|

市場調查報告書

商品編碼

2072553

菲律賓潤滑油市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Philippines Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

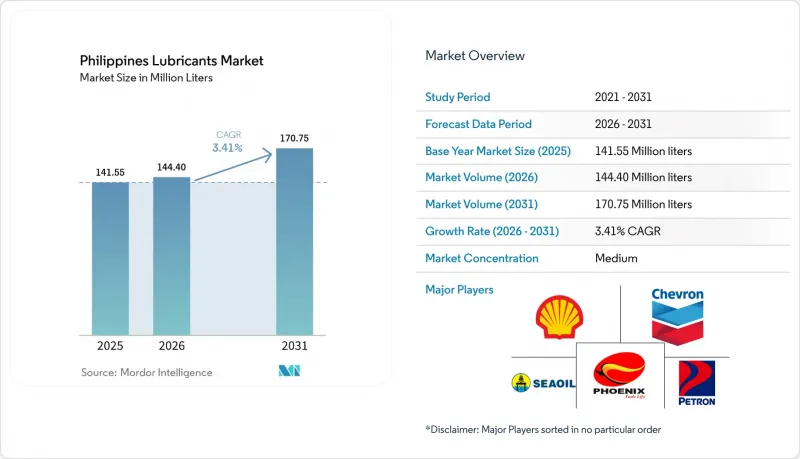

據 Mordor Intelligence 稱,菲律賓潤滑油市場在 2025 年的價值為 1.4155 億公升,預計到 2031 年將達到 1.7075 億公升,而 2026 年為 1.444 億公升,在預測期(2026-2031 年)複合年成長率為 3.41%。

本報告按產品類型(汽車機油、工業引擎油、潤滑脂、金屬加工液、渦輪機油及其他)、終端用戶產業(汽車、船舶、航太、重型機械、工業)及基礎油類型(礦物油基潤滑油、合成潤滑油、半合成潤滑油及其他)進行分類。市場預測以體積(公升)為單位。

菲律賓潤滑油市場趨勢與洞察

增加大型企劃(建設更好、更多)

2024年,菲律賓政府支出1.545兆披索(約266億美元),佔國內生產毛額(GDP)的5.8%,用於支持大規模公路、鐵路和橋樑的建設。這確保了挖土機、起重機和混凝土攪拌機等設備能夠以高強度的運作週期持續運作。設備所有者正在縮短換油週期,從而增加了對高鋅液壓油和極壓潤滑脂的需求。諸如巴丹-甲米地大橋和馬尼拉地鐵等項目需要數千台重型機械,這些機械依賴II類基礎油混合物來減少煙塵排放。然而,由於選舉前資本支出的暫停,2025年前三個季度的支出佔GDP的比例下降至4.2%,潤滑油訂單也出現了顯著的季度波動。擁有跨區域倉儲網路的供應商,特別是殼牌的10個倉庫和Petron的21000個銷售網點,在靈活調整庫存方面具有得天獨厚的優勢。此外,與新建鐵路相關的發電工程也推高了對渦輪機油的需求,從而增強了高階市場。

工業數位化正在推動對預測性維護潤滑油的需求。

政府的「工業4.0」計畫和先進製造中心正在推動配備感測器的機械設備的應用,促使企業更傾向於使用長壽命合成油壓油。儘管在2024年只有14.9%的工廠實現了物聯網賦能的維護,但電子和金屬加工行業的領先企業已經開始指定使用經OEM已通過核准、在ASTM D943測試中使用壽命超過10,000小時的無鋅液壓油。 「雪佛龍Clarity」及類似產品價格較高,通常包含油品質分析服務。由於中小型製造商仍傾向使用礦物油基AW 68液壓油,殼牌等供應商正在部署移動式油品質分析車,以促進客戶向合成油市場提升銷售。這種經營模式依賴於增加技術人員和擴大庫存。

電動車和混合動力汽車的廣泛應用

在第11697號共和國法令免除進口關稅和增值稅的推動下,電動車註冊量從2023年的13,000輛激增至2024年中期的21,000輛,政府的目標是到2040年電動車銷量佔比達到50%。以Meralco、Shell Recharge和AC Energy為核心的充電站數量在2024年超過了800個。混合動力汽車仍使用機油,但其用量僅為內燃機車的60-70%左右。而純電動車則無需機油。供應商正透過推出專用絕緣冷卻液來規避風險,但預計這一轉變將使菲律賓潤滑油市場的複合年成長率下降0.6個百分點。

細分市場分析

到2025年,汽車引擎機油的銷售量將佔總銷售量的33.78%,但隨著混合動力汽車換油週期的延長,其成長曲線正逐漸趨於平緩。變速箱油受惠於乘用車自排變速箱的普及,預計到2024年將佔總銷售量的48%。潤滑脂、金屬加工油、渦輪機油和變壓器油仍屬於小眾市場,但利潤率高,促使供應商加快高附加價值工業混合油轉型。在菲律賓潤滑油市場,預計到2031年,工業機油市場的成長速度將超過其他任何產品類別。受29,853兆瓦裝置容量和24小時運作,工業機油的複合年成長率預計將達到3.15%,超過汽車級潤滑油。

中小企業必須在銷量大、利潤低、易受假冒仿冒品的汽車潤滑油,和銷量小、規格高、需要技術支援的工業混合油之間做出選擇。 SEAOIL 的策略兼顧兩者,利用其 700 多個銷售點來刺激零售需求,同時銷售用於壓榨廠的 ISO VG 150-320 齒輪油。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大型企劃增加(建設更好、更多)

- 工業數位化正在推動對預測性維護潤滑油的需求。

- 叫車服務和摩托車的快速成長推高了對高溫四行程機油的需求。

- OEM 推薦的低黏度合成油,以及因延長保固而增加的銷售量。

- 透過電子商務進行的即時銷售以及 QuickLubBay 的擴張正在增加零售通路。

- 市場限制因素

- 電動車和混合動力汽車的廣泛應用

- 假冒劣質潤滑劑的氾濫

- 與廢油循環經濟相關的合規成本增加

- 價值鏈分析

- 法律規範

- 終端用戶趨勢

- 汽車產業

- 製造業

- 發電業

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 汽車引擎油

- 工業機油

- 變速箱油

- 齒輪油

- 煞車油

- 油壓

- 潤滑脂

- 加工油(包括橡膠加工油和白油)

- 金屬加工液

- 渦輪機油

- 變壓器油

- 其他

- 按最終用戶行業分類

- 車

- 搭乘用車

- 商用車輛

- 摩托車

- 船

- 航太

- 重型機械

- 建造

- 礦業

- 農業

- 工業的

- 發電

- 冶金與金屬加工

- 紡織品

- 石油和天然氣

- 其他終端用戶產業

- 車

- 依基礎油類型

- 礦物油性潤滑劑

- 合成潤滑油

- 半合成潤滑油

- 生物性潤滑劑

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率**(%)/排名分析

- 公司簡介

- BP plc

- Chevron Corporation

- China Petroleum & Chemical Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil International

- Idemitsu Kosan(ENEOS)

- Liqui Moly

- Motul

- Petron Corporation

- PETRONAS Lubricant International

- Phoenix Petroleum

- PTT Lubricants

- Rainchem International Inc.

- Repsol

- Saudi Arabian Oil Co.

- SEAOIL Philippines, Inc.

- Shell plc

- TotalEnergies

第7章 市場機會與未來展望

第8章:執行長面臨的關鍵策略挑戰

According to Mordor Intelligence, the philippines lubricants market size was valued at 141.55 million liters in 2025 and is estimated to grow from 144.40 million liters in 2026 to reach 170.75 million liters by 2031, at a CAGR of 3.41% during the forecast period (2026-2031).

This report is Segmented by Product Type (Automotive Engine Oil, Industrial Engine Oil, Greases, Metalworking Fluids, Turbine Oil, and More), End-User Industry (Automotive, Marine, Aerospace, Heavy Equipment, and Industrial), and Base Stock Type (Mineral Oil-Based Lubricants, Synthetic Lubricants, Semi-Synthetic Lubricants, and More). The Market Forecasts are Provided in Terms of Volume (liters).

Philippines Lubricants Market Trends and Insights

Increasing Construction Mega-Projects (Build-Better-More)

The PHP 1.545 trillion (USD 26.6 billion) outlay in 2024, equal to 5.8% of GDP, underwrites large road, rail, and bridge builds that keep excavators, cranes, and concrete mixers running in punishing duty cycles. Equipment owners shorten drain intervals, inflating demand for high-zinc hydraulic fluids and extreme-pressure greases. Projects such as the Bataan-Cavite Interlink Bridge and Metro Manila Subway require thousands of heavy machines that rely on Group II base-oil blends for soot control. Yet capital-outlay pauses before elections pared spending to 4.2% of GDP in Q1-Q3 2025, swinging lubricant orders sharply from quarter to quarter. Suppliers with multi-regional depots, notably Shell's 10 warehouses and Petron's 21,000-outlet network, are best placed to flex inventories. Power projects tied to new rail lines also lift turbine-oil pull-through, reinforcing the premium segment.

Industrial Digitalization Boosting Predictive-Maintenance Grade Lubricants

Government Industry 4.0 programs and the Advanced Manufacturing Center spur adoption of sensor-equipped machinery that favors longer-life synthetic hydraulics. Only 14.9% of factories had deployed IoT maintenance by 2024, but early movers in electronics and metalworking already specify OEM-approved zinc-free oils rated beyond 10,000 hours in ASTM D943 testing. Chevron Clarity and equivalents command sizeable premiums and often bundle oil-analysis services. Small and medium manufacturers still default to mineral-based AW 68 fluids, so vendors such as Shell push mobile oil-analysis vans to up-sell synthetics, a model that hinges on scaling technical staff as much as stock volume.

Growing Penetration of Electric and Hybrid Vehicles

EV registrations jumped from 13,000 in 2023 to 21,000 by mid-2024 on the back of import-duty and VAT exemptions under RA 11697, and the government targets a 50% EV sales mix by 2040. Charging stations surpassed 800 sites in 2024, anchored by Meralco, Shell Recharge, and AC Energy. Hybrids still use engine oil but at roughly 60-70% of internal-combustion volume; full battery EVs eliminate it. Suppliers hedge by launching specialized dielectric-cooling fluids, yet the transition is expected to shave 0.6 percentage points off the Philippines lubricants market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Ride-Hailing and Motorcycle Fleets Demanding High-Temperature 4T Oils

- OEM-Backed Low-Viscosity Synthetic Oils with Extended-Warranty Pull-Through

- Proliferation of Counterfeit/Adulterated Lubricants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive Engine Oil, while still accounting for 33.78% of 2025 volume, faces a gradually flattening curve as hybrids lengthen drain intervals. Transmission fluids benefit from automatic-transmission uptake in passenger cars, now 48% of 2024 sales. Greases, metalworking, turbine, and transformer oils remain niche but margin-rich pockets, reinforcing supplier moves toward value-added industrial blends. The Philippines lubricants market size for Industrial Engine Oil is projected to grow faster than any other product family through 2031. Industrial Engine Oil is poised to outpace automotive grades at a 3.15% CAGR, fueled by 29,853 MW of installed power capacity and around-the-clock genset operations that mandate high-soot-load formulations.

Smaller players must pick sides: high-volume, low-margin automotive oils vulnerable to counterfeits, or low-volume, high-spec industrial blends that require technical support. SEAOIL's strategy spans both, leveraging 700+ stations for retail pull while marketing ISO VG 150-320 gear oils to crushing plants.

Complete Report Scope:

- By Product Type

- Automotive Engine Oil

- Industrial Engine Oil

- Transmission Fluids

- Gear Oil

- Brake Fluids

- Hydraulic Fluids

- Greases

- Process Oil (Including Rubber Process Oil and White Oil)

- Metalworking Fluids

- Turbine Oil

- Transformer Oil

- Other Product Types

- By End-user Industry

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Two-Wheelers

- Marine

- Aerospace

- Heavy Equipment

- Construction

- Mining

- Agriculture

- Industrial

- Power Generation

- Metallurgy and Metalworking

- Textiles

- Oil and Gas

- Other End-Use Industries

- Automotive

- By Base Stock Type

- Mineral Oil-Based Lubricants

- Synthetic Lubricants

- Semi-Synthetic Lubricants

- Bio-Based Lubricants

List of Companies Covered in this Report:

- BP plc

- Chevron Corporation

- China Petroleum & Chemical Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil International

- Idemitsu Kosan (ENEOS)

- Liqui Moly

- Motul

- Petron Corporation

- PETRONAS Lubricant International

- Phoenix Petroleum

- PTT Lubricants

- Rainchem International Inc.

- Repsol

- Saudi Arabian Oil Co.

- SEAOIL Philippines, Inc.

- Shell plc

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing construction mega-projects (Build-Better-More)

- 4.2.2 Industrial digitalization boosting predictive-maintenance grade lubricants

- 4.2.3 Rapid growth of ride-hailing and motorcycle fleets demanding high-temperature 4T oils

- 4.2.4 OEM-backed low-viscosity synthetic oils with extended-warranty pull-through

- 4.2.5 E-commerce live-selling and quick-lube bay expansion widening retail access

- 4.3 Market Restraints

- 4.3.1 Growing penetration of electric and hybrid vehicles

- 4.3.2 Proliferation of counterfeit/adulterated lubricants

- 4.3.3 Tightening used-oil circular-economy compliance costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Framework

- 4.6 End-User Trends

- 4.6.1 Automotive Industry

- 4.6.2 Manufacturing Industry

- 4.6.3 Power Generation Industry

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Automotive Engine Oil

- 5.1.2 Industrial Engine Oil

- 5.1.3 Transmission Fluids

- 5.1.4 Gear Oil

- 5.1.5 Brake Fluids

- 5.1.6 Hydraulic Fluids

- 5.1.7 Greases

- 5.1.8 Process Oil (Including Rubber Process Oil and White Oil)

- 5.1.9 Metalworking Fluids

- 5.1.10 Turbine Oil

- 5.1.11 Transformer Oil

- 5.1.12 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.1.1 Passenger Vehicles

- 5.2.1.2 Commercial Vehicles

- 5.2.1.3 Two-Wheelers

- 5.2.2 Marine

- 5.2.3 Aerospace

- 5.2.4 Heavy Equipment

- 5.2.4.1 Construction

- 5.2.4.2 Mining

- 5.2.4.3 Agriculture

- 5.2.5 Industrial

- 5.2.5.1 Power Generation

- 5.2.5.2 Metallurgy and Metalworking

- 5.2.5.3 Textiles

- 5.2.5.4 Oil and Gas

- 5.2.5.5 Other End-Use Industries

- 5.2.1 Automotive

- 5.3 By Base Stock Type

- 5.3.1 Mineral Oil-Based Lubricants

- 5.3.2 Synthetic Lubricants

- 5.3.3 Semi-Synthetic Lubricants

- 5.3.4 Bio-Based Lubricants

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 BP plc

- 6.4.2 Chevron Corporation

- 6.4.3 China Petroleum & Chemical Corporation

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Gulf Oil International

- 6.4.7 Idemitsu Kosan (ENEOS)

- 6.4.8 Liqui Moly

- 6.4.9 Motul

- 6.4.10 Petron Corporation

- 6.4.11 PETRONAS Lubricant International

- 6.4.12 Phoenix Petroleum

- 6.4.13 PTT Lubricants

- 6.4.14 Rainchem International Inc.

- 6.4.15 Repsol

- 6.4.16 Saudi Arabian Oil Co.

- 6.4.17 SEAOIL Philippines, Inc.

- 6.4.18 Shell plc

- 6.4.19 TotalEnergies

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs

開式齒輪潤滑劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

開式齒輪潤滑劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 潤滑油和潤滑脂市場預測至2034年-按產品類型、基礎油、增稠劑類型、應用、最終用戶、分銷管道和地區分類的全球分析

潤滑油和潤滑脂市場預測至2034年-按產品類型、基礎油、增稠劑類型、應用、最終用戶、分銷管道和地區分類的全球分析 特種潤滑油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年

特種潤滑油市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、最終用戶、地區和競爭格局分類,2021-2031年 鑽井潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、功能和地區分類-2026-2033年產業預測

鑽井潤滑劑市場規模、佔有率和成長分析:按產品類型、應用、功能和地區分類-2026-2033年產業預測 海上潤滑油市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)機器人潤滑劑市場預測至2034年—按產品類型、潤滑劑類型、應用、最終用戶和地區分類的全球分析德國潤滑油市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

海上潤滑油市場規模、佔有率和趨勢分析報告:按應用、最終用途、地區和細分市場分類(2026-2033 年)機器人潤滑劑市場預測至2034年—按產品類型、潤滑劑類型、應用、最終用戶和地區分類的全球分析德國潤滑油市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲潤滑油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 拉絲潤滑劑市場:2026-2032年全球市場預測(依產品類型、添加劑類型、線材類型、應用、終端用戶產業和銷售管道分類)

拉絲潤滑劑市場:2026-2032年全球市場預測(依產品類型、添加劑類型、線材類型、應用、終端用戶產業和銷售管道分類) 潤滑油市場:依產品類型、基礎油、終端用戶產業及地區分類(2026-2034 年)

潤滑油市場:依產品類型、基礎油、終端用戶產業及地區分類(2026-2034 年)