution of bio-based greases, achieving high biodegradability alongside strong Four-Ball Extreme Pressure weld points. To address spill liabilities and meet corporate sustainability goals, offshore wind farms and coastal cement terminals are increasingly turning to bio-esters. This transition is further bolstered by Europe's OSPAR convention and impending bans on per- and polyfluoroalkyl substances, spurring swift adoption among North Sea marine fleets. Suppliers boasting original equipment manufacturer approvals for bio-based formulations are emerging as preferred vendors in bid assessments. With life-cycle carbon accounting gaining traction in boardrooms, offerings in the bio-based open gear lubricants market are poised to secure long-term contracts, even with a price premium over traditional mineral oils.

Geopolitical Supply-Chain Instability

Disruptions in the Strait of Hormuz, through which a significant portion of Europe's Group II base stocks transit, can lead to a substantial increase in blending costs within a short period. A diversion to the Red Sea extended lead times considerably, compelling just-in-time cement plants to rely on emergency mineral-oil inventories at a higher cost. While North American blenders have turned to domestic sourcing of polyalphaolefin as a hedge, the transition to synthetic stocks requires an extensive process involving laboratory testing and original equipment manufacturer reapproval. Spot prices for Group II oils have risen significantly, squeezing profit margins for independent blenders.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Uptake of Synthetic Base Oils

- AI-Enabled Predictive Maintenance Lowering Lubricant Wastage

- Emerging PFAS Restrictions Affect Legacy Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral oils captured 43.56% of the open gear lubricants market share in 2025, thanks to entrenched use in cost-sensitive Asian cement kilns, where buyers still purchase by the drum rather than by equipment life results. The segment is projected to expand at a 3.68% CAGR during 2026-2031. As legacy assets in India and Indonesia come online, synthetics are challenging this dominance. Polyalphaolefin and Group III blends now account for a significant portion of North American sales, driven by the International Electrotechnical Commission mandate for wind-turbine gearboxes. In the cement sector, Kluber's field data reveals that synthetics reduce consumption and operating temperatures, persuading multinationals to adopt premium grades as the standard. While bio-based esters currently hold a small market share, they are witnessing substantial growth, especially where VIDA compliance is essential for deck machinery. Blenders merging bio-esters with polyalphaolefin to expand the temperature range could tap into new revenue streams in Asia's marine sector. Given the technical advantages and regulatory incentives, synthetics are poised to surpass mineral oils in value terms long before the end of the decade, even if their volumes remain subdued due to lower consumption rates.

The market for synthetic oils in open gear lubricants is projected to expand significantly, marking it as the most rapidly advancing segment in the larger market. With original equipment manufacturer-endorsed nano-additives becoming commonplace in kiln and mill gearboxes, mineral oils face the threat of being confined to niche, price-driven applications. In response, suppliers are pairing high-margin synthetics with digital monitoring services, aiming to safeguard their market share and establish enduring service contracts. Concurrently, as Group I mineral capacities dwindle in Europe, supply tightens, and the price gap to Group III narrows. This shift highlights why procurement teams are now prioritizing total cost of ownership over mere invoice price, hastening the industry's pivot towards synthetics.

Complete Report Scope:

- By Base Oil

- Mineral Oil

- Synthetic Oil

- Bio-based Oil

- By End-user Industry

- Mining

- Cement

- Construction

- Power Generation

- Oil and Gas

- Marine

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific generated 35.40% of global revenue in 2025. China's robust heavy-industry foundation, coupled with India's cement expansion, is steering the region's industrial narrative. Sinopec's expansion in Tianjin is set to boost the supply of humidity-resistant open-gear products, coinciding with the launch of nickel and copper smelters in Indonesia. The region's technical prowess is evident as Japanese and South Korean inputs shape International Electrotechnical Commission gearbox standards, guiding original equipment manufacturers towards adopting low-temperature polyalphaolefin blends. In a bid to address labor shortages at its remote Pilbara sites, Australian iron-ore miners are turning to automatic spray systems, further emphasizing the industry's shift towards synthetic solutions.

The Middle East and Africa is the fastest-growing territory at 3.82% CAGR during 2026-2031. Saudi Vision 2030's infrastructure projects are fueling continuous cement production. In Riyadh, kilns face extreme ambient temperatures and abrasive sand, increasing the demand for high-viscosity synthetics that resist wash-off. South Africa's platinum revival encounters similar high-dust challenges; however, centralized lubrication systems have proven effective in significantly reducing unplanned downtime in underground shafts. North African marine hubs, with Egypt's new Mediterranean ports leading the charge, are adopting bio-based greases for dockside cranes, aligning with International Maritime Organization pollution protocols. Yet, regional political volatility occasionally inflates freight premiums for imported base oils, steering buyers towards locally packaged synthetics.

While North America and Europe may lag in overall growth, they wield significant influence over chemistry trends, largely due to stringent environmental regulations. Europe's open gear lubricants market is expected to grow modestly, but the prohibition of per- and polyfluoroalkyl substances threatens to overhaul product lineups. In the United States, offshore operators are phasing out mineral oils in stern tubes, a move aimed at securing drilling permits under Vessel Incidental Discharge Act regulations, subsequently boosting demand for polyalphaolefin and ester environmentally acceptable lubricants. The British Gear Association's endorsement of International Electrotechnical Commission standards is further propelling wind-sector demand in the United Kingdom and Nordic regions. Meanwhile, South America, particularly Chile and Peru, is witnessing robust volume growth driven by copper expansion. However, logistical challenges in the Andes mines are inflating prices for centralized lubrication systems, which are often flown in from the United States or Europe.

- Bel-Ray Company LLC

- BP p.l.c.

- Carl Bechem GmbH

- Castrol Limited

- Chevron Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil Lubricants

- Idemitsu Kosan Co. Ltd.

- Kluber Lubrication

- Lubrication Engineers Inc.

- Lubriplate Lubricants Company

- Petro-Canada Lubricants

- Petron Corporation

- Phillips 66 Lubricants

- Shell plc

- Sinopec Lubricants

- Specialty Lubricants Corporation

- TotalEnergies

- Valvoline Inc.

- Whitmore Manufacturing LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from mining and cement expansion

- 4.2.2 Growth in bio-based lubricants adoption

- 4.2.3 Increasing uptake of synthetic base oils

- 4.2.4 AI-enabled predictive maintenance lowering lubricant wastage

- 4.2.5 OEM-approved nano-additive packages extending gear life

- 4.2.6 Shift toward centralized spray systems in high-altitude mines

- 4.3 Market Restraints

- 4.3.1 Geopolitical supply-chain instability

- 4.3.2 Application difficulties with large-diameter open gears

- 4.3.3 Emerging PFAS restrictions affecting legacy chemistries

- 4.3.4 Skill shortage for advanced lubrication audits in developing regions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Base Oil

- 5.1.1 Mineral Oil

- 5.1.2 Synthetic Oil

- 5.1.3 Bio-based Oil

- 5.2 By End-user Industry

- 5.2.1 Mining

- 5.2.2 Cement

- 5.2.3 Construction

- 5.2.4 Power Generation

- 5.2.5 Oil and Gas

- 5.2.6 Marine

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Nordic Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Bel-Ray Company LLC

- 6.4.2 BP p.l.c.

- 6.4.3 Carl Bechem GmbH

- 6.4.4 Castrol Limited

- 6.4.5 Chevron Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Gulf Oil Lubricants

- 6.4.9 Idemitsu Kosan Co. Ltd.

- 6.4.10 Kluber Lubrication

- 6.4.11 Lubrication Engineers Inc.

- 6.4.12 Lubriplate Lubricants Company

- 6.4.13 Petro-Canada Lubricants

- 6.4.14 Petron Corporation

- 6.4.15 Phillips 66 Lubricants

- 6.4.16 Shell plc

- 6.4.17 Sinopec Lubricants

- 6.4.18 Specialty Lubricants Corporation

- 6.4.19 TotalEnergies

- 6.4.20 Valvoline Inc.

- 6.4.21 Whitmore Manufacturing LLC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Subsidised Cool Roofs for Low-income Urban Housing

潤滑油和潤滑脂市場預測至2034年-按產品類型、基礎油、增稠劑類型、應用、最終用戶、分銷管道和地區分類的全球分析

潤滑油和潤滑脂市場預測至2034年-按產品類型、基礎油、增稠劑類型、應用、最終用戶、分銷管道和地區分類的全球分析 菲律賓潤滑油市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

菲律賓潤滑油市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 特種潤滑油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

特種潤滑油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 鑽井潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、功能和地區分類-2026-2033年產業預測

鑽井潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、功能和地區分類-2026-2033年產業預測 海上潤滑油市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)機器人潤滑劑市場預測至2034年—按產品類型、潤滑劑類型、應用、最終用戶和地區分類的全球分析德國潤滑油市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

海上潤滑油市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)機器人潤滑劑市場預測至2034年—按產品類型、潤滑劑類型、應用、最終用戶和地區分類的全球分析德國潤滑油市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 拉絲潤滑劑市場:2026-2032年全球市場預測(依產品類型、添加劑類型、線材類型、應用、終端用戶產業和銷售管道分類)

拉絲潤滑劑市場:2026-2032年全球市場預測(依產品類型、添加劑類型、線材類型、應用、終端用戶產業和銷售管道分類) 潤滑油市場:依產品類型、基礎油、終端用戶產業及地區分類(2026-2034 年)

潤滑油市場:依產品類型、基礎油、終端用戶產業及地區分類(2026-2034 年)